A customer just asked for a larger order than you can comfortably fulfill. Or a key machine needs replacing before it fails. Or you found the right location to expand, but your cash is tied up in payroll, inventory, and receivables. That’s when the key question shows up.

Not “Can I borrow money?”

Should I borrow as the business, or as myself?

That choice looks small in the moment. It isn’t. In a business loan vs personal loan decision, you’re choosing more than speed or convenience. You’re choosing what balance sheet carries the debt, which credit profile gets strengthened or damaged, and how much of your personal financial life you want attached to the company’s next move.

A lot of owners make the fast choice because they’re under pressure. I get it. Urgency narrows your vision. But if you only look at who can fund you first, you can end up solving this month’s cash problem by creating next year’s credit, tax, and liability problem.

Table of Contents

- The Funding Crossroads Every Founder Faces

- Business Loans and Personal Loans at a Glance

- A Head-to-Head Comparison of Key Loan Terms

- The Hidden Impact on Your Credit and Taxes

- The Case for Using a Personal Loan and Its Limits

- How to Choose the Right Funding Path for Your Business

- From Decision to Funding with Business Loan Warrior

The Funding Crossroads Every Founder Faces

You don’t usually compare loan types in a calm, academic mood. You compare them when something important is on the line.

A contractor lands a project and needs materials before the first draw comes in. A retailer wants inventory ahead of a seasonal push. A service business sees a chance to hire a producer who could enable the next stage of growth. The opportunity is real, but the cash isn’t sitting there waiting.

In that moment, a personal loan can feel like the spare key hidden under the mat. It’s accessible, familiar, and fast. A business loan feels more like the proper front-door entry. Cleaner, safer, built for the job, but sometimes harder to open.

That’s why owners get stuck. They’re not confused about whether they need money. They’re torn between speed now and structure later.

Practical rule: If the loan will help the company grow beyond a short-term gap, treat the decision like a strategic move, not an emergency purchase.

Here’s the issue most people miss. The debt doesn’t just fund inventory, equipment, or expansion. It also tells lenders, credit bureaus, and tax records how your company operates. When you borrow personally for a business purpose, you blur a line that should usually stay clean.

For an early-stage owner, that blur may be unavoidable. For an established company, it’s often a mistake.

The right answer depends on where your business stands today, how much you need, how fast you need it, and whether you’re building a company that can finance itself cleanly in the future.

Business Loans and Personal Loans at a Glance

At the simplest level, a personal loan is tied to you. A business loan is tied to your company.

That sounds obvious, but the practical consequences are huge. When you use a personal loan, your personal income, personal credit, and personal repayment history carry the weight. When you use a business loan, the lender evaluates the company and the debt is structured for commercial use.

The core difference

A personal loan is built for individual borrowing. Lenders look mainly at your personal credit profile and ability to repay as a consumer. You may still use those funds for business in some cases, but the loan itself wasn’t designed around the economics of a growing company.

A business loan is built for commercial activity. It exists to fund equipment, expansion, inventory, payroll support, acquisitions, and working capital. That matters because business cash flow behaves differently from household cash flow.

It's comparable to insurance.

Using a personal loan for your company is a bit like using personal auto insurance for a delivery van. You might get away with it for a while. But the policy wasn’t designed for the risk, the use case, or the scale. When something goes wrong, the mismatch becomes expensive.

Quick comparison

| Feature | Business Loan | Personal Loan |

|---|---|---|

| Who the loan is tied to | The business | You personally |

| Primary use | Commercial growth and operations | Personal borrowing, sometimes used for business |

| Underwriting focus | Business revenue, time in business, financials | Personal credit, income, debt-to-income |

| Best fit | Established businesses with clear funding goals | Startups, urgent small gaps, owners with strong personal credit |

| Long-term value | Can support business credit and cleaner financial separation | Can create speed, but keeps debt attached to your personal profile |

| Main strategic risk | More documentation and stricter approval standards | Personal liability and mixed personal-business finances |

The cleanest financing structure is usually the one that matches the actual purpose of the money.

If you run an established business and need capital for a business objective, I usually favor the business loan route. It aligns the debt with the asset or growth initiative it’s funding. That keeps your records cleaner and your future financing options stronger.

If you’re still in the launch stage and the company doesn’t yet have the history to qualify on its own, a personal loan can work. But you should treat it as a bridge, not as your permanent funding strategy.

A Head-to-Head Comparison of Key Loan Terms

You’re deciding between two very different tools. One is built to fund a company. The other is built to fund a person who happens to own one.

That difference shows up in your approval odds, your monthly payment pressure, and how much room the loan gives your business to grow without choking cash flow.

Eligibility and application

Business loans ask for proof that the company can carry the debt. Personal loans ask whether you can carry it yourself.

As noted in NerdWallet’s comparison of business loans and personal loans, business lenders often review time in business, revenue, and business financials, while personal lenders focus more heavily on your personal credit, income, and debt-to-income ratio.

Here’s the practical impact:

- Business loan applications usually require bank statements, revenue history, and business records.

- Personal loan applications are often faster because they rely more on your consumer credit profile.

- Newer businesses often qualify more easily on the personal side, but that convenience comes with more personal exposure.

If your books are clean and the business has real operating history, use that strength. Put the debt where it belongs. If the company is still young and cannot qualify on its own, a personal loan can fill a gap, but don’t confuse access with fit.

Loan amounts and repayment terms

Loan size and term length shape your business more than owners expect.

A business loan can give you enough capital to fund a real initiative and enough time to repay it without forcing the company into a monthly cash squeeze. A personal loan usually gives you a smaller amount and a shorter runway. That may work for a quick inventory buy or a modest startup expense. It is usually a poor match for equipment, expansion, or a longer growth cycle.

| Feature | Business Loan | Personal Loan |

|---|---|---|

| Typical borrowing capacity | Higher limits designed for commercial use | Lower limits tied to consumer lending |

| Repayment term | Can stretch much longer, depending on loan type | Usually shorter repayment windows |

| Monthly payment pressure | Often easier to spread over time | Often higher on the same dollar amount because the term is shorter |

| Best fit | Equipment, expansion, hiring, working capital planning | Small gaps, short-term needs, early-stage funding |

A short repayment term works like sprinting uphill with a backpack. You may get there, but your cash flow pays the price every month.

That’s why term length is a strategic decision, not a footnote. If the benefit of the money will play out over years, your repayment schedule should give the business years, not months, to absorb it.

Interest rates and what they mean in real cash flow

Rate matters. Term matters too. The question is what the payment does to your business after payroll, rent, inventory, and taxes.

In early 2025, NerdWallet reported that SBA 7(a) and bank business loan rates often landed in lower ranges than many personal loans, while personal loan APRs could run much higher depending on credit quality. The headline rate only tells part of the story. A smaller loan with a shorter term can still hit your monthly cash flow harder than a larger business loan structured over a longer period.

That is where owners get trapped. They choose the faster loan, then spend the next year feeding it with operating cash.

A good funding decision should do three things:

- Protect monthly liquidity, so the loan does not crowd out payroll, marketing, or inventory.

- Match the life of the debt to the life of the investment, so you are not repaying a long-term business move on a short consumer schedule.

- Keep the tax and recordkeeping side clean, especially if you want clearer deductions and cleaner reporting later. Our guide to tax-smart business financing strategies explains why that structure matters.

Here’s my view. If you need a modest amount and speed matters more than structure, a personal loan can work. If you are funding something meant to grow the company, protect cash flow, and support future financing, a business loan is usually the smarter choice.

Use the tool built for the job. Your balance sheet will feel the difference long after the money lands.

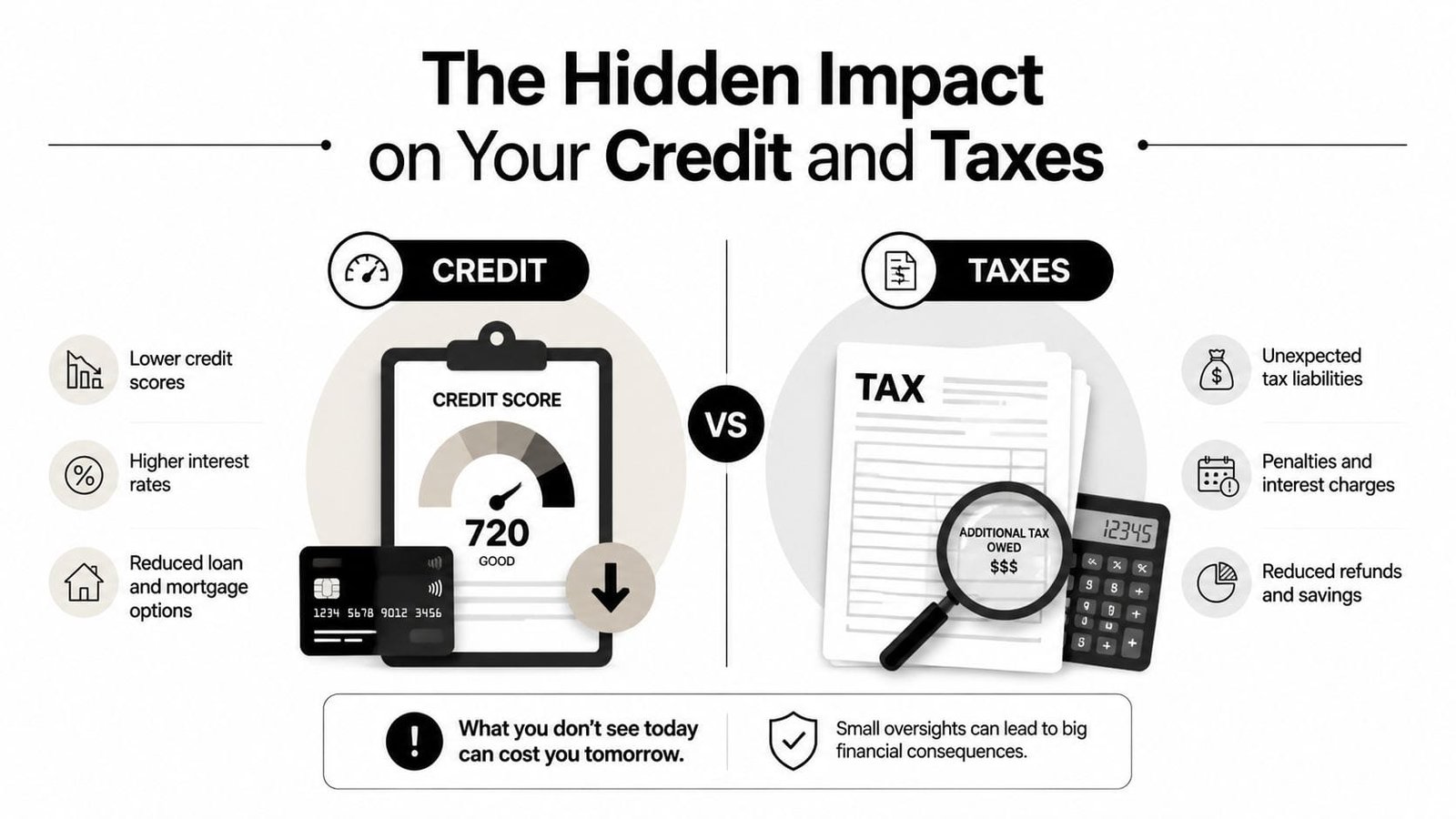

The Hidden Impact on Your Credit and Taxes

A founder takes a fast personal loan to buy equipment, cover a hiring gap, or smooth out inventory. The cash arrives. The business keeps moving. A year later, the company still has no real credit profile, the debt sits on the owner's consumer file, and the tax treatment is weaker than it could have been.

That is the part many owners miss.

What happens to your credit profile

A business loan does more than fund a purchase. It helps establish the business as a borrower in its own right. A personal loan does the opposite. It ties business growth back to your personal credit file.

That choice has long-term consequences. If the loan reports on the business side and the account is managed well, you start building a financial track record under the company name. That can make future borrowing easier, cleaner, and less dependent on your personal score. If you keep using personal loans for business needs, the company may grow in revenue while staying weak on paper.

A business that always borrows through the owner never fully separates from the owner.

That matters for more than future approvals. It affects negotiating power, lender options, and how much personal exposure you carry every time the business needs capital. Using personal debt to run a company is like wiring a commercial building through a household breaker box. It may work at first. It was not built for repeated strain.

Why tax treatment changes the true cost

Tax treatment changes your real borrowing cost, not just your paperwork.

Interest on a properly structured business loan is often deductible as a business expense. Personal loan interest usually is not treated the same way, even if you used the funds to support the company. That means two loans with similar payments can produce very different after-tax results.

Owners give away margin. They compare the monthly payment and stop there. The smarter comparison is what the debt costs after deductions, how cleanly it fits your books, and whether it supports a clear line between business obligations and personal obligations. If you want a practical breakdown, read our guide to tax-smart business financing strategies.

My recommendation is simple. If your business can qualify for a business loan, use the business loan. You get cleaner records, a better shot at building business credit, and a stronger boundary between company debt and personal liability. Easy money can solve today's problem. Properly structured money helps you grow without dragging your personal finances behind the business every step of the way.

The Case for Using a Personal Loan and Its Limits

Personal loans are not necessarily wrong for business use. In many cases, they’re how the business gets moving at all.

You can dislike that reality and still respect it.

When a personal loan is a smart bridge

The reason is access. Survey evidence in the Consumer Financial Protection Bureau conference paper shows that 86% of small employer firms use personal credit for funding activities, and 45% of small business loan approvals hinge primarily on personal credit scores.

That tells you something important. A lot of business funding still begins with the owner, not the company.

A personal loan can be a rational move when:

- The business is brand new. No operating history means the company may not qualify on its own.

- The capital need is modest. You’re covering a small inventory purchase, initial setup cost, or a temporary cash squeeze.

- Time matters more than optimization. Personal loans often move faster because the underwriting is simpler.

- Your personal credit is strong but the business file is thin. That can make personal borrowing the only realistic near-term option.

For owners in that position, I don’t recommend guilt. I recommend discipline. Use the personal loan for a defined purpose, keep records clean, and treat it as transitional funding. If you’re exploring capital options that don’t rely on hard collateral, this guide to unsecured business loans and how they work can help you map the next step.

Where the strategy breaks down

The problem starts when owners keep using personal debt after the business should have outgrown it.

Here’s where a personal loan stops being useful and starts becoming sloppy:

- You need more money than a personal loan can comfortably provide. That caps growth before the opportunity does.

- Repayment lands on your household budget. If the business has a rough quarter, your personal credit takes the hit.

- You blur personal and business finances. That makes bookkeeping messier and liability boundaries weaker.

- You never build business borrowing capacity. The company stays dependent on you instead of becoming financeable on its own.

Borrowing personally for a startup is understandable. Borrowing personally for an established operating company is often a sign that the capital structure hasn’t kept up with the business.

That’s the line I use. A personal loan is a bridge. It is not a foundation.

How to Choose the Right Funding Path for Your Business

You are not just choosing how to get cash. You are choosing where the risk lives for the next several years.

That matters more than the interest rate headline. The wrong loan can box in future growth, muddy your books, weaken liability protection, and keep the business tied to your personal credit long after it should be standing on its own.

Start with the outcome, not the loan

Ask one question first: Do you want to fund a short-term need, or do you want to build a financeable company?

If the goal is survival for a very early-stage business, a personal loan may be acceptable. If the goal is growth, cleaner reporting, stronger business credit, and better financing options later, choose business financing whenever the company can qualify.

That is the dividing line.

A business loan works like putting commercial tires on a work truck. A personal loan is more like borrowing your family car for a jobsite run. You might get through the day, but it is the wrong vehicle for repeated heavy use.

The four filters that actually matter

Use these filters in order.

- Business maturity: If you have operating history, steady revenue, and organized financials, stop defaulting to personal borrowing. The business should carry business debt.

- Use of funds: Inventory, payroll support, equipment, expansion, and hiring usually belong under business financing because the debt is tied to business output.

- Risk location: If a slow quarter would force repayment from your household income, you are putting personal stability in front of business volatility. That is a dangerous setup.

- Long-term strategy: If you want stronger business credit, cleaner tax reporting, and a company that can qualify for larger funding later, business borrowing is the smarter move.

My recommendation by stage

For a new business with limited history and a small, defined capital need, a personal loan can work. Keep the amount controlled. Tie it to a specific use with a clear payoff, such as launch inventory or equipment that produces revenue quickly. Treat it as temporary.

For an operating business with real sales and repeatable cash flow, choose a business loan. That keeps the obligation closer to the asset it supports, gives your accountant cleaner records, and helps the company build its own borrowing profile instead of riding on yours.

For a larger company planning expansion, equipment purchases, or an acquisition, the decision is simple. Use structured business financing. Personal borrowing is too small, too exposed, and too messy for a commercial objective of that size.

Watch the second-order effects

Owners often focus on approval speed and monthly payment. That is too narrow.

The better question is what this choice does six, twelve, and twenty-four months from now.

A business loan can help establish business credit history and create a cleaner paper trail for interest expense and business use. A personal loan can do the opposite if you mix accounts, commingle spending, or make the company look less financeable because too much of its capital stack still sits on your personal side.

If you expect to use multiple products over time, read this guide on how to layer financing tools without over-leveraging your small business. Good funding strategy is not about grabbing one loan. It is about building a structure your business can keep using.

One final rule. Do not choose a personal loan because it feels simpler. Choose the option that protects cash flow, preserves liability boundaries, and gives the business room to grow.

From Decision to Funding with Business Loan Warrior

Once you know which path fits, execution matters. A good financing decision still falls apart if the process is slow, confusing, or built around the wrong lenders.

Business Loan Warrior is useful because it simplifies that front end. Through a single, no-fee application, owners can check pre-approval without affecting credit, connect accounts, review options in a secure dashboard, and track progress from application through approval. That’s valuable when you’re weighing term loans, SBA options, lines of credit, equipment financing, or other commercial products and don’t want to waste time chasing lenders that don’t fit your profile.

The other advantage is matching. A restaurant with uneven monthly cash flow doesn’t need the same structure as a growing contractor, retailer, or service company. Larger firms pursuing expansion or acquisition financing need a different conversation entirely. Business Loan Warrior combines technology with human support, so you’re not left guessing which product belongs in your capital stack.

If your business has moved beyond bootstrapping, the next step is straightforward. Stop treating financing like a one-off scramble. Build a funding strategy that supports growth, protects personal downside, and gives the company room to operate.

If you’re ready to compare business funding options without turning it into a full-time project, Business Loan Warrior gives you a practical place to start. You can explore customized offers, check pre-approval without affecting credit, and find financing that fits your business instead of forcing your business to fit the loan.