You're ready to act. Inventory is moving, a vendor is offering better pricing if you buy now, or a machine has to be replaced before it slows down production. Then the financing question hits: what will lenders see when they check your credit, and will shopping for a loan make things worse?

That concern is justified. Credit can decide which lenders will take your application seriously, how much documentation they ask for, and whether your rate is workable or expensive enough to strain cash flow. A weak approach to loan shopping can create another problem. Too many hard inquiries in a short window can make an already borderline file harder to place.

The safer move is to approach financing the way lenders do. Check where your business and personal credit stand before you apply, narrow the products that fit your profile, and use pre-approval tools when available so you can compare options without adding unnecessary hits to your credit file.

Borrowers who handle this well usually save more than points on a rate. They avoid wasted applications, protect their score while they shop, and get to a lender that fits the deal the first time.

Table of Contents

- Your Business Loan Credit Score Explained

- Business Credit vs Personal Credit for Loans

- What Credit Score Do You Need for a Business Loan

- How Lenders Evaluate Your Credit Profile

- How to Check and Improve Your Business Credit Score

- Shop for Loans Safely with Pre-Approval Insights

- Frequently Asked Questions About Business Loan Credit

Your Business Loan Credit Score Explained

A common borrower scenario looks like this: the business is healthy enough to use capital well, but the owner doesn't know whether a lender will focus on the company's credit, the owner's FICO, or both. So they wait. They put expansion on hold, delay inventory buys, or cover short-term needs with expensive workarounds.

That delay usually costs more than the credit check itself.

A business loan credit score isn't one universal number that every lender uses the same way. It's a shorthand for how a lender prices risk. Some lenders lean heavily on personal credit. Some focus more on business performance. Some care most about collateral or repayment source. The mistake owners make is assuming the score is a simple pass or fail line.

It's not.

Why this matters before you apply

A lender doesn't just ask, “Is this borrower good?” They ask, “Is this borrower a fit for this product?” That's why a score that won't clear a traditional bank can still work for equipment financing, invoice-based funding, or certain online products.

Practical rule: Don't ask whether your score is “good.” Ask which loan structures your score can realistically support.

The useful way to think about credit

Credit matters because it affects three things at once:

- Approval access: Some products are off-limits below certain ranges.

- Pricing pressure: Weaker credit usually means more expensive financing.

- Shopping strategy: The wrong application sequence can create unnecessary hard inquiries and reduce your options.

If you understand those three levers, the process stops feeling mysterious. You stop applying blindly and start narrowing the field before a lender makes a full decision.

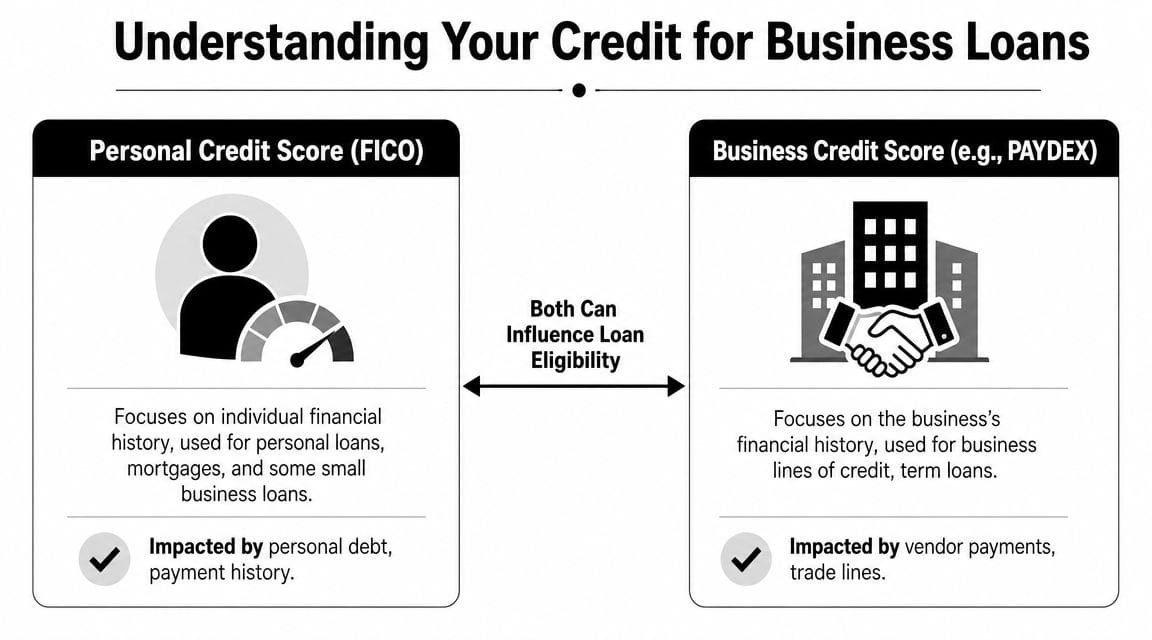

Business Credit vs Personal Credit for Loans

A common mistake happens before the application even starts. An owner sees strong sales, assumes the business will stand on its own, then gets surprised when the lender pulls personal credit and the deal prices worse than expected.

That is how borrowers end up with avoidable hard inquiries.

Business and personal credit are separate files, but lenders often read them together. If you want to shop carefully and protect your options, you need to know which file is likely to drive the decision before you apply.

Two files, two underwriting jobs

Personal credit shows how you handle debt as an individual. Lenders use it to judge repayment habits, current obligations, and whether there are signs of stress such as recent late payments, high revolving utilization, or collections.

Business credit shows how the company pays vendors and creditors in the business name. It can include trade lines, payment history, public records, and other account activity tied to the company.

The practical difference is simple. Personal credit answers, “How has the owner managed obligations?” Business credit answers, “How has the company managed obligations?”

That distinction matters if you are comparing a business loan vs personal loan for funding a company, because the lender is not reviewing the same risk profile in each case.

Why personal credit still matters so much

For many small businesses, especially newer ones, the owner is still part of the credit decision whether the application is filed in the business name or not. A legal entity helps with structure and documentation. It does not automatically remove the owner from underwriting.

In practice, lenders often treat personal credit as an early filter when the business has limited borrowing history, thin trade reporting, or inconsistent financials. That is one reason owners should avoid shotgun applications. If a lender is likely to rely heavily on personal credit, it makes sense to screen for fit first and use pre-approval tools where available before authorizing a hard pull.

Which file carries more weight

It depends on the stage of the business and the loan type.

A newer company with light business credit usually gets judged first on the owner's file. An established company with solid revenue, clean bank statements, time in business, and reporting trade lines has a better chance of shifting the focus toward business performance.

Even then, strong business numbers do not completely cancel out weak personal credit. They may improve the structure of the offer, expand collateral-backed options, or keep a file alive that would otherwise be declined. That is a real advantage, but it is not a free pass.

How to manage both without hurting your chances

Borrowers get better results when they prepare for both files to matter.

- Protect personal credit before shopping: Bring down revolving balances, fix past-due accounts, and avoid unnecessary applications.

- Build business credit on purpose: Open accounts that report, pay vendors on time, and make sure the business profile is properly matched to the legal entity.

- Ask how the lender pulls credit: Some products start with a soft pull or pre-qualification review. Others go straight to a hard inquiry.

- Apply in the right order: Start with lenders and loan types that fit your current profile instead of testing multiple options blindly.

That last point matters more than many owners realize. Good loan shopping is not just about getting approved. It is about preserving credit strength while you compare options.

What Credit Score Do You Need for a Business Loan

This is the question most owners ask first, and it's the right one. You need a realistic range before you choose where to apply. The problem is that most articles flatten everything into one number, when actual lending is product-specific.

A bank term loan, an SBA loan, a line of credit, invoice factoring, and a merchant cash advance don't underwrite risk the same way. They shouldn't.

Typical score ranges by loan type

The table below gives you a practical screening view.

| Loan Type | Typical Score Range | Best For |

|---|---|---|

| SBA 7(a) Standard | 650 to 690 | Established businesses seeking broad-use financing |

| SBA 7(a) Express | Around 600 minimum | Faster SBA-backed working capital needs |

| SBA 504 | 680 minimum | Owner-occupied real estate or major fixed assets |

| SBA Microloan | About 620 | Smaller borrowing needs and newer borrowers |

| Traditional bank loan | Roughly 670 to 700+ | Lower-cost financing for strong borrowers |

| Online or alternative business loan | About 500 to 600 | Borrowers who need access despite weaker credit |

| Business term loan or line of credit | About 600 to 680 | Unsecured or lightly secured working capital |

| Invoice factoring | Around 500+ | Businesses with eligible receivables |

| Merchant cash advance | Around 500+ | Businesses with card sales needing speed |

| Equipment financing | Often viable in the mid-range when the asset supports the deal | Equipment purchases where collateral helps |

According to Crestmont Capital's breakdown of business loan credit score requirements, many SBA lenders look for personal FICO scores around 650 or higher, with cited benchmarks including 650 for SBA 7(a), 680 for SBA 504, and about 620 for Microloans. The same source notes that alternative online lenders may approve borrowers in the 500 to 600 range, usually with higher borrowing costs.

A separate lending overview from SoFi notes that traditional banks commonly require roughly 680+ personal credit, many online or alternative lenders consider borrowers in the 500 to 600 range, SBA-oriented lenders often sit in the 620 to 640 band, and some SBA 7(a) guidance ties to a FICO SBSS minimum of 155.

Why the ranges vary so much

The score requirement follows the lender's downside risk.

Banks usually price for lower risk and tighter standards. They want cleaner credit because they're often offering better pricing and longer-term debt.

Alternative lenders often approve lower scores because they price the risk differently. That can mean shorter terms, more expensive capital, or structures tied more closely to daily or weekly business performance.

NerdWallet's lending guide explains the product logic well: unsecured products like business term loans and lines of credit typically require about a 600 to 680 score, while invoice factoring and merchant cash advances can approve around 500+ because repayment is tied more to receivables or card sales than overall creditworthiness.

The lower the lender's reliance on your overall credit profile, the more flexible score expectations often become.

A practical way to read your own score

If you're 700+, you usually have the widest menu and the best shot at bank-priced or strong SBA options.

If you're in the mid-600s, you may still have workable access to SBA, equipment, term loan, and line-of-credit products, but lender selection matters more.

If you're in the 500s, the question changes. It's less about chasing the cheapest capital and more about finding structures where cash flow, collateral, receivables, or documentation can offset the score.

That's why raw score alone doesn't tell the whole story. It tells you where to start looking.

How Lenders Evaluate Your Credit Profile

A lender doesn't see only a number. They see a pattern. The business loan credit score is the headline, but underwriters still read the details behind it.

That's where good borrowers separate themselves from rushed applicants.

What the score signals

When a lender reviews credit, they're trying to answer a simple question: does this borrower handle obligations predictably? The actual review usually centers on a handful of signals:

- Payment behavior: Late payments tell lenders that repayment discipline may be inconsistent.

- Debt load: High revolving balances can suggest strain, even if the score still looks passable.

- Length of history: A longer file gives lenders more behavior to assess.

- Public derogatories: Bankruptcies, liens, and severe delinquencies change the conversation fast.

- Recent inquiries: Multiple recent applications can make a borrower look like they're scrambling for cash.

None of those items lives in isolation. Underwriters read them together.

What can offset weaker credit

Lower scores don't always end the process. They do force the borrower to present stronger support elsewhere.

When owners ask how to find the right lender for a small business loan, the solution is often about fit between credit weakness and underwriting strength. If unsecured lenders don't like the file, a collateral-backed or cash-flow-based structure may still work.

Here's what lenders commonly use as compensating strength:

- Revenue consistency: Stable deposits suggest the business can support repayment.

- Cash-flow visibility: Clean statements help an underwriter trust the story.

- Time in business: Older businesses usually look less speculative.

- Collateral quality: Equipment, receivables, or other assets can reduce lender risk.

- Documentation discipline: Missing records create doubt. Clear records reduce it.

Why product type changes the review

An unsecured line of credit asks the lender to trust the borrower more broadly, so credit standards tend to be tighter. A receivables-based product asks the lender to trust a more specific repayment source, so the score can matter less.

If the repayment source is easier for the lender to verify and control, the score often matters less than it would on a general-purpose unsecured loan.

Borrowers get in trouble when they apply as if every lender evaluates risk the same way. They don't. The structure determines the scrutiny.

How to Check and Improve Your Business Credit Score

Most owners make this harder than it needs to be. They either avoid checking until they urgently need money, or they chase quick fixes that don't meaningfully change underwriting. A better plan is simple: check both files, clean what you can, and strengthen the parts lenders use.

Start by checking the right reports

For personal credit, review reports from the major consumer bureaus and know the FICO range lenders are likely to see.

For business credit, monitor your files with providers commonly used in business lending, such as Dun & Bradstreet, Experian Business, and Equifax Business. Don't assume your business has a strong profile just because it has revenue. Plenty of firms have good sales and thin credit files.

Check for:

- Reporting errors: Wrong balances, duplicate accounts, or incorrect payment history

- Missing trade data: Vendor relationships that don't appear

- Old issues still lingering: Resolved items that still create friction

- Identity mismatches: Business name, address, and entity inconsistencies

What improves approval odds fastest

If funding may be needed soon, focus on actions that underwriters reward.

- Pay on time, every time: This is the cleanest signal you can send.

- Lower revolving balances: Heavy utilization raises concern even before a lender reviews the full file.

- Separate business activity cleanly: Use business accounts and business credit tools where possible.

- Add reporting trade lines: Vendor accounts only help if they report.

- Review before shopping: Fix errors before any lender sees them.

Some borrowers with weaker personal credit still get approved when the business fundamentals are strong. The Credit People notes that alternative lenders may approve borrowers below traditional thresholds, including a cited example at a 580 personal score, when the borrower can show consistent monthly revenue, a long operating history, and documentation such as bank statements and tax returns.

That's a useful lesson. If your score isn't ideal, don't just try to “improve the score.” Strengthen the full file the lender will review.

Build lender-trusted habits

A lot of business owners need a practical operating checklist more than theory. If you want a structured plan, this guide on the 90-day business credit blueprint lending partners actually trust is a useful next read.

Here's the rhythm that works in practice:

- Pull your personal and business reports.

- Dispute obvious inaccuracies.

- Pay down balances that make the file look stressed.

- Establish or strengthen reporting vendor relationships.

- Gather statements, returns, and entity documents before you apply.

This walkthrough gives a solid visual explanation of what lenders often look for in the file:

What doesn't work

Borrowers waste time when they rely on cosmetic fixes. Opening random accounts with no underwriting purpose, moving balances around without reducing overall strain, or applying repeatedly to see who says yes usually creates a mess.

Clean files win. Complete files win. Desperate application patterns usually don't.

If you need funding soon, the goal isn't perfection. It's presenting a file that makes repayment look believable and manageable.

Shop for Loans Safely with Pre-Approval Insights

This is the part most owners miss. They spend all their time asking what credit score they need and almost none asking how to compare options without damaging that score.

That's backward.

Soft pull versus hard pull

Some lenders and financing platforms use a soft pull during pre-approval. That lets you review possible options without the immediate score impact associated with a hard inquiry. A hard pull usually comes later, when you move forward with a specific application and the lender begins full underwriting.

Crestmont Capital highlights this directly in its bad-credit funding guidance, noting that some lenders and platforms use a soft pull during pre-approval so borrowers can compare options without immediate score damage.

Why this changes the borrowing strategy

If you apply one lender at a time without understanding each lender's process, you can create unnecessary inquiries before you even know whether the product fits. That's avoidable.

The smarter workflow looks like this:

- Start with pre-qualification or pre-approval tools

- Confirm whether the first review is a soft pull

- Compare structure, likely pricing, term length, and documentation needs

- Advance only with the lender that best matches your profile

That sequence protects your credit and your time.

The strategic advantage of pre-approval

Pre-approval tools are useful because they turn loan shopping into screening instead of guesswork. You can see whether your profile lines up with bank-style products, SBA-oriented options, revenue-based offers, or asset-backed products before you commit to a full application.

That matters most for borrowers in the middle ranges. If your score is excellent, many doors stay open. If your score is weak, every inquiry matters more. Safe comparison becomes part of the underwriting strategy itself.

The best borrowers don't apply everywhere. They narrow the field first, then let one lender perform the hard pull that actually has a purpose.

Frequently Asked Questions About Business Loan Credit

A few questions come up in nearly every funding conversation. Here are the straight answers.

Quick answers

| Question | Answer |

|---|---|

| Does a business loan always use my personal credit? | Not always, but many lenders review it, especially when the business is smaller, newer, or doesn't have a deep business credit file. |

| Can I get funding with bad credit? | Sometimes, yes. Approval often depends on the product type, repayment source, collateral, revenue consistency, and documentation quality. |

| Is there one minimum score for every lender? | No. Credit thresholds vary by lender, product, and risk model. |

| Do SBA loans require stronger credit than online lenders? | Usually, yes. SBA-backed options often have tighter expectations than many online or alternative products. |

| Will shopping for loans hurt my score? | It can if every lender runs a hard inquiry. That's why pre-approval and soft-pull screening matter. |

| Can strong revenue offset a lower score? | In many cases, it can help. It usually won't erase weak credit, but it can improve how some lenders view risk. |

| What if my business credit is thin? | Expect lenders to lean more on personal credit and on the strength of your financial documents. |

| How fast can I improve my credit profile? | There's no universal timetable. Error correction, lower balances, cleaner payment history, and stronger documentation usually help more than quick-fix tactics. |

The questions owners should ask lenders

Before you authorize a full application, ask these directly:

- Is the initial review a soft pull or a hard pull?

- What credit profile matters most for this product, personal or business?

- What documentation can offset a weaker score?

- Is this product underwritten mainly on cash flow, collateral, or general credit quality?

Those questions cut through vague sales talk fast.

One final practical point

Don't wait until the funding need is urgent. Credit strategy works best before the pressure hits. Owners who review their files early, organize documents, and use pre-approval carefully usually keep more options open when timing matters most.

Business Loan Warrior gives owners a practical way to compare financing without jumping straight into blind applications. Through a single pre-approval application at Business Loan Warrior, you can review personalized funding options, check fit before committing, and move toward the right lender with more clarity and less credit risk. If you want a safer way to shop for business financing, it's a strong place to start.