Your cash is tied up in receivables, payroll hits on Friday, and a repair you can't postpone just landed on your desk. That's when OnDeck usually enters the conversation. It's one of the names business owners hear when they need capital fast and don't want to spend weeks crawling through a bank process.

But speed isn't the same as fit.

A fast loan can solve a real problem, or it can become an expensive patch on a deeper cash flow issue. If you're looking at OnDeck, you need a straight answer to three questions: when it makes sense, when it costs too much for the problem you're solving, and when another route gives you a cleaner outcome. If you need context on short-duration funding in general, this guide to short-term business financing options is a useful companion.

Table of Contents

- Is an OnDeck Loan Your Best Move?

- What Is OnDeck and Who Is It For?

- OnDeck's Loan Products Explained

- The OnDeck Application and Funding Process

- Key Advantages and Drawbacks of OnDeck

- OnDeck vs. Alternatives (Banks and Business Loan Warrior)

- The Final Verdict When to Choose Each Option

Is an OnDeck Loan Your Best Move?

A lot of owners shop OnDeck in a pressure moment. An oven dies in a restaurant. A contractor needs materials before the next draw comes in. A wholesaler gets a large order and has to buy inventory before the customer pays. In all three cases, the problem isn't profitability. The problem is timing.

That's the lane where OnDeck can be useful.

OnDeck is the business lender here, not Garmin's marine monitoring product with the same name. If you're evaluating the lender, the key question isn't whether it's legitimate. The key question is whether the urgency of your situation justifies paying for speed and easier access.

If the financing helps you protect revenue or capture near-term revenue, fast money can be smart money. If it's covering a chronic hole, it usually gets expensive fast.

Use this simple filter before you apply:

- Choose speed when the need is immediate: equipment failure, payroll timing, urgent inventory, or a short gap between invoice and collection.

- Slow down when the need is strategic: expansion, refinancing, major renovation, or anything with a long payoff window.

- Be honest about the source of the problem: a temporary squeeze is one thing. Repeated borrowing to survive ordinary operating weeks is another.

My view is blunt. OnDeck is often a good emergency or opportunity tool. It is not a good substitute for healthy margins, disciplined cash management, or longer-term capital planning.

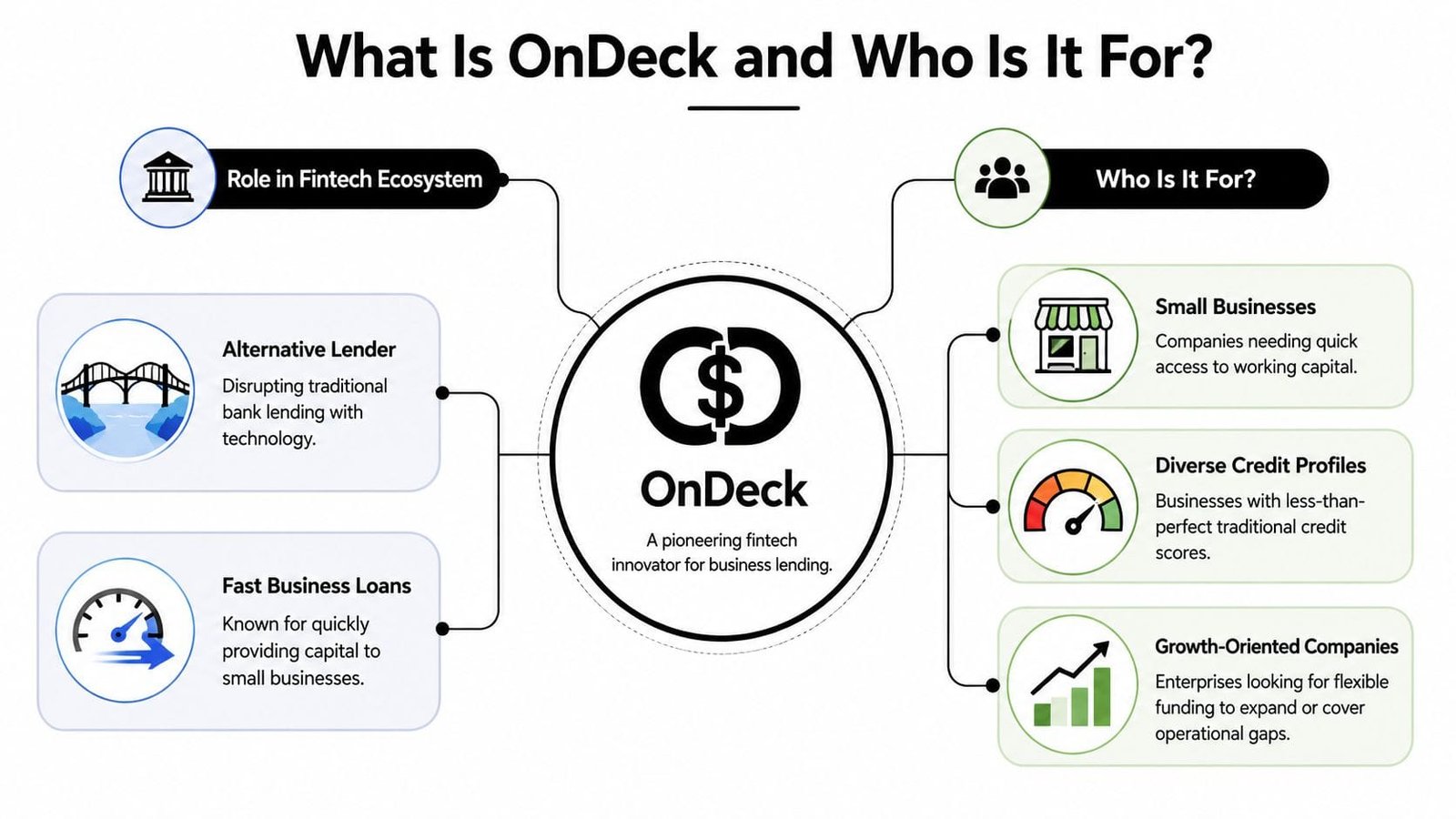

What Is OnDeck and Who Is It For?

OnDeck is an online small-business lender built for owners who need a credit decision fast and can show an operating business, not just an idea. It has been around since 2006 and built its name serving companies that sit between two bad fits. They are often too established for friends-and-family money and too pressed for time, or too lightly documented, for the full bank process.

Here is the clean way to understand it. A bank is usually the cheaper contractor, but it wants blueprints, permits, inspections, and time. OnDeck is the repair crew you call when the pipe burst today. You will usually pay more for that speed. Sometimes that is a smart trade. Sometimes it is how owners overpay for capital they should have sourced elsewhere.

That distinction matters more than the brand name.

OnDeck fits businesses with real revenue, at least some operating history, and a short-term use for cash. The common pattern is simple. You need working capital now, the opportunity or problem has a near-term payoff, and waiting three to six weeks for a traditional lender could cost you more than the higher financing cost.

A good OnDeck candidate usually looks like this:

- You have an operating business, not a pre-revenue startup.

- You need funds for a short-cycle purpose like inventory, repairs, payroll timing, marketing tied to near-term sales, or a brief cash-flow gap.

- You can handle frequent repayments without choking the business.

- You value speed and access more than getting the absolute lowest rate.

- You have a decent but not perfect borrower profile, which may make bank approval slower or less likely.

OnDeck is a weaker fit in three situations. First, you are funding a long-term project like a major expansion, acquisition, or large equipment purchase with a payoff that stretches over years. Short-term money for a long-term project creates pressure fast. Second, your business is already borrowing repeatedly just to cover ordinary weeks. That is not a financing problem. That is a margin or cash-management problem. Third, you have strong financials, clean tax returns, and time to shop. In that case, lower-cost bank financing or an SBA option usually deserves the first look.

This is also where many reviews miss the point. They describe OnDeck as if every owner asking for capital is in the same situation. They are not. A company with stable cash flow and time to compare offers should treat OnDeck as a convenience option, not a default choice. A company in a true timing crunch may decide the premium is justified. And a business in a transition stage, beyond emergency borrowing but not yet ideal for a bank, may be better served by a marketplace approach such as Business Loan Warrior, where the goal is matching the loan to the stage of the business instead of forcing every need into one lender's box.

My recommendation is straightforward. Use OnDeck when speed protects revenue or helps you capture a near-term return. Skip it when you need patient capital, the cheapest available rate, or a lender to solve deeper operating weakness.

OnDeck's Loan Products Explained

A lot of owners overcomplicate this choice. You usually need one of two tools. A lump sum for a specific job, or a reusable credit line for short-term gaps.

That is OnDeck's product lineup in plain English.

Term loan

An OnDeck term loan fits best when the plan is clear before the money hits your account. You know the amount, the use, and how the project pays you back.

Use it for a vehicle replacement, a planned equipment purchase, a store refresh, or a one-time inventory buy tied to demand you can already see. It is a closed-end tool. You receive the money upfront and repay it on a fixed schedule.

OnDeck offers term loans from **$5,000 to $400,000, with repayment periods of two years or less. This brief repayment period is a key characteristic. Fast capital can solve an immediate problem, but short-term repayment raises the monthly burden. If you use a short loan for something that will not produce returns for years, you are forcing this year's cash flow to carry a long-term investment.

That is bad matching. It is like paying for a delivery van on the same timeline you would use for a holiday inventory push.

My advice is simple. Use the term loan when the payoff is visible and near-term. If the return is slow, the structure gets expensive fast, even if the rate looks tolerable at first glance.

Line of credit

An OnDeck line of credit works better when the exact need is hard to pin down.

This is the tool for uneven timing. Inventory ahead of a busy season. Payroll while you wait on receivables. Repairs that cannot wait. You draw what you need, when you need it, up to your limit.

OnDeck's line of credit ranges from $6,000 to $200,000. Draws are typically repaid over 12, 18, or 24 months. That flexibility helps if your cash flow is healthy but lumpy.

It also creates one of the most common borrowing mistakes I see. Owners treat the line like a permanent patch for ordinary operating strain. A credit line should work like a shock absorber. It should absorb bumps, then reset. If you are drawing repeatedly just to survive normal weeks, the problem is not timing anymore. The problem is that the business is not generating enough cushion.

That distinction matters.

A line of credit is the better OnDeck product if your revenue is solid and the friction is temporary. If your business has moved past emergency borrowing but you still want to compare structures from multiple lenders, a marketplace can be the smarter middle ground. Reviewing realistic timelines for small business funding from application to cash in your account can help you decide whether speed alone justifies OnDeck's cost, or whether a broader search is still practical.

OnDeck Term Loan vs. Line of Credit at a Glance

| Feature | Term Loan | Line of Credit |

|---|---|---|

| Best use | One-time purchase or defined project | Ongoing working capital and uneven cash flow |

| Funding structure | Lump sum | Draw as needed |

| Amount range | $5,000 to $400,000 | $6,000 to $200,000 |

| Repayment profile | Two years or less | Draws typically repaid over 12, 18, or 24 months |

| Good fit example | Equipment, renovation, large inventory buy | Seasonal expenses, payroll timing, repair cushion |

| Core risk | Short repayment window on a long-lived asset | Repeated use for routine expenses |

Two judgment calls matter more than the product names:

- Choose the term loan when the need is defined and the return has a deadline. It creates discipline and a clean payoff path.

- Choose the line only when the need is variable and you can clear draws quickly. Flexibility without repayment discipline turns into expensive drift.

OnDeck is a scaled online lender with a long track record in small-business funding. That matters. Experience usually means a smoother process and clearer credit boxes. But scale does not make every product a fit. The right question is not whether OnDeck can fund you. The right question is whether this specific loan matches your stage of growth, your cash cycle, and the speed you need.

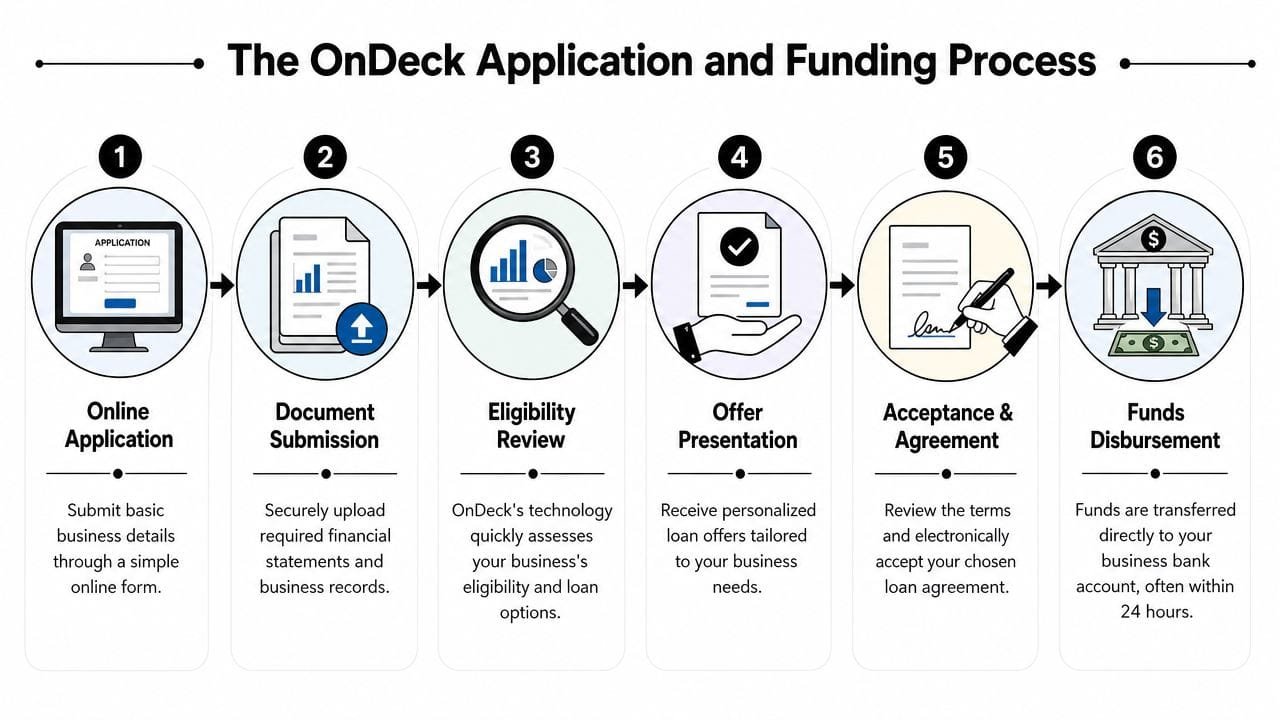

The OnDeck Application and Funding Process

The application experience is one reason owners look at OnDeck in the first place. It's built to move online and move quickly.

What the process looks like

At a practical level, most borrowers should expect a sequence like this:

- Start with the online application. You enter basic business details and the kind of financing you want.

- Provide your operating information. That typically includes business bank activity and supporting records.

- Go through underwriting review. The lender evaluates revenue patterns, time in business, credit, and account behavior.

- Review available offers. If approved, you compare product structure and terms.

- Accept and sign. Once documents are complete, funding can move to your business bank account.

OnDeck's published requirements include 3 months of business bank statements, which tells you exactly what kind of operating visibility it wants during review, according to OnDeck's compare lenders page.

For a broader sense of how online small-business funding timelines usually play out, this breakdown of realistic timelines from application to cash in your account is worth reading.

Here's a short video overview that gives useful context around the funding journey:

What slows things down

Fast funding is real. So are delays.

The biggest slowdowns usually come from incomplete records, inconsistencies between the application and bank activity, late-day submissions, and any situation that requires extra follow-up. Holidays and bank processing windows can slow the final transfer even when approval itself moves quickly.

Keep your side clean:

- Match your paperwork: revenue, legal business name, and account details should line up.

- Use current records: stale statements create avoidable back-and-forth.

- Apply before a crisis hour: urgency helps nobody if your documents are messy.

If your situation is urgent, the best thing you can do isn't to rush. It's to be organized.

Key Advantages and Drawbacks of OnDeck

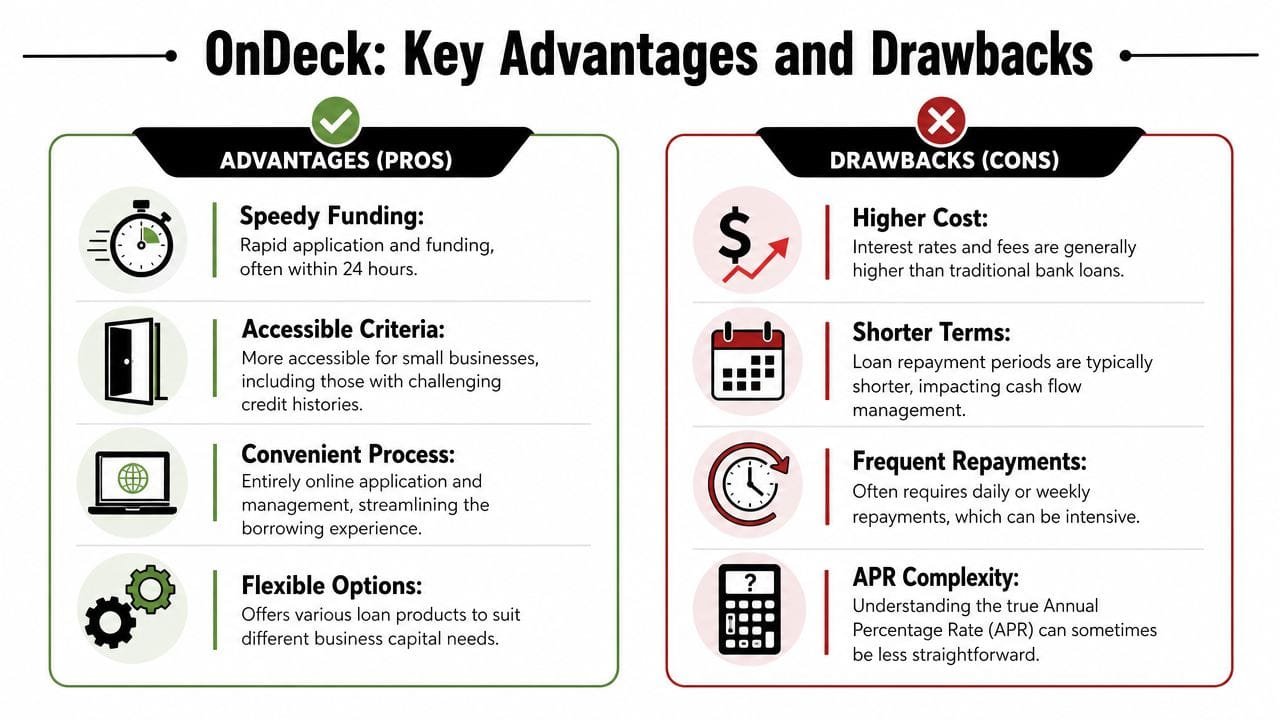

A delayed payroll run, a broken piece of equipment, or a supplier discount that expires this week changes the math. In those moments, OnDeck can be useful because it sells speed. The trade-off is simple. Fast money usually costs more, and you need to know whether the problem in front of you justifies that price.

Where OnDeck earns its place

OnDeck works best for established small businesses that need working capital quickly and have a clear use for it. If the funds help you buy inventory with known margins, cover a short timing gap from receivables, or fix an operational problem that is actively costing revenue, speed has real value.

That is the core advantage.

Another plus is that OnDeck is easier to fit into than a traditional bank for many owners. A business can be healthy in real life and still look imperfect through a bank's lens. OnDeck is often a practical middle ground for owners with decent revenue, active bank activity, and a legitimate capital need, but without the patience or profile for a slower bank process.

The product lineup also stays simple. You are usually choosing between a term loan for a defined need or a line of credit for repeated short-term working capital use. That makes decision-making easier for busy owners who do not want to sort through a dozen financing structures.

Here is where OnDeck tends to make sense:

- Urgent, revenue-linked uses: inventory, repairs, payroll gaps tied to incoming receivables, or time-sensitive opportunities

- Established businesses that need speed: not startups, not turnaround stories, but operating companies that need money on a business timeline

- Short-term needs with a clear payoff plan: you know how the advance gets paid back before you take it

Where owners get burned

Cost is the biggest drawback. That is not a minor detail. It is the whole decision.

OnDeck can be a smart tool for short-term problems, but it becomes expensive fast if you use it like a long-term capital solution. A line of credit or short-term loan works like paying extra for overnight shipping. If the package is urgent, the premium is justified. If it is routine, you are just overpaying because planning broke down.

Repayment pressure is the second problem. Even if the total borrowing amount looks manageable, frequent or compressed payments can squeeze cash flow harder than owners expect. That is how a loan that looked helpful on approval day starts creating stress a few weeks later.

Watch for these warning signs:

- You are borrowing to cover ordinary monthly overhead: that points to a cash flow problem, not a one-time funding need

- You cannot name the repayment source: every short-term loan needs a defined exit, such as receivables, seasonal sales, or a specific margin event

- You expect to redraw just to stay current: that is dependency, not strategy

My advice is blunt. Use OnDeck for speed, not for comfort. If the capital solves a clear short-term problem and protects or creates more value than it costs, it can be the right move. If your real need is cheaper, longer-term financing or help comparing several lender types, a broader review of the trade-offs between fintech lenders and banks for faster approvals is a better next step.

OnDeck is strongest in a narrow lane. Immediate need, clear use, clear payoff. Outside that lane, it gets expensive quickly.

OnDeck vs. Alternatives (Banks and Business Loan Warrior)

The cleanest way to judge OnDeck is to put it beside the two real alternatives most owners weigh: a traditional bank and a lending marketplace.

How the three options differ

A traditional bank usually makes the most sense when cost matters more than speed, your financials are strong, and you have time. Banks are built for borrowers who can tolerate a slower process in exchange for a better long-term capital structure.

OnDeck makes the most sense when the clock is working against you. You need a practical amount of capital, you meet the lender's baseline profile, and the business purpose is immediate enough to justify faster money.

A marketplace approach can be useful when you don't want to guess which lender box you fit. Business Loan Warrior works through a single application to help owners compare funding options across different product types and lender profiles. That can make sense if your situation isn't a textbook fit for either a bank or a single direct online lender. For more context on the trade-offs, this comparison of fintech lenders vs. banks for faster approvals is useful.

Lender Comparison OnDeck vs. Banks vs. Business Loan Warrior

| Feature | Traditional Bank | OnDeck | Business Loan Warrior |

|---|---|---|---|

| Best fit | Strong borrower with time to wait | Established small business needing speed | Owner who wants to compare lender fits through one application |

| Speed | Usually slower | Faster online process | Faster than a bank in many cases, with multiple lender pathways |

| Cost profile | Usually lower if you qualify | Usually higher because speed and access are the value | Varies by lender and product |

| Product approach | More formal underwriting, often broader long-term structures | Two core products, term loan and line of credit | Multiple funding categories depending on need |

| Good use case | Expansion, longer-term investments, lower-cost borrowing | Urgent working capital, repairs, timing gaps, short-term opportunities | Comparing options when fit is unclear or specialized funding is needed |

| Main trade-off | Better pricing, more friction | More convenience, more expensive capital | More choice, but still requires good decision-making |

Here's my blunt recommendation by growth stage:

- Early but operating steadily: OnDeck can work if you need working capital fast and already have a clear repayment path.

- Mid-stage and financially organized: compare broader options before locking into a single fast lender.

- Larger, more established company: don't default to OnDeck for long-duration needs. Your business may be better served by a bank structure or a wider lender search.

That last point matters for firms doing meaningful revenue. If you're running a larger small business, the downside of convenience borrowing grows. A product built for quick access can still be the wrong fit if your funding need is strategic, layered, or tied to a longer return cycle.

The Final Verdict When to Choose Each Option

A financing decision gets simple once you stop asking, “Can I qualify?” and start asking, “What job does this money need to do?”

Choose OnDeck for short-term moves with a clear payoff. Use it when fast cash keeps a good business from stalling, such as covering payroll during a receivables delay, replacing equipment that just failed, or buying inventory tied to an order you already expect to collect on. OnDeck works best when speed matters more than getting the lowest possible borrowing cost.

Choose a traditional bank when the return on the project will take time. If you are opening a second location, funding a major equipment purchase, or financing a longer expansion plan, lower-cost capital usually matters more than fast approval. A bank is slower, but for long-duration needs, that slower money is often the smarter money.

Choose a marketplace approach when your business does not fit neatly into one lender's product menu. That matters most in the middle stage of growth, when the company is past the startup scramble but not yet so established that a bank is the obvious answer. One lender offers one box. A marketplace lets you compare structures before you commit.

Here is the rule I want you to keep: do not use fast, expensive capital for a problem that will pay back slowly. That is like putting a short sprint on your calendar to solve a long hike. The mismatch is what hurts, not just the rate.

The right question is simple: What specific cash event will repay this financing? If you can answer that in one sentence, your choice gets clearer fast.

If you want to compare loan structures before committing to one lender, Business Loan Warrior lets you start with one application and explore options based on your business stage, urgency, and funding purpose.