You're running a solid business. Sales are real, customers are paying, and then cash gets tight anyway. A key machine breaks. Inventory is available at a discount if you can move today. A large client pays slowly, but payroll and rent won't wait.

That's the moment many owners start looking at fast funding and stumble into the merchant cash advance business. The pitch sounds simple. Quick approval, money fast, flexible repayment. The problem is that the true cost often hides behind unfamiliar terms, and the cash flow impact can be much bigger than it first appears.

Table of Contents

- Your Business Needs Cash Fast What Are Your Options

- How a Merchant Cash Advance Actually Works

- Calculating the True Cost of an MCA

- When a Merchant Cash Advance Is a Smart Business Move

- Navigating the MCA Application and Approval Process

- How MCAs Compare to Other Business Funding Options

- How to Choose a Provider and Spot Red Flags

Your Business Needs Cash Fast What Are Your Options

A restaurant owner gets a call on Monday morning. The walk-in cooler is failing. Waiting a few weeks for a bank committee isn't realistic. A retailer sees a chance to buy inventory at a strong margin, but the supplier wants payment now. A contractor has work lined up, but cash is tied up in receivables.

Those are not signs of a bad business. They're common operating problems in otherwise healthy companies. The issue is timing. Cash rarely arrives exactly when opportunity or disruption shows up.

That's why fast capital products keep gaining traction. In fact, the merchant cash advance market was valued at $17.9 billion in 2023 and is projected to reach $32.7 billion by 2032, according to Allied Market Research's merchant cash advance market analysis. The same research says North America led global revenue in 2023. That tells you something important. MCAs are no longer a fringe product. They're a mainstream funding option.

The practical menu in front of you

When owners need cash quickly, they usually weigh a short list:

- Traditional bank financing: Lower cost, but often slower and document-heavy.

- Line of credit: Useful if you already have one in place before the crunch hits.

- Short-term financing: Fast and simple for many working capital needs. A practical overview of short-term business financing options helps frame where these products fit.

- Merchant cash advance: Fast access to funds, but with a very different cost structure and repayment rhythm.

The urgent question isn't just “Can I get funded?” It's “What will repayment do to my cash flow next week?”

That's where many owners get tripped up. They compare products by speed, not by structure. Speed matters, but so does how the money gets paid back and what that does to daily operations.

How a Merchant Cash Advance Actually Works

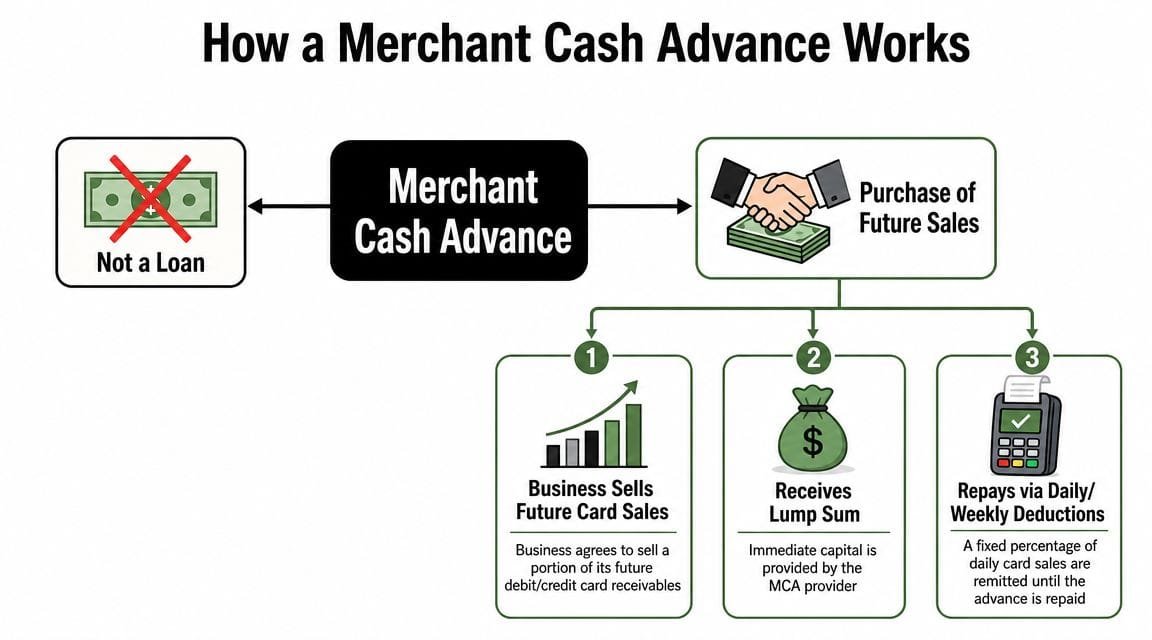

A merchant cash advance, or MCA, is usually not a loan. It's structured as a purchase of future receivables. That sounds technical, but the mechanics are simple once you strip away the jargon.

An MCA can be understood as selling part of a future harvest. You get cash now. In return, the provider takes an agreed share of what your business brings in later. With an MCA, that future harvest is usually your card sales or business receivables.

The four terms that matter most

If you understand these, you'll understand most MCA offers.

- Advance amount: The cash your business receives upfront.

- Factor rate: The multiplier used to determine total repayment.

- Payback amount: The fixed total you must repay under the agreement.

- Holdback or remittance: The share of daily card sales, or fixed ACH withdrawal, used to repay the advance.

According to SoFi's explanation of merchant cash advance regulations and structure, MCA repayment commonly comes from a fixed percentage of daily card sales or fixed ACH withdrawals. The same source notes repayment is often completed in 3 to 18 months, with factor rates commonly ranging from 1.1x to 1.5x.

What makes an MCA feel different from a loan

With a normal term loan, you borrow principal and pay interest over time. As the balance falls, the interest charge usually changes with it. An MCA doesn't work that way.

The provider sets the total payback at the start using the factor rate. Then collections happen automatically until that full amount is satisfied. If your sales are strong, the balance gets paid down faster. If sales slow, repayment may stretch out, depending on the structure.

That creates a confusing point for many owners: flexible payment does not mean cheap payment.

A fluctuating payment stream can make an MCA feel easier to carry, but the total obligation was usually baked in on day one.

Why providers like the structure

From the provider's point of view, the MCA model is attractive because it ties collection to incoming business revenue. They're looking at sales velocity and consistency more than the sort of underwriting a bank might emphasize.

For owners comparing fast-capital products, this matters. An MCA may sit beside short-term loans and invoice-based products in the same conversation, but it behaves differently once repayment begins. A useful comparison of short-term loans, MCA, and invoice factoring for quick capital can help you see those differences before you sign.

Calculating the True Cost of an MCA

Owners must exercise caution. In the merchant cash advance business, the sales pitch often highlights the factor rate because it sounds smaller and cleaner than an annualized cost. But a factor rate is not the same thing as an APR, and that distinction matters.

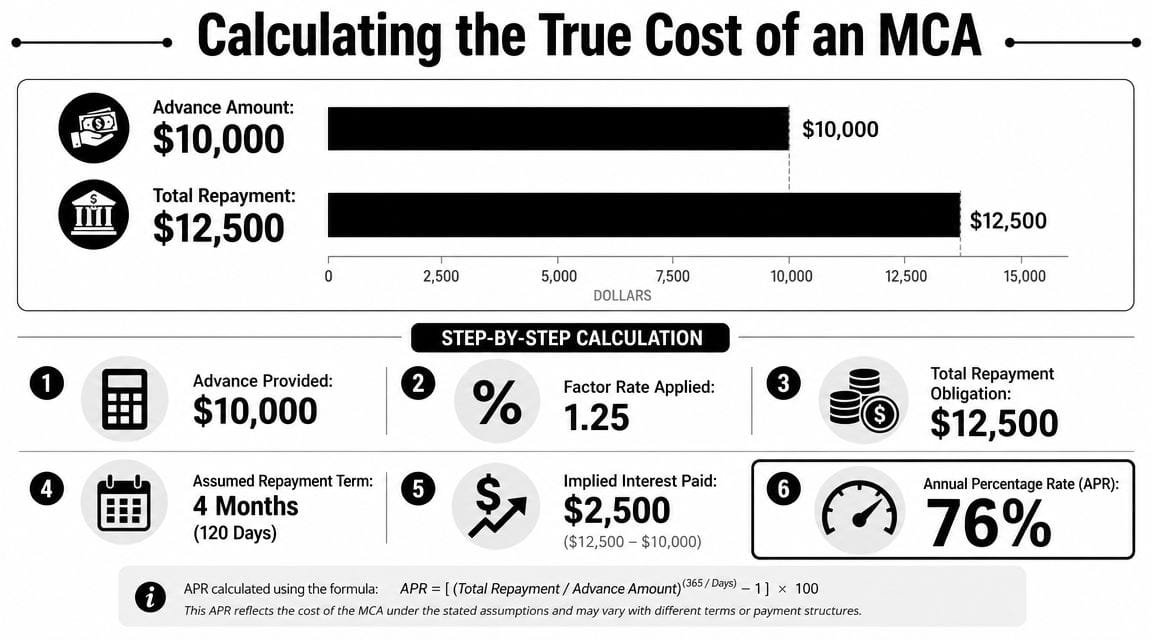

The core economic feature is simple. The pricing is front-loaded and balance-independent. Bankrate's guide to merchant cash advances gives a clear example: if a business receives $100,000 at a 1.4 factor rate, the total repayment is fixed at $140,000 from day one. There is no amortizing interest schedule reducing cost over time.

Start with the payback amount

Use basic multiplication.

If you receive $100,000 and the factor rate is 1.4, then:

| Item | Amount |

|---|---|

| Advance received | $100,000 |

| Factor rate | 1.4 |

| Total repayment obligation | $140,000 |

That means the gross financing cost is $40,000, before any extra fees.

Now bring in the business reality. If remittances are pulled daily from card sales or through recurring ACH, the speed of repayment changes the effective annualized cost. The shorter the payoff period, the more expensive that fixed cost becomes when viewed like a loan.

Why owners get confused on APR equivalents

An APR-style comparison tries to answer this question: if I paid this much financing cost over this amount of time, what would that look like on an annual basis?

You can estimate an MCA's implied APR, but you should treat it as an approximation, not a perfect legal disclosure. That's because actual repayment can speed up or slow down with sales volume. Still, the exercise is valuable because it forces an apples-to-apples comparison against lines of credit and term loans.

A practical way to think about it:

- Identify the advance amount

- Calculate the total payback

- Subtract to find the financing cost

- Estimate the likely repayment period

- Translate that cost into an annualized view

For a deeper walkthrough, this guide on how to calculate the real cost of a small business loan is useful because it frames pricing in decision terms, not just lender terms.

A short explainer can also help visualize the math:

The cash flow test matters more than the headline

The biggest mistake isn't misunderstanding arithmetic. It's ignoring timing.

Suppose two businesses take the same advance with the same factor rate. The one with stronger sales may retire the obligation much faster. That sounds good, but because the total cost doesn't shrink as principal falls, fast repayment can make the implied annualized cost much steeper than the factor rate suggests.

Practical rule: Don't ask only, “What's the factor rate?” Ask, “What's the total payback, and how quickly do you realistically expect to collect it from my business?”

Early payoff usually doesn't create the savings owners expect

Many owners assume they can refinance later or pay early and save money, the way they might with a loan. Often, that assumption doesn't hold with an MCA because the payback amount is usually fixed at origination.

So the right lens isn't “Can I survive this payment today?” It's “Does the use of funds create enough value, fast enough, to justify a fixed and potentially expensive payback?”

If the advance helps you capture a high-margin opportunity or avoid a severe operational loss, the answer may be yes. If you're using it to cover routine shortfalls with no clear return, the answer is often no.

When a Merchant Cash Advance Is a Smart Business Move

An MCA is a tool. Expensive tools still have a place when they solve the right problem.

The strongest use cases tend to share one trait. The business can point to a near-term economic reason the advance makes sense. Not hope. Not vague optimism. A concrete operating outcome.

Good reasons to consider one

A merchant cash advance may be reasonable when timing is the whole game.

- Emergency continuity: A critical repair keeps your doors open or prevents spoiled inventory.

- Time-sensitive inventory buy: You can lock in product that should produce a strong gross profit quickly.

- Short bridge to known receivables: You have a predictable path to incoming cash, but the gap is immediate.

- Revenue-backed expansion burst: A proven channel needs capital now, and delay would cost more than the funding.

In these situations, speed has real value. If delayed action costs sales, customers, or operations, paying more for faster capital can be rational.

Seasonal businesses need extra discipline

The merchant cash advance business involves greater nuance when considering its repayment structure. MCAs are repaid through a percentage of daily sales, which can strain cash flow during volatile or seasonal periods. The Emory law research discussing MCA repayment mechanics and liquidity pressure notes that daily pulls can compress operating liquidity during the off-season when working capital is already tight.

That doesn't mean seasonal businesses should never use MCAs. It means they need to model the worst month, not the average month.

Ask yourself:

- What happens in my slowest sales period?

- How much operating cash do I need after remittances clear?

- Will this advance fund a clear return, or just patch a recurring hole?

If your margin is thin and your sales swing sharply, daily remittances can turn a manageable slow month into a cash squeeze.

Bad reasons to use one

Some uses should make you stop.

Using an MCA to cover chronic losses, stack one advance on top of another, or fund a long-term project with uncertain payoff usually creates stress, not relief. The product works best for short-duration needs with visible business logic. It works poorly as a substitute for durable capitalization.

Navigating the MCA Application and Approval Process

MCA applications are usually faster and less document-heavy than bank loan packages. That's one reason owners turn to them under pressure. The tradeoff is that the provider focuses heavily on your revenue behavior, because that's what repayment depends on.

In practice, providers often want recent business bank activity, payment processing history if card sales are central to your operation, and basic business details. They're trying to answer a narrower question than a bank would ask: does this business produce enough recurring inflow to support automatic collections?

What providers are really reviewing

They're often less focused on a long narrative about your business and more focused on patterns in the numbers.

Look at the application from their side:

- Revenue consistency: Are deposits steady, or do they swing sharply?

- Sales channel quality: Is card volume strong and recurring if repayment is tied to card sales?

- Cash balance behavior: Does the account stay healthy, or does it run close to empty?

- Operational stability: Are there signs the business is functioning predictably?

That's why clean records matter. If your statements are hard to interpret, approval may get slower, even in a fast-moving product category.

How to prepare before you apply

A little organization can improve both speed and clarity.

Pull current statements

Gather recent business bank statements and payment processing statements if applicable.Know your use of funds

State the purpose plainly. Equipment repair, inventory purchase, bridge need, or another immediate operating requirement.Map your cash inflows

Be ready to explain when revenue lands and whether sales are stable, rising, or seasonal.Review your weak spots

If there were unusual dips or overdrafts, prepare a short factual explanation.

The fastest applications happen when the owner already understands their own revenue rhythm and can explain it in plain English.

What approval speed can hide

Quick underwriting feels convenient, but it can also push owners past the most important pause point, which is contract review. A fast approval is useful. A rushed signature is dangerous.

Before accepting anything, make sure you know the total payback, the collection method, how remittances are calculated, and what happens if sales drop materially. Those details matter more than how fast the money can hit your account.

How MCAs Compare to Other Business Funding Options

The right comparison is not “MCA versus no funding.” The right comparison is “MCA versus the other realistic ways I can solve this problem.”

That's especially important because MCA structures can sit outside standard loan framing. California's DFPI advisory to small businesses about merchant cash advances warns owners to speak up about possible unfair, deceptive, or abusive practices. That growing scrutiny is one more reason to compare total economics carefully against products with APR-based disclosures.

Funding options at a glance

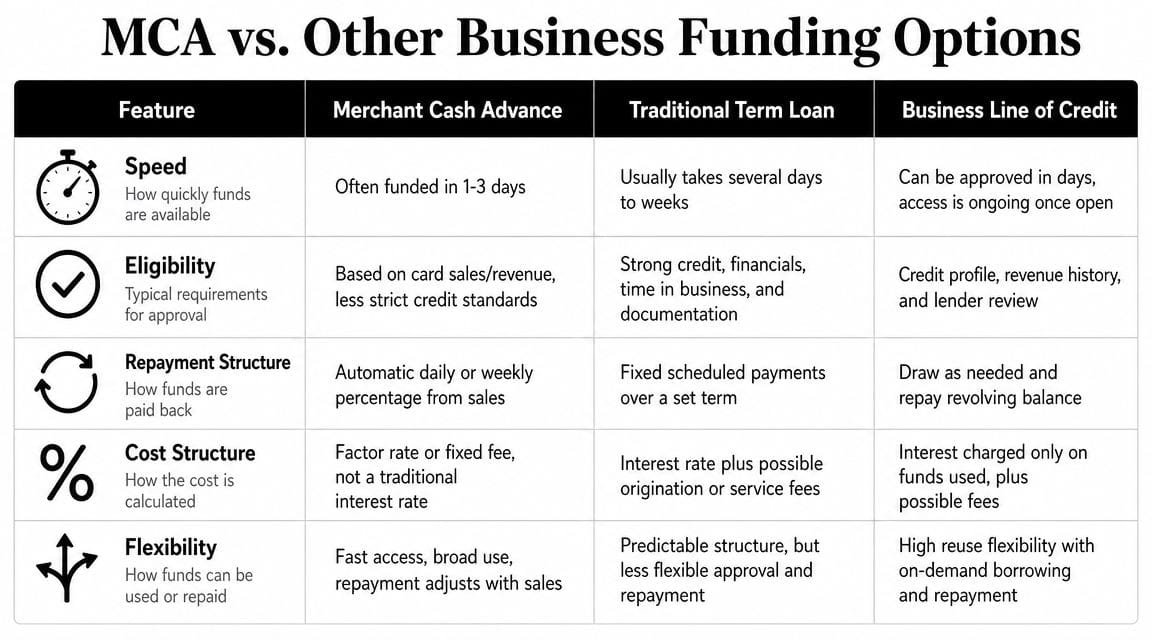

| Funding Type | Typical Speed | Cost Profile | Repayment Structure |

|---|---|---|---|

| Merchant cash advance | Fast | Often expensive and harder to compare directly because cost is usually shown as a factor rate | Daily or weekly remittances tied to sales or ACH |

| Traditional term loan | Slower | Usually easier to compare because pricing is framed more like standard lending | Fixed scheduled payments over a set term |

| Business line of credit | Fast if already established, otherwise moderate | Often more flexible for short working capital needs | Draw as needed, then repay based on line terms |

| Invoice financing | Depends on receivables quality and customer base | Cost depends on invoice structure and timing | Repayment linked to receivable collection |

| SBA-style financing | Usually slower | Often attractive on cost if you qualify | Structured loan payments under formal terms |

The real trade-offs

A term loan is usually better when you have time, documentation, and a stable borrowing profile. A line of credit is often ideal for recurring working capital needs because you don't have to take a full lump sum every time cash gets tight.

An MCA earns its place when the need is urgent and the business can support frequent remittances. It loses its appeal when the funding need is routine, the use of proceeds is vague, or the business would benefit more from revolving flexibility.

A quick decision lens

Use this filter before you move forward:

- If speed matters most, an MCA may stay on the table.

- If cost transparency matters most, term loans and lines of credit often compare more cleanly.

- If your cash flow is uneven, daily remittances deserve extra caution.

- If your need repeats, a line of credit often fits better than repeated advances.

The strongest financing choice usually isn't the one that approves first. It's the one whose repayment structure fits how your business produces cash.

How to Choose a Provider and Spot Red Flags

By the time you're comparing offers, the goal is simple. Slow the process down enough to see what you're really agreeing to.

A solid provider should be able to explain the economics in plain language. If they can't or won't, assume the confusion benefits them, not you.

Red flags that deserve a hard stop

- Pressure to sign immediately: If someone insists the offer disappears unless you sign now, step back.

- Fuzzy payback language: If the total repayment obligation isn't clear, don't move forward.

- Evasive answers on collections: You need to know whether repayment comes from card sales, ACH, or another mechanism.

- No room for review: If they resist giving you documents to read carefully, that's a warning.

- Stacking encouragement: If the proposed solution to stress is more short-term funding piled on top, the risk goes up fast.

How to compare offers like an operator

Don't compare only the amount funded. Compare the structure.

Review these items side by side:

- Total cash received

- Total payback

- Collection method

- Expected repayment speed under your normal sales pattern

- Best-case and worst-case cash flow impact

- Any added fees or contract provisions you don't fully understand

The best offer isn't always the biggest advance. It's the one your business can use profitably without choking next month's operating cash.

If you want help evaluating offers without adding more confusion, Business Loan Warrior gives business owners a way to check funding options through a single no-fee application, compare suitable offers, and review repayment details with guidance before choosing a path.