A competitor's owner calls on Monday. They'll sell a location, a customer list, or a piece of equipment at a discount if you can close fast. Or a supplier offers inventory on terms that could protect your margin for the next quarter, but only if funds hit this week. Your bank relationship may be solid, but that doesn't mean your bank can move at deal speed.

That gap is where hard money business loans enter the conversation. Not as a panic button. As a tool. An expensive one, yes. A risky one, if used carelessly. But in the right situation, speed has economic value, and the cost of waiting can be higher than the cost of capital.

For established companies, especially those doing $20M to $50M in annual revenue, the primary question usually isn't “Can I qualify somewhere?” It's “Is paying more for fast capital the smarter move than missing the opportunity?” That's a different conversation than the usual hard money content aimed at distressed borrowers or first-time investors.

Table of Contents

- When Opportunity Knocks Faster Than Your Bank Answers

- What Exactly Are Hard Money Business Loans

- The True Cost of Speed Terms Rates and Fees

- Strategic Use Cases When Hard Money Is a Smart Move

- Hard Money Loans vs Other Business Financing

- How to Get Approved and Prepare Your Application

- Let Business Loan Warrior Be Your Guide

When Opportunity Knocks Faster Than Your Bank Answers

A lot of owners learn about hard money the same way. They don't go looking for it until timing turns into the whole deal.

A restaurant group sees a second-generation operator ready to sell a profitable location. A retailer gets a one-time chance to buy inventory before a competitor does. A service company needs equipment now because a signed contract starts next month, not next quarter. The business is healthy. The opportunity is real. The problem is that conventional underwriting moves on bank time, not operating time.

In those moments, owners usually discover an uncomfortable truth. Cheap capital is often slow capital. Fast capital is rarely cheap.

Hard money exists for that exact gap. It's built for borrowers who have a financeable asset and a time-sensitive use of funds, but not the luxury of waiting through a long approval process. If your business is staring at an opportunity that goes stale while the file sits in underwriting, it helps to understand the short-term options available, including quick short-term business loans for urgent cash flow needs.

Speed only matters when delay changes the outcome. That's when premium-priced capital deserves a serious look.

The mistake I see most often is treating hard money like either a miracle solution or a desperate last resort. It's neither. It's more like a bridge crane on a jobsite. Powerful, useful, and absolutely the wrong thing to use casually. If the asset is solid and the exit is clear, it can solve a real business problem. If the margin for error is thin, it can magnify a bad one.

What Exactly Are Hard Money Business Loans

A hard money business loan is short-term capital secured primarily by a hard asset and secondarily by the borrower's broader financial profile. The lender's first question is usually, “What can secure this loan, and how do we get repaid?” That is a very different conversation from a bank asking for a full operating history, covenant package, and committee approval.

For a mid-market company, that distinction matters. A $30 million manufacturer buying a competitor's warehouse at a discount may use hard money not because the business is weak, but because the closing window is tight and the collateral is clear. In that case, the loan is less about rescue financing and more about buying time until cheaper capital can replace it.

The underwriting centers on two things.

First, collateral. Second, exit.

Collateral gives the lender protection if the deal goes sideways. The exit gives the lender confidence that this is a temporary loan, not a long-term capital solution forced into the wrong job. A credible exit might be a refinance after stabilization, a property sale, a customer payment event, or a recap once the balance sheet reflects the new asset.

A useful comparison is commercial pawn lending with better documentation, more diligence, and larger stakes. The lender is still asking a basic question: if they had to liquidate or step into the collateral position, how much protection is really there?

That is why lenders focus on assets with resale value and a clean path to lien perfection, such as:

- Commercial real estate tied to operations, expansion, or a pending acquisition

- Equipment with a reliable secondary market

- Transitional or construction-related assets that are temporarily outside bank credit standards

- Business-use property with enough equity to support a conservative advance

For established businesses, the underlying issue is not whether hard money is expensive. It usually is. The fundamental concern is whether speed creates enough enterprise value to justify that cost. If a delayed closing kills a margin-rich expansion, forfeits an inventory buy at a discount, or forces a company to miss a contract start date, the cheaper loan can become the more expensive choice.

That is where owners get this product wrong. They treat hard money as distressed capital only. In practice, strong companies use it as interim capital when timing, collateral, and payoff visibility line up.

The trade-off is unforgiving. If the asset value is overstated, or the exit depends on optimistic assumptions, hard money gets dangerous fast. Short maturities leave little room for slow lease-up, delayed permits, or a refinance market that tightens at the wrong moment. Before signing, it helps to run the numbers using a framework for calculating the real cost of a small business loan, including points, legal fees, carrying cost, and the backup plan if your first exit falls through.

Hard money lenders are usually private credit groups, specialty finance firms, or local operators that can make decisions quickly because they are judging a narrower set of risks. They are not trying to compete with banks on price. They compete on speed, flexibility, and willingness to fund situations that do not fit standard credit boxes.

Used well, hard money is bridge capital with a job to do. Used casually, it can turn a timing problem into a balance-sheet problem.

The True Cost of Speed Terms Rates and Fees

Hard money gets expensive in ways borrowers often underestimate. The rate is only the visible part. The true cost sits in the combination of pricing, fees, and a short clock that starts running the day funds hit your account.

What you actually pay for

For an established company, the right question is not “What is the rate?” It is “What is the all-in cost of buying time?”

That cost usually comes from three places. First, interest. Second, upfront points and closing costs. Third, a repayment window short enough to force action. A mid-market borrower can absorb a premium rate for a few months if the capital secures discounted inventory, closes a tuck-in acquisition, or prevents a production delay that would damage margin. The same loan becomes dangerous if the payoff depends on a refinance that is not lined up or an asset sale that slips by one quarter.

I tell owners to model hard money like a rush order in operations. Paying extra can make perfect sense when speed protects profit. Paying extra without a clear use of proceeds just burns cash faster.

If you want a cleaner way to evaluate that trade-off, run the deal through a framework for calculating the real cost of a small business loan before you sign term sheets.

How lenders size the loan

Hard money lenders protect themselves at origination. They do it by controlling loan size against collateral.

You will hear two terms often:

- LTV: Loan-to-value. The loan amount compared with the asset's current value.

- ARV: After-repair value. The projected value after improvements, repositioning, or completion of a business plan tied to the asset.

In practice, lenders stay conservative. They want room for error if construction runs long, a tenant does not sign on schedule, or the refinance market gets tighter. That matters for companies in the $20 million to $50 million revenue range because a collateral shortfall usually means bringing more equity to the table, pledging more assets, or accepting a smaller facility than the deal model assumed.

The first real underwriting question is usually about collateral coverage and exit clarity, not the amount requested.

That is why two borrowers with similar revenue can get very different offers. A borrower with a clean first lien position, realistic valuation support, and a credible payoff source will usually have more room to negotiate than one relying on projected value and optimistic timing.

This overview helps clarify some of the moving parts:

When alternatives may fit better

Hard money is not the only fast capital option. For established businesses that need growth capital but do not want every decision tied to a single asset, other structures can fit better.

IDB Invest's financing toolkit notes that alternatives such as mezzanine debt and revenue-based financing are increasingly common, with ticket sizes from $500K to $20M. The same source says mezzanine debt often carries 12% to 20% interest with equity kickers, while revenue-based financing is often repaid as 2% to 8% of monthly revenue until a cap is reached.

Those options solve different problems. Mezzanine debt can preserve momentum when a company has enterprise value but wants to avoid heavy collateral constraints. Revenue-based financing can work when cash flow is predictable and the business wants payments to flex with performance. Both can be a poor fit if margins are under pressure, revenue swings hard month to month, or ownership does not want to give up economics through warrants or revenue sharing.

A practical cost screen looks like this:

| Cost question | Why it matters |

|---|---|

| Can the opportunity produce enough value before the loan matures? | Short maturities punish slow execution |

| Are points and fees justified by a measurable timing or pricing advantage? | Upfront charges raise the effective borrowing cost on day one |

| Does the exit still work if closing, leasing, permits, or refinancing take longer than expected? | Hard money gets painful when the backup plan is weak |

Strategic Use Cases When Hard Money Is a Smart Move

Hard money earns its keep when speed changes the economics of the transaction. If timing doesn't alter price, access, or profitability, the premium usually isn't justified. For mid-market companies, that distinction is everything.

Acquisitions where speed changes the price

One of the clearest examples is a time-sensitive acquisition. National Debt Relief's discussion of hard money business loans highlights a useful scenario for businesses with $20M to $50M in revenue: a $30M company using a 12% hard money loan to secure an acquisition at a 20% discount can come out ahead of waiting 3+ months for an 7% SBA loan and losing the deal.

That example captures the essential decision. You're not comparing rates in a vacuum. You're comparing outcomes. If the seller values certainty and speed more than an extra few points of price, the fast buyer can win on terms the slow buyer never gets to negotiate.

Hard money stops looking like emergency financing and starts looking like strategic financing at this point. The cost is still high. The return can still justify it.

Bridge financing with a clear exit

Another smart use is a bridge between two known events. A company may need short-term capital now to secure property, fund construction, stabilize operations after expansion, or cover a gap before long-term financing closes.

The key phrase there is known events. Hard money works far better when the exit is visible than when the borrower is “hoping to figure something out later.” Common strong setups include:

- Property acquisition before refinance: You close quickly, improve the asset or documentation, then refinance into cheaper debt.

- Equipment purchase tied to signed demand: The equipment starts producing revenue quickly, and repayment comes from a defined business event.

- Construction or repositioning bridge: The project needs fast capital now, then graduates into another financing structure once it stabilizes.

- Cash flow gap tied to a near-term resolution: For example, a temporary mismatch between a pressing obligation and a credible incoming capital event.

Hard money works best when it buys time for a plan already in motion. It works badly when it substitutes for a missing plan.

Situations where it usually does not work

There are also situations where owners should be skeptical, even if a lender says yes.

If your margin on the underlying opportunity is thin, expensive short-term money can erase it. If your collateral is the crown jewel of the business and the payoff source is uncertain, the downside may be too severe. If the transaction depends on everything going right, from timeline to valuation to refinance market, hard money can turn a manageable risk into a dangerous one.

A quick self-test helps:

- Would I still do this deal if execution takes longer than planned?

- Is there a realistic second exit if the first one fails?

- Am I using speed to capture value, or using debt to rescue a weak idea?

That last question matters most. Hard money can fix a timing problem. It usually can't fix a bad deal.

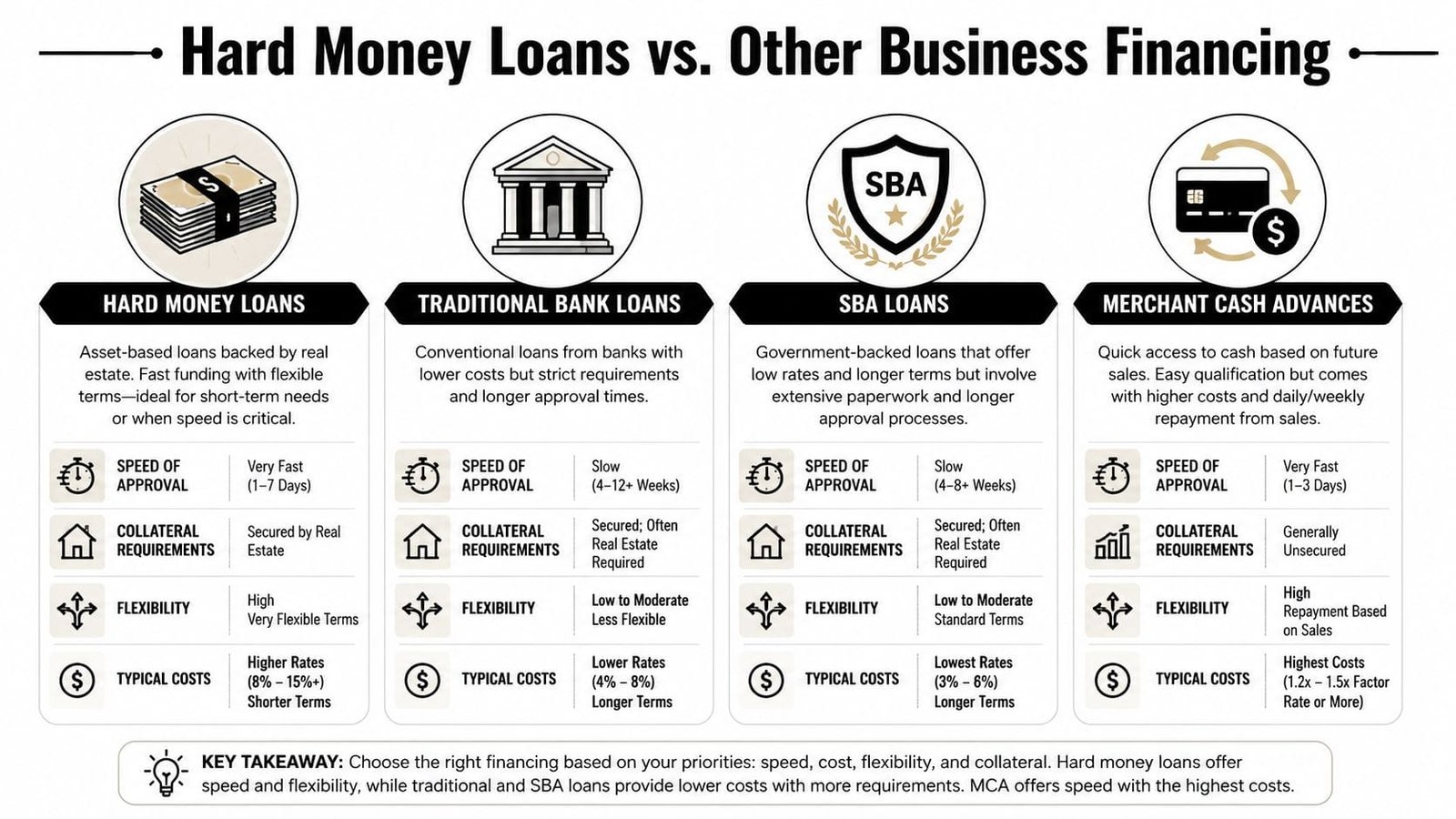

Hard Money Loans vs Other Business Financing

A $35 million manufacturer gets the call every operator wants. A competitor is unloading a facility and specialized equipment at a discount, but the seller wants certainty now, not after 90 days of committee review. In that situation, the financing question is not just “What is cheapest?” It is “What gets this done fast, and does the speed create more value than it costs?”

That is the primary comparison. Mid-market companies rarely look at hard money because they are out of options. They look at it when a bank timeline does not match a business timeline. For a wider view of that financing gap, this article on how alternative lenders are redefining business financing provides useful context.

Financing options at a glance

| Feature | Hard Money Loan | Bank/SBA Loan | Merchant Cash Advance |

|---|---|---|---|

| Primary underwriting focus | Asset value, equity position, exit plan | Credit, cash flow, historical financials, covenants | Revenue stream, card sales, deposit activity |

| Typical speed | Fast, often measured in days or a few weeks | Slow, often measured in weeks or months | Very fast |

| Credit flexibility | More forgiving than banks if collateral is strong | Usually tighter | Often flexible |

| Documentation burden | Lighter, but still requires a clean collateral and payoff story | Heavy | Light |

| Typical term profile | Short-term bridge financing | Longer repayment structures | Very short repayment cycle |

| Typical pricing | Higher cost, often with points and fees | Lowest cost of the three | Can be very expensive on an effective annual basis |

| Best fit | Time-sensitive, asset-backed transaction with a clear exit | Planned growth, working capital, acquisitions with time to underwrite | Immediate liquidity need tied to near-term sales |

How the trade-offs work in practice

Bank and SBA money usually wins on cost. If a company has time, clean financials, and a transaction that can survive a longer underwriting process, lower-cost debt is usually the right choice. For permanent equipment financing, owner-occupied real estate, or stable expansion plans, patience often pays.

Merchant cash advances solve a different problem. They convert future receivables into immediate cash, but the repayment structure can pressure weekly liquidity. For a company with uneven collections or tight operating margins, that pressure can spread from treasury into payroll, purchasing, and vendor relations faster than management expects.

Hard money sits in the middle. It is expensive, but it can be controlled. The loan is usually tied to a specific asset and a specific event, such as a refinance, sale, recapitalization, or receivable collection. That makes it very different from financing that drains cash from daily operations with no clear finish line.

What established businesses should compare before they choose

For companies in the $20 million to $50 million revenue range, analysis is not a simple matter of rate versus rate. It is total economics.

Ask four questions:

What value does speed create?

If fast funding secures discounted inventory, a strategic parcel, or equipment tied to contracted demand, the return may justify a short burst of expensive capital.What is the carry cost if the cheaper loan arrives too late?

Losing the deal, missing a production window, or giving a competitor time to act has a cost too. Owners often ignore that because it does not show up as an interest line item.How exposed is the business if the exit slips?

A bridge loan with a strong second repayment option is one thing. A short-term loan backed by core collateral with no fallback is another.Which structure creates the least operational strain during the hold period?

A higher nominal rate can still be the safer choice if repayment is deferred and the loan does not squeeze weekly cash flow.

That last point matters more than many borrowers realize.

I have seen healthy middle-market companies reject hard money on price, then accept a structure that looked cheaper but restricted operations, delayed closing, or forced cash sweeps at the wrong time. Cheap capital is not cheap if it costs the deal.

Where hard money wins, and where it does not

Hard money is usually the better tool when the company has a financeable asset, a short deadline, and a credible exit already mapped out. It also fits cases where management wants to act first and refinance into lower-cost debt after the asset is stabilized or the documentation catches up.

It is usually the wrong tool for ongoing operating losses, vague turnaround plans, or situations where the business is pledging mission-critical collateral to buy time. In those cases, speed does not solve the core problem. It just makes the clock more expensive.

The right comparison is not hard money versus bank debt in theory. It is speed-adjusted value versus downside if the plan takes longer or costs more than expected.

For established businesses, that framing changes the conversation. Hard money is not just emergency capital. It is a tactical bridge for narrow situations where timing has measurable economic value, and management is disciplined enough to treat the loan like a tool, not a habit.

How to Get Approved and Prepare Your Application

Hard money underwriting is lighter than bank underwriting, but it isn't casual. The fastest approvals usually go to borrowers who make the lender's job easy. That means telling a clean story about the asset, the use of funds, and the exit.

What lenders want to see first

Lenders usually care about three things before anything else.

The collateral

They need to understand what the asset is, what it's worth, how liquid it is, and where their security sits. If the appraisal is weak, title is messy, or the asset is hard to value, the process slows down quickly.

The borrowing entity

Even in asset-based lending, entity documents matter. The lender wants to know who owns the business, who can sign, and whether the structure creates legal friction.

The exit strategy

This is the heartbeat of the file. Refinance, sale, recapitalization, or payoff from a specific business event. “We'll probably figure it out” isn't an exit strategy.

A practical prep list usually includes:

- Asset package: Appraisal or valuation support, photos, equipment list, property details, or project information.

- Entity documents: Formation documents, operating agreement, and signer authorization.

- Use of funds summary: Exactly where proceeds go and why timing matters.

- Exit memo: A short written explanation of how and when the loan gets repaid.

- Supporting financial context: Enough information to show the business can carry the plan, even if the lender isn't underwriting like a bank.

A strong hard money application doesn't try to impress with volume. It removes unanswered questions.

How to vet the lender before you sign

This matters more than many borrowers realize. LendingTree's overview of hard money business loans notes a major transparency gap in the market. Federal licensing isn't required for many hard money lenders, which creates fraud risk, and state-level oversight is only slowly tightening as of 2026.

That means borrowers need to do their own screening. I'd start here:

- Ask for a term sheet early: Don't spend days in conversation only to discover the pricing or structure later.

- Review points, maturity, and extension terms carefully: A reasonable headline rate can hide pain in the back half of the deal.

- Check for prepayment friction and default triggers: You want to know what happens if you repay early or hit a delay.

- Confirm closing process and third parties: Ask who handles title, legal docs, and disbursement.

- Pressure-test responsiveness: If a lender is vague before commitment, they usually won't become clearer after closing.

One practical habit helps a lot. Have counsel or an experienced advisor review the documents before you sign. In hard money, details that look minor in a rush can become expensive later. Extension rights, collateral language, fees on default, and cure periods all matter when a project slips.

Let Business Loan Warrior Be Your Guide

Hard money is one of the most useful financing tools in the market when it matches the deal. It's also one of the easiest to misuse. The difference usually comes down to structure, lender quality, and whether the borrower is honest about the exit.

That's why most owners benefit from looking at hard money as one option inside a broader funding strategy, not as the automatic answer. A fast acquisition might justify it. A bridge into cheaper long-term debt might justify it. A thin-margin deal with no backup plan usually won't.

Business Loan Warrior helps simplify that decision. Instead of forcing owners to hunt across scattered lenders and compare opaque offers one by one, the platform brings technology and human guidance together in one process. Borrowers can check options through a single application, review pre-approval paths, and evaluate whether hard money, SBA financing, equipment funding, a line of credit, or another structure fits the situation better.

That matters because the best financing outcome isn't just getting approved. It's getting approved for the right product, with a lender you'd trust to close on time and communicate clearly.

If you need capital fast and want to compare hard money against other real funding options without wasting weeks, start with Business Loan Warrior. You can check pre-approval through a single no-fee application, review offers in one place, and move toward a structure that fits the opportunity instead of forcing the opportunity to fit the loan.