You're probably here because something didn't add up.

Your business has revenue. Customers pay. You manage payroll, inventory, vendors, and taxes. Then you apply for financing and hear some version of this: the file is thin, the credit profile is weak, or the application needs more support. That's frustrating because the business may be healthy while the credit file still looks underdeveloped.

Tradelines are critical. They are the account records that lenders and credit bureaus use to judge whether you handle credit well. Most articles stop at the definition. That's not enough if you're trying to get approved for a loan, a line of credit, or equipment financing. The primary issue is whether the tradelines in your file help an underwriter trust the application, or make the whole thing look staged.

Table of Contents

- Why Your Business Credit File Matters More Than You Think

- What Exactly Are Tradelines

- The Different Types of Tradelines You Will Encounter

- The Promise and Peril of Buying Tradelines

- How Lenders and Scoring Models Actually View Tradelines

- Build Strong Tradelines the Right Way for Business Funding

- Frequently Asked Questions About Tradelines

Why Your Business Credit File Matters More Than You Think

A strong business doesn't automatically produce a strong credit file. Lenders don't underwrite your effort. They underwrite records, payment behavior, and consistency.

I've seen owners with real traction get stuck because their file shows very little usable credit history. Maybe they've funded growth from cash flow. Maybe they use debit cards for everything. Maybe the business has supplier relationships, but none of those suppliers report to commercial bureaus. Operationally, the company is fine. On paper, the credit file still looks unproven.

Why thin files create problems

A lender wants evidence that you can manage borrowed money, not just earn money. Those are related, but they're not the same.

A thin file creates several practical problems:

- Limited repayment evidence means the lender has fewer records showing how you handle obligations over time.

- Weak trend visibility makes it harder to see whether balances stay controlled and payments stay current.

- More manual scrutiny usually follows when the automated view of the file doesn't tell a clear story.

Practical rule: Revenue can support a loan. Tradelines help prove you can manage one.

For small business owners, this matters even more because many funding decisions blend business data with owner data. If the business file is young, underwriters often look harder at the owner's personal credit behavior, especially for newer companies, closely held firms, and applications with a personal guarantee.

What a good file actually does

A credible credit file reduces uncertainty. That's the whole game.

When an underwriter sees well-managed accounts, the file starts answering the key questions on its own. Do you pay on time? Do you keep balances under control? Have you managed more than one type of account? Has that behavior stayed steady long enough to trust it?

If the answer is yes, the conversation gets easier. If the file looks manufactured, sparse, or erratic, approval gets harder even when the business itself is solid.

What Exactly Are Tradelines

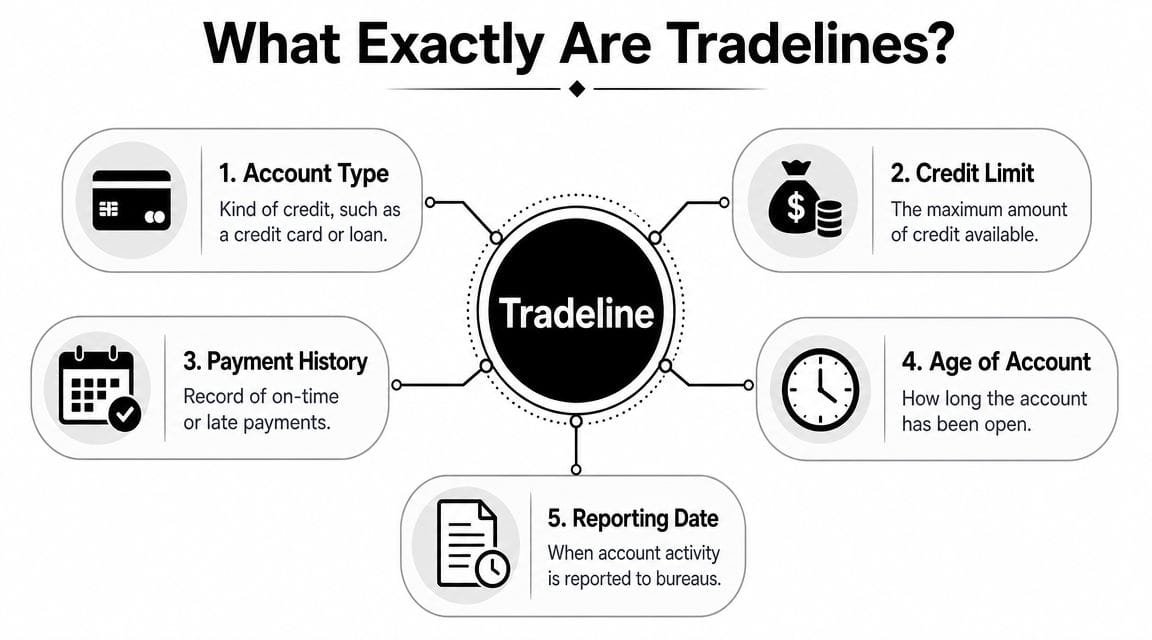

A tradeline is the credit-bureau record for a specific account. In consumer credit, major bureaus treat each credit card, mortgage, auto loan, student loan, or personal loan as its own entry, and those entries can show the lender's name, account type, opening date, balance, payment history, and status, as explained in Citi's overview of what tradelines are and how long they can remain on a report. That same reference notes that open tradelines remain indefinitely, while closed tradelines in good standing can stay for 10 years and closed tradelines in poor standing generally remain for 7 years.

Think of tradelines as account report cards

The easiest way to think about tradelines is this. Each account gets its own report card.

That report card tells the lender what kind of account it is, when it was opened, whether it's open or closed, how it has been paid, and whether anything has gone wrong. One account can look excellent while another looks messy. Underwriters read both.

Here's the practical breakdown:

| Tradeline field | What it tells a lender |

|---|---|

| Account type | Whether you're handling a card, loan, mortgage, vendor account, or something else |

| Open date | How long the account has been part of your history |

| Balance or amount owed | Whether debt looks controlled or stretched |

| Payment history | Whether you pay as agreed |

| Current status | Whether the account is current, late, charged off, or closed |

The file isn't just administrative. It becomes a shortcut for trust. A lender can't sit in your office and watch how you manage cash. Tradelines are one of the records they use instead.

Personal and business tradelines are not the same thing

Many owners often get mixed up here.

Your personal tradelines are tied to your consumer credit. Think personal credit cards, mortgages, auto loans, and personal loans. Your business tradelines are tied to the business credit file and come from suppliers, lenders, or card issuers that report commercial account activity.

In business credit, Experian describes a tradeline as the monthly reported account record a supplier, lender, or card issuer sends to commercial bureaus, and that record typically includes balance, payment history, and status in Experian's business tradeline glossary.

That distinction matters because a lender may review both files, but not give them equal weight. A well-run company with no reporting business accounts may still rely heavily on the owner's personal profile. A mature business with established commercial tradelines can stand on its own more convincingly.

Good underwriting doesn't ask only, “What's the score?” It asks, “Whose account history is this, and does it fit the borrower we're looking at?”

The Different Types of Tradelines You Will Encounter

Not all tradelines help the same way. Some are strong evidence of repayment behavior. Others are little more than cosmetic improvements.

Primary tradelines carry the most weight

A primary tradeline is an account you opened in your own name or in the business's name. This is the gold standard because responsibility is clear. If it's on the report, it's your obligation.

Examples include:

- Personal primary accounts such as your own business-purpose credit card, auto loan, or mortgage.

- Business primary accounts such as a business credit card, term loan, equipment loan, or line of credit opened by the company.

- Supplier accounts if the business directly established the payment relationship and the supplier reports it.

These usually carry the most credibility in underwriting because there's no question about who made the payment decisions.

Authorized user tradelines can help optics but raise questions

An authorized user tradeline appears when someone adds you to an existing account. You didn't originate the account. You may not be legally responsible for paying it. You're benefiting from the history attached to it.

That's why lenders treat these with caution.

In some contexts, being added by a spouse or family member to a shared account can make sense. But when a file suddenly gains a polished authorized user account from a third party, underwriters may read it very differently. The issue isn't just whether the score moved. The issue is whether the added account reflects your actual repayment behavior.

A long, clean primary account usually means more than a recently added authorized user account, even if the score impact looks attractive at first glance.

Business vendor tradelines matter when they actually report

Vendor tradelines can be useful, but only if they report consistently.

These usually come from suppliers extending terms on inventory, materials, office products, shipping, or other operating needs. If the account is paid as agreed and the vendor reports to commercial bureaus, the tradeline can help build a real business credit file.

What owners often miss is simple: an account that doesn't report doesn't build much visible history.

Here's how I'd rank tradelines for lending credibility:

- Established primary business tradelines with steady, on-time history.

- Established primary personal tradelines when the owner is part of the credit decision.

- Reporting vendor tradelines tied to normal business operations.

- Authorized user tradelines that may affect score optics but often carry less underwriting value.

- Purchased authorized user tradelines that may trigger skepticism.

That order isn't about theory. It reflects a basic lending question. Which accounts show the borrower took responsibility and managed credit over time?

The Promise and Peril of Buying Tradelines

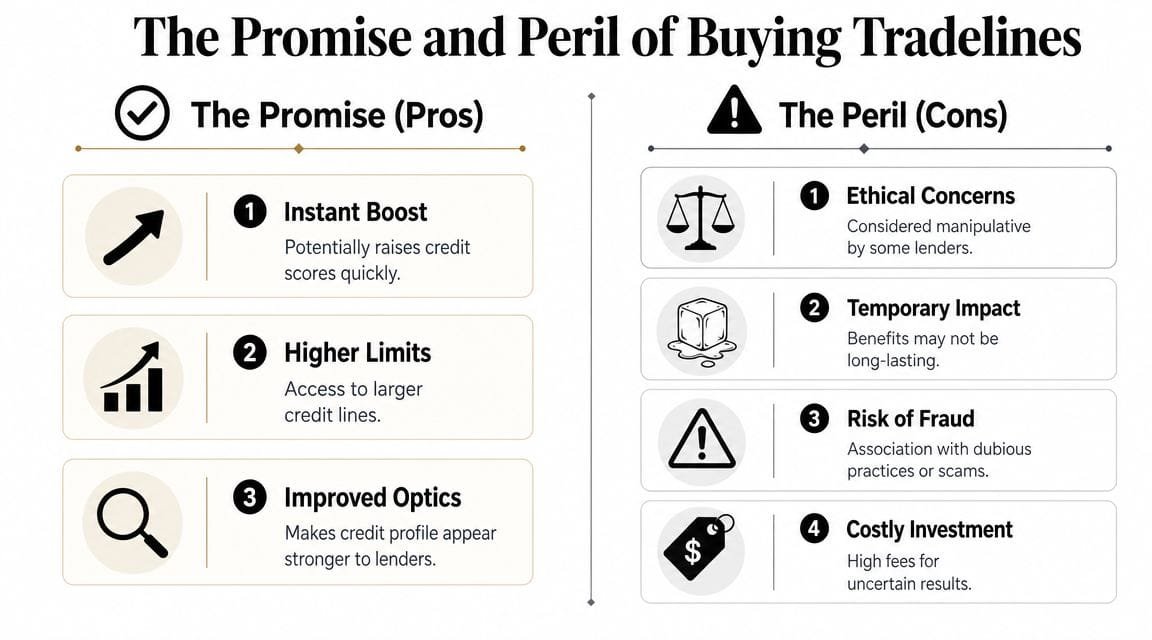

Buying tradelines usually means paying to be added as an authorized user on someone else's seasoned credit card account. The sales pitch is straightforward. Their older account, higher limit, or cleaner history shows up on your report and may improve how your file looks.

Why people buy them

I understand the appeal. If you need financing soon, waiting for organic credit history to build can feel too slow. A purchased tradeline offers the promise of a shortcut.

The usual logic goes like this:

- You need speed because a loan, lease, or vendor approval is coming up.

- Your file is thin so even one polished account may change how a scoring model reads it.

- The marketplace presents it as harmless because authorized user arrangements can be lawful in some settings.

That's the promise. Fast optics.

A more durable approach is usually to strengthen the application package and use practical funding options for businesses dealing with weak credit profiles instead of trying to decorate the file.

Later in the process, many owners discover the gap between score improvement and approval improvement.

Why lenders often discount them

Independent guidance is cautious. Nav says there is “no guarantee” purchased tradelines will improve scores and that building your own credit is safer in its discussion of tradelines for sale and the limits of the tactic.

That caution is well placed because buying tradelines creates several real risks:

- Temporary value. If the account is removed, the borrowed benefit can disappear.

- Weak ownership signal. An underwriter may see the account but not view it as proof that you manage debt yourself.

- Application risk. If the overall file looks engineered, the lender may ask harder questions or reduce confidence in the borrower.

- Counterparty risk. You're relying on a third party to keep the account in good shape while your name is attached to it.

The score can move while the loan decision stays the same. That's the part most marketplaces leave out.

There's also a gray-area problem. A setup may be technically permissible as an authorized user arrangement, but if the purpose is to create a stronger appearance of creditworthiness than the borrower possesses, some lenders will treat that as a credibility issue. Not always fraud. Often just a red flag.

In practice, purchased tradelines are usually a weak answer to a stronger question: do you have your own history of handling credit responsibly? If the answer is thin or no, a rented history rarely fixes the underwriting problem.

How Lenders and Scoring Models Actually View Tradelines

A score and an approval are related, but they are not the same event. That distinction matters more than most borrowers realize.

Scores and underwriting are not the same thing

Scoring models compress a lot of account data into one number. Underwriters don't stop there. They review what produced the number.

A credit score generally requires active account data within the prior six months, so a borrower with few or no recently active tradelines may not produce a strong signal even if older accounts exist, as explained in this review of how active tradelines affect score generation. The same source notes that impact comes from the combination of account age, payment history, and current status.

That tells you something important. A dormant file, or a file padded with the wrong kind of account, may still leave lenders unconvinced.

If you want context on where your profile stands before applying, this guide to business loan credit score expectations is a useful reality check.

What an underwriter notices fast

Manual review changes everything. A human can spot patterns a score alone won't explain.

These are the kinds of things underwriters notice quickly:

| Underwriter observation | Typical interpretation |

|---|---|

| A thin file with one or two sudden polished accounts | Possible score engineering |

| Few recently active primary accounts | Limited current repayment evidence |

| Strong score but weak business file | Personal profile may be carrying the application |

| Several new accounts opened close together | Borrower may be scrambling for capacity |

Underwriters are trained to ask whether the tradelines fit the rest of the borrower story. Does the age of the accounts make sense? Does the business use credit in a normal way for its industry? Do the balances and statuses look lived in, or newly staged?

Underwriting lens: Believable history beats impressive optics.

That’s why gaming the score is often the wrong objective. Serious lenders aren’t just buying the score. They’re buying the repayment story behind it.

Build Strong Tradelines the Right Way for Business Funding

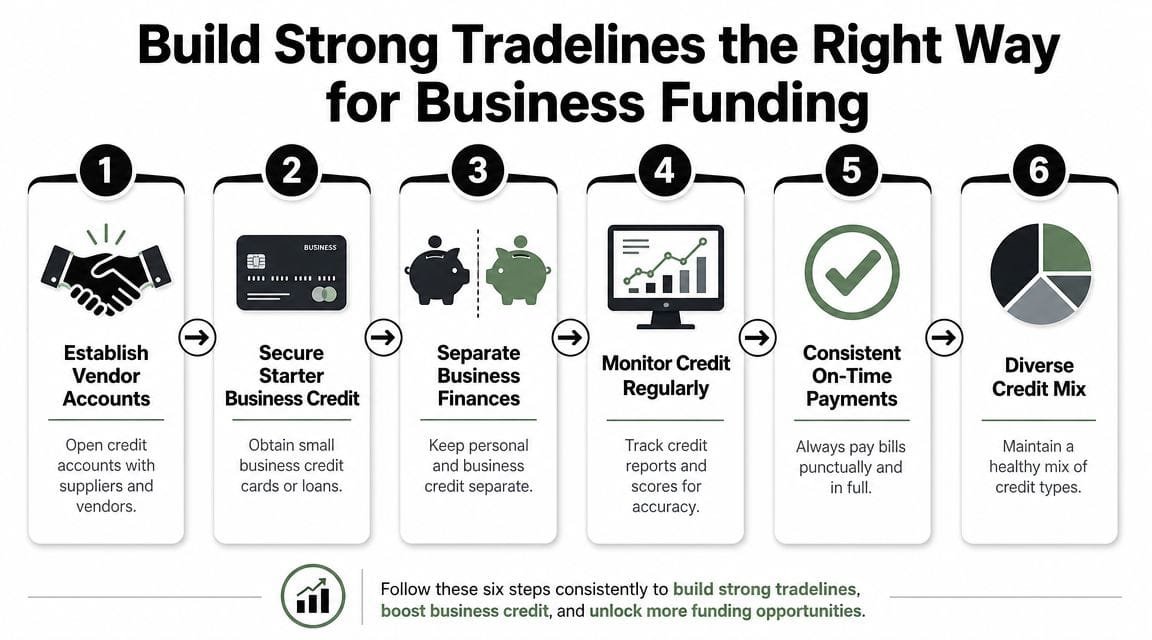

The right strategy is less exciting than buying a shortcut, but it works better in real lending. Build tradelines that look normal because they are normal.

Start with accounts that create believable history

Good business credit building starts with accounts your company can use.

A practical sequence looks like this:

- Open reporting vendor accounts with suppliers you already buy from or can use consistently.

- Add a starter business card or small credit facility that reports and is easy to manage.

- Keep personal and business borrowing separate where possible so the business file can stand on its own over time.

- Use accounts lightly and pay predictably so the file shows control rather than stress.

The goal isn’t to stack random accounts. It’s to create a clean record of routine, on-time repayment.

If you want a more structured playbook, this walkthrough of a business credit plan lending partners actually trust is the kind of approach lenders respect because it focuses on reporting, separation, and consistency.

Focus on reporting cadence and account management

In business credit, reporting cadence matters. Experian’s business guidance explains that tradelines are monthly reported account records, which means improvement depends on whether creditors send usable account data to commercial bureaus. A non-reporting account can be operationally useful and still do almost nothing for your visible file.

A few habits matter more than anything flashy:

- Choose accounts that report. Before opening anything, confirm whether the creditor reports to commercial bureaus.

- Pay on time every cycle. One late pattern can outweigh a lot of cosmetic cleanup.

- Review reports for accuracy. Wrong statuses, balances, or business identity details can weaken an otherwise solid file.

- Build for durability. Tradelines can stay on reports a long time, so the ones you build now can shape future borrowing.

Long-term strategy matters because credit reporting rules can shift. Experian notes in its consumer discussion of how long tradelines remain and why long-lasting accounts matter that open accounts can remain indefinitely, while closed accounts in good standing can remain for up to 10 years. That same discussion also references the now-vacated 2025 medical debt rule and why the reporting environment can change.

The takeaway is simple. Build tradelines you’d still be comfortable defending in front of a lender years from now. That’s what resilient credit looks like.

Frequently Asked Questions About Tradelines

Is buying a tradeline illegal or just a bad idea?

Usually the better answer is that it’s a bad lending strategy. Some authorized user arrangements are lawful. The problem is that purchased tradelines can create credibility issues if they’re being used to make an applicant appear stronger than the underlying file really is. Lenders may ignore them or question the application.

How long does a new tradeline take to matter?

It depends on when the creditor reports and whether the account becomes active enough to create a useful signal. In business credit, monthly reporting cadence matters. In consumer scoring, recently active account data matters too. A brand-new account that doesn’t report yet won’t do much.

Can you remove a negative tradeline?

You can dispute inaccurate information. If the tradeline is accurate, removal is much harder. Some negative items also remain visible for years, so the practical move is often to clean up current behavior and stop adding fresh damage.

How many tradelines do you need for a business loan?

There isn’t one magic number. Lenders care more about quality than count. A few believable, well-managed primary tradelines usually help more than a pile of weak or recently added accounts.

The strongest file is one that answers basic underwriting questions without drama. Who owes the debt? Have they paid on time? Has that behavior stayed consistent? If your tradelines make those answers obvious, you’re in much better shape.

If you want funding guidance grounded in real underwriting, Business Loan Warrior helps small business owners explore financing options without turning the process into a guessing game. You can check potential offers, understand where your credit profile may help or hurt, and move toward funding with a clearer picture of what lenders are looking for.