Your line cook is in the middle of dinner service. The fryer starts tripping. The reach-in cooler won't hold temperature. The POS terminal freezes at the worst possible moment. None of that feels like a finance decision. It feels like an operations emergency.

But for restaurant owners, equipment problems become financing decisions fast. The wrong move drains cash you needed for payroll, food orders, and marketing. The right move keeps service running and gives you room to breathe. That's why restaurant equipment financing matters so much. It isn't just about getting approved. It's about matching the payment structure to how your store earns money.

Most guides stop at rates, approvals, and loan types. That's useful, but incomplete. The core issue is whether the payment schedule fits your cash flow. A fixed payment that looks manageable in a strong month can become a strain when traffic softens, seasonality hits, or one location underperforms. That mismatch is where good deals turn into bad pressure.

Table of Contents

- Why Smart Equipment Financing Is Your Secret Ingredient

- Comparing Your Restaurant Equipment Financing Options

- Calculating the True Cost of Your New Equipment

- Qualifying for Restaurant Equipment Financing

- The Application Process From Start to Funding

- How to Choose the Right Lender and Avoid Pitfalls

- Frequently Asked Questions About Equipment Financing

Why Smart Equipment Financing Is Your Secret Ingredient

A broken combi oven during service is expensive. Not just because of the repair or replacement bill, but because it disrupts output, slows tickets, and forces your team to work around a bottleneck. Owners often react by paying cash because debt feels risky. In restaurants, that instinct can backfire.

Restaurant equipment financing is often the cleaner decision because it protects working capital. In a business where profit margins average 3% to 5% and where food and labor already take so much of the operating budget, cash on hand matters more than theoretical savings from writing one large check. Restaurant financing data summarized by REIL Capital makes that margin pressure plain.

The financing market exists for a reason. The equipment finance industry saw nearly 6% growth in new volume through 2025, with credit approval rates staying favorable at over 78%, according to restaurant financing market figures from GoFoodservice. The same source notes that restaurant equipment financing typically comes with rates in the 8% to 30% range and can cover 80% to 100% of the purchase price.

That tells you two things. First, financing is common. Second, lenders understand that equipment is core to restaurant operations, not a luxury purchase.

Financing protects the money you actually need

Owners usually think about the equipment itself. Lenders think about repayment. Strong operators think about cash flow first.

Use financing to preserve cash for the expenses that can't wait:

- Payroll: Your team has to be paid whether your new walk-in is financed or not.

- Inventory: Product buys create revenue. An empty kitchen doesn't.

- Marketing: Promotions, digital ads, and local outreach often get cut first when cash gets tight.

- Repairs and surprises: Restaurants never run on a perfectly smooth calendar.

Practical rule: The best equipment financing keeps the kitchen moving without starving the rest of the business.

Smart financing is about timing, not just borrowing

The strongest use of restaurant equipment financing isn't panic replacement. It's planned replacement and planned growth. That means financing a prep line before the old one fails, adding refrigeration before a menu expansion, or upgrading POS hardware before service friction starts costing you tickets and guest experience.

When owners treat financing as a scheduling tool instead of a rescue tool, they negotiate better, choose better terms, and avoid desperate decisions. That's the primary advantage.

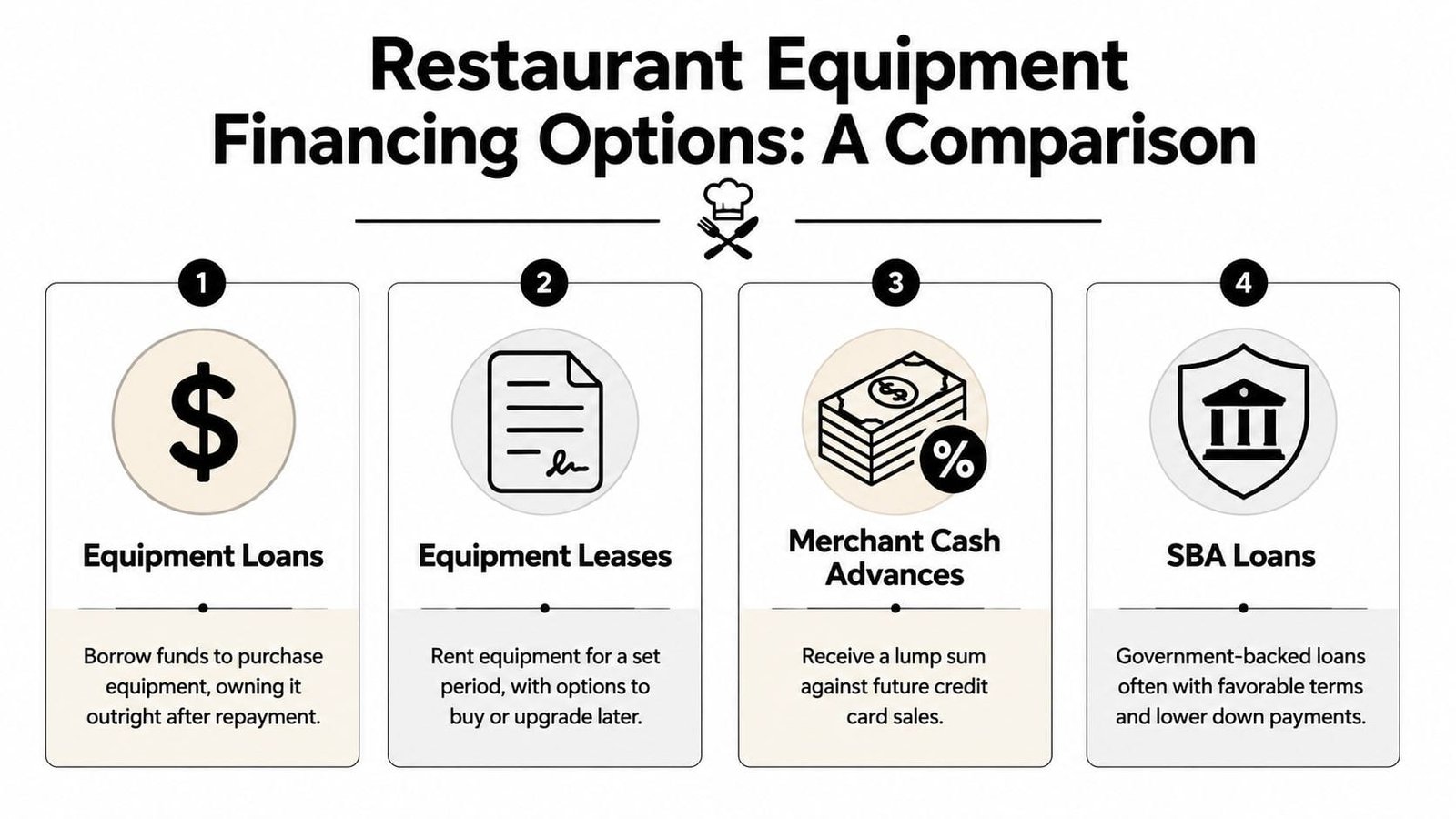

Comparing Your Restaurant Equipment Financing Options

A busy Saturday service can hide a financing mistake for months. Then February hits, sales soften, and a payment structure that looked manageable in July starts competing with payroll, food orders, and rent. That is why the right question is not just which product has the lowest rate. It is whether the repayment schedule fits how your restaurant collects cash.

A six-year oven should not be financed with a product that wants its money back in nine months. That term-revenue mismatch is one of the most common mistakes I see. Owners focus on approval and monthly payment. The actual risk shows up later, when the equipment is still useful but the repayment pressure has already drained working capital.

Equipment loans

An equipment loan is the cleanest option for many restaurants. You finance a specific asset, the equipment usually secures the loan, and you own it at the end.

This structure fits durable, revenue-critical equipment such as combi ovens, refrigeration, dish machines, mixers, and POS hardware. It works best when the equipment life is long enough to support the loan term and the payment can fit inside your slower months, not just your busy ones.

Best for: Established operators buying core equipment they expect to keep for years.

Main advantage: Clear ownership and predictable repayment.

Main drawback: The payment is fixed even when your sales are not.

For owners comparing structures beyond restaurant-specific programs, this commercial equipment financing and machinery guide gives a broader look at how asset-backed financing is set up.

SBA loans

SBA-backed financing usually makes sense when the project is larger, the repayment horizon needs to be longer, or the monthly burden on cash flow needs to stay lower. The U.S. Small Business Administration explains that SBA 7(a) loans can be used for equipment purchases and other business purposes, while CDC/504 loans are designed for major fixed assets.

That longer structure can help a restaurant avoid forcing a large capital project into a repayment schedule the business cannot comfortably support. The trade-off is time. SBA loans usually require stronger documentation, more lender review, and more patience from the borrower.

Best for: Large equipment packages, buildout-related assets, and operators who want longer repayment terms.

Main advantage: Lower monthly strain relative to the project size.

Main drawback: Slower process and more underwriting.

Lease-to-own and operating leases

Leasing can protect cash better than a traditional loan, but owners need to separate two very different products. A lease-to-own agreement is built around eventual ownership. An operating lease is closer to renting, with flexibility at the end if you expect technology or equipment needs to change.

Credit Key's restaurant equipment financing playbook notes that lease-to-own structures often carry effective APRs of 8% to 15% and preserve working capital. The same source explains that a true operating lease can stay off the balance sheet under certain GAAP and IFRS treatments, which can improve debt-to-equity ratios.

Leasing is often a better fit for equipment with shorter refresh cycles, uncertain menu direction, or multi-unit operators who want upgrade flexibility. It is less attractive for equipment you know you will keep for a decade, because the total cost can end up higher than a straightforward loan.

Best for: Owners who want lower upfront cash use or expect equipment needs to change.

Main advantage: Better near-term liquidity.

Main drawback: End-of-term terms matter. Buyout formulas, return conditions, and renewal pricing can change the economics fast.

Lines of credit and cash advance products

These products solve speed problems, not term-matching problems.

A line of credit can help with smaller add-on purchases, freight, installation overruns, or a phased equipment rollout. A merchant cash advance or similar product is usually a poor match for durable kitchen equipment because repayment tends to come out too quickly and at too high a cost.

Best for: Small gaps, short timing issues, and secondary costs around an equipment purchase.

Main advantage: Fast access to capital.

Main drawback: Short repayment cycles can squeeze cash flow before the equipment has paid for itself.

The practical rule is simple. Match long-life equipment with longer repayment. Match variable restaurant sales with a payment structure your business can carry during the slow season, not just during peak weeks. That is how financing stays useful instead of becoming another operational problem.

Calculating the True Cost of Your New Equipment

Owners often focus on the purchase price because that's what the vendor shows first. Lenders know the essential question is monthly burden. Your business doesn't repay equipment with sticker price logic. It repays from operating cash flow.

What the monthly payment really tells you

A useful benchmark comes from The Restaurant Warehouse financing calculator guide. For a 5-year, $100,000 equipment loan, a 10% rate produces a monthly payment of about $2,100, while a 25% rate pushes that payment to about $2,800. The same source notes that borrowers with FICO scores above 680 typically access the 7% to 12% range.

That spread changes daily operations. A payment that starts with a 2 instead of a 3 may decide whether you can keep inventory levels healthy in a slower stretch. The equipment may be identical. The financing burden is not.

The same source also notes that high-rate structures can dramatically increase total cost over the term. That matters because owners often compare offers based only on approval speed.

Sample repayment scenarios

| Interest Rate (APR) | Estimated Monthly Payment | Total Repayment Cost | Total Interest Paid |

|---|---|---|---|

| 10% | about $2,100 | qualitatively lower than the high-rate scenario | qualitatively lower than the high-rate scenario |

| 25% | about $2,800 | qualitatively much higher than the lower-rate scenario | qualitatively much higher than the lower-rate scenario |

This is why I tell owners to calculate the payment before they negotiate the equipment package. Once a vendor bundles install, warranty, and add-ons into one big number, many operators stop evaluating the debt correctly.

- Look past the monthly teaser: A lower starting payment can still hide a costly structure.

- Ask whether the offer uses APR or factor-style pricing: If the quote isn't transparent, slow the process down.

- Model the payment against a soft month: Don't test affordability using your best month.

- Separate must-have equipment from nice-to-have add-ons: Financing is cleaner when the asset list is disciplined.

For owners trying to preserve cash at closing, this zero-down equipment financing guide for startups is worth reviewing, especially if you're weighing upfront liquidity against long-term cost.

If a payment only works when sales are strong, it doesn't work.

Qualifying for Restaurant Equipment Financing

A lender reviewing your file is trying to answer one practical question: will this payment still get made in a weak month, not just in a strong one?

That matters more in restaurants than in many other industries because cash flow rarely arrives in a straight line. Weather shifts traffic. Patio season changes average ticket. Holidays lift one quarter and leave the next one tight. If financing terms ignore that pattern, a loan that looked affordable on paper can start competing with payroll, food orders, and rent.

What underwriters look for

Underwriters do care about the equipment, especially whether it holds value and fits the business. They care even more about repayment capacity and consistency.

For a restaurant, that usually comes down to a few questions:

- Does the business generate enough cash after normal operating expenses?

- Are deposits reasonably consistent, even if sales are seasonal?

- Does ownership have a track record of paying obligations on time?

- Do the financial statements and tax returns tell the same story?

- Does the requested term fit the useful life of the equipment?

The last point gets overlooked. A combi oven or walk-in cooler can support a longer structure than smallwares or lower-value add-ons. If the equipment will produce value for years, the financing can often be stretched in a way that lowers payment pressure. If the equipment may need replacement sooner, a long term can leave you paying for an asset after its best working years are over.

SBA financing comes up often for that reason. The U.S. Small Business Administration explains that 7(a) loans can be used for equipment and may offer longer repayment periods than many conventional options, depending on use of proceeds and lender structure. Longer terms can help monthly cash flow, but they are only helpful when the equipment life and the restaurant's sales cycle support them.

https://www.sba.gov/funding-programs/loans/7a-loans

A strong file gives the lender confidence that the debt fits the business, not just the asset.

Your lender checklist

Bring a complete file before you apply. It changes the conversation from guesswork to underwriting.

- Recent business financials: Profit and loss statements and balance sheets show whether the restaurant produces enough cash to carry new debt.

- Business bank statements: These show deposit patterns, seasonal swings, and whether cash regularly runs tight before major bills clear.

- Tax returns: Lenders use them to confirm that reported income matches the internal numbers.

- Equipment quote: A vendor invoice should list the exact items, installed cost, and any soft costs being included.

- Ownership and entity documents: These confirm who owns the business and who has authority to sign.

- Debt schedule, if applicable: Existing loan and lease payments help the lender see how much fixed payment load the business already carries.

A short educational overview may help if you want a refresher before you gather documents:

What makes an application stronger

Specificity helps.

"We need kitchen equipment" sounds unfocused. "We are replacing failing refrigeration and adding prep equipment for a higher-margin catering line" gives the lender a clearer operating reason and a cleaner credit story.

Explain uneven months before the underwriter has to ask. A seasonal store, a campus-adjacent location, or a concept with sharp holiday peaks can still qualify. The application gets stronger when ownership shows it understands those cycles and has chosen a payment structure that can survive the down periods.

A good approval is not just approval. It is a payment schedule your restaurant can carry in February, not only in December.

I also advise owners to separate replacement equipment from expansion equipment when possible. Replacement usually protects current revenue. Expansion assumes future revenue. Lenders view those two requests differently, and they should. Mixing them into one large ask can make a practical request look more speculative than it is.

The Application Process From Start to Funding

The financing process feels easier when you treat it like an operating system, not a one-time scramble. The owners who get clean approvals usually do a few things in order and don't skip steps.

Start with the equipment plan

Begin internally, not with a lender. List the exact equipment, the vendor, the full installed cost, and whether each item is essential now or can wait. Don't mix emergency replacements with wish-list upgrades unless both are supportable.

Then pressure-test the payment against your business reality:

- Map the revenue cycle: Look at strong months, weak months, and any seasonal dips.

- Match the asset to the term: Long-life equipment can justify a longer structure. Short-life or uncertain-use equipment deserves more caution.

- Decide what cash must stay untouched: Payroll, inventory, rent, and reserve needs should set the borrowing plan.

- Gather documents early: Clean financials speed decisions and reduce back-and-forth.

Review the offer like an operator

Once quotes arrive, owners tend to jump to rate. That's too narrow. The offer has to work in the store, not just on paper.

Review these points before signing:

- Repayment rhythm: Monthly, weekly, or another cadence. The schedule should fit how cash lands.

- Collateral and guarantees: Understand what secures the debt and what personal obligations exist.

- Prepayment terms: If business improves, can you pay down early without punishment?

- Documentation quality: A clear, readable agreement is usually a better sign than a fast, vague one.

A good process also includes comparison. Don't stop at the first approval, especially when terms vary in structure even if the headlines look similar.

Funding should solve the problem you actually have

Fast funding is helpful when a unit is down. But speed can distract owners from fit. A loan that closes quickly and strains the business for years isn't efficient. It's just fast.

The right approval should do three things at once. Replace or add the equipment you need, preserve enough cash for operations, and avoid locking the business into a payment pattern that becomes painful in ordinary slow periods.

How to Choose the Right Lender and Avoid Pitfalls

The best lender isn't always the one quoting the lowest rate. In restaurants, the better lender is often the one who understands volatility and structures the repayment to match it.

The hidden cash flow crisis

One of the most overlooked risks in restaurant equipment financing is term-revenue mismatch. Sofi's restaurant equipment financing discussion points to a critical mismatch between equipment loan terms of up to 84 months and the restaurant's operational reality of 3% to 9% margins with seasonal revenue swings. That mismatch can create a hidden cash flow crisis, especially for multi-unit operators.

This is the issue most guides gloss over. A fixed payment doesn't care that patio season ended, a location underperformed, or labor ran hot. If you finance based on average revenue instead of weak-month revenue, you can trap the business in a permanent catch-up cycle.

A fryer at one location should not be underwritten mentally as if the whole brand will rescue that unit if it misses plan. Multi-unit owners make that mistake more often than they admit.

What to ask before you sign

You want clarity, not just approval. Ask direct questions.

- Can the repayment schedule reflect seasonality: If your revenue has predictable swings, ask whether the lender offers flexibility that tracks business reality.

- What happens if I want to prepay or refinance: Some agreements are far less flexible than they seem up front.

- How transparent is the pricing: If the lender struggles to explain the economics in plain English, keep looking.

- How often do you work with restaurant operators: Industry familiarity matters because restaurant cash flow behaves differently from many other sectors.

For a broader look at lender types and how they differ, review this equipment financing lenders guide.

A cheaper loan that breaks your cash flow is more expensive than a slightly higher-priced loan that the business can comfortably carry.

What usually works and what usually doesn't

What works is simple. Match durable equipment with durable repayment. Keep room in the operating account. Use loans for core assets and use flexible working capital sparingly.

What doesn't work is financing long-life equipment with short, expensive products just because approval was easy. Another common mistake is borrowing based on optimism after a few strong months. Lenders can price optimism. Your bank account cannot repay with optimism.

Frequently Asked Questions About Equipment Financing

Can I finance used restaurant equipment

Yes, many lenders will finance used equipment. The main trade-off is that older equipment may come with shorter terms or higher pricing because the remaining useful life is shorter. That makes used equipment attractive when the purchase price is compelling and the seller is credible, but less attractive when the lower price is offset by tighter financing.

The practical move is to compare the full payment structure, not just the equipment discount.

Will applying affect my personal credit

It depends on the lender and the product. Some financing processes begin with a lighter prequalification review, while others move quickly to a harder credit review or require a personal guarantee. Ask that question before you submit anything.

Don't assume every application works the same way. Good lenders explain the credit review process clearly before they pull reports.

How should I think about Section 179

Think of Section 179 as a tax conversation, not a financing decision by itself. Some equipment financing structures can support tax advantages tied to ownership, while true leases may be treated differently. The financing should still make sense operationally even if the tax treatment is helpful.

Have your CPA review the specific structure before you sign. Tax benefits are valuable, but they don't rescue a bad payment schedule.

How fast can funding happen

Timelines vary by lender, equipment type, documentation quality, and loan structure. Simple asset-backed requests with clean paperwork can move faster than larger or more document-heavy requests. SBA-related requests generally require more process than a straightforward equipment deal.

If speed matters, the owner's preparation matters too. Missing statements, vague vendor quotes, and inconsistent financials slow funding more than most borrowers expect.

Is leasing better than buying

Sometimes. Leasing is usually stronger when preserving working capital matters most, when the equipment may need to be upgraded later, or when balance sheet presentation matters. Buying through financing is usually stronger when the equipment is core to the operation and you expect to keep it long enough to justify ownership.

The better question isn't “lease or buy.” It's “which structure fits this asset and this store's cash flow.”

What's the biggest mistake owners make

They underwrite the payment using a good month. Restaurants should underwrite debt using an ordinary month, and then stress-test it against a weak one. That habit alone prevents a lot of avoidable strain.

If you're sorting through restaurant equipment financing and want to compare options without wasting time on mismatched offers, Business Loan Warrior helps owners review specific funding paths through one no-fee application. It's a practical way to check pre-approval, compare structures, and find terms that fit how your restaurant runs.