You've likely already done the exciting part. You found the site, talked through the layout, sketched the expansion, and started pricing the build. Then the financing conversation began, and suddenly the project felt less like growth and more like paperwork, inspections, draw requests, and lender conditions.

That reaction is normal. Construction project financing is not a standard business loan with a bigger dollar amount. It's a controlled funding process built around a moving target: a project that doesn't exist yet, depends on multiple parties, and can go sideways if budget, timing, or documentation slips.

For a small to mid-size business owner, that difference matters in practical ways. The financing structure affects when your contractor gets paid, how much cash you need to keep in reserve, how often you'll be asked for documents, and what happens if the project changes midstream. If you're early in the process, this guide on what small businesses should know before breaking ground is a useful companion.

The good news is that this situation is manageable once you understand how lenders think and how the money moves through a project.

Table of Contents

- From Blueprint to Reality Awaiting a Signature

- Decoding Construction Finance Fundamentals

- Comparing Your Top Financing Options

- The Lender's Checklist for Underwriting

- Your Step-by-Step Application Roadmap

- Managing Project Risk and Contingencies

- Build with Confidence and the Right Partner

From Blueprint to Reality Awaiting a Signature

A familiar scenario goes like this. A company has outgrown its current space. The owner needs a new warehouse, a second location, a medical office buildout, or a manufacturing expansion. The plans look solid. The contractor says the schedule is workable. Then the lender asks for plans, budget detail, permits, equity injection, contractor information, projected cash flow, and a draw process the owner has never dealt with before.

That's where many good projects stall. Not because the project is weak, but because the owner assumed financing would work like buying a finished building. It doesn't. In construction, the lender is funding a process, not just an asset.

I've seen owners get tripped up by the same issue again and again. They focus on rate first and structure second. In construction financing, that's backwards. If the draw process is clunky, if the contingency is thin, or if the contractor paperwork is sloppy, a lower rate won't save the project from delays.

The best financing package isn't the one that looks cheapest on day one. It's the one your team can actually execute without starving the project of cash mid-build.

That's why experienced borrowers treat financing as part of project management. The loan terms influence vendor relationships, inspection timing, and even how confident a contractor feels taking your job. Once you understand those moving parts, the financing stops feeling like a brick wall and starts looking like a build plan with rules.

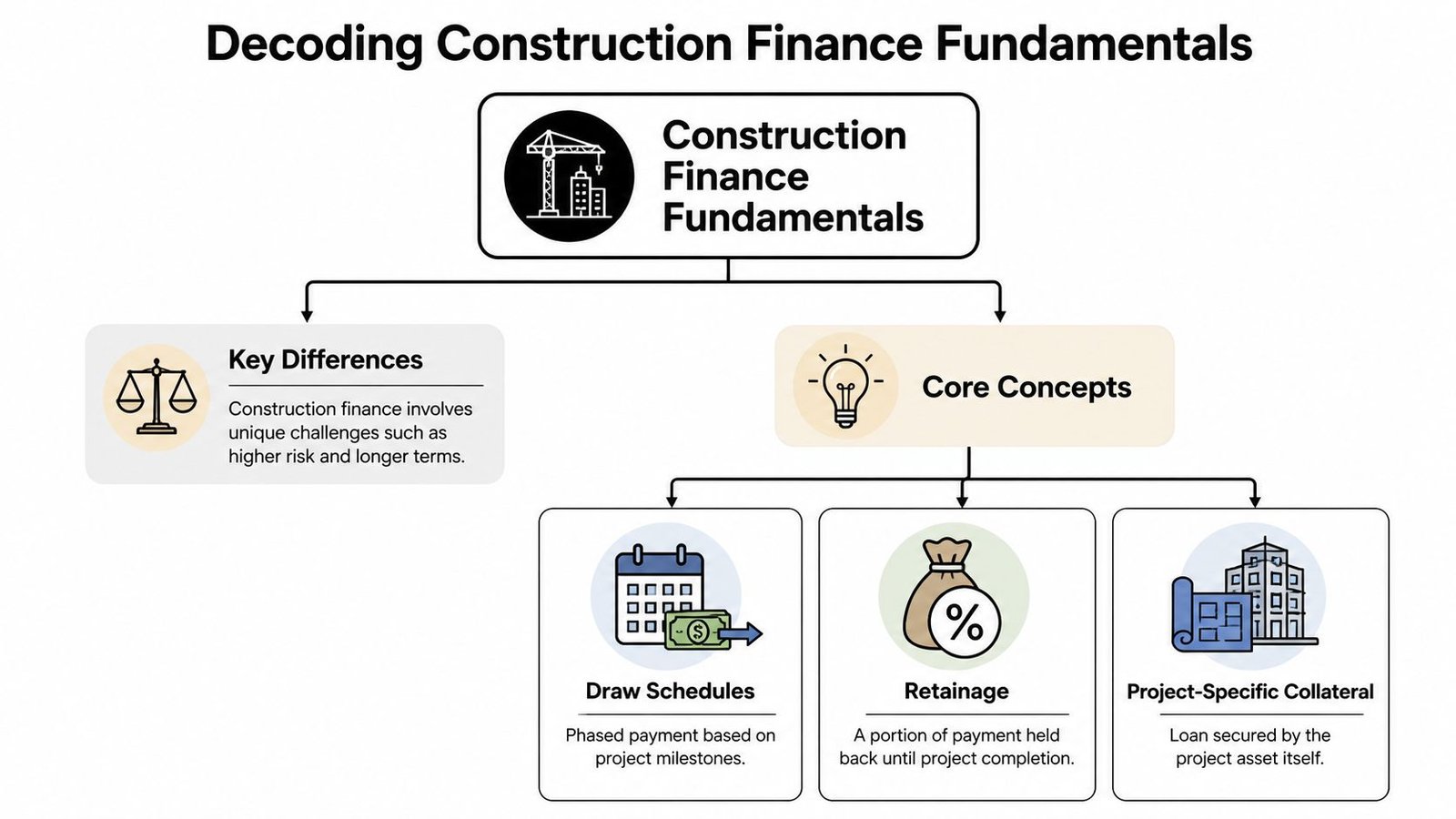

Decoding Construction Finance Fundamentals

Construction financing exists because the money goes out long before the project starts producing value. Carnegie Mellon notes that construction investment is a short-term cost that produces long-term benefits, which is why contractors and developers often need bridge financing during the build phase, with funding structured around the project schedule rather than the long life of the asset, as explained in Carnegie Mellon's construction finance reference.

Why this loan behaves differently

Think of it this way. Buying an existing building is like buying a finished machine. Construction project financing is like paying to assemble that machine in stages, with several teams handling different parts, while the lender checks the work before releasing the next batch of money.

That staged approach is why construction loans involve more monitoring than ordinary term loans. The lender isn't just asking, “Can this borrower repay?” The lender is also asking, “Is the project progressing as planned, and is the unfinished collateral becoming more valuable with each draw?”

If you're weighing how this differs from other asset-based borrowing, this breakdown of construction loans versus equipment financing helps clarify where owners often mix the two up.

The terms that affect daily operations

A few terms matter more than the rest because they show up during the build, not just at closing.

- Draw schedule means the lender releases funds in phases, usually after verifying completed work. If your contractor expects weekly money but your lender draws monthly after inspection, you have a coordination problem.

- Retainage means part of a payment is held back until later in the project. Owners sometimes underestimate how much this affects subcontractor cash flow and morale.

- Lien waiver is a document confirming a contractor or supplier has been paid and waives the right to file a lien for that amount. It's one of the simplest tools for preventing a payment dispute from becoming a title problem.

- Completion risk is the risk that the project costs more, takes longer, or doesn't reach usable completion as planned.

Here's the practical takeaway. The financing mechanics shape your jobsite behavior. They determine when invoices need to be submitted, what backup has to accompany payment requests, and how disciplined your budget management must be.

Practical rule: Never approve a draw request the way you'd approve a routine accounts payable batch. A draw is part payment event, part legal control, and part lender reporting package.

Owners who do well in this process usually assign one person to own the paperwork trail. That person tracks invoices, draw support, change orders, inspections, lien waivers, and lender requests in one place. Without that discipline, even a good project can get jammed up by preventable administrative delay.

Comparing Your Top Financing Options

Most owners start by asking which loan type has the lowest rate. A better question is which option best fits the project's size, timeline, and tolerance for structure. In the current market, that choice isn't as simple as “go to your bank.” The construction lending market has become more fragmented, with nonbank lenders playing a larger role and often offering more speed or flexibility at a higher cost, as discussed in ConstructConnect's coverage of nonbank construction funding.

Construction financing options at a glance

| Feature | SBA Loans (7a, 504) | Traditional Bank Loan | Alternative/Fintech Lender |

|---|---|---|---|

| Best fit | Owner-occupied projects and borrowers who want structured support | Strong borrowers with organized financials and a clear project story | Borrowers who need flexibility, speed, or a second option when banks tighten |

| Speed | Often slower due to process and documentation | Moderate, depends on lender appetite and project complexity | Often faster, but review can still be detailed |

| Cost | Often competitive, but structure matters | Often attractive when the deal fits bank policy | Usually higher borrowing cost |

| Equity requirement | Owner contribution is typically required | Owner contribution is typically required | Usually required, sometimes with stricter economics |

| Underwriting style | Documentation-heavy, often process-driven | Credit, cash flow, collateral, and project discipline | More flexible on structure, often tougher on pricing or controls |

| Best use case | Stable operating business building for its own use | Straightforward project with solid contractor, budget, and borrower strength | Time-sensitive deal, unusual project, or gap left by bank pullback |

How owners usually choose

SBA financing can work well when the project is tied to your own operating business and you want a structure that supports longer-term occupancy plans. The trade-off is that paperwork discipline matters. If your file is loose, the process can drag.

Traditional banks remain the natural first stop for many borrowers. If your business financials are clean, your equity is available, and your contractor package is credible, a bank can be an excellent fit. Banks usually like projects they can explain clearly in a credit memo. Clean story, clean file, clean execution.

Alternative and fintech lenders fill a real gap. They can be useful when timing matters, when a deal falls outside normal bank boxes, or when the borrower needs a more customized capital stack. The trade-off is usually cost, tighter controls, or both.

A few decision filters help narrow the field fast:

- Choose SBA when your project supports your operating business, you can tolerate a more formal process, and you want a financing structure built for small business use.

- Choose a bank when your project is straightforward, your records are strong, and you want a relationship lender that may also support treasury, lines of credit, or permanent financing later.

- Choose an alternative lender when the opportunity is real, the timing is compressed, or a bank has become too rigid for the deal in front of you.

If rate comparison is part of your screening process, this guide to construction loan rates gives useful context on how owners evaluate pricing against structure.

Fast money can be expensive. Cheap money can be slow. The right answer is the one that fits your schedule, your contractor's payment rhythm, and your margin for delay.

One caution matters here. Owners sometimes pair a complex project with a financing source that's only attractive on paper. A lender that doesn't understand construction administration can create friction after closing. When that happens, the project doesn't fail because the approval was denied. It fails because the money can't move smoothly once work begins.

The Lender's Checklist for Underwriting

Lenders rarely fund the full cost of a project, and they underwrite based on plans, cost estimates, and projected cash flow, not just on the borrower's name, as outlined in the AGC Guide to Construction Financing.

What the lender is really trying to prove

A lender reviewing your deal is testing several things at once.

First, can the borrower support the project if the build gets messy? That includes business performance, liquidity, guarantor strength, and whether the owner has enough skin in the game.

Second, does the project make sense on paper? The budget has to match the plans. The schedule has to match the scope. The contingency has to match the risk. If those pieces don't line up, the lender assumes the project team is guessing.

Third, can the contractor and professional team execute? Lenders pay attention to the general contractor, architect, engineer, and sometimes third-party reviewers because a weak team can destroy a good capital structure.

The file that gets traction

The strongest loan packages tell a coherent story. They don't just dump documents into a folder.

A workable underwriting package usually includes:

- Detailed plans and specs that show exactly what is being built, renovated, or expanded.

- A sources-and-uses budget that separates hard costs, soft costs, equity, and loan proceeds.

- A realistic schedule that shows major milestones and how draw timing will line up with work in place.

- Contractor package including contract, credentials, insurance information, and evidence the builder can handle the job.

- Borrower financials that show operational stability and the ability to absorb surprises.

A lender can live with risk. What a lender hates is uncertainty caused by inconsistent documents.

Here's where many owners weaken their own application. They provide a contractor estimate that doesn't match the architectural plans. Or they submit projections that assume the project opens instantly at full strength. Or they leave soft costs vague because they're still collecting bids.

That approach forces the lender to become skeptical. A better approach is to identify open items directly. If a permit is pending, say so. If a vendor quote is still being finalized, mark it clearly and show your placeholder assumption. Lenders don't expect perfection. They expect control.

When owners prepare the package this way, underwriting moves faster because the credit team spends less time trying to reconcile contradictions.

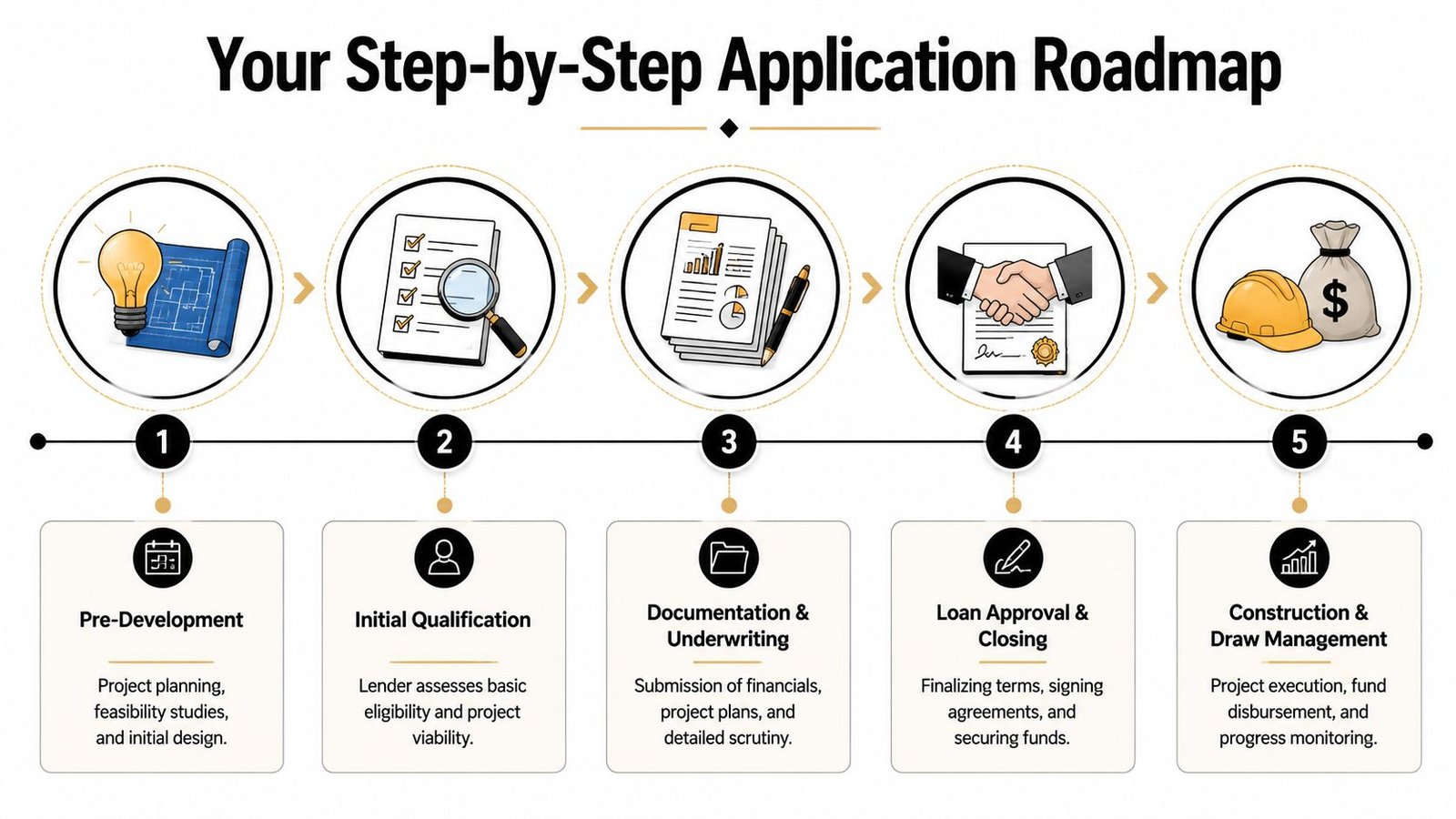

Your Step-by-Step Application Roadmap

Many owners think the financing process starts when they submit a formal application. In reality, it starts earlier, during the stage where money is being spent on concept work, site analysis, engineering, legal review, and permitting. HUD highlights that pre-development costs are often funded separately from the main construction loan, and that capital is commonly staged across pre-development, construction, and permanent financing, as described in HUD's overview of basic project financing.

To make that progression easier to visualize, start with the roadmap below.

The stages most owners miss

A clean construction financing process usually unfolds in five practical phases.

Pre-development

Site control, preliminary design, feasibility work, and permitting all begin in this phase. Owners also frequently invest significant funds during this period, prior to a bank issuing the main construction commitment.Initial qualification

The lender takes a first look at the borrower, project type, rough budget, and likely structure. This stage tells you whether the deal fits the lender's appetite before everyone wastes time on a full package.Documentation and underwriting

This is the deep review. Financial statements, plans, contracts, budgets, and projections all get pressure-tested. If a deal slows down, it usually slows here.

Before moving deeper into the process, some owners like a visual primer. This short video can help frame how lenders and borrowers move through the application cycle.

Approval and closing

Loan documents are finalized, conditions are cleared, equity requirements are confirmed, and the draw administration process is established.Construction and draw management

Here, significant discipline is required. Work progresses, inspections occur, draw requests are reviewed, and paperwork has to stay current all the way to completion.

The handoffs that slow projects down

The biggest delays usually happen at handoff points between parties, not because the financing is impossible.

Common trouble spots include:

- Owner to lender when documents are incomplete or revised versions are floating around.

- Contractor to owner when pay applications don't match the approved budget lines.

- Owner to title or closing parties when lien waiver requirements aren't understood.

- Project team to permanent financing when the construction loan nears completion but the takeout plan hasn't been prepared.

A practical workflow looks like this:

- Assemble your team early. Lender, contractor, architect, and legal counsel should be working from the same version of the project story.

- Create a document map. Don't rely on email memory. Track who owes what, in what format, and by when.

- Separate pre-development from construction funding. They're related, but they're not the same credit event.

- Plan for conversion or payoff before the first draw. A project shouldn't reach the finish line without a clear path for what comes next.

Owners who treat the financing process like a managed timeline, rather than a one-time loan application, usually avoid the worst surprises.

Managing Project Risk and Contingencies

Getting approved is only half the job. A financed project can still lose money if the owner treats risk management as an afterthought. Strong operators distinguish themselves from hopeful ones through effective risk management.

Protect margin before the first overrun

The best protection starts before construction mobilizes.

Use these controls from day one:

- Build a real contingency that reflects the job's uncertainty, not your optimism. A contingency is there for scope gaps, timing friction, field conditions, and pricing surprises.

- Enforce change order discipline. If work changes, price it, document it, and understand whether the lender must approve it before the contractor proceeds.

- Collect lien waivers with every payment cycle. This helps prevent the nightmare scenario where you think a sub has been paid but the title record says otherwise.

- Match the draw package to the budget. If your budget categories are vague, your draw review will be messy, and disputes will follow.

- Monitor schedule drift early. A small delay can become a financing issue if inspections, occupancy, or loan maturity dates start colliding.

The project usually doesn't blow up from one giant mistake. It bleeds margin through small approvals nobody controlled tightly enough.

Owners sometimes treat draw inspections like a nuisance. That's a mistake. The inspection process is one of the few moments where everyone is forced to compare the field, the invoices, and the budget at the same time. Used well, it's an early warning system.

Bankability improves when revenue risk drops

In larger project finance transactions, lenders may use non-recourse or limited-recourse structures where repayment depends primarily on project-level revenues rather than the sponsor's broader assets, and a practical takeaway for smaller businesses is that contracted revenue can improve bankability and lower capital cost, as discussed in Morgan Lewis on project finance structures.

That lesson applies even outside formal project finance. If you can show the finished property will have dependable revenue, the deal gets easier to finance.

Examples include:

- Pre-leased space in a retail, office, or industrial project

- Long-term customer commitments tied to the expanded facility

- Service contracts or offtake-style arrangements that make future cash flow easier to underwrite

This isn't only about lender comfort. It also changes how you manage your own downside. A project with visible post-completion revenue gives you more room to handle delays or carry costs without panicking.

Build with Confidence and the Right Partner

Construction project financing rewards preparation. Owners who understand the mechanics behind draws, lender controls, contractor paperwork, and staged capital tend to make better decisions before the project becomes expensive to fix.

The practical pattern is consistent. Strong projects start with realistic pre-development planning, move into the right financing structure for the deal, arrive at underwriting with a coherent package, and stay disciplined through draws, change orders, and payment controls. Weak projects usually break down at the seams between those steps.

If you're a business owner, keep one principle in front of you: the loan is part of the jobsite. It affects timing, communication, cash flow, and bargaining power with your vendors. Treat it like an operating system for the project, not a separate financial event.

A good financing strategy won't eliminate construction risk. Nothing can. What it does is give you a framework for controlling that risk while keeping the build moving.

That's the right mindset for a new facility, expansion, renovation, or owner-occupied development. Get the structure right, and the project has room to succeed. Get it wrong, and even a promising build can become a cash flow problem with concrete walls.

Business Loan Warrior helps owners manage that complexity without adding more friction. Through a single, no-fee application, you can explore funding options, check pre-approval without affecting credit, and track progress in one secure dashboard. If you're comparing construction financing, SBA support, lines of credit, or other growth capital, Business Loan Warrior gives you a practical way to move from application to funding with both technology and human guidance.