Cash feels fine until it doesn’t. One week you’re waiting on receivables from good customers, and the next week a freezer dies, a supplier wants payment before release, or a rush order lands that could open a new account if you can move fast enough.

That tension is especially familiar for established companies in the $20M to $50M revenue range. You’re not a startup looking for a tiny loan, but you’re also not a giant public company with a treasury desk and easy bank access. You need funding that fits real operating cycles, not generic advice built for businesses much smaller or much larger than yours.

Short term business financing sits right in that gap. Used well, it’s not a panic button. It’s a way to protect momentum, keep cash flow stable, and buy time when money is tied up somewhere else.

Table of Contents

- Why Your Business Needs a Short-Term Funding Plan Now

- Understanding Short-Term Business Financing

- The Main Types of Short-Term Financing Products

- Comparing Costs Terms and Funding Speed

- Who Qualifies and What Lenders Look For

- Your Next Steps to Secure Funding with Business Loan Warrior

Why Your Business Needs a Short-Term Funding Plan Now

A lot of owners wait to think about financing until something breaks or a deal is on the table. That’s understandable, but it puts you in the weakest possible position. When the need is urgent, speed starts to outweigh judgment, and expensive money can look reasonable for a day or two.

The lending climate has made that risk more common. Banks tightened credit standards for 13 consecutive quarters, while U.S. small business lending still grew 7.5% in Q2 2025. That shift pushed 72% of businesses to seek non-bank funding sources, often for operating expenses and expansion needs, according to Cardiff’s 2025 small business lending market review.

That tells you something important. Healthy businesses still need capital. They’re just finding it in different places.

The real issue isn’t only access

For a business in the middle market, the problem usually isn’t whether funding exists at all. The problem is matching the right tool to the actual situation before the clock starts ticking.

A cash gap caused by slow-paying customers is one kind of problem. A temporary inventory opportunity is another. An emergency repair is different again. If you treat all three the same way, you can easily end up with the wrong structure, the wrong repayment rhythm, or the wrong lender.

Practical rule: Decide on your financing plan before you need money. You’ll compare offers more clearly when your back isn’t against the wall.

Agility matters more than ever

Short term business financing works best when you treat it like part of operations, not a rescue mission. That means knowing which products you’d consider, what documents you’d need, and what cost trade-offs you’d accept for speed.

For established companies, that planning creates room to act. You can cover payroll without draining reserves, buy inventory tied to a profitable order, or bridge a receivables gap without forcing every other department to freeze spending. In a cautious credit market, that kind of flexibility can matter as much as the funding itself.

Understanding Short-Term Business Financing

A bridge, not a mortgage

The easiest way to understand short term business financing is to think of it as a bridge. You’re using outside money to get from today’s cash need to tomorrow’s expected cash inflow.

That’s different from long-term debt. Long-term financing usually supports assets or projects that will pay off over years, like real estate, major buildouts, or large equipment programs. Short-term financing is built for timing problems and near-term opportunities.

If your receivables are strong but slow, a bridge can help. If you need to stock inventory before a known sales window, a bridge can help there too. If a repair needs to happen before production slips, same idea. The money is meant to solve a short-cycle problem.

When this tool fits and when it doesn’t

Good uses of short-term funding often share one trait. You can see a believable path to repayment from normal business activity.

That repayment might come from collected invoices, incoming card sales, a seasonal spike, or margin from a specific order. The key is that the financing lines up with a real cash event, not a vague hope that “sales should improve.”

Here’s a simple way to sort the decision:

- Use short-term financing when you need to bridge a cash timing gap, handle a temporary working capital squeeze, or move quickly on an opportunity with near-term payoff.

- Use longer-term financing when the investment will produce value gradually over many years.

- Pause and rethink if you’re borrowing repeatedly just to cover ordinary operating losses with no clear path to stabilization.

If you want a side-by-side look at that distinction, this guide on short-term vs. long-term business loans is a useful companion.

A common point of confusion is repayment pressure. Owners often focus on approval speed and loan size first, then realize later that the payment schedule is too tight for their actual cash cycle. That’s why the right question isn’t only “Can I get funded?” It’s “Can this structure breathe with my business?”

This quick video gives a helpful overview before you compare products in detail.

Short-term money should solve a short-term problem. If it creates a long-term strain, the fit is wrong.

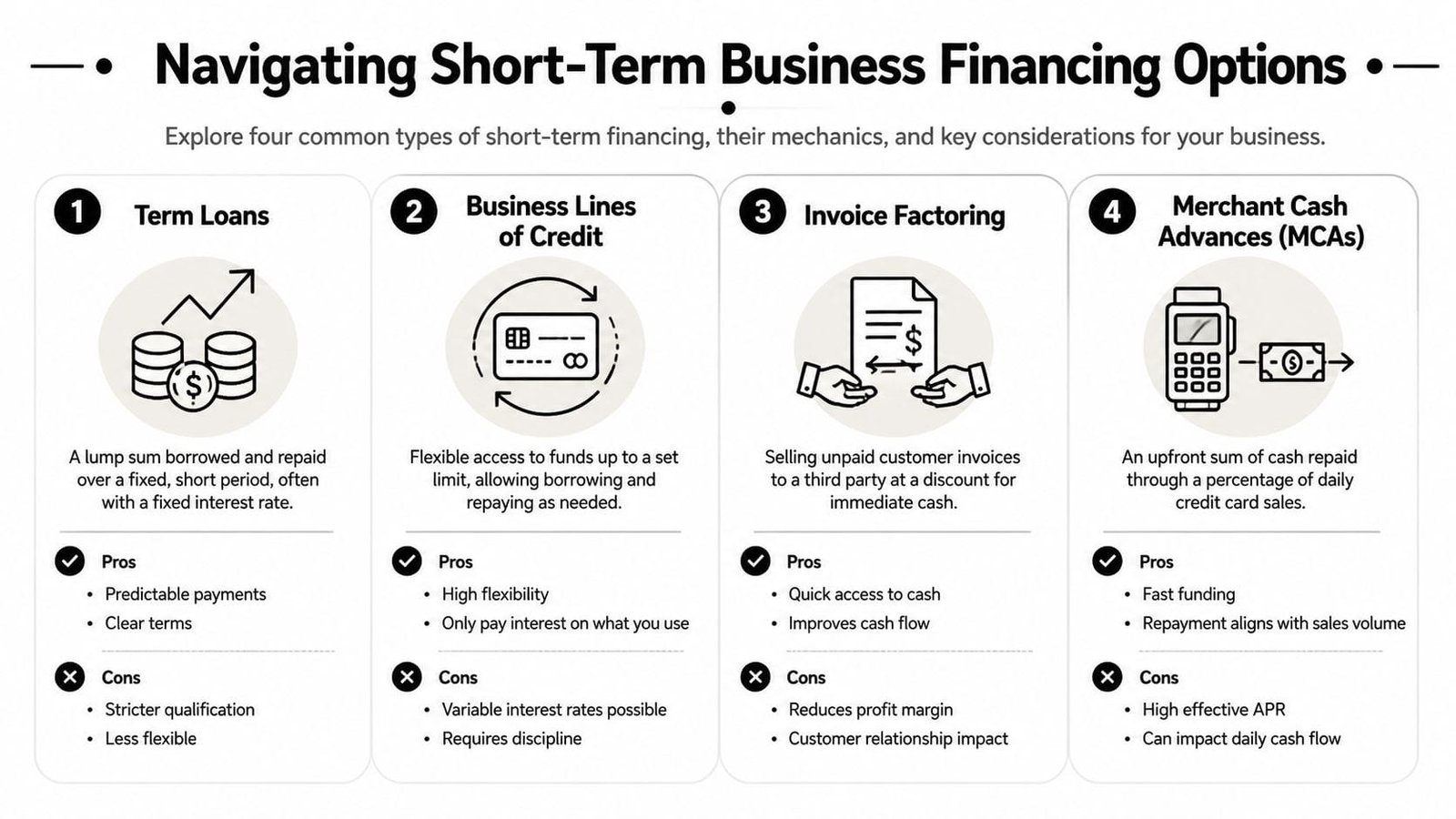

The Main Types of Short-Term Financing Products

The product matters because repayment mechanics matter. Two offers can provide the same cash amount and feel completely different once repayment starts hitting your account.

Short-term loans

This is the most familiar structure. You receive a lump sum up front and repay it over a defined period through scheduled payments.

For an established business, this can work well when the need is specific and the use of funds is easy to define. Think equipment repair, a time-sensitive inventory buy, or a targeted operating cushion while a large receivable clears.

Why owners like it: the structure is straightforward. You know what you borrowed, the term is clear, and you can model repayment in advance.

Where it can pinch: flexibility is limited after funding. If your needs change, you don’t get to redraw what you’ve paid back the way you could with a line of credit.

Business lines of credit

A line of credit is the financing version of a standby tool chest. The lender approves a borrowing limit, and you draw only what you need.

That makes it useful for uneven cash cycles. A retailer might use it to prepare for a buying window. A service business might use it to smooth payroll while waiting for large client payments. A multi-location operator might keep it available for recurring working capital gaps that don’t arrive on a neat schedule.

The biggest strength here is control. You don’t have to borrow the full amount on day one.

A line of credit is often the most practical fit when your challenge is ongoing variability rather than a one-time event.

Invoice financing and factoring

If your business issues invoices to creditworthy customers and waits to get paid, this option can turn receivables into usable cash sooner.

The broad idea is simple. Instead of waiting through the full payment cycle, you use unpaid invoices to improve current cash flow. That can be especially attractive if your customer base is solid but pays on long terms that pressure your operating cash.

There are relationship considerations, though. Some structures involve more lender visibility into your receivables process than others. Owners should understand exactly how customer communication works before signing anything.

If your bottleneck is timing, not demand, receivables-based financing can be cleaner than taking on a general-purpose loan.

Merchant cash advances

An MCA is not the same as a traditional loan. In plain language, a provider advances cash now and collects repayment from future sales, often tied to card receipts or daily revenue activity.

That’s why MCAs appeal to businesses that need speed and have strong card volume. Restaurants, retail operators, and some service businesses often look at them when immediate funding matters more than perfect pricing.

But this product deserves caution. It can be easy to get and hard to carry if daily or frequent remittances tighten your operating cash too much.

A simple way to think about the trade-offs:

- Short-term loan: good when the need is defined and fixed payments fit your cash flow.

- Line of credit: good when cash needs come and go.

- Invoice financing: good when strong receivables are the asset.

- MCA: good only when speed is critical and you fully understand the cost and repayment drag.

How to narrow your first choice

Instead of asking which product is “best,” ask which one matches the source of repayment.

- Repaying from incoming invoices: start with invoice financing.

- Repaying from variable working capital cycles: look at a line of credit.

- Repaying from a known short-term event: consider a short-term loan.

- Repaying from daily card sales under time pressure: an MCA may enter the conversation, but compare carefully.

Most mistakes happen when owners choose based on approval speed alone. The smarter filter is operational fit.

Comparing Costs Terms and Funding Speed

The cheapest-looking offer isn’t always the least expensive in practice. That’s where many business owners get tripped up.

The number on the offer sheet can mislead you

Some products are quoted with an APR, which helps you compare borrowing costs on a more standardized basis. Others, especially MCAs, may use a factor rate, which tells you the repayment multiple but doesn’t read like a traditional annualized interest cost.

That distinction matters because repayment speed changes the burden. A product with frequent repayment can squeeze cash harder than a slower-pay structure, even if the headline figure looks manageable at first glance.

You also need to look at payment frequency. Daily, weekly, and monthly payments create very different operating realities. A profitable business can still feel cash-starved if repayments are too frequent relative to how money comes in.

If you want a plain-English walkthrough for evaluating offers, this resource on how to calculate the real cost of a small business loan is worth bookmarking.

A practical comparison table

Use the table below as a screening tool, not a final verdict.

| Financing Type | Typical Amount | Repayment Term | Funding Speed | Common Cost Structure |

|---|---|---|---|---|

| Short-term loan | Varies by lender and cash flow profile | Short duration, fixed end date | Often faster than traditional bank term debt | Usually interest-based pricing or fixed financing charge |

| Business line of credit | Varies by lender and approved limit | Draw, repay, and reuse if revolving | Often relatively fast once approved | Interest charged on amount drawn, sometimes with fees |

| Invoice financing or factoring | Linked to eligible receivables | Tied to invoice collection cycle | Can be quick when invoices are verifiable | Fees tied to invoice value and timing |

| Merchant cash advance | Based on sales history and provider appetite | Repaid through future sales activity | Often very fast | Factor-rate style pricing and frequent remittance structure |

Reality check: Speed, simplicity, and low cost rarely show up together in the same offer. Usually you get two of the three.

How company value affects what you can borrow

Borrowing capacity doesn’t come from lender mood alone. It’s tied to what the business appears able to support.

For valuation context, businesses under about $5M in revenue often trade at 2 to 4 times SDE, while businesses with $20M+ in revenue can command 5 to 7 times EBITDA. Lenders use these multiples as hard caps, often limiting loans to about 3 times SDE according to FE International’s 2025 business valuation guide.

For middle-market companies, the practical takeaway is this: stronger earnings quality and clearer cash flow often expand your options. But even then, lenders won’t ignore repayment capacity just because revenue is large. They still underwrite to supportable debt levels.

That’s why two businesses with similar sales can receive very different offers. One has clean margins, disciplined reporting, and predictable collections. The other has revenue, but weak conversion to cash. Lenders care about the second part more than many owners expect.

Who Qualifies and What Lenders Look For

Qualification isn’t one universal checklist. It changes by lender type, product type, and how your business makes money.

What most lenders review first

Most providers start with a handful of practical questions. Is the business producing reliable revenue? Has it been operating long enough to show a pattern? Does recent bank activity support the repayment story? Are there signs of stress such as heavy overdrafts, declining deposits, or unstable margins?

Traditional banks often put more weight on historical financial statements, conventional credit metrics, collateral, and stricter policy boxes. Fintech and alternative lenders usually move with a different rhythm. They may focus more on recent cash flow and current operating performance.

That’s why two lenders can look at the same company and reach different conclusions. One sees a business outside standard policy. Another sees a business with enough verified cash movement to support a short-term facility.

A few items usually deserve attention before you apply:

- Recent revenue pattern: Lenders want consistency more than a single big month.

- Cash flow quality: Deposits matter, but timing and stability matter too.

- Existing debt load: Current obligations affect how much room is left for another payment.

- Use of funds: A specific purpose usually underwrites better than a vague request for “working capital.”

Why middle-market positioning matters

Many owners in the $20M to $50M revenue range assume they’ll automatically fit bank credit boxes. In reality, this segment often falls into an awkward middle ground. You may be too complex for simplistic small-business underwriting and not large enough for the most customized institutional treatment.

In private credit, lenders often segment companies by earnings. The core middle market is commonly defined as $30M to $50M EBITDA, and for sub-$50M EBITDA companies, private credit providers can offer covenant-light structures and alternative underwriting based on metrics such as ARR, as explained in ABF Journal’s discussion of direct lending down-market.

That matters because structure can be as important as approval. A lender that understands recurring revenue, seasonality, or uneven cash cycles may give you a facility that fits the business better than a rigid bank product.

A good underwriting match doesn’t just increase approval odds. It reduces the chance that the loan becomes a problem after closing.

Your Next Steps to Secure Funding with Business Loan Warrior

The smartest next move is simple. Don’t shop for money only by rate or only by speed. Build a decision filter and use it every time.

A simple decision checklist

Start with the purpose of the funding. Is this for inventory, payroll support, emergency repair, a receivables gap, or a short runway for expansion? The answer should point you toward the structure.

Then pressure-test the repayment plan. Ask yourself what exact cash event pays this off. If the answer is fuzzy, pause. Short term business financing works best when repayment comes from a clear operating source.

Before you submit anything, gather your recent business financials, bank activity, debt details, and a concise explanation of how the funds will be used. Clean information shortens the process and makes mismatches easier to spot early.

How to move without hurting your credit

A lot of owners hesitate because they don’t want to trigger unnecessary credit inquiries while comparing options. That concern is fair.

Fintech platforms can offer no-impact pre-approvals by using linked bank-account data for real-time underwriting, giving owners a way to check options without the credit dings common in traditional applications, as described in Biz2Credit’s overview of lower-rate financing paths for underserved businesses.

One practical route is using Business Loan Warrior’s application portal, which lets business owners complete a single no-fee application, connect accounts for underwriting review, and check pre-approval options without a hard-credit-first approach. For a busy operator, that kind of workflow can make comparison shopping less disruptive.

The goal isn’t to chase every possible offer. It’s to narrow quickly to the structures that fit your timing, cash flow, and credit priorities.

If you’re weighing speed versus cost versus credit impact, Business Loan Warrior gives you a practical place to start. You can review short-term funding options through one application, check pre-approval without a hard-credit-first process, and see which structures may fit your business before committing.