You're probably in a familiar spot. Revenue looks solid. The sales team is doing its job. Your backlog is healthy. Then one major customer pays late, inventory lands before receivables clear, or payroll and vendor terms collide in the same week, and suddenly a profitable company is tight on cash.

That's the difference between profit and liquidity. On paper, your business is fine. In your bank account, it isn't.

For established companies in the $20M to $50M revenue range, this problem is even more frustrating. You're past the stage of chasing tiny working capital fixes, but you're still too operationally complex for many banks to move quickly. You need capital that matches the way your business runs. Fast, flexible, and based on cash generation, not just hard collateral.

Table of Contents

- Why Even Profitable Businesses Run Out of Cash

- Decoding Cash Flow Loans and How They Work

- Comparing the Four Main Types of Cash Flow Loans

- How Lenders Analyze Your Business for Approval

- Beyond Survival Using Cash Flow Loans for Growth

- Your Pre-Approval and Cash Management Checklist

- Frequently Asked Questions About Cash Flow Loans

Why Even Profitable Businesses Run Out of Cash

A business can book a strong quarter and still get squeezed hard.

Take a company that ships on net terms to large customers. It buys materials now, staffs production now, pays freight now, then waits to collect. If one customer stretches payment or a big order lands at the wrong moment, cash gets trapped in the gap between delivery and collection. Nothing is broken. Timing is.

That's where owners get blindsided. They think the issue is margin when the primary issue is velocity. Cash has to move through the business fast enough to support payroll, inventory, rent, debt payments, and growth at the same time.

The risk isn't theoretical. Cash flow problems are the primary cause cited by 60% of small businesses that fail, which is why reliable access to funding matters so much to long-term survival, according to cash flow failure statistics compiled here.

Profit doesn't pay bills on schedule

Your income statement can tell you the business is healthy. Your bank balance tells you whether you can operate this week.

That gap gets wider when you're scaling. Mid-market companies usually face bigger swings because the numbers are larger and the commitments are heavier:

- Larger payroll runs: A growing team raises the cost of every delayed receivable.

- Bigger inventory buys: Expansion often means ordering ahead of demand.

- More complex customer terms: Larger accounts often negotiate slower payment cycles.

- Project-based cash strain: Construction, distribution, manufacturing, and services all front-load expense before cash comes back in.

Cash pressure usually shows up before distress. Smart operators treat it as a financing problem to solve early, not a crisis to explain later.

The real job of a cash flow loan

A cash flow loan isn't a rescue tool for failing businesses. Used properly, it's a timing tool.

It helps you bridge the mismatch between when cash leaves and when cash arrives. That matters if you want to keep control, avoid slashing growth plans, and stop using retained earnings to patch every temporary hole.

Busy owners often wait too long because they assume borrowing means weakness. I think that's backwards. If your business has predictable inflows but awkward timing, using the right debt product is disciplined financial management.

Decoding Cash Flow Loans and How They Work

Cash flow loans are exactly what they sound like. The lender underwrites your ability to generate future cash, not just the resale value of your assets.

This financing model involves borrowing against confirmed future paychecks instead of borrowing against your building. The lender wants evidence that money reliably comes into the business and that enough of it remains after expenses to support repayment.

What a cash flow loan really is

Traditional asset-based lending leans heavily on collateral such as equipment, inventory, or receivables. Cash flow lending starts from a different question: does this business consistently produce enough operating cash to carry debt?

That makes cash flow loans a strong fit for companies that are operationally healthy but not asset-heavy. Service firms, distributors, multi-location operators, e-commerce brands, restaurants, and project-driven businesses often fall into this category. They may have solid revenue and recurring demand without a big pile of hard collateral sitting on the balance sheet.

Lenders usually evaluate bank activity, accounting data, payment processor history, and recent financial performance. They're trying to see the rhythm of the business. Are deposits steady? Are margins stable enough? Do obligations stack up in a manageable way? Can the company handle a rough month without immediately tripping into a crunch?

Why mid-market companies use them

Most online guidance falls short. It's built for startups chasing their first loan or for enterprise borrowers running institutional processes. That leaves a major gap for established firms. There's a significant financing gap for mid-market companies in the $20M to $50M revenue range that need fast, asset-light capital without equity dilution, as noted in this mid-market financing gap discussion from IDB Invest.

That gap is real. Businesses at this size usually want to:

- fund working capital without pledging every asset,

- move faster than a conventional bank can move,

- preserve ownership instead of raising equity,

- match financing to operational cash generation.

Practical rule: If your business can repay from operations but a bank is stuck on collateral, structure, or timeline, cash flow lending is worth a serious look.

Cash flow loans are not one single product. They're a category of products built around future revenue and operating performance. The right version depends on what problem you're solving, how quickly cash comes in, and how predictable your collections are.

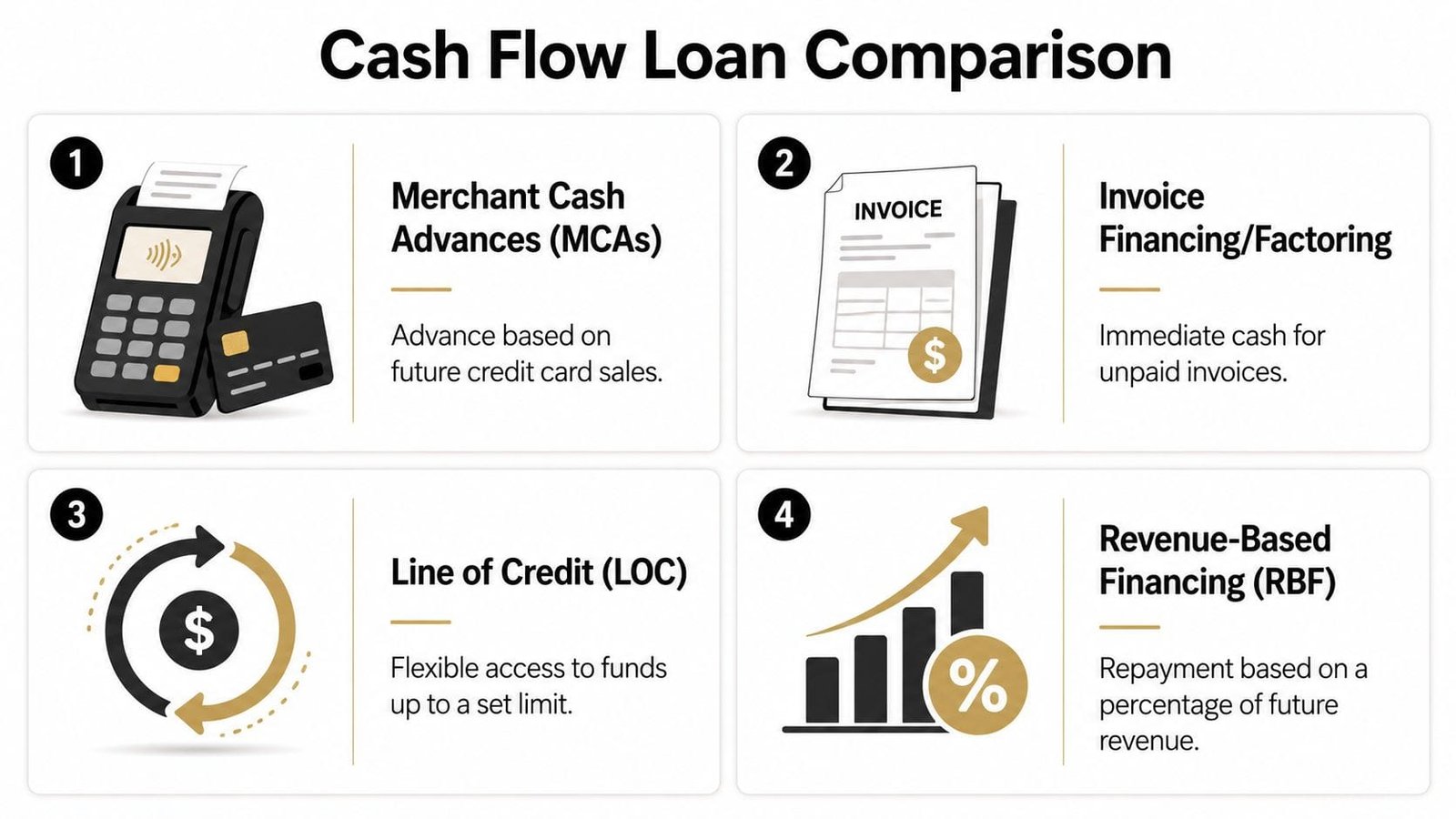

Comparing the Four Main Types of Cash Flow Loans

Not all cash flow loans behave the same way. Some are useful. Some are expensive but appropriate in the right scenario. Some are dangerous when owners use them to cover structural problems instead of short-term timing gaps.

A quick comparison

| Loan type | How it works | Repayment style | Best use case | Main caution |

|---|---|---|---|---|

| Merchant cash advance | You receive an advance tied to future card or sales volume | Frequent remittances tied to sales or fixed withdrawals | Businesses with strong card volume that need speed | Can get expensive fast if used repeatedly |

| Invoice financing or factoring | You unlock cash tied up in unpaid invoices | Repaid when invoices pay, or the factor collects directly depending on structure | B2B firms with reliable customers on long terms | Customer concentration and slow-paying accounts can create friction |

| Business line of credit | You draw funds up to a limit and repay as needed | Revolving, flexible repayment | Ongoing working capital swings, seasonal needs, vendor timing | Easy to overuse if you don't tie draws to a clear purpose |

| Short-term term loan | You receive a lump sum upfront | Fixed scheduled payments | One-time need such as inventory, equipment gap, expansion step, or project mobilization | Less flexible than a line once funds are used |

If you want a more product-by-product breakdown, this comparison of short-term loans, MCAs, and invoice factoring is worth reviewing alongside your cash cycle.

Which option fits which situation

Merchant cash advances work best when speed matters more than elegance. If you run a restaurant group, retail operation, or high-volume card business and need capital immediately for a short-duration opportunity, an MCA can be useful. I would not use one to paper over chronic margin issues. That's how owners get trapped.

Invoice financing or factoring is often the cleanest answer for B2B companies that sell to solid customers but get paid slowly. If your receivables are good and the problem is waiting, this product aligns financing with the asset causing the bottleneck. Construction, staffing, logistics, wholesale, and specialty manufacturing often fit well here.

If your biggest asset is your accounts receivable, finance the receivable. Don't force a general-purpose loan to solve a specific collections delay.

Business lines of credit are the most versatile option for established companies with recurring working capital swings. They're especially useful when the need is intermittent. Draw for inventory, payroll bridge, or marketing push. Repay when receivables land. Draw again when timing tightens. This is usually the best tool when the cash gap repeats but doesn't justify a new full underwriting process each time.

Short-term term loans make sense when the use of funds is clear and finite. A large inventory buy before a seasonal rush. Mobilization for a new contract. A temporary expansion cost that should produce near-term revenue. The discipline here is simple. Borrow for a defined purpose with a defined payoff path.

My blunt recommendation

Use the product that matches the source of repayment.

- If repayment depends on future card sales, consider an MCA carefully.

- If repayment depends on specific invoices, use invoice financing.

- If repayment depends on general operating flexibility, use a line of credit.

- If repayment depends on a one-time initiative, use a short-term term loan.

Owners get into trouble when they choose based on speed alone. Speed matters. Fit matters more.

How Lenders Analyze Your Business for Approval

Underwriting for cash flow loans is less mysterious than most owners think. Lenders are trying to answer one basic question: can this business repay from normal operations without straining itself every month?

They care about your story, but they trust your data more. Bank statements, accounting feeds, receivables, debt obligations, and cash balances tell them how the business behaves.

The numbers that matter most

One of the most important metrics is the operating cash flow ratio. It shows whether daily operations generate enough cash to cover current liabilities. A ratio above 1.0 is considered adequate, while 1.5 to 2.0 signals strong liquidity, according to this guide to cash flow metrics.

That matters because lenders aren't just checking whether revenue exists. They're checking whether operating cash turns into repayment capacity.

Here's what they typically focus on:

- Operating cash flow quality: They want to see cash coming from operations, not one-off balance sheet moves.

- Deposit consistency: Steady inflows matter more than one big month.

- Average balances: Thin balances suggest the business runs with no margin for error.

- Debt load: Existing payments have to leave room for the new one.

- Receivables behavior: If customers pay unpredictably, lenders price for that risk.

- Working capital discipline: Strong collections and payable management help approval.

If you want to understand one related metric that often influences the lender's view of your overall profile, this working capital ratio explanation adds useful context.

A lender doesn't expect a perfect business. They expect a business that produces cash predictably enough to survive an imperfect month.

Why private lenders can often do more than banks

For established companies, capital structure matters as much as approval odds.

Banks often cap borrowing capacity for smaller firms at 3.5 to 4.0x EBITDA, while private credit providers can extend 5.0 to 5.5x EBITDA or more, which can provide materially more growth capital for established businesses, according to this analysis of down-market direct lending.

That difference matters if you're funding expansion, acquisitions, equipment, or a major working capital step-up. It also explains why many mid-market businesses move outside traditional bank channels. Banks tend to prefer standardized deals. Cash flow lenders are often more willing to underwrite the actual operating model.

Here's the practical takeaway:

| What lenders like | What lenders dislike |

|---|---|

| Recurring or repeatable revenue | Sharp, unexplained revenue swings |

| Clean bank statement trends | Frequent overdraft pressure |

| Clear use of funds | Borrowing with no defined purpose |

| Reasonable debt burden | Stacked obligations with no cushion |

| Timely internal reporting | Financials that are late or inconsistent |

If you want better loan options, start acting like your lender is already inside the business. Clean books. Current reporting. Stable deposit activity. Clear explanations for anomalies. That's how you improve approval quality, not just approval odds.

Beyond Survival Using Cash Flow Loans for Growth

The best use of cash flow loans isn't plugging holes. It's financing moves that produce more cash than the debt consumes.

A lender will care about your operating strength either way. The operating cash flow ratio is a key signal, with anything above 1.0 seen as adequate and 1.5 to 2.0 viewed as strong, as noted earlier from the cited cash flow metrics source. You should care for the same reason. If a growth move weakens repayment capacity too much, it's not smart expansion. It's debt dressed up as ambition.

Three smart uses of fast capital

A consumer brand lands a surprise purchase order from a major retailer. Great news, except the retailer won't pay quickly and the brand needs packaging, production, and freight now. A short-term cash flow loan can bridge that gap. The loan lets the company fulfill the order instead of declining it or giving away margin by scrambling for emergency vendor terms.

A construction firm wins a larger project than usual. Labor has to be mobilized. Materials need to be secured. The receivable won't clear for a while. Invoice financing is often the clean play here because it aligns funding with billed work instead of forcing the company to absorb the entire timing mismatch internally.

A multi-location hospitality or retail operator wants to renovate during a slower period and launch a marketing push before demand returns. A line of credit is usually better than a lump-sum loan because the owner can draw in phases, keep interest tied to actual use, and preserve flexibility if project timing shifts.

Good debt helps you act before cash arrives. Bad debt covers decisions that should have been fixed in operations.

The common thread is simple. Each of these businesses uses financing to support a revenue-producing action with a visible repayment path. That's the discipline.

What not to finance

I tell owners to avoid using cash flow loans for problems that are operational, not temporary:

- Chronic margin compression: Fix pricing, purchasing, or labor mix first.

- Permanent overhead bloat: Debt won't solve a cost structure problem.

- Customer concentration risk: One large payer can create dangerous dependency.

- Unclear expansion bets: If the return logic is fuzzy, don't finance it.

Cash flow loans work best when the business already knows how to make money and just needs capital timed correctly.

Your Pre-Approval and Cash Management Checklist

A good application starts before you talk to a lender. A good outcome depends on what you do after funding.

What to prepare before you apply

Get your information clean and current. Speed in underwriting usually comes from organization, not luck.

- Recent bank statements: Lenders want to see deposit patterns, average balances, and outflow pressure.

- Current profit and loss statement: Make sure it matches how the business performed, not how you hope it performed.

- Balance sheet: This shows debt levels, liquidity, and whether working capital is healthy.

- Accounts receivable aging: Critical if collections timing is part of the story.

- Accounts payable snapshot: This helps explain cash demands and vendor pressure.

- Existing debt schedule: Be ready to show what's already being paid and when.

- Clear use of funds: Expansion, payroll bridge, inventory buy, project mobilization, acquisition support. Be specific.

Owners lose time when they submit partial data and then try to explain the rest by email. Don't do that. If the business is strong, make it easy to see.

What to manage after funding

Funding isn't the finish line. It's the moment discipline starts to matter more.

The best move you can make is building a 13-week rolling cash flow forecast. That approach can reduce the cash conversion cycle by 15 to 25 days, which frees up cash and makes debt service easier, according to this 13-week cash flow forecasting guide.

If you need a practical framework, this cash flow forecast guide for loan strategy is a useful starting point.

Operator move: Review cash weekly, not when the controller says there's a problem.

Use this post-funding checklist:

Track inflows by week

Don't rely on monthly hindsight. Weekly visibility catches timing problems early.Separate essential draws from optional spending

If you use a line of credit, tie every draw to a purpose that either protects operations or generates revenue.Watch receivables aggressively

Slow collections can gradually turn a manageable facility into a permanent crutch.Map repayments to real cash events

Match your expected paydown to invoice collections, seasonal demand, or project milestones.Keep reporting current

Clean books improve renewal options and negotiating power later.

A cash flow loan should make your business more flexible, not more fragile. If your forecasting improves after funding, future capital gets easier and cheaper to manage.

Frequently Asked Questions About Cash Flow Loans

Do cash flow loans affect personal credit

Sometimes. Many lenders require a personal guarantee, especially for closely held businesses. That doesn't always mean a hard pull at the pre-approval stage, but it can mean personal liability if the business defaults. Read the guarantee language carefully. Owners often focus on speed and miss the recourse terms.

Are cash flow loans more expensive than traditional loans

Often, yes. But that's not the right first question.

The better question is whether the financing creates more value than it costs. If a line of credit helps you take on a profitable opportunity, smooth a known timing gap, or avoid equity dilution, higher cost can still be rational. If you're borrowing just to survive the same recurring problem every month, the product is probably being misused.

Also, don't compare unlike things. A factor rate product, a revolving line of credit, and a conventional term loan don't behave the same way. Ask for the full repayment structure, timing of payments, fees, and total expected payback before signing anything.

Can you qualify with weak credit

Yes, sometimes, because cash flow lenders care heavily about business revenue and bank activity. Weak credit doesn't automatically kill the deal if the company generates dependable cash and the use of funds makes sense.

But weak credit usually narrows your options and can lead to stricter terms. The strongest move is to present a clean file: current financials, stable deposits, a clear explanation for any past issues, and a defined repayment path. Lenders can work with imperfection. They hate uncertainty.

If you're an established business in the mid-market range, don't think about cash flow loans as emergency money. Think of them as strategic capital. Used well, they protect ownership, support growth, and keep timing problems from turning into expensive distractions.

If your business needs fast, flexible capital without wasting weeks on the wrong lenders, Business Loan Warrior is worth a look. You can check options through a single no-fee application, review pre-approval without affecting credit, and explore funding built for working capital, equipment, expansion, invoices, and short-term liquidity needs.