Growth usually gets expensive before it gets easy. You're selling well, the team is stretched, and the next move is obvious: a second location, more equipment, a deeper inventory position, a hiring push, or a new product line. The problem is that growth eats cash at the front end. Payroll starts before revenue catches up. Equipment payments begin before output stabilizes. Lease obligations arrive before the new site finds its rhythm.

That's where business expansion loans become useful. Not as a generic source of capital, but as a way to fund a specific move with a structure that fits the economics of that move. Good financing supports expansion. Bad financing turns growth into a liquidity problem.

Table of Contents

- Why Expansion Capital is a Strategic Tool

- Decoding Business Expansion Loan Products

- What Lenders Look for to Approve an Expansion Loan

- Matching the Right Loan to Your Growth Strategy

- Your Application Roadmap from Start to Finish

- Common Pitfalls and Smarter Alternatives

- Your Next Steps to Secure Growth Funding

Why Expansion Capital is a Strategic Tool

A strong business can still stall. I've seen owners with healthy demand delay expansion because cash is trapped in receivables, inventory, build-out costs, or the timing gap between hiring and production. They aren't failing. They're outgrowing the capital structure that got them this far.

That's why expansion capital matters. The Federal Reserve's Small Business Credit Survey found that in 2023, 59% of employer firms sought funding, and among those applicants, 46% were seeking capital to expand the business, pursue new opportunities, or acquire assets, within a U.S. small-business lending market estimated at about $1.4 trillion, as summarized by Credit Suite's review of small-business lending statistics and trends.

Expansion debt works best when it does one thing clearly. It helps you move sooner than retained earnings alone would allow, while keeping day-to-day operations stable. That could mean financing a build-out without draining working capital, buying revenue-producing equipment without choking payroll, or entering a new market before a competitor gets there first.

Practical rule: Borrow for a defined growth event, not for a vague ambition.

Owners who use debt well usually know exactly what the capital is supposed to accomplish. They know whether they're funding a fixed asset, a temporary working-capital squeeze, or a staggered rollout. They also know what success looks like. More capacity, stronger margins, faster fulfillment, broader geographic reach, or a cleaner path to larger contracts.

If you're at the point where growth is starting to pressure your balance sheet, the financing conversation needs to be strategic, not reactive. This is the same discipline behind growing an established business with smart financing and operational scaling. The goal isn't just to get approved. It's to choose capital that gives the expansion room to work.

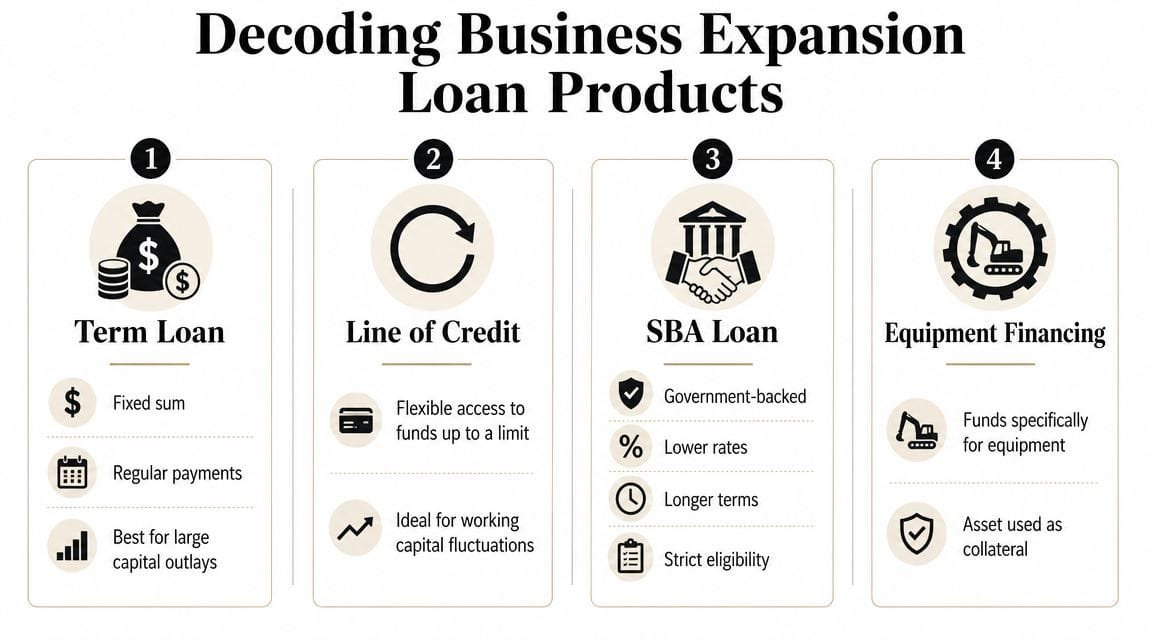

Decoding Business Expansion Loan Products

Not all business expansion loans solve the same problem. Owners often shop by rate first, but structure usually matters more. The right product depends on whether you're financing a one-time investment, a recurring cash need, or an asset with clear collateral value.

What each product is built to do

Term loans are the classic choice when the project has a defined cost and a defined payoff period. Think leasehold improvements, a major remodel, a controlled acquisition of inventory tied to expansion, or a product launch with a clear budget. You receive a lump sum and repay it on a schedule. That makes term loans easier to model, but less flexible if the project scope shifts midway.

Lines of credit fit uneven working-capital needs. If the expansion creates timing gaps, such as carrying payroll ahead of receivables, buying inventory before a seasonal push, or managing vendor deposits during a rollout, a line is often more practical than a lump-sum loan. You draw what you need, when you need it, up to a limit. For short-cycle needs, that flexibility matters more than a fixed amount.

SBA 7(a) loans are often the most versatile option for established businesses with a broad expansion plan. According to the SBA's 7(a) loan program overview, these loans can fund real estate, equipment, working capital, and refinancing, with loan amounts of up to $5 million. The same SBA guidance notes that maturities can extend up to 25 years for real estate, which can reduce monthly payment pressure during the early phase of an expansion.

The biggest advantage of a longer-term structure is simple. It gives the project time to produce cash before debt service becomes a strain.

Equipment financing is the specialist tool in the group. If your expansion depends on vehicles, production machinery, kitchen equipment, medical devices, or other tangible revenue-producing assets, this can be a cleaner fit than a general-purpose loan. Because the financed asset serves as collateral, lenders often view the request differently than they would an unsecured working-capital loan. That doesn't guarantee easier approval, but it does align the debt with the equipment's useful life.

For short gaps between permanent financing events, some owners also look at interim capital. If that's your situation, it helps to understand how bridge loans can support business expansion timing.

Comparing top business expansion loans

| Loan Type | Best For | Typical Term | Key Feature |

|---|---|---|---|

| Term Loan | Build-outs, large one-time growth investments, major launch budgets | Fixed repayment period set by lender and use case | Lump-sum funding with predictable payments |

| Line of Credit | Inventory swings, payroll timing gaps, rollout-related working capital | Revolving access rather than one fixed amortization schedule | Flexible draws as needs arise |

| SBA 7(a) Loan | Multi-part expansion plans involving real estate, equipment, or working capital | Can run long, including up to 25 years for eligible real estate uses | Broad use of proceeds and longer maturities |

| Equipment Financing | Trucks, machinery, production assets, specialized tools | Matched to the asset and lender terms | Asset-backed structure tied to the purchase |

A quick way to choose between them is to ask one question. Are you funding a project, a cycle, or an asset? Projects usually fit term debt. Cycles often fit a line. Assets often fit equipment financing. Mixed-use growth plans are where SBA-backed structures tend to stand out.

What Lenders Look for to Approve an Expansion Loan

Owners often assume underwriting is mainly about collateral and credit score. In practice, lenders spend more time asking whether the expansion will produce enough cash to repay the debt without stressing the core business.

Bankability matters more than enthusiasm

Lenders underwrite expansion loans by focusing on the business's capacity to generate enough incremental earnings to service the new debt. One lender resource explains that these loans are generally designed for businesses at least two years old with strong financial performance and a clear, data-backed expansion plan, as outlined by PNC's guidance on using a business loan for expansion.

That standard matters because expansion risk is different from startup risk. A lender isn't just evaluating whether your existing operation is healthy. They're evaluating whether the next move is realistic, timed well, and supported by evidence rather than optimism.

A strong file usually answers questions like these:

Why now

Show what changed. New contracts, capacity constraints, geographic demand, vendor opportunities, or operating bottlenecks all help if they're documented.Why this amount

Lenders want to see a use-of-proceeds breakdown that ties directly to the expansion. Round numbers with no support create friction.What repays the debt

The answer can't be “growth.” It needs to be gross profit from a new location, added production volume, stronger utilization, or another defined cash source.

What your file needs to prove

Most approvals rise or fall on the quality of the narrative behind the numbers. Financial statements, tax returns, ownership information, debt schedules, and projections are necessary. But the lender is really testing whether the business can absorb the new obligation and still operate comfortably if the expansion takes longer than expected.

Lenders don't reward ambition by itself. They reward plans that still work when revenue ramps slower than the owner hopes.

This short video gives a useful primer on how lenders think about approval and risk during the financing process.

Three details deserve extra attention:

- Consistency in the historical financials matters because it shows the base business can carry the expansion period.

- A realistic projection model matters because lenders can spot inflated assumptions quickly.

- Collateral awareness matters because asset support can strengthen a request, even when repayment still depends on cash flow.

If your business is established, profitable, and operationally disciplined, the right preparation can make underwriting feel much less mysterious. If the file is thin, lenders will fill the gaps with caution.

Matching the Right Loan to Your Growth Strategy

The most common financing mistake isn't choosing the wrong lender. It's choosing the wrong structure for the job. Expansion plans look similar from a distance, but the cash profile of each one is different.

When the expansion is a new location

A second site, satellite office, or additional service territory usually has several layers of cost at once. Leasehold improvements, deposits, equipment, signage, staff hiring, marketing, and working capital all hit before the new location reaches stable revenue. For these reasons, a longer-term, flexible-use structure often makes sense.

For many established operators, an SBA 7(a) loan fits this scenario well because one facility can cover multiple uses under one expansion plan. That's especially helpful when the project isn't just a real estate decision. It's also a staffing, equipment, and operating-capital decision.

If the expansion has a long ramp-up, short-duration debt can put the new location under pressure before it has a fair chance to perform.

When the expansion is equipment capacity

A manufacturer adding a production line, a contractor buying trucks, or a restaurant outfitting another kitchen has a different profile. The asset itself is central to the growth plan, and the purchase usually has a direct connection to revenue capacity. In that case, equipment financing is often the cleaner choice because the debt is tied to the equipment being acquired.

That structure works best when the equipment is identifiable, essential, and expected to generate value over time. It works less well when the equipment purchase is only one small piece of a broader expansion that also requires working capital, hiring, and marketing support.

When the expansion is inventory, hiring, or launch timing

Some growth plans aren't about a building or a machine. They're about timing. A distributor may need to buy more inventory before demand peaks. A service firm may need to hire ahead of a contract start date. A brand may need to fund product launch expenses before sales settle into a pattern.

These situations often call for a line of credit or a modest term structure instead of a large long-term facility. The capital need is usually revolving or uneven, not permanent and fixed. Flexibility becomes more valuable than maximum size.

A practical matching guide looks like this:

New location with build-out and working capital needs

Often best served by a broad-use term structure, frequently SBA-backed when the business qualifies.Revenue-producing equipment purchase

Usually best matched to equipment financing, especially when the asset is central to repayment logic.Seasonal inventory expansion

Often better suited to a line of credit because purchases and paydowns repeat.Hiring ahead of growth

Depends on timing. If payroll pressure is temporary, a flexible working-capital facility often fits better than long-term debt.

The right answer isn't the product with the lowest headline appeal. It's the one that matches how the expansion consumes cash and how it will repay.

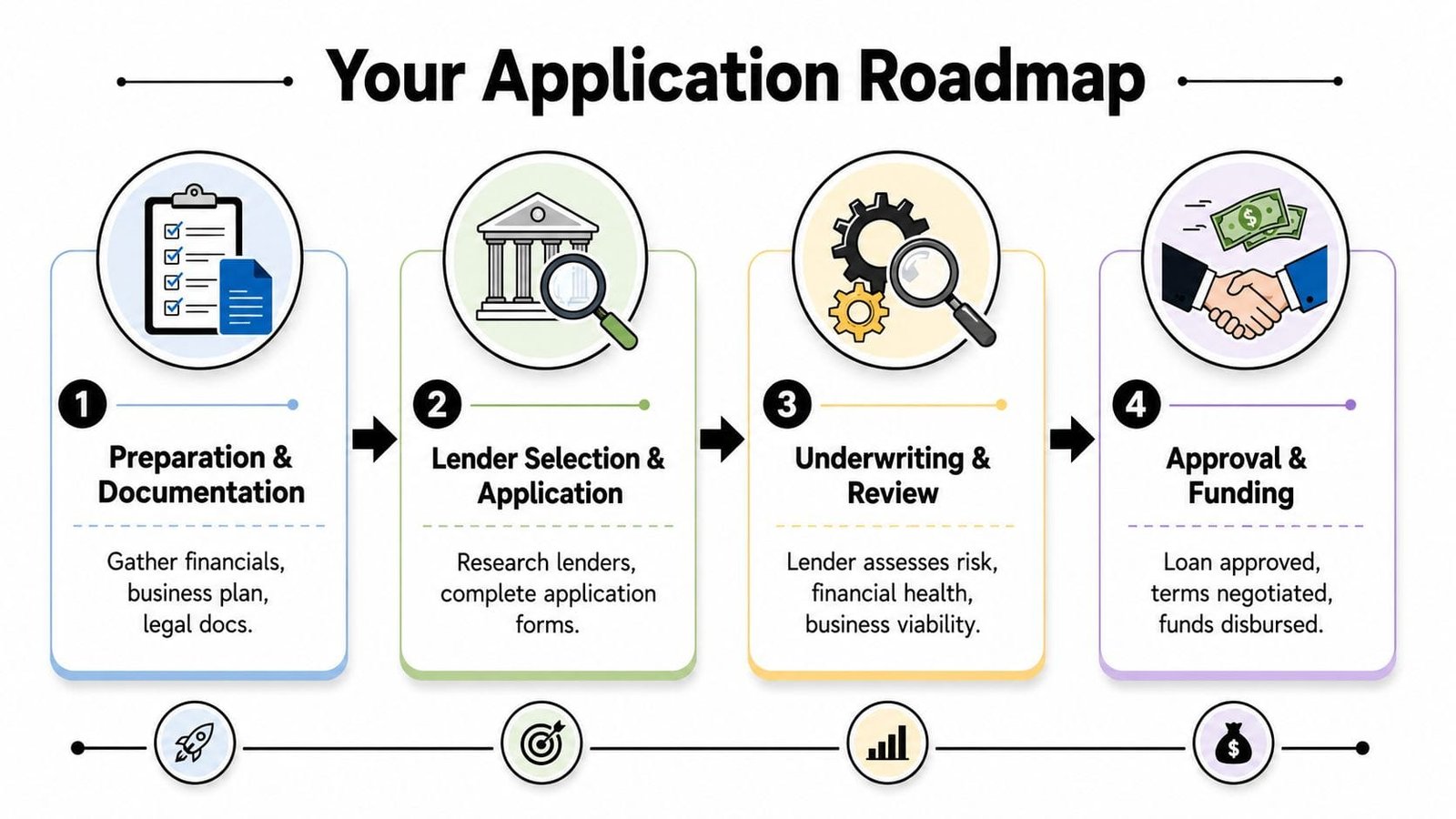

Your Application Roadmap from Start to Finish

The application process feels much easier when you treat it like a transaction, not a mystery. Strong borrowers don't just submit forms. They package a clear credit story.

Phase one and two

Preparation comes first. Gather recent financial statements, business tax returns, ownership documents, current debt details, and a use-of-proceeds schedule. If the expansion is significant, include projections that show how the business performs during the ramp period, not just after everything goes right.

A solid business plan for an expansion loan doesn't need marketing fluff. It needs operating logic. Explain what you're adding, why demand supports it, what costs arrive first, and how repayment works if the rollout takes longer than expected.

Lender selection comes next. Owners frequently lose time by applying too broadly or to lenders that don't fit the transaction. Match the request to the lender's appetite. Banks, SBA-focused lenders, equipment finance groups, and working-capital lenders each evaluate the same business through a different lens.

A few practical screens help:

Use of proceeds fit

Make sure the lender supports the purpose of the loan you need.Documentation tolerance

Some lenders want a highly detailed package. Others move faster but may offer less structural flexibility.Collateral expectations

If the request depends on asset support, identify that early instead of hoping it won't come up.

Phase three and four

Underwriting is the review period. During this time, lenders test consistency. They compare your application, statements, tax returns, debt schedule, and narrative. If one item says the funds are for expansion and another suggests they're plugging an existing cash shortfall, expect questions.

Clean files close faster. Most delays come from missing explanations, inconsistent reporting, or vague use-of-proceeds requests.

Expect follow-up questions. They're normal. A good response is specific and documented, not defensive. If you're opening a new site, show lease terms, build-out scope, staffing assumptions, and expected operating timeline. If you're buying equipment, show quotes, expected utilization, and how the asset affects revenue or margin.

Approval and funding are the final stage. Read the offer with an operator's eye, not just a borrower's eye. Focus on payment burden, structure, collateral terms, reporting requirements, and whether the facility matches the expansion plan. Funding solves nothing if the repayment schedule squeezes the project before it stabilizes.

The businesses that handle this process well usually do one thing differently. They present the loan request as a well-scoped growth investment, not as a hopeful ask for capital.

Common Pitfalls and Smarter Alternatives

A lot of owners ask whether they can qualify. Fewer ask whether the debt improves the business. That's the more important question.

The SBA notes that expansion financing can support a wide range of purposes, but broader eligibility doesn't automatically make borrowing wise. It also points to a bigger shift in lending. Lenders increasingly focus on bankability and proven repayment capacity, which reinforces that successful expansion debt is as much about cash-flow resilience as it is about asset purchasing, as reflected in the SBA's broader loan program guidance.

Where expansion loans go wrong

The most common mistake is duration mismatch. Owners use short-term capital for a long-term expansion, then get hit with heavy payments before the project matures. A build-out, market entry, or equipment-heavy initiative usually needs time. If the debt demands quick repayment, the business ends up financing the lender instead of the growth plan.

Another mistake is overestimating the speed of the ramp. New locations often take time to stabilize. New hires usually become productive in stages. New product lines rarely follow the clean curve in the first forecast. If the model only works under favorable assumptions, it's too fragile.

A third mistake is borrowing more than the expansion can absorb efficiently. Extra capital sounds safe, but idle borrowed money still creates repayment pressure.

When another tool fits better

Sometimes a different instrument is better than a traditional expansion loan.

- Invoice financing can make sense when growth is strong but cash is tied up in receivables.

- A line of credit may be better than term debt for temporary working-capital pressure.

- A merchant cash advance may be considered for short-duration needs, but it shouldn't be used casually for long-horizon expansion.

- Layered financing can work if each piece has a clear role and the total debt load remains manageable. Owners benefit from understanding how to layer multiple financing tools without over-leveraging a small business.

The point isn't to avoid debt. It's to avoid using the wrong debt for the wrong job.

Your Next Steps to Secure Growth Funding

A good expansion loan starts long before the application. It starts with a clear business case and an honest view of how the expansion will consume cash before it generates return.

Use this checklist before you approach lenders:

Finalize the business case

Define the expansion in concrete terms. New site, equipment, hiring, inventory, or launch. Tie each item to expected operational impact.Organize the financial package

Prepare current financial statements, tax returns, debt details, ownership information, and realistic projections.Test funding readiness

Ask whether the core business can support the new obligation if revenue ramps slower than expected.Match the structure to the strategy

Don't choose a product because it's familiar. Choose it because it fits the asset life, cash cycle, and ramp timeline.Review alternatives before committing

If the need is temporary, flexible capital may be smarter than a long-term facility.

Expansion works best when capital is matched to the move you're making. That's what keeps growth from turning into strain.

If you're ready to evaluate funding options, Business Loan Warrior gives you a practical place to start. You can check pre-approval through a single no-fee application, review suitable offers, and explore structures that fit your expansion plan without turning the process into a paperwork marathon.