You need a machine on the floor, a truck on the road, or a diagnostic unit in service this quarter. The main delay usually is not deciding whether the equipment will pay for itself. It is choosing a lender that fits the deal before you lose time in underwriting, pricing calls, and document requests that go nowhere.

I see owners run into the same three friction points. Speed. Deal size. Credit profile. A lender can be strong on one and weak on the other two. A bank may price well on a larger, cleaner transaction but move slowly. An independent lender may approve faster and ask for less paperwork, but the cost can run higher or the structure can be less flexible.

Equipment financing is a standard tool in the middle market and small business world, not a distress signal. Analysts at the Equipment Leasing & Finance Foundation found in the Horizon Report that the equipment finance industry reached $1.34 trillion in 2023 financing volume, with banks holding a large share of the market. That is why lender type matters. It affects approval speed, documentation, rate, term options, and how well the financing matches the useful life of the asset.

A useful short list should do more than name lenders. It should help you sort them fast.

That is the point of this guide. You will get a scannable comparison table up front, a practical review of seven equipment financing lenders, and a decision checklist you can use to match your situation to the right kind of funding. If you want more background on lender types, rates, and term structures before comparing providers, this guide to commercial equipment lenders, rates, and terms is a good place to start.

Table of Contents

- 1. Business Loan Warrior

- 1. Business Loan Warrior

- 3. Crest Capital

- 4. First Citizens Bank CIT

- 4. First Citizens Bank CIT

- 6. Key Equipment Finance

- 7. PEAC Solutions

- 7. PEAC Solutions

- Top 7 Equipment Financing Lenders Comparison

- How to Choose Your Lender & Get Funded

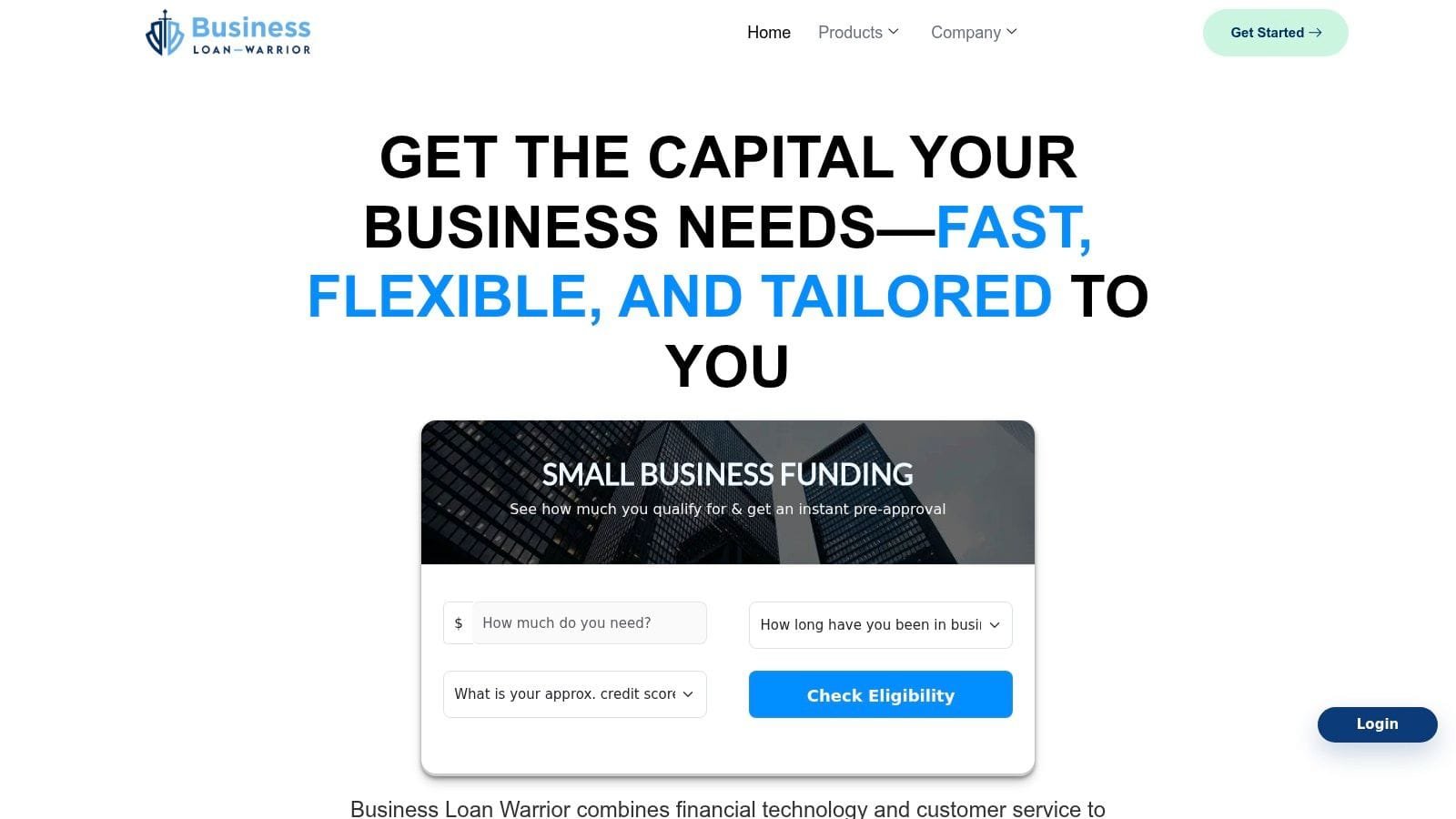

1. Business Loan Warrior

A common owner problem looks like this. You need a truck, CNC machine, or packaging line fast, but you do not have time to fill out five different lender applications, repeat the same story to five different reps, and wait while each one asks for another document. Business Loan Warrior fits that situation well.

The platform is built for comparison shopping without creating more admin work. You submit one no-fee application, check pre-approval without a hard credit pull, connect accounts through a secure dashboard, and review matched offers in one place through Business Loan Warrior. For an owner who values speed and optionality, that can save real time.

Why it stands out

The practical advantage is not just software. It is software plus guidance.

Plenty of online marketplaces are good at collecting your information. They are less helpful once the file gets complicated, such as when cash flow is uneven, the equipment is specialized, or the tax return does not tell the whole story. Business Loan Warrior gives borrowers a dashboard to track progress, but the stronger point is having real people help position the request so the lender review goes more smoothly.

That matters because equipment deals are rarely one-size-fits-all. A startup contractor buying a single skid steer needs a different structure than a manufacturer financing a six-figure line expansion. In my experience, borrowers make better decisions when they can compare term length, payment size, down payment, and approval conditions side by side instead of chasing quotes one lender at a time.

Best fit and trade-offs

Business Loan Warrior is a strong fit for owners who want to save time, compare multiple options, and avoid unnecessary hard credit pulls early in the process. It also makes sense for borrowers who are not sure which lender type fits their file and want a more guided search.

The trade-off is straightforward. A platform can widen your access to lenders, but it is still an intermediary model. If you already know the exact bank or captive finance company you want, going direct may feel simpler. Some owners also prefer dealing with one lender relationship from day one, especially on repeat purchases.

For everyone else, the value is in efficiency and visibility. You get a clearer picture of what is available before committing, which is often the difference between taking the first offer and choosing the right one.

1. Business Loan Warrior

Business Loan Warrior is the best fit for owners who don't want to run the same financing process five different times. Instead of applying lender by lender, you fill out one no-fee application, check pre-approval without a hard credit hit, connect your accounts in a secure dashboard, and review matched options in one place through Business Loan Warrior.

That model matters because speed is no longer a nice extra. In the U.S. equipment financing market, lenders have been adopting digital underwriting quickly, and the source material tied to this market notes a sharp year-over-year increase in digital underwriting tool adoption among top lessors, along with approval timelines shrinking from traditional cycles to much faster review windows in digitally enabled setups, according to this lower middle-market equipment finance overview. Business Loan Warrior is built around that reality instead of treating it like a side feature.

Why it stands out

What I like most is the blend of software and actual human help. Plenty of platforms promise speed, then leave you alone once the numbers get messy. Business Loan Warrior gives you a dashboard to track approvals, repayments, and credit insights, but it also lets you chat directly with underwriters. That's useful when you're trying to compare an equipment loan against an SBA option or a line of credit tied to installation costs and timing.

The platform also covers more than one use case. If your equipment purchase is part of a bigger project, such as expansion, construction, working capital support, or even an acquisition, you aren't forced into a narrow lane. It offers business loans, SBA loan processing, lines of credit, short-term financing, equipment and construction loans, merchant cash advances, invoice financing, and business acquisition loans.

Practical rule: If you still don't know whether you need a lease, a term loan, an SBA-backed structure, or a blended package, a marketplace-style platform is often smarter than starting with a single-product lender.

Business Loan Warrior has also served more than 2,000 businesses and delivered over $100 million in funding, based on its company materials on the Business Loan Warrior platform. For a borrower, that doesn't replace due diligence, but it does signal that you're not dealing with a brand-new shop still figuring out its workflow.

Best fit and trade-offs

This lender is especially practical for U.S. small and mid-sized companies that want options without burning time. The published positioning points toward businesses in the lower middle market and up to larger small business revenue ranges, which makes sense if you're buying meaningful equipment, not just replacing a laptop or two.

A few trade-offs are worth being clear about:

- Big advantage: One application can surface multiple financing paths.

- Big advantage: Soft-pull pre-approval lets you shop without damaging credit.

- Big drawback: Rates and fees aren't published up front, so you need to go through matching to see exact economics.

- Big drawback: It's primarily U.S.-focused, so it isn't the right platform for an international borrower needing cross-border execution.

If you want a broader primer before applying, Business Loan Warrior's guide to commercial equipment lenders and terms is a useful starting point.

3. Crest Capital

A common owner scenario goes like this. You need a machine this month, your vendor quotes one payment option, and by the time the contract shows up you realize the structure matters as much as the rate. Crest Capital stands out because it makes those structure choices easier to compare early, instead of burying them in the paperwork.

Crest is a direct lender, and that usually shows up in a more straightforward product menu. The company offers several common equipment finance structures, including $1 buyout, 10% purchase option, fair market value leases, equipment finance agreements, and options such as deferred, seasonal, used equipment, and some software financing, as noted earlier on Crest Capital's site.

That clarity matters because these products solve different problems. A $1 buyout usually fits a business that expects to keep the asset for years and wants a path that behaves more like ownership. An FMV lease can make more sense for equipment that ages fast, gets replaced on a short cycle, or carries uncertain resale value. If you're comparing lenders from the table in this article, Crest earns its place for one reason in particular. It helps you match the deal structure to the equipment instead of forcing every purchase into the same box.

Soft costs are another place where owners get tripped up. The equipment itself may be financeable, but freight, installation, training, and setup often decide whether the project works effectively. If you're trying to preserve cash at closing, this guide on equipment financing with no money down is worth reading before you sign, because "100% financing" does not always mean every project cost is included.

Best fit and trade-offs

Crest is a practical option for businesses that want to compare structures carefully, especially if the asset has a clear useful life and the wrong end-of-term option could get expensive.

The upside is straightforward. Owners get a lender that presents several common financing formats clearly, which helps with decision-making and speeds up internal approval. That is useful if you are choosing between lower monthly payments now and cleaner ownership later.

The trade-offs are familiar. Public pricing is limited, so you still need a quote to judge the actual economics. And with any lease or finance agreement, the decision checklist should include prepayment terms, end-of-term obligations, treatment of soft costs, and whether the equipment is likely to outlast the contract. Those details determine whether a "good approval" becomes a good deal.

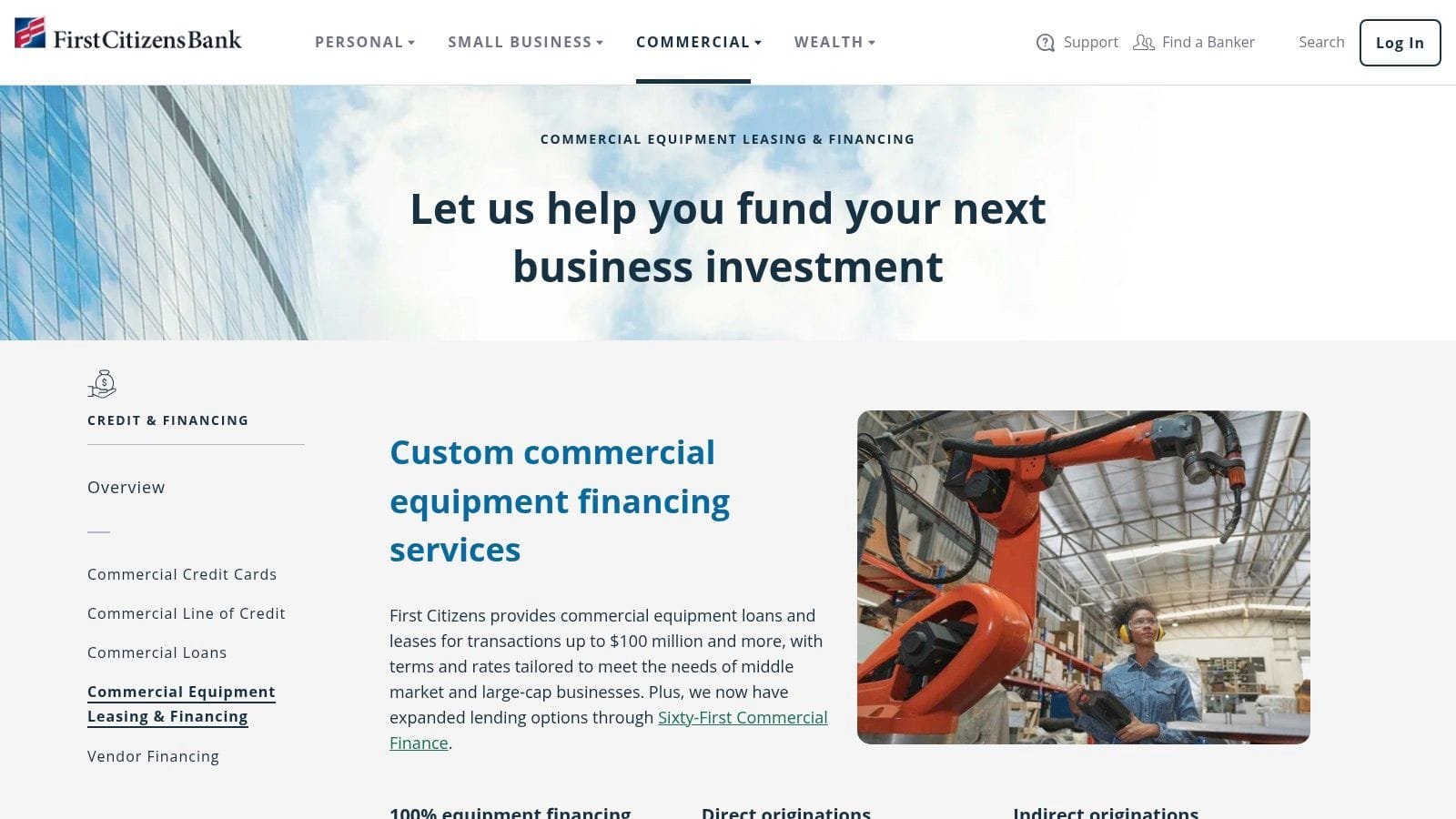

4. First Citizens Bank CIT

A company replacing one forklift has different needs than a company rolling out equipment across several locations. First Citizens Bank's CIT equipment finance platform fits the second case better. It is geared toward businesses with larger capital plans, industry-specific equipment, or repeat purchasing needs, which is why it belongs on the shortlist through First Citizens equipment financing and leasing.

The practical advantage is scale. Borrowers looking at a fleet refresh, production line expansion, or a multi-asset package often need more than a fast approval. They need a lender that can handle larger ticket sizes, coordinate documentation across assets, and stay useful after the first transaction closes. CIT tends to make more sense in that setting than in a small one-time equipment purchase.

That distinction matters.

Owners often focus on rate first. With a lender like CIT, the bigger question is whether the financing structure fits the broader growth plan. If the equipment purchase is tied to expansion, capacity planning, or a staged investment schedule, this guide to the strategic use of business equipment loans for growth is a helpful companion before you compare offers.

Where CIT fits best

CIT is usually a stronger fit for middle-market borrowers, established companies, and firms buying equipment that calls for more specialized underwriting. That can include transactions with multiple asset classes, industry-specific collateral, or a financing request that needs to line up with a broader banking relationship.

The trade-off is speed and simplicity. A smaller business shopping for a modest equipment note may find a more simple lender easier to work with. Bank-affiliated platforms often bring more process, more documentation, and a higher expectation that the borrower can present clean financials and a clear business case.

- Good fit: Middle-market companies financing large or multi-unit equipment purchases.

- Good fit: Businesses that want a lender capable of supporting repeat transactions over time.

- Watch out for: Smaller borrowers may face a longer process than they would with a lender focused on fast small-ticket approvals.

CIT works best when the financing decision is part of a capital strategy, not just a shopping decision. If you need a lender that can grow with the project, not just approve a single invoice, it deserves serious consideration.

4. First Citizens Bank CIT

First Citizens Bank's CIT equipment finance platform is built for scale and complexity. If your deal involves multiple assets, industry-specific underwriting, or a programmatic purchasing plan rather than a one-off transaction, CIT belongs on the shortlist through First Citizens equipment financing and leasing.

This isn't the lender I'd point a small company toward for the fastest small-ticket approval. It is the lender I'd consider when the equipment purchase is tied to a broader capital plan and you want a financing partner with bank balance sheet depth.

Who should call CIT

Middle-market companies stand to gain the most. The market data supports why that matters. In lower middle-market manufacturing transactions, lenders often prioritize businesses with meaningful enterprise value and EBITDA, with average deal sizes landing in a substantial middle range and lease terms stretching across several years, as summarized in the earlier cited equipment finance market overview. CIT is positioned more naturally for that world than for the borrower who just wants a small, fast approval online.

This lender's strengths show up when the asset is specialized or the transaction has moving parts. Think medical systems, transportation fleets, industrial production equipment, or a recurring vendor program for a growing business unit. The site also points to online customer portal access for managing contracts and payments, which helps once the portfolio gets larger.

Bank lenders usually win on depth, not on simplicity. If your deal has unusual collateral, staged purchases, or several entities involved, that depth can matter more than headline speed.

The trade-off is the usual bank trade-off. The process can be more underwriting-intensive and more relationship-driven. That's fine when the structure matters. It's frustrating when you're shopping a standard request and need an answer now.

6. Key Equipment Finance

A business owner ordering a custom production line, paying deposits before delivery, and trying to preserve working capital has a different problem than someone financing a single truck. Key Equipment Finance fits the first case better. Its offerings include loans, finance and operating leases, sale-leasebacks, tax-exempt structures, progress payment facilities, and syndication support through Key Equipment Finance.

That product mix points to a lender built for structured transactions.

Key's value shows up when timing, asset type, and capital strategy all need to line up. A sale-leaseback can turn owned equipment into liquidity without forcing a sale to an outside buyer. A progress payment facility helps when a manufacturer wants money in stages while equipment is still being built. Tax-exempt financing can matter for municipalities, nonprofits, and other eligible borrowers where the structure changes the economics of the deal.

This lender also separates itself by industry coverage. The platform highlights specialties across healthcare, manufacturing, transportation, agribusiness, public sector, and clean energy. That matters because equipment finance gets easier when the lender already understands useful life, resale risk, installation timelines, and how the asset produces revenue.

The trade-off is straightforward. Key is usually a better fit for larger or more customized transactions than for a small-ticket borrower who wants a same-day answer. If your request is plain vanilla, a simpler lender may be faster. If the equipment is specialized, delivery happens in phases, or several entities are involved, Key deserves a serious look.

According to the Horizon Report cited earlier, businesses continue to put significant capital into equipment and software. That supports the practical case for lenders that can do more than standard term notes.

- Best for: Companies with custom, staged, or strategically structured equipment purchases.

- Best for: Borrowers that need lease options, sale-leasebacks, or tax-exempt financing.

- Less ideal for: Small, standard requests where speed matters more than structure.

Before you call Key, map the deal on one page. List the equipment, vendor payment schedule, installation date, and whether preserving cash is more important than owning the asset immediately. That short exercise usually tells you whether you need a specialist like Key or a lender built for simpler approvals.

7. PEAC Solutions

A common financing moment looks like this. You have a quote in hand, the vendor wants an answer this week, and the equipment is standard enough that you do not need a custom capital structure. That is the lane for PEAC Solutions.

PEAC is built for throughput. Its platform emphasizes digital applications, fast credit decisions, vendor programs, deferred payment options, and several lease structures. For a borrower, that usually translates into less back-and-forth between the seller, the finance company, and your operations team.

Where PEAC tends to fit best

PEAC makes the most sense on small-ticket to lower mid-ticket equipment purchases where execution speed matters more than tailoring every term. If your vendor already offers PEAC financing at the point of sale, that can shorten the path from quote to funded deal. In practice, that matters because many equipment purchases stall after the buyer agrees on the machine but before the financing paperwork catches up.

The menu of structures also helps. FMV leases, 10% purchase option leases, 10% security deposit structures, and $1 buyout options are not just contract labels. They affect monthly payment size, end-of-term flexibility, and how much residual risk stays with you versus the lender. If the equipment may age out quickly, an FMV structure can preserve flexibility. If you know you want to keep the asset, a $1 buyout often fits better.

The trade-off is narrower flexibility on unusual deals.

If your transaction includes staged deliveries, highly specialized equipment, multiple related entities, or a financing request that depends on tax, accounting, or asset disposition planning, PEAC may feel too standardized. That is not a flaw. It is the reason the process can move faster on ordinary equipment purchases.

Use PEAC when the deal is straightforward and time-sensitive. If the financing plan needs to do more than get the equipment in the door, a more structured lender usually earns the extra paperwork.

- Best for: Standard equipment purchases through vendors or dealers with financing built into the sales process.

- Best for: Businesses that want quick decisions, digital applications, and clear lease options.

- Less ideal for: Complex transactions that need custom structuring, phased funding, or broader treasury coordination.

7. PEAC Solutions

A common PEAC scenario looks like this. The equipment quote is ready, the vendor wants to close this week, and the buyer needs financing that fits into the sales process instead of slowing it down. In that situation, PEAC Solutions is often a practical fit.

PEAC is built for volume and repeatable equipment transactions, especially on smaller and lower mid-ticket deals. The value proposition is speed, digital applications, vendor coordination, and lease options that cover the financing patterns many buyers ask for every day.

Best use cases for PEAC

PEAC tends to work well when the equipment is standard, the vendor is financing-aware, and the main goal is getting the asset in service without a long structuring exercise. That setup matters in practice because many purchases stall after the quote is approved but before financing lines up with the vendor's timeline.

It also helps when you want clear end-of-term choices. FMV, 10% purchase option, 10% security deposit, and $1 buyout structures each shift the balance between payment size, ownership, and flexibility. If the equipment may lose relevance quickly, keeping more flexibility can make sense. If you expect to use it for years, a buyout structure is often easier to justify.

The trade-off is scope.

PEAC is less compelling for deals that need unusual documentation, phased funding, large startup approvals, or a broader capital plan tied to working capital and treasury needs. Working capital products also come through a partner bank with separate terms, which can add another layer if you are trying to solve several financing needs at once.

As noted earlier, some equipment categories are easier for lenders to process quickly because the assets are easy to identify, price, and document. That is where PEAC usually fits best. Use it for straightforward equipment purchases where execution speed matters more than heavy customization.

Top 7 Equipment Financing Lenders Comparison

| Provider | Implementation Complexity 🔄 | Resource Requirements | Expected Outcomes ⭐ / 📊 | Ideal Use Cases | Key Advantages 💡 / ⚡ |

|---|---|---|---|---|---|

| Business Loan Warrior | Low 🔄, single digital app + human underwriting | Minimal, basic business docs; optional bank connection for matching | Effective ⭐⭐⭐⭐, fast matched offers; proven funding track record (>$100M) | U.S. SMBs needing fast, flexible capital, SBA, acquisitions, equipment | Single no‑fee app, soft credit checks, dashboard + underwriter chat ⚡💡 |

| Ascentium Capital (Regions) | Moderate 🔄, digital flow with vendor program options | Moderate, equipment specs, vendor setup; larger deals need more docs | Good ⭐⭐⭐, 100% financing, terms to 84 months; bank-backed stability 📊 | Equipment purchases $250K–$2M, vendor-financed deals | 100% financing incl. soft costs, long terms, Regions balance-sheet 💡 |

| Crest Capital | Low 🔄, rapid underwriting, common same‑day decisions | Minimal–Moderate, equipment docs; may require personal guarantees | High ⭐⭐⭐⭐, funding often in 24–48 hrs; multiple end‑of‑term choices 📊 | Small–mid ticket equipment, used equipment, quick funding needs | Fast decisions, flexible lease/buy options, tax resources ⚡💡 |

| First Citizens (CIT) – Equipment Finance | High 🔄🔄, relationship and structuring intensive | High, detailed docs, sector specialists, syndication for large deals | Very High ⭐⭐⭐⭐⭐, handles complex, large and programmatic transactions 📊 | Mid‑market to large‑ticket, multi‑asset, industry‑specific financing | Deep structuring expertise, scale, bank funding/syndication 💡 |

| U.S. Bank Equipment Finance | Moderate 🔄, app-only for small amounts; full underwriting for others | Moderate, equipment/vendor docs; existing relationship helps | Good ⭐⭐⭐, clear program params, broad asset eligibility 📊 | SMBs (esp. existing customers) needing broad asset financing up to moderate size | Published fast‑track fee/thresholds, vendor support, treasury services ⚡ |

| Key Equipment Finance (KeyBank) | High 🔄🔄, bespoke, relationship-driven structuring | High, sector specialists, lifecycle planning, syndication for large tickets | Very High ⭐⭐⭐⭐⭐, strong for complex, large transactions and lifecycle management 📊 | Middle‑market to enterprise, sale‑leasebacks, tax‑exempt, progress payments | End‑to‑end asset strategies, syndication, industry specialists 💡 |

| PEAC Solutions (formerly Marlin) | Low 🔄, high-volume, mostly digital approvals | Minimal, streamlined app; vendor channel integration; small-ticket focus | Good ⭐⭐⭐, fast approvals (often hours), $0‑down promotions, deferred programs 📊 | Small‑ticket equipment via vendors; quick, promotional financing | Speed and simplicity, deferred payments, strong vendor programs ⚡💡 |

How to Choose Your Lender & Get Funded

You have a machine picked out, the vendor wants an answer this week, and operations cannot wait another quarter. At that point, lender choice stops being a research project and becomes a business decision with real cost attached to it.

Use the comparison table above first. It gives you the fast screen. Then use this checklist to pressure-test the fit before you sign anything.

Your Decision Checklist:

- Timeline: If the equipment has to ship now, speed matters more than perfect pricing. Fast digital lenders and vendor programs often win here. If you have a few weeks, banks and larger captives may earn the time with better structure or lower cost.

- Deal size: Match the lender to the full request, not just the base equipment price. Include freight, installation, software, training, taxes, and other soft costs. Small-ticket requests can move through lighter approval paths. Larger or multi-unit deals usually benefit from a lender that can structure more than a simple note.

- Credit profile: Strong credit opens more bank options and usually improves pricing. Borrowers with thinner files, recent volatility, or limited time in business often do better with lenders that underwrite the business story along with the score.

- Asset type: Standard titled or widely used equipment is usually straightforward. Specialized medical, manufacturing, construction, or technology assets often require a lender that understands resale value, useful life, and installation risk.

- Payment structure: Rate matters, but payment timing matters too. Seasonal businesses should ask about deferred, step, skip, or seasonal payments before comparing offers side by side.

- Ownership goals: Some owners want the lowest monthly payment. Others want clear ownership at the end, or flexibility to upgrade before the equipment ages out. Lease versus loan is not just a tax question. It is an operations question.

A simple deal should stay simple. A bakery replacing two ovens usually does not need a relationship-driven lender with a long underwriting process. A contractor financing several pieces across entities, with progress payments and uneven revenue, probably does.

The same rule applies to repayment. A flat monthly payment looks clean, but clean is not always practical. If cash flow rises and falls through the year, the wrong payment schedule can create stress even when the quoted rate looks competitive.

The financing market keeps expanding, which gives borrowers more choice and more room to make an expensive mismatch. Analysts at Grand View Research describe a growing equipment finance market in their equipment finance market analysis. More options help only if you narrow the field by fit, not by marketing claims.

A practical way to make the decision

Start with four numbers: total project cost, down payment available, monthly payment range, and how quickly the equipment must be in service. Then answer one plain question. Are you buying a standard asset with a clean borrower profile, or do you need a lender that can handle complexity?

That answer usually points you in the right direction faster than another hour of rate shopping.

Delays are expensive. Old equipment keeps draining productivity, maintenance costs keep rising, and the purchase you meant to make this quarter turns into another year of patchwork.

If you are comparing options, focus on the all-in result. Approval speed, documentation burden, payment shape, end-of-term flexibility, and total financed cost matter more than a headline rate pulled from a sales email.

Your next step is simple. Use the table to narrow the lender type, use the checklist to screen for fit, and apply where the structure matches the way your business runs.