You're staring at the same problem most retail owners hit right before a busy stretch. A vendor wants payment now. Your shelves need fresh inventory. Payroll doesn't pause. Rent is due whether sales spike next week or not. The opportunity is obvious. The cash timing isn't.

That's why business loans for retailers matter so much. This isn't about borrowing for the sake of borrowing. It's about using the right capital at the right moment so you can buy inventory before demand hits, smooth out uneven cash flow, upgrade the store, or open the next location without choking the current one.

A lot of owners assume they need a huge loan to make financing worth pursuing. They usually don't. In 2024, 37% of U.S. employer small businesses applied for financing, and half of applicants sought $100,000 or less, according to small business lending trends reported by Credit Suite. That tells you something important. Most businesses aren't chasing oversized debt. They're trying to solve practical operating problems.

Table of Contents

- The Retailer's Dilemma Funding Growth vs Managing Cash Flow

- Matching the Loan to Your Retail Need

- Are You Ready What Lenders Want to See

- Your Application Checklist From Preparation to Submission

- Deep Dive SBA Loans vs Fintech Lenders

- Real-World Retail Scenarios and Repayment Examples

- Funding Your Future A Strategic Growth Lever

The Retailer's Dilemma Funding Growth vs Managing Cash Flow

A retailer I'd describe as typical had a strong holiday forecast, a supplier ready to lock in favorable pricing, and customers already asking about incoming products. On paper, the business was healthy. In real life, cash was trapped between current expenses and future sales.

That's the retail funding trap. Growth usually demands cash before revenue lands. You pay for inventory, labor, fixtures, packaging, marketing, and freight first. Customers pay later. If you guess wrong, debt becomes pressure. If you wait too long, you miss margin and lose sales.

The problem is common, not a sign that your business is broken. Retail owners regularly need modest, targeted capital to bridge timing gaps and stock for demand. The smart move isn't “borrow as much as possible.” The smart move is borrowing only for a specific job, with a repayment structure that fits how your store generates cash.

Practical rule: If you can't explain exactly what the funds will do in one sentence, you're not ready to borrow yet.

That sentence should sound like this: buy seasonal inventory, remodel a higher-converting front end, replace failing equipment, cover a short-term dip, or refinance expensive short-term debt into something saner.

Retail lenders also care about whether you understand your own cycle. If your biggest swings come from holiday traffic, back-to-school demand, tourism, or vendor ordering windows, your financing strategy has to track those rhythms. If you haven't built that view yet, start with a cash flow forecast that supports your loan strategy.

Borrowing can absolutely help a retail business grow. Bad borrowing can just as easily trap a good store in weekly repayment stress. The difference comes down to fit.

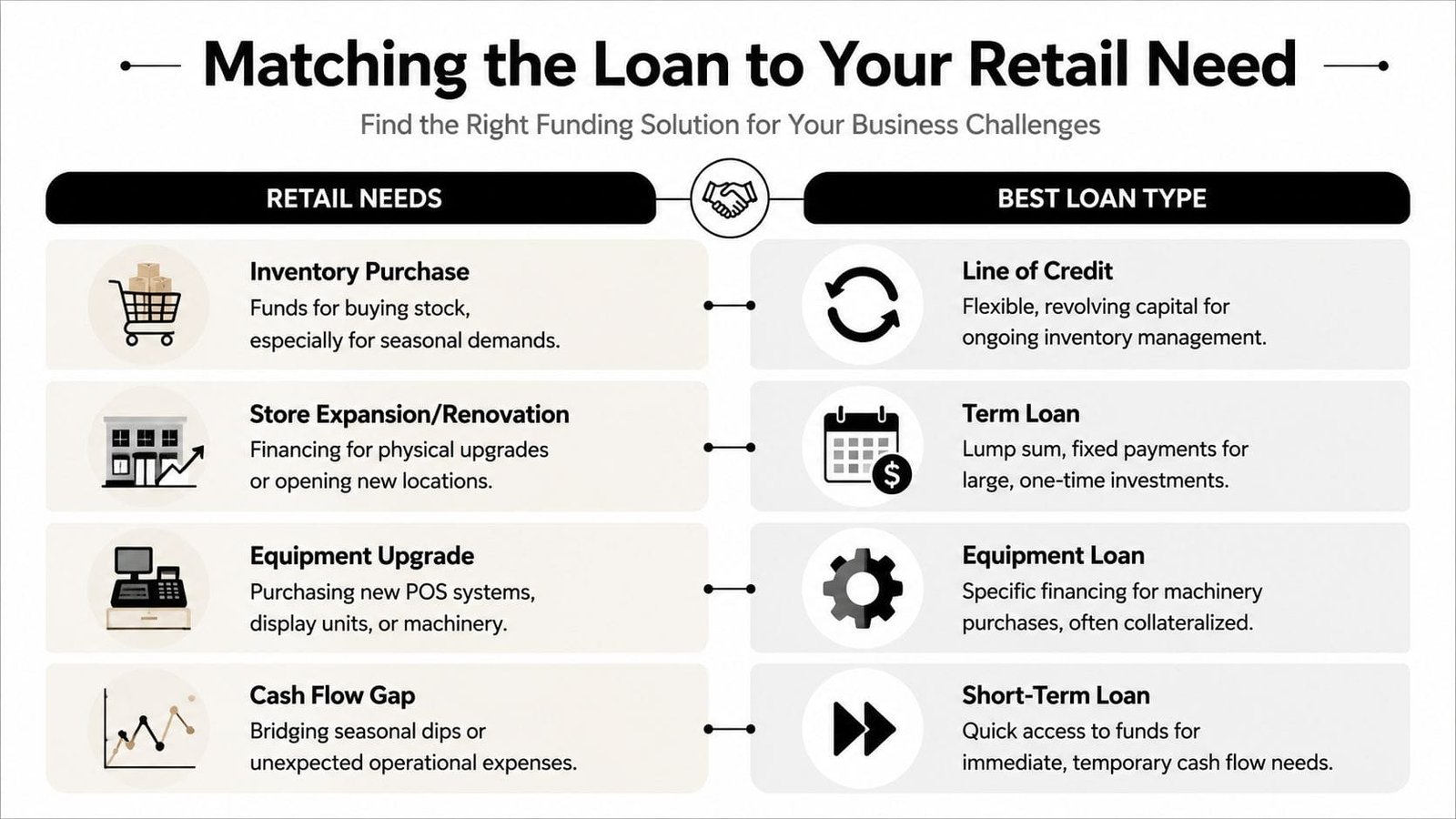

Matching the Loan to Your Retail Need

Most articles on business loans for retailers make this harder than it needs to be. They list products. They define terms. They leave you to sort it out. That's backward.

Start with the problem. Then match the financing.

Use case first, loan type second

If your issue is inventory, a line of credit or inventory financing usually makes more sense than a long-term lump-sum loan. Inventory is a moving target. You buy, sell, reorder, and adjust. A revolving facility matches that better than fixed debt.

That matters because many retailers struggle to finance inventory through traditional channels. Inventory is often treated as a softer asset, while fintech inventory financing has grown as a practical option for retailers expanding SKUs without giving up equity, according to Founderpath's overview of CPG and inventory funding.

If your issue is store expansion, renovation, or a major one-time investment, use a term loan. You get a lump sum, fixed payments, and a defined payoff path. That's cleaner for build-outs, leasehold improvements, and opening another location.

If you need equipment, choose equipment financing when available. Keep the debt tied to the asset. Don't burn a flexible line of credit on a long-lived purchase like refrigeration, shelving systems, displays, or a POS rollout.

If the actual problem is a temporary cash flow gap, a short-term loan or line of credit can work. The difference is simple. A short-term loan gives you a chunk of money now and a fixed repayment schedule. A line of credit gives you reusable access, which is better if your need repeats.

The best retail loan isn't the one with the biggest approval. It's the one that fits the timing of the problem.

Retail Business Loans At-a-Glance

| Loan Type | Best For | Typical Amount | Repayment Structure |

|---|---|---|---|

| Line of credit | Reordering inventory, bridging uneven cash flow, covering payroll during slower stretches | Varies by lender and business profile | Revolving. You draw what you need and repay based on usage |

| Term loan | Expansion, renovations, opening a new location, large marketing or operational investments | Varies by lender and business profile | Fixed installment payments over a set term |

| Equipment loan | POS systems, refrigeration, display units, packaging machinery, store fixtures | Varies by equipment value and lender | Fixed payments, often tied to the financed asset |

| Short-term loan | Immediate working capital needs with a clear payoff plan | Varies by lender and business profile | Frequent fixed payments over a shorter period |

| Inventory financing | Large purchase orders, SKU expansion, stocking ahead of demand | Varies by inventory strategy and lender | Structured around inventory purchases and business cash flow |

| Merchant or performance-based advance | Fast working capital based on sales or processing activity | Offer size varies by platform and sales history | Repayment often tied to sales activity or preset remittances |

Here's how I'd rank the options in plain English:

- For recurring inventory buys: Use a line of credit first. Use inventory financing when your product margins and turnover support it.

- For a remodel or expansion: Use a term loan. Don't fund a multi-year project with short-term money.

- For equipment: Match the financing to the equipment.

- For urgent cash needs: Use short-term money only if you know exactly how it gets paid back.

- For processor-based fast funding: It can be useful, but convenience usually costs more.

What retailers often get wrong

Retail owners commonly make three mistakes.

- They finance long-term assets with short-term debt. That creates unnecessary payment pressure.

- They borrow without a use-of-funds plan. Lenders notice. More critical is the fact that your business feels it later.

- They choose speed over structure when speed isn't necessary. Fast money has a place. It shouldn't be your default.

If you're choosing among business loans for retailers, think in terms of asset life and sales timing. Short-lived need, short money. Long-lived investment, long money. Flexible need, flexible credit.

Are You Ready What Lenders Want to See

Lenders don't care how excited you are about your next season. They care whether your business can absorb debt and still operate cleanly.

Capacity beats optimism

The first thing a lender wants to see is capacity. That means cash flow. Can the business make the payment without starving inventory, payroll, rent, and taxes?

Some lenders use formal debt service coverage tests. You don't need the jargon to understand the point. They're asking whether your operating cash flow comfortably covers the new debt payment. If repayment only works when everything goes perfectly, you're not ready.

The next issue is credit quality. That includes business credit, often personal credit for owner-backed deals, and your payment behavior. Clean trends matter more than heroic explanations. A late-payment pattern tells a lender you react to pressure instead of planning for it.

Then there's time in business and revenue consistency. A retailer with clear reporting, stable deposits, and understandable seasonal swings is easier to underwrite than a retailer with messy books and unexplained volatility. Seasonality isn't a problem by itself. Unclear seasonality is.

Don't try to hide the slow months. Label them, explain them, and show how the strong months carry the year.

Retail-specific weak spots to fix

Retail businesses have a few predictable underwriting pain points.

- Inventory-heavy balance sheets: Some lenders discount inventory because resale values can be uncertain.

- Thin cash reserves: Common in retail, but still a red flag.

- Merchant processing dependence: Convenient for underwriting, but it can expose volatility if sales are concentrated.

- Owner commingling: If you mix personal and business spending, expect friction.

You can improve your file before a lender ever reviews it.

- Clean up your financial statements. Your profit and loss, balance sheet, and cash flow records should match your tax returns and bank activity.

- Separate business and personal activity. If you still pay business expenses from personal accounts, stop.

- Show margin discipline. If you've dropped weak SKUs, tightened buying, or improved sell-through, put that in writing.

- Prepare a short seasonality note. Explain your buying cycle, peak months, and how you manage slower periods.

What strong borrowers usually show

A lender gets comfortable when your file answers basic questions without drama.

- Where does the money go

- How does the loan create or protect cash flow

- What supports repayment if sales soften

- What does management track each week

If you can answer those in plain English, you're ahead of many applicants. If you can't, the issue isn't the lender. It's preparation.

Your Application Checklist From Preparation to Submission

The businesses that get funded efficiently usually don't have perfect numbers. They have organized numbers.

Build the file before you apply

Treat your application like a buyer presentation. You're not dumping documents into a portal. You're making it easy for an underwriter to say yes.

Gather these first:

- Profit and loss statements: Show sales trends, margin behavior, and expense control.

- Balance sheets: Lenders use these to understand liquidity, debt load, and inventory position.

- Business tax returns: They validate what your internal reporting says.

- Business bank statements: They reveal actual deposit flow and spending behavior.

- Entity documents: Formation records, licenses, leases, and ownership information help lenders verify the business.

- Debt schedule: List current loans, balances, and payment obligations.

- Use-of-funds summary: Keep it short and concrete.

A sharp executive summary helps. One page is enough. Say who you are, what you sell, where you sell, what capital you need, what it will be used for, and why repayment makes sense. If your business has multiple locations or channels, include that structure clearly.

Underwriter shortcut: Make your application package easy to skim. Label files clearly, use consistent dates, and keep your explanation tighter than you think it needs to be.

How to submit like a serious operator

Before you hit submit, check the package for gaps. Missing pages, blurred scans, mismatched totals, and unsigned forms slow deals down. They also make lenders wonder what else is sloppy.

One thing worth watching is your story around cash flow. If a lender sees a temporary dip in margin, a large one-time inventory purchase, or unusual payroll timing, explain it up front. Silence invites suspicion.

This walkthrough can help you think through the process before you apply:

A few final submission rules matter more than owners realize:

- Answer quickly: If underwriting asks for clarification, respond fast and directly.

- Don't change the ask midstream: Shifting amount or use-of-funds late can reset the review.

- Be honest about pressure points: Existing debt, seasonality, and supplier issues are manageable. Surprises aren't.

- Keep one version of the truth: Your application, bank data, and financial statements should tell the same story.

A lender can work with imperfect facts. They won't work comfortably with inconsistent ones.

Deep Dive SBA Loans vs Fintech Lenders

You need to solve the right problem first.

If your store is planning a second location, buying expensive equipment, or refinancing costly debt into a longer repayment term, SBA financing is usually the better answer. If you need to place a large inventory order this week, cover a short cash gap, or act on a narrow buying opportunity, fintech lenders often make more sense. Retail owners get in trouble when they pick based on speed alone or rate alone instead of matching the product to the job.

When SBA is the right answer

SBA loans are the better fit for retail projects that should be paid back over time. Store buildouts, location expansion, major equipment purchases, and working capital that supports steady growth belong here. The benefit is structure. You typically get lower rates than short-term online products and repayment terms that put less strain on monthly cash flow.

That matters in retail because growth rarely pays you back overnight. A remodel may lift traffic over months. A new location may take time to stabilize. Spreading repayment over a longer period gives the project room to work.

SBA lending has also remained active for smaller borrowing needs, not just big expansion deals. Canopy Servicing's small business lending statistics note strong SBA 7(a) activity and meaningful volume in loans under $150,000. That fits retail well. Many owners need a practical amount for inventory support, a refresh, or a targeted growth push, not a massive capital injection.

If you need help sorting the SBA options, read this guide on comparing SBA 7(a), 504, and microloans. The right SBA product depends on what you are funding.

When fintech is the better move

Fintech lenders win on speed and simpler underwriting. They often pull from bank activity, card sales, accounting data, and recent revenue trends instead of requiring the full bank-style package and a longer review cycle.

That speed solves real retail problems. A vendor offers a discount for immediate purchase. A freezer dies in your specialty food shop. A cash gap opens because payroll and rent hit before receivables clear. In those cases, the best long-term structure matters less than getting usable capital fast enough to protect revenue.

The trade-off is straightforward. Fintech money usually costs more. Terms are often shorter. Payments may be weekly or even daily, which can squeeze a store with uneven sales.

That payment structure is the part many owners underestimate.

A fast approval is helpful. A repayment schedule that drains your register during a slow stretch is not.

How to choose without overcomplicating it

Use SBA financing for longer-lived investments. Use fintech funding for short-term needs where speed matters and the return is close at hand. Do not fund a five-year expansion plan with a product that wants repayment on a compressed timeline. Do not spend six weeks chasing an SBA approval for an inventory opportunity that disappears in three days.

Here is the practical comparison:

| Retail need | SBA loan | Fintech lender |

|---|---|---|

| Opening or expanding a location | Strong fit | Usually too expensive for the job |

| Equipment with a long useful life | Strong fit | Can work, often a weaker structure |

| Refinancing expensive debt | Strong fit | Usually not the first choice |

| Fast inventory purchase | Often too slow | Strong fit |

| Emergency cash flow gap | Possible if timing allows | Often the better choice |

| Underwriting based heavily on live sales data | Less common | Common |

My recommendation is simple. Choose SBA when the project needs time to produce returns. Choose fintech when delay would cost you sales, margin, or operating stability. Retail lending works best when the repayment term matches the business problem.

Real-World Retail Scenarios and Repayment Examples

The best way to judge business loans for retailers is to map them to actual operating problems.

Scenario one seasonal inventory for a boutique

A boutique apparel retailer gets strong holiday traffic every year. The owner needs capital before sales arrive because top vendors require early commitments.

The wrong move is a large long-term loan for a short inventory cycle. The better fit is a line of credit or a processor-based working capital offer if speed matters and the repayment structure matches expected sales flow.

For merchants already operating inside Square, this type of funding can be especially practical. Square Loans offers performance-based funding from $100 to $350K, and qualified users can see approval rates of 80% to 90%, based on processing history rather than a traditional credit-first approach, according to Square's business financing information.

Repayment example, in plain terms: the owner draws funds to buy seasonal inventory, sells through during the peak window, then pays down the balance as receipts come in. The key is simple. Short inventory cycle, short flexible capital.

Scenario two store remodel for a multi-location retailer

A growing home goods retailer wants to renovate an existing location and open a second one in a nearby trade area. That project has a long payoff horizon. It's supposed to increase sales over time, not in a few weeks.

This is term-loan territory. Potentially SBA territory, if the borrower profile and timeline fit. The owner wants predictable payments and enough runway for the upgraded stores to produce returns before debt pressure gets tight.

A short-term product would be dangerous here. Weekly or frequent payments can strain the original store before the expansion fully contributes. Long project, long money. That's the rule.

Use debt that matures on the same general timeline as the value it creates.

Scenario three equipment replacement for a specialty food shop

A specialty food retailer loses a refrigeration unit and needs a replacement fast. The equipment directly supports revenue. Waiting isn't realistic.

Equipment financing is the most logical fit if available. It keeps the financing attached to the asset and preserves working capital for inventory and payroll. If timing is urgent and equipment financing is delayed, a short-term bridge can make sense, but only if the owner has a clear plan to refinance or rapidly pay it down.

The repayment lesson across all three stories is the same. Don't focus only on approval. Focus on whether the payment schedule matches the way the money will come back into the business.

Funding Your Future A Strategic Growth Lever

It's October. Your shelves need holiday inventory now, your cash is tied up in payroll and rent, and a lender is offering fast money with payments that start almost immediately. This is the moment that separates smart retail borrowing from expensive panic.

Financing should solve a specific retail problem. Stock up before peak season. Spread out the cost of a remodel. Cover a short cash flow gap without choking the business next month. If the loan does not match the job, it creates a second problem right after it solves the first.

The best rule is simple. Match the repayment schedule to the way the investment pays you back. Use a line of credit for uneven working capital needs. Use a term loan or SBA structure for expansion, buildout, or equipment that should produce value over years, not weeks. Use fast funding only when speed protects revenue and you already know how you will absorb the higher cost.

That discipline matters more than rate shopping alone.

Retail owners get into trouble when they borrow long for short needs, or short for long projects. A seasonal inventory buy can justify flexible capital that gets paid down after sales come in. A second location usually needs longer runway and predictable monthly payments. A promo campaign needs funding that protects margin, not debt that eats it. If you are planning a sales push, read this guide on using financing strategically for retail promotions that actually grow revenue before you borrow.

Good funding gives you room to execute. Bad funding turns a healthy store into a store that is always catching up.

If you want help sorting through your options, Business Loan Warrior can help you check no-fee pre-approval, compare funding paths, and find a loan structure that fits your retail business instead of forcing your business to fit the loan.