You've got a real business idea, real expenses coming due, and no revenue yet. Maybe you need equipment, a small buildout, inventory, software, licensing, or launch capital to get to the point where sales can start. That's a hard place to be, because most founders assume zero revenue means automatic rejection.

It doesn't.

A business loan with no revenue is harder to get, but it's not rare in the way people think. The mistake is applying like an established business when you're still a pre-revenue company. If you don't have sales history, you need to replace it with something else lenders can evaluate. That means building a funding case the way an underwriter sees it: risk, repayment, backup support, and credibility.

That's the mindset shift that matters. You're not asking a lender to ignore the absence of revenue. You're giving them other reasons to believe the deal still makes sense.

Table of Contents

- Why 'No Revenue' Does Not Mean 'No Funding'

- How Lenders Evaluate You Without Revenue

- Finding the Right Loan When Revenue Is Zero

- Alternative Funding Sources to Fuel Your Launch

- Your Strategy for a Successful Application

- Building a Fundable Future for Your Business

Why 'No Revenue' Does Not Mean 'No Funding'

A founder with zero sales usually hears the same thing from banks: come back later. The business may be legitimate, the plan may be sound, and the owner may be fully committed, but the file still stalls because traditional lenders want proof of repayment from operating history.

That's why so many founders feel stuck. They need money to generate revenue, but lenders want revenue before they'll lend money.

The financing gap is real. Only about 48% of small businesses successfully meet their full financing needs, leaving 52% either completely unfunded or only partially financed. Traditional lenders often require annual revenues exceeding $100,000, which excludes many pre-revenue businesses, according to Capital Bank's summary of small business loan statistics.

That number matters because it tells you your situation isn't unusual. It's structural. A lot of businesses aren't failing to get funded because the idea is weak. They're failing because they're trying to fit a bank-style credit box that was built for operating companies, not early-stage ones.

Practical rule: If revenue is zero, stop trying to win with revenue-based arguments. Win with preparedness, personal strength, and a credible repayment story.

A lender still wants the same answer to one basic question: why should they believe this money comes back? When revenue isn't available, the file shifts toward other evidence. Your credit profile matters more. Your business plan matters more. Your cash management matters more. Your own cash in the deal matters more.

That's why a business loan with no revenue isn't really about “finding a lender who doesn't care.” It's about finding the lenders and products designed to look at a different kind of evidence.

Some founders should pursue a small loan first, not the biggest one they think they need. Some should use debt only for equipment that clearly supports launch. Some should avoid debt entirely until they tighten the plan. Those are judgment calls, and they matter more at zero revenue than they do later.

How Lenders Evaluate You Without Revenue

When there's no sales history, underwriters don't stop evaluating risk. They just change what they use. The cleanest way to understand it is through the 5 Cs of credit: character, capacity, capital, collateral, and conditions.

Character matters more than founders expect

At this stage, you are a big part of the credit decision. Character includes personal credit, your payment habits, prior borrowing behavior, and whether your background fits the business you're starting.

If you've got strong personal credit, clean recent history, and direct experience in the industry, you've already improved the file. If your credit is shaky and your experience is thin, the lender sees two risks instead of one.

What helps here:

- Strong personal credit profile: Lenders want evidence that you handle obligations responsibly.

- Relevant operating experience: A chef opening a food concept looks different from a first-time owner with no sector background.

- Consistent personal financial behavior: Fewer surprises in your personal accounts usually make underwriting easier.

Capacity gets replaced by projections and personal stability

Capacity normally means current ability to repay from business cash flow. With no revenue, that shifts toward projected performance, burn discipline, and whether the founder has enough stability to bridge the startup period.

For no-revenue startups, lenders look closely at projected EBITDA margins, with targets in the 15% to 25% range by Year 2, a manageable burn rate, and an owner equity injection of 10% to 20%, as described in SoFi's overview of startup business loans with no revenue.

That doesn't mean your spreadsheet needs to be flashy. It means it needs to make sense.

If your plan says expenses stay low while sales ramp quickly, an underwriter will ask what specifically drives that result. If you can't explain it simply, the projection won't carry weight.

A believable forecast usually includes:

- A clear use of funds tied to launch steps.

- A revenue model that shows how customers are acquired and how sales start.

- Expense assumptions that match the actual conditions of your industry.

- A runway view showing how long the capital lasts if sales start slower than expected.

Capital collateral and conditions still count

Capital is your own money in the deal. Founders often underestimate how much this affects lender confidence. If you're asking a lender to fund everything while you put in nothing, the file gets weaker fast.

Collateral can also change the conversation. Equipment, vehicles, or other business-use assets can support lending where unsecured borrowing would fail. This doesn't solve every problem, but it can make approval more realistic.

Conditions refers to the business environment and purpose of the loan. Some uses of funds are easier to underwrite than others. Equipment with a direct business purpose is easier to explain than a broad request for “startup expenses.” A focused funding request tells the lender you've thought through what you need and why.

A strong no-revenue applicant usually looks like this:

- Personal finances are under control

- The business plan is specific, not generic

- The owner has some cash in the deal

- The funding request matches a clear business purpose

- The repayment story works even if launch takes longer than hoped

Finding the Right Loan When Revenue Is Zero

Not every funding product is built for a startup. Some are realistic. Some are expensive but situationally useful. Some should only be touched if you understand the downside completely.

The option most founders should check first

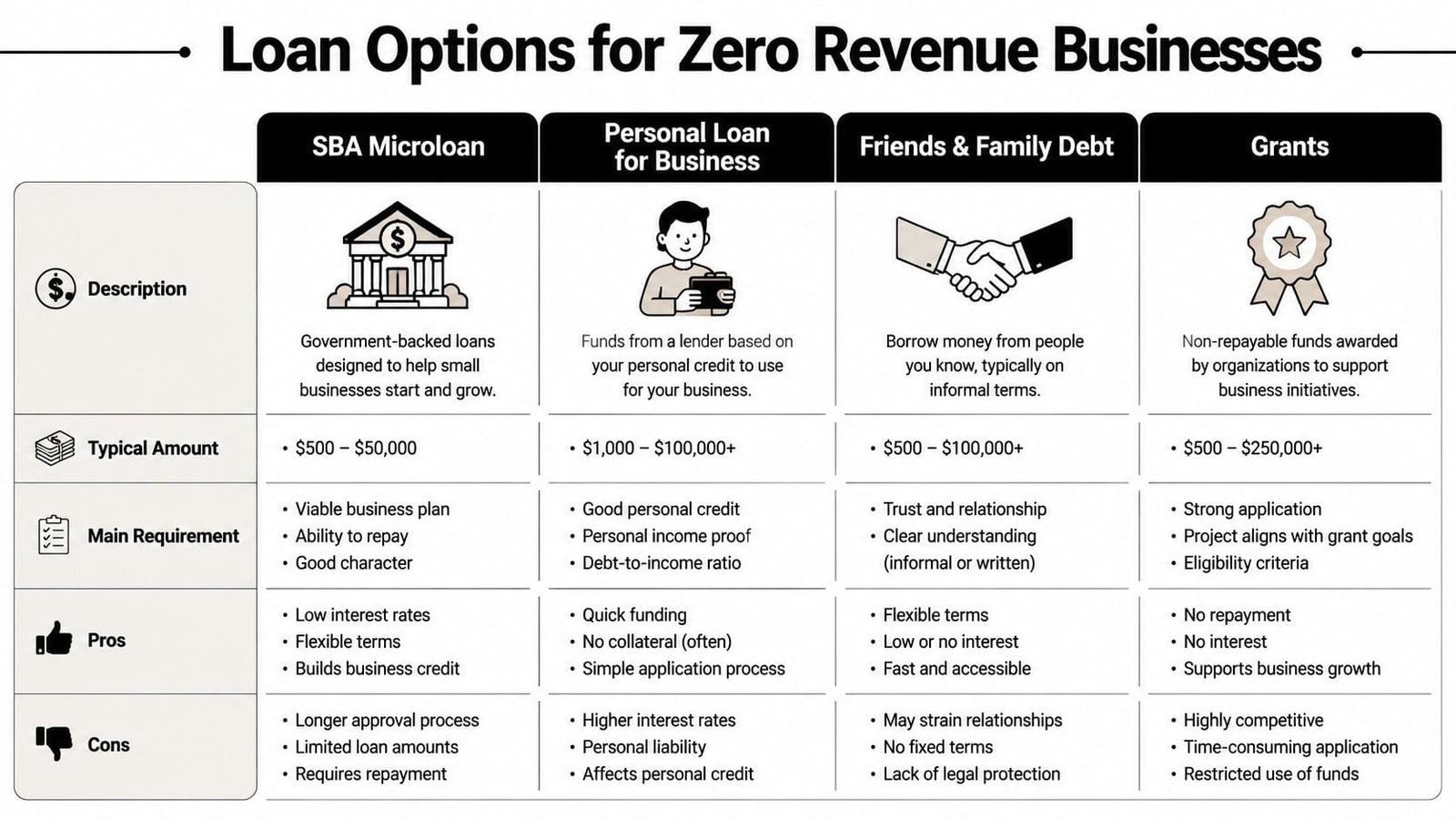

For many pre-revenue businesses, the best starting point is the SBA Microloan. It exists closer to the actual startup world than a standard bank term loan does.

SBA Microloans offer up to $50,000, with an average loan size of $13,000, through nonprofit CDFIs and don't require business revenue. They often focus on personal credit above 650, a detailed business plan, and financial forecasts, according to Startup Science's summary of no-revenue startup loan options.

That matters because the underwriting logic fits early-stage companies better. Instead of asking, “Show me your current revenue,” the lender is asking, “Show me why this business is viable and why you're the person to execute it.”

SBA Microloans are often best for:

- Equipment purchases: Small kitchen equipment, shop tools, POS systems, or launch hardware

- Working capital: Limited startup operating needs with a defined plan

- Inventory: Modest opening stock with a clear path to sale

- Service businesses: Founders who need a manageable amount to begin operations

The trade-off is size. If your real need is much larger, a microloan may only cover the first stage.

Other funding paths that can work

A personal loan used for business purposes can make sense when the business itself can't yet qualify, but the owner's credit is strong. This is common for founders who need a smaller amount and want faster underwriting. The risk is obvious. The debt sits on your personal profile, and repayment remains your responsibility even if the business launch slips.

Friends and family debt can also work if it's documented properly. This sounds informal, but it shouldn't be. If someone lends you money, put the terms in writing, define repayment clearly, and treat it like a real obligation. Sloppy agreements damage both cash flow and relationships.

Grants deserve a place on the list even though they aren't loans. They're competitive and usually narrower in scope, but they're attractive because there's no repayment. If your business fits a specific mission, geography, founder demographic, or community purpose, grants can reduce how much debt you need.

For founders exploring revolving capital later, this guide on whether startups can get a business line of credit with no revenue is useful. A line of credit can be powerful, but many pre-revenue businesses are better served by a simpler first-stage structure.

The right product is the one that matches the stage of the business. Early founders get into trouble when they borrow for flexibility when what they really need is discipline.

No-Revenue Funding Options Compared

| Funding Type | Best For | Typical Amount | Key Requirement |

|---|---|---|---|

| SBA Microloan | Founders needing structured startup capital with lender support | Up to $50,000, average $13,000 | Personal credit, business plan, forecasts |

| Personal Loan for Business | Owners with strong personal credit funding early launch costs | Qualitative only | Personal repayment strength |

| Friends & Family Debt | Flexible early support when both sides want simple terms | Qualitative only | Written agreement and trust |

| Grants | Businesses that fit a targeted mission or eligibility group | Qualitative only | Strong application fit |

A few practical judgments matter here.

- Use SBA Microloans for focused startup needs: They're often the cleanest fit for pre-revenue businesses that can present a serious plan.

- Use personal loans carefully: They're simple on the front end but can strain personal finances if launch takes longer.

- Use friends and family debt professionally: A handshake isn't enough when money is involved.

- Use grants to reduce debt, not delay action forever: Apply, but don't build your whole launch around waiting.

Alternative Funding Sources to Fuel Your Launch

Debt isn't always the best first move. Sometimes the smartest funding stack for a new business combines a small loan with non-debt capital, or skips borrowing entirely until the launch has more proof behind it.

When grants fit better than debt

A community-oriented food concept, childcare provider, creative studio, or mission-driven local business may be better served by grants than by immediate borrowing. Grants take work. Applications are detailed, and eligibility can be narrow. But they don't pressure the business with repayment before the first stable sales cycle arrives.

A founder in that situation might use grant dollars for licensing, a small equipment package, or program development, then borrow later only after operations are underway.

How crowdfunding can do two jobs at once

Reward-based crowdfunding works best when the product is easy to explain and easy to pre-sell. Consumer products, design-led brands, specialty goods, and highly visual concepts often fit here.

The advantage isn't just cash. Crowdfunding can also validate demand. If strangers are willing to put money down before launch, that tells you something useful about the market. If they aren't, that tells you something useful too.

For a broader look at non-revenue funding paths, review these practical startup funding options without revenue.

Some founders borrow too early for ideas the market hasn't confirmed. Validation capital is often safer than repayment capital when the business is still proving demand.

What accelerators really offer

An accelerator can be a fit when the company needs structure, mentoring, and network access as much as money. That tends to matter most for founders selling something repeatable and scalable, especially if outside expertise can tighten the model quickly.

The trade-off is control. You may give up equity, follow a structured program, and shape the business around investor expectations rather than your original pace.

Other alternatives sit somewhere in between:

- Equity crowdfunding: Useful when your audience wants to support the business as backers or owners, but it requires a public-facing raise and strong communication.

- Strategic partners: A supplier, distributor, or launch customer may provide favorable terms if your business solves a real need for them.

- Founder savings: Not glamorous, but often the cheapest capital available if used carefully and within a clear plan.

The point isn't to avoid loans at all costs. It's to avoid using debt where a softer form of capital would give the business more breathing room.

Your Strategy for a Successful Application

Most weak applications fail before underwriting starts. The founder asks for money first and builds the case second. That order needs to be reversed.

Build the file before you fill out the form

When revenue is zero, your application package has to do more work. You need documents that answer lender questions before the lender asks them.

Start with these:

- Business plan: Not a motivational essay. A clear explanation of what you sell, who buys it, how you'll reach them, and what the money will do.

- Use of funds list: Show exactly where the loan goes.

- Financial projections: Monthly at the beginning, with assumptions you can defend.

- Personal financial information: Be ready for lenders to evaluate you, not just the company.

- Formation and operating documents: Keep everything organized and current.

A lot of founders sabotage themselves with vagueness. “Marketing,” “operations,” and “growth” aren't enough. A lender wants to know what gets purchased, what gets launched, and what that should produce.

Write projections that survive scrutiny

Many no-revenue files either become credible or fall apart during this phase. You don't need fantasy upside. You need a model that reflects the actual pace of customer acquisition, delivery, and expense buildup.

A useful forecast usually includes three views:

- Base case: What happens if launch goes roughly as planned.

- Conservative case: What happens if sales start slower.

- Use-of-funds timing: When the borrowed money gets spent.

If you need help structuring that, this guide on building a cash flow forecast that supports your loan strategy is worth reviewing.

A cosigner can materially strengthen a weak file. Securing a cosigner with a FICO score over 720 can boost approval odds by 40% to 50%, and startups with strong detailed business plans see approval rates around 60% from programs like the SBA, compared with 15% for those without a solid plan, according to Experian's guidance on startup business loans with no money.

That tells you where to focus. If the plan is thin, fix that first. If your credit profile is borderline, a stronger borrower in the file may help. If neither exists, the best decision may be to pause and improve the package before applying.

A short walkthrough can help frame what lenders are listening for during review.

Prepare for the underwriting conversation

Underwriting is not a trap. It's a stress test. The lender is checking whether your story stays coherent when they push on it.

Expect questions like:

- Why this amount and not less

- What happens if launch is delayed

- What personal liquidity or support exists

- Why you're qualified to execute

- How repayment works before revenue stabilizes

Answer plainly. If the plan depends on everything going right, it's not ready. The stronger answer usually includes a backup path, a smaller first phase, or personal support that carries the business through early months.

Underwriter lens: They don't need certainty. They need a borrower who understands the risks, has prepared for them, and isn't hiding from the weak spots.

A good application feels calm, specific, and complete. A weak one feels rushed, oversized, and vague.

Building a Fundable Future for Your Business

Getting a business loan with no revenue is rarely about proving the business is already mature. It's about proving the business is fundable now because the founder has done the work to reduce uncertainty.

That means thinking like an underwriter, not just like an owner. Show personal strength. Show a credible plan. Show disciplined use of funds. Show how this first round of capital gets the company to the next milestone.

The founders who handle this best usually follow a simple pattern:

- They borrow for a defined purpose, not for vague breathing room

- They present realistic projections, not heroic ones

- They strengthen the file with personal credit, cash injection, or a cosigner when needed

- They choose funding that fits the stage, even if the amount is smaller than they hoped

- They treat the first loan as a bridge to future financing, not a permanent solution

Once the business starts producing revenue, the financing conversation changes. More lenders open up. Better pricing becomes possible. Larger products may become realistic. Business credit becomes more relevant. That first funded step can lead to stronger options later, but only if the first deal is structured carefully and used well.

The immediate goal isn't just approval. It's using capital in a way that makes the business more financeable the next time around.

If you're ready to explore a practical funding path, Business Loan Warrior lets you check pre-approval through a single no-fee application without affecting credit, compare customized options, and move from uncertainty to a lender-ready plan faster.