Revenue can be up, orders can be strong, and you can still feel broke on Thursday afternoon.

That usually shows up the same way. Payroll is due. A large customer still hasn’t paid. Inventory is sitting on shelves or in a warehouse. A supplier wants faster payment than your customers give you. On paper, the business looks healthy. In the bank account, it feels fragile.

That gap is where working capital for businesses stops being an accounting term and starts becoming an operating discipline. If you run a company in the $20 million to $50 million range, you already know the pain. Growth creates pressure before it creates comfort. More sales often mean more receivables, more inventory, more labor, and more timing risk.

The upside is real. In 2025, U.S. companies realized a potential $1.7 trillion in working capital through optimized cash conversion cycles, and top performers reached a 37-day cash conversion cycle, according to The Hackett Group’s 2025 working capital survey. That matters because cash discipline doesn’t just protect you in a tight month. It gives you room to buy better, negotiate harder, and grow without financing every operational mistake.

Table of Contents

- Your Business Is Growing But Cash Is Tight

- What Is Working Capital Really

- How to Measure Your Working Capital Health

- Diagnosing Your Business Cash Flow Gaps

- A Practical Comparison of Working Capital Loans

- How to Choose and Secure the Right Funding

- From Cash-Strapped to Capital-Confident

Your Business Is Growing But Cash Is Tight

A business can be busy and cash-starved at the same time. That’s one of the first hard lessons owners learn when growth accelerates.

The usual pattern is simple. You hire ahead of demand, place bigger inventory orders, take on larger jobs, and give customers terms to win business. Then cash leaves your account long before it returns. Profit may exist. Liquidity doesn’t.

That’s why I treat working capital as fuel, not as a line item. If the fuel line is restricted, the engine may still run for a while, but every turn gets riskier. Owners often respond by chasing revenue harder, which can make the strain worse if collections, inventory planning, and payment timing stay sloppy.

Profit doesn’t pay this week’s bills

A profitable P&L won’t cover payroll if your receivables are aging. Strong margins won’t help if you bought too much stock too early. And a packed sales pipeline won’t calm your suppliers if payment terms are shorter than your collection cycle.

Practical rule: If sales growth makes cash tighter every month, you likely have a working capital problem, not a sales problem.

The businesses that stay steady in rough stretches aren’t always the ones with the highest growth rate. They’re the ones that understand where cash gets trapped and how to release it before they reach for outside funding.

Tight cash isn’t always a crisis

Sometimes the issue is healthy strain. You’re growing, customers are ordering, and the business needs a bridge. Sometimes it’s a symptom of poor controls. Late invoices, weak purchasing discipline, and unplanned vendor payments create avoidable pressure.

The distinction matters. If you know which one you have, you can fix the root problem instead of layering debt onto a process failure.

What Is Working Capital Really

Working capital is the cash cushion that keeps operations moving between spending money and collecting money. It’s the amount tied up in the everyday motion of the business.

The clean formula is straightforward. Current assets include cash, accounts receivable, and inventory. Current liabilities include accounts payable, short-term debt, and other obligations due soon. The difference between those two buckets is your working capital position.

Think of it as your operating bloodstream

Cash is the oxygen. Receivables are cash that hasn’t reached the bank yet. Inventory is cash sitting in product form. Payables are obligations you haven’t paid yet. If those flows stay balanced, the business moves smoothly. If one area backs up, pressure builds somewhere else.

A lot of owners focus only on the amount of cash in the account. That’s like checking your pulse once and deciding you understand your health. The better question is how cash moves through the company, where it slows down, and how long it stays trapped.

The components that matter most

Here’s the practical way to look at it:

- Cash on hand keeps you flexible. It covers payroll, rent, urgent buys, and surprises.

- Accounts receivable represent earned revenue that hasn’t become usable cash yet.

- Inventory supports sales, but excess inventory acts like cash locked in a storeroom.

- Accounts payable can help preserve cash if terms are managed well.

- Short-term debt can support operations, but it can also crowd out flexibility if repayments hit before collections do.

Working capital isn’t about having the most cash. It’s about having cash available at the right time.

That timing point is where many businesses get into trouble. A company may carry solid assets and still struggle because too much of that value is tied up in receivables or inventory. Another company may look leaner on paper but operate better because its cash turns quickly.

Why owners misread it

Owners often assume cash pressure means they need more financing. Sometimes they do. But often they need cleaner invoicing, firmer collections, tighter purchasing, or better supplier terms.

Good working capital management doesn’t mean hoarding cash. It means shortening the distance between spending and collecting. When you do that well, growth becomes easier to finance because operations start funding more of themselves.

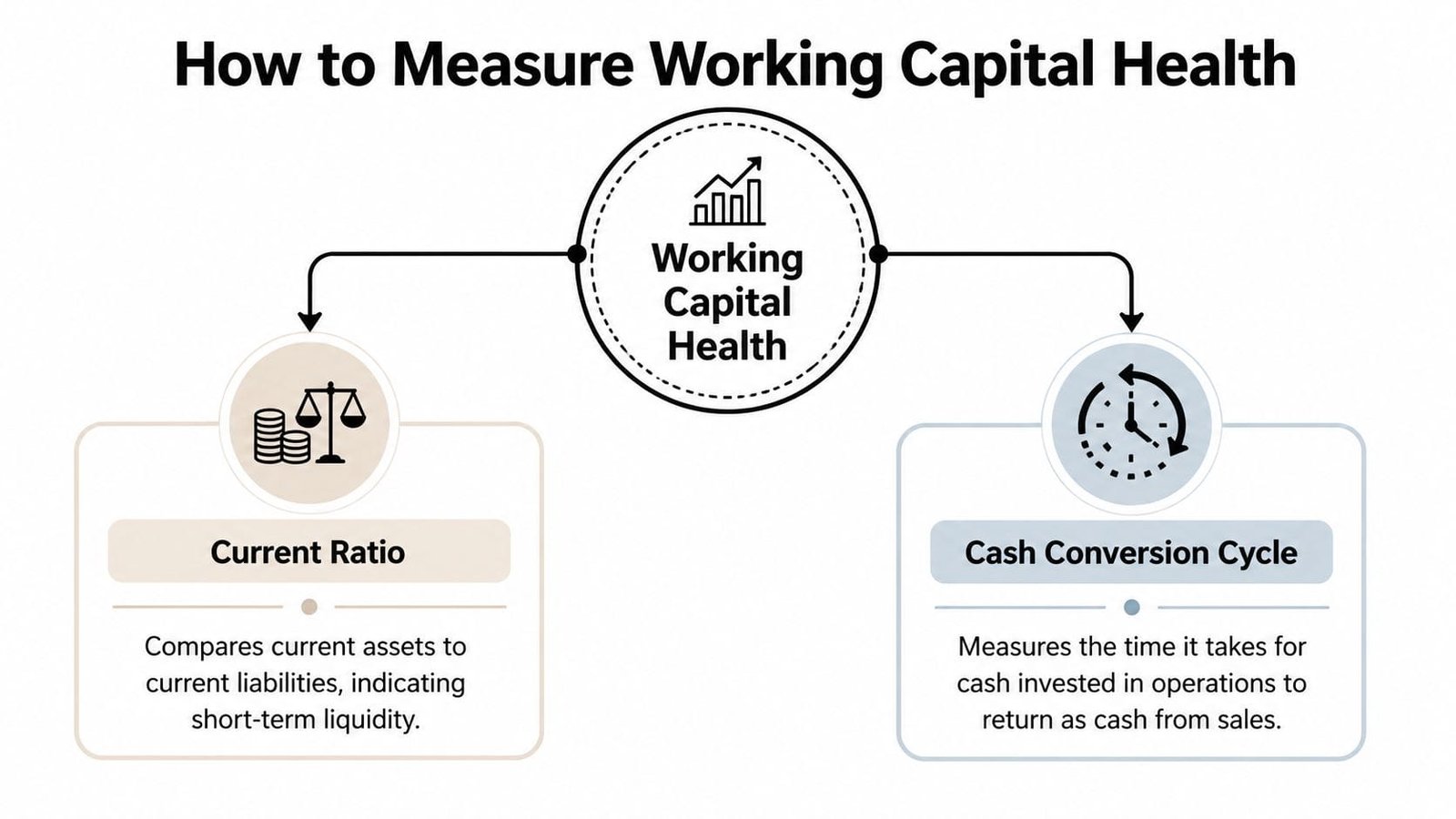

How to Measure Your Working Capital Health

If you want control, start with a few numbers you can review every month. Not fifty numbers. A few. The two I care about first are your current ratio and your cash conversion cycle.

Start with liquidity

Your current ratio tells you whether near-term assets can cover near-term obligations.

Formula: Current Assets ÷ Current Liabilities

For a hypothetical $25 million business, imagine this balance sheet snapshot:

| Item | Amount |

|---|---|

| Cash | $800,000 |

| Accounts receivable | $3,000,000 |

| Inventory | $2,200,000 |

| Total current assets | $6,000,000 |

| Accounts payable | $2,400,000 |

| Short-term debt and other current liabilities | $1,100,000 |

| Total current liabilities | $3,500,000 |

Current ratio = $6,000,000 ÷ $3,500,000 = 1.71

That means the business has $1.71 of current assets for every $1 of current liabilities. In practice, many operators like to see a current ratio in a generally healthy middle range, often around 1.5 to 2.0. Too low can signal strain. Too high can also mean capital is sitting idle or trapped.

For a deeper look at how lenders read this metric, see this guide on healthy working capital ratios and loan approval.

Then measure the cash cycle

The current ratio gives you a static picture. The cash conversion cycle, or CCC, tells you how long cash stays tied up in operations.

Formula: DSO + DIO – DPO

- DSO is Days Sales Outstanding. How long customers take to pay.

- DIO is Days Inventory Outstanding. How long inventory sits before it sells.

- DPO is Days Payables Outstanding. How long you take to pay suppliers.

Let’s use the same hypothetical $25 million business:

- DSO = 52 days

- DIO = 41 days

- DPO = 36 days

CCC = 52 + 41 – 36 = 57 days

That means cash invested in operations is tied up for 57 days before it comes back through collections.

What the numbers mean in practice

This metric matters because even a modest improvement can release serious cash. For firms with $20 million to $50 million in revenue, a 10-day reduction in CCC can free up between $547,000 and $913,000 in cash, according to Planr’s operational efficiency analysis.

That’s why I push owners to stop treating CCC like a finance-only metric. It’s an operating metric. Sales affects DSO. Purchasing affects DIO. Procurement and vendor management affect DPO. Everyone touches it.

A few practical reads:

- A decent current ratio with a long CCC means liquidity may look fine today, but cash is still moving too slowly.

- A weak current ratio with a short CCC can be manageable if collections are consistent and inventory is lean.

- A long CCC over time usually means one of three things is happening: customers pay slowly, inventory sits too long, or suppliers get paid too quickly.

If you only watch the bank balance, you’ll react late. If you watch the cycle, you’ll see the squeeze coming.

Track both numbers monthly. Weekly is even better when growth, seasonality, or supply chain variability is putting pressure on cash.

Diagnosing Your Business Cash Flow Gaps

Once you know your ratios and cycle, the next step is diagnosis. Don’t jump straight to a loan product. Start by naming the exact problem.

A high cash burn from payroll and rent feels the same in the bank account as a slow collections problem. They are not the same issue. One may call for financing. The other may call for better discipline.

When receivables are the problem

If your DSO is the main culprit, cash is getting stuck after the sale. Common causes include slow invoicing, weak follow-up, unclear customer terms, billing disputes, or a sales team that pushes volume without respecting credit discipline.

For a business with $5 million in revenue, reducing DSO from 60 to 45 days frees up over $200,000 in working capital, based on this fractional CFO scenario guide. The lesson is simple. Collections work can create cash faster than many financing products.

Signs this is your issue:

- Invoices go out late after work is completed or goods are delivered.

- Aging reports keep growing but no one owns collection calls.

- Big customers pay on their own schedule because your terms aren’t enforced.

- Disputes sit unresolved and freeze payment.

If this sounds familiar, build a tighter cash flow forecast that supports your loan strategy before you borrow. It will show whether the gap is temporary or structural.

When inventory is eating your cash

Inventory problems are quieter. You don’t notice them because the product looks like value. But slow-moving inventory can be one of the most expensive forms of cash leakage.

The pattern usually looks like this: buying teams order for certainty, sales forecasts are too optimistic, or product mix gets bloated. Then cash sits in SKUs that don’t turn fast enough.

Here’s the operational giveaway:

- Fast sellers stock out, while slow sellers pile up.

- Purchasing decisions are made in bulk because unit costs look attractive.

- Warehouse value rises, but sell-through doesn’t keep pace.

A financing product can help you bridge a seasonal build or a strategic buy. It won’t fix poor replenishment logic.

This short video gives a useful overview of how owners think through cash flow pressure before choosing funding:

When payables are too short for your business model

Sometimes the business is sound, but vendor terms don’t match how cash comes in. Restaurants, retail, distribution, and service businesses often face this mismatch. You may need to pay suppliers quickly while customers pay later, or demand may rise before cash receipts catch up.

That shows up as a short DPO relative to your collection and inventory cycle. In plain English, cash leaves too soon.

A funding product should match the asset or timing gap you’re financing. Borrow short for short needs. Use receivables-based tools for receivables problems.

That diagnosis-to-solution mapping is where owners save themselves a lot of pain. When the diagnosis is wrong, the financing choice usually is too.

A Practical Comparison of Working Capital Loans

Not all working capital financing solves the same problem. A line of credit, an invoice facility, and a merchant cash advance may all put cash in the account, but they behave very differently once repayment starts.

Working Capital Financing Options at a Glance

| Financing Option | Best For | Funding Speed | Cost/Structure |

|---|---|---|---|

| Business line of credit | Seasonal swings, uneven receivables, recurring short-term needs | Often faster than bank term debt once approved | Revolving access. You draw what you need and pay based on the balance used |

| Invoice financing or factoring | High DSO, large receivables balances, slow-paying customers | Can be quick when invoices are verifiable | Structured around receivables. Advance is tied to unpaid invoices |

| Merchant cash advance | Card-heavy businesses needing speed and willing to trade cost for access | Usually very fast | Repayment is tied to sales activity or fixed remittances, which can pressure margins |

| Short-term loan | One-time cash gap, inventory buy, urgent operational need with clear payoff window | Typically faster than traditional bank loans | Fixed amount with short repayment term and frequent payments in many cases |

| SBA working capital option such as CAPLines | Businesses that qualify and want structured working capital support | Usually slower due to documentation and underwriting depth | More formal process. Often better suited when timing is less urgent and documentation is strong |

The mechanics matter more than the label. Owners get into trouble when they choose the fastest product instead of the most appropriate one.

For a side-by-side breakdown of several quick-capital products, this comparison of short-term loans, MCA, and invoice factoring is worth reading.

Match the product to the problem

Here’s how I’d map common diagnoses to likely solutions.

If receivables are slow but your customers are creditworthy, invoice financing often makes sense. You’re funding against a specific asset that already exists. That’s cleaner than using a generic high-cost product to cover a collections lag.

If your business deals with recurring volatility, a line of credit usually fits better. It’s a tool, not a one-time event. You can draw, repay, and redraw as timing shifts through the year.

If you need to buy inventory for a short window with a visible payback cycle, a short-term loan may be enough. The key is having confidence in when that cash returns. If the inventory takes longer to convert than expected, a short repayment schedule can become a problem fast.

If you process a lot of card sales and need speed above all else, an MCA can be an option. But I’d treat it carefully. It solves access. It does not solve economics. If your gross margin is already tight, daily or frequent remittances can crowd out breathing room.

If your records are strong and the need is large enough to justify more paperwork, an SBA-oriented working capital facility can be a solid fit. It tends to reward businesses that can document the use of funds clearly and wait through a more formal process.

One practical note. A fintech-enabled platform such as Business Loan Warrior can help owners check pre-approval, connect bank data, and compare options like lines of credit, short-term financing, invoice financing, SBA processing, and MCA products in one workflow. That’s useful when speed matters, but the product choice still needs to follow the diagnosis.

The right loan feels boring after funding. It fits the cycle, repayment is predictable, and it doesn’t force bad operating decisions.

That’s the standard to use.

How to Choose and Secure the Right Funding

Choosing the right funding starts with honesty. Not optimism. Not lender marketing. Not the amount you wish you needed. The amount, structure, and repayment rhythm have to fit the cash gap you have.

Growth-oriented middle-market firms already use working capital this way. For Growth Corporates in the $50M to $1B range, 68% used working capital for operations, up 18% from 2023, and they saw a 300% surge in capturing supplier discounts through optimized payments, according to Visa’s 2024-25 working capital index. The practical lesson isn’t that you need more debt. It’s that flexible capital works best when it’s attached to a clear operating purpose.

Choose based on the gap not the marketing

Ask yourself a few blunt questions:

- Is the need recurring or one-time? Repeating gaps usually call for a revolving solution or process fix. One-time uses may fit a fixed loan.

- Is the problem tied to receivables, inventory, payroll timing, or payables? The answer points toward the product structure.

- How quickly will the cash come back? If repayment starts before the cash cycle closes, the loan will create stress.

- Can the business handle frequent payments? Many owners underestimate the pressure this creates.

- Will this funding solve the root issue, or just buy time? Time can be valuable, but only if you use it to correct the underlying problem.

What lenders want to see

Lenders are trying to answer a few practical questions. Is the business real, stable, and understandable? Is cash flow visible? Does the owner know why funds are needed and how repayment works?

Bring a clean package:

- Recent financial statements. P&L, balance sheet, and business bank activity should tell the same story.

- Accounts receivable aging. If you’re asking for receivables-related funding, this matters a lot.

- Inventory detail if inventory is part of the request. Lenders want to know whether stock is moving.

- A simple use-of-funds explanation. Not a vague growth story. A precise operational use.

- A cash flow view for the next period. Even a practical, lender-friendly forecast is better than hand-waving.

Owners also help themselves by explaining anomalies before underwriting finds them. If one large customer paid late, say so. If margins dipped because of a one-time buy, explain it. Good financial storytelling reduces friction because it gives context to the numbers.

Applications move faster when the request matches the records. If you say funds are for inventory, your statements should show inventory behavior that makes sense. If you say the issue is slow receivables, your aging report should support that.

From Cash-Strapped to Capital-Confident

The strongest businesses don’t wait until cash is uncomfortable to think about working capital. They watch the cycle, diagnose the choke point, and choose a fix that matches the problem.

That’s the real shift. Working capital for businesses isn’t just about survival funding. It’s about building a company that can keep moving when growth creates strain. Measure liquidity. Track your cash conversion cycle. Separate a collections problem from an inventory problem. Then choose financing that fits the asset, the timing gap, and the repayment reality.

That approach matters even more for owners who face structural financing barriers. Underserved businesses often face a “catalytic capital” gap, and directing at least 30% of capital to these firms is a target. Strong financial storytelling in a working capital application can help bridge gaps left by traditional lenders, according to the HTDC board packet on capital formation gaps.

The goal isn’t to borrow more often. It’s to borrow more intelligently, and eventually need less emergency capital because the business is converting cash more efficiently.

If you need a practical next step, start with Business Loan Warrior. You can review funding options for working capital, compare structures that fit your cash cycle, and move toward a financing decision based on the actual problem you’re solving.