Your business can be profitable on paper and still feel broke on Friday morning.

That usually shows up in familiar ways. Payroll is due before two large customers pay. Inventory arrives a week before your seasonal rush. A supplier wants payment now, but your biggest client always takes its full terms. You're selling, invoicing, and even growing, yet your bank balance keeps forcing hard choices.

That's why cash flow isn't just an accounting concern. It's the operating heartbeat of the business. If cash is tight, every decision gets smaller. You delay hires, postpone equipment purchases, pass on marketing, and spend too much time solving short-term gaps instead of building a stronger company.

A better approach starts with a simple idea. Don't treat cash flow as a monthly review after the damage is done. Build a system that gives you control every week. The businesses that handle uncertainty best usually do three things well: they tighten day-to-day operations, they forecast cash before problems hit, and they line up financing while they still have options.

Table of Contents

- Beyond Surviving the Month to Month

- Quick Operational Wins for Immediate Impact

- Mastering Your Inflows and Outflows

- Building Your Cash Flow Forecasting System

- Using Smart Financing as a Strategic Tool

- Making Cash Flow Your Competitive Advantage

Beyond Surviving the Month to Month

Most owners first think about cash flow when something feels off. Sales look decent. The P&L doesn't look terrible. Then a routine expense lands at the wrong time and suddenly the business feels fragile. That's the moment many people realize profit and cash are not the same thing.

A healthy company doesn't just survive the month. It creates enough control over timing to make good decisions before pressure builds. That means you know what's likely to clear this week, what's going out next week, and where the pressure points sit if one customer pays late or demand softens.

Cash stress usually isn't caused by one dramatic mistake. It comes from timing gaps that stack up across receivables, inventory, payroll, and purchasing.

Owners often get told the same two lines of advice. Invoice faster. Cut costs. Both matter, but neither is enough on its own. If spending approvals are loose, inventory sits too long, and nobody updates a weekly cash view, you'll keep revisiting the same problem.

The stronger play is to think like an operator, not just a bookkeeper. Tighten the way cash moves through the business. Put visibility around the next several weeks, not just last month. Use financing as support for the system, not a substitute for it.

That shift changes your posture. Instead of reacting to shortages, you start shaping your cash position on purpose.

Quick Operational Wins for Immediate Impact

When cash feels tight, start with operational changes that free up money without waiting for a big strategic overhaul.

Start with the cash conversion cycle

The cleanest framework is the cash conversion cycle, or CCC. In plain English, it measures how long cash stays tied up in the business before it returns. Practical guidance from G-Squared CFO on managing the cash conversion cycle recommends tackling three separate areas: receivables, payables, and inventory. The same guidance points to immediate invoice issuance, automated reminders, shorter due dates, and active DSO monitoring, while warning that poor forecasting and weak expense discipline often undermine results.

That matters because owners often attack the wrong problem. They focus only on sales, when the faster fix is often hidden in billing delays, excess stock, or vendor terms that were never renegotiated.

If you want a useful operating companion to this work, review a practical funding-focused operations checklist for small business growth. It helps connect workflow cleanup with cash impact.

A short list of fixes you can make this week

Don't start with a broad “reduce overhead” meeting. Start with a short cash review and force a decision in each category.

Issue every completed invoice immediately. If work is done, billing shouldn't wait for the end of the week or month. Administrative lag is one of the easiest cash leaks to remove.

Review slow-moving inventory by SKU or category. Old stock ties up cash and hides in plain sight. Discount it, bundle it, return it where possible, or stop reordering until demand proves itself.

Renegotiate non-critical vendor terms. Longstanding suppliers will often discuss due dates, payment timing, or order cadence if you ask early and communicate clearly.

Pause spending that doesn't affect delivery. Keep buying what protects revenue, customer experience, and core operations. Delay purchases that are convenient but not urgent.

Check pricing on low-margin work. Some customers are busy but not healthy. If a product line or account consumes cash without enough return, price changes or tighter terms may be overdue.

Practical rule: If a cost doesn't help you collect faster, sell faster, or deliver reliably, it deserves scrutiny.

A few more operational habits tend to work better than dramatic cuts:

| Area | What to check now | What usually helps |

|---|---|---|

| Billing | Delays between completion and invoice | Same-day invoicing, standardized approval |

| Inventory | Aging items and reorder habits | Demand-based replenishment |

| Purchasing | Habit spending and duplicate tools | Approval thresholds by spend type |

| Vendors | Old terms no one has revisited | Renegotiated timing, consolidated ordering |

Many owners ask how to improve cash flow quickly. The answer is usually less glamorous than they hope. Clean up timing. Stop funding stale inventory. Make sure spending has an owner. Those moves often release cash faster than another push for revenue.

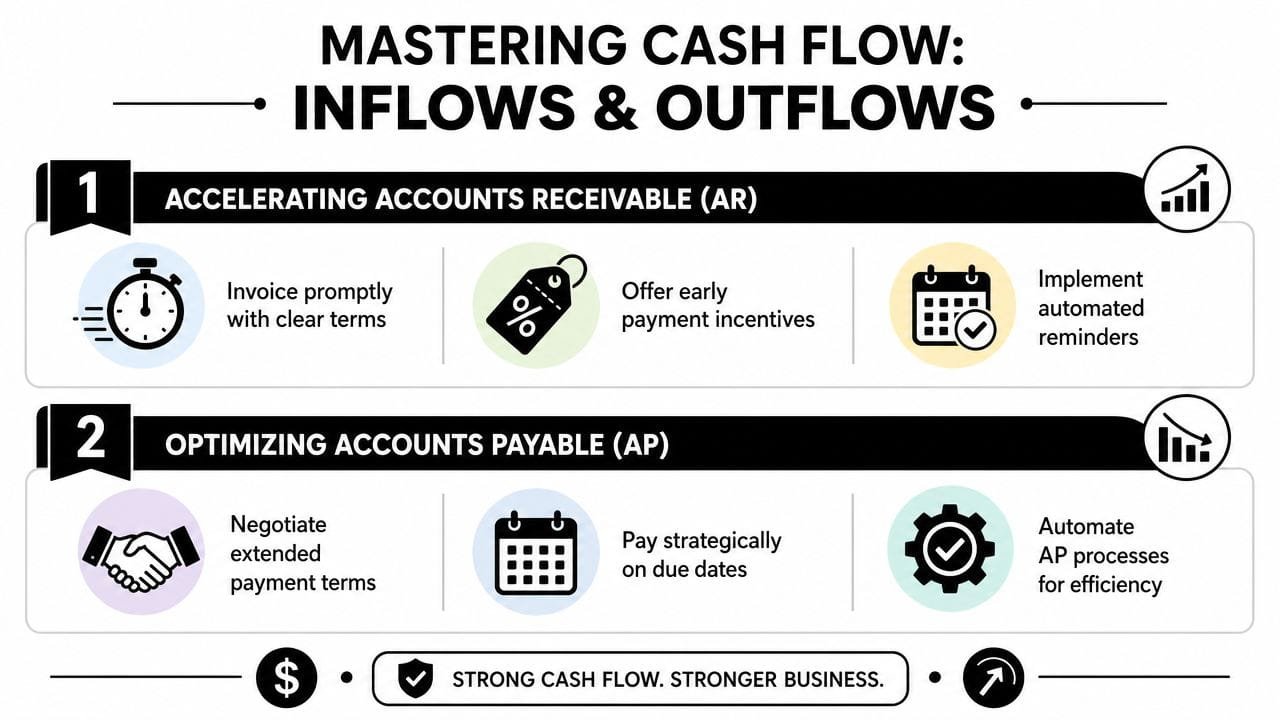

Mastering Your Inflows and Outflows

Cash flow improves when you treat collections and payments as operating disciplines, not back-office chores. One side is offense. Get cash in sooner. The other is defense. Control when cash leaves without weakening supplier trust.

The visual below captures the basic structure.

Get cash in faster

A foundational way to improve cash flow is to shorten the gap between earning revenue and collecting cash. Bank of America's cash flow guidance for small businesses recommends invoicing customers the same day a sale or service is completed, setting payment terms up front, and using discounts for quick payment. It also notes that faster payments speed up the business's cash conversion cycle. The same guidance highlights practical collection methods such as electronic invoicing, prompt follow-up on overdue accounts, and penalties for late payments.

Those recommendations work because they remove ambiguity. Businesses don't get paid faster by hoping. They get paid faster by making the payment path easy and the expectations obvious.

Use a simple structure:

Set terms before work starts. Don't leave payment terms to the invoice footer after the job is done. Put them in the proposal, contract, or onboarding paperwork.

Send invoices the same day. If fulfillment is complete, trigger billing immediately. Waiting creates preventable delay and signals that timing doesn't matter.

Automate reminders. A polite reminder before due date and a firm follow-up after due date removes emotion from collections.

Here's a useful explainer if you want a quick break from reading:

Then tighten the process further.

- Use electronic invoicing. Make it easy for the customer to receive, approve, and pay without extra steps.

- Create an overdue sequence. Decide who follows up, when they follow up, and when the issue gets escalated.

- Offer early payment discounts selectively. This works best when the margin trade-off is worth the acceleration in cash.

Customers usually don't pay faster because you need the money. They pay faster when your process makes delay inconvenient.

Control cash going out without damaging relationships

Managing payables well doesn't mean paying late. It means paying intentionally.

Too many businesses burn cash by paying invoices the moment they hit the inbox, even when the supplier granted reasonable terms. That habit shrinks your cushion for no real gain. Pay on agreed due dates unless an early-payment discount clearly benefits you.

Use these ideas to keep outflows under control:

- Negotiate terms before you need relief. Suppliers respond better when the request comes from planning, not panic.

- Align payment runs with expected inflows. Time vendor payments around known customer receipts, payroll, and recurring obligations.

- Separate strategic vendors from replaceable ones. Protect the relationships that protect your revenue. Push harder on terms where the business risk is low.

- Use cards or vendor financing carefully. These tools can smooth timing, but only if you track payoff dates and avoid turning short-term flexibility into expensive rollover debt.

A small internal rule can help a lot: no one changes payment timing, purchasing cadence, or discount terms without checking the current cash view. That one habit forces operations and finance to work from the same reality.

Building Your Cash Flow Forecasting System

Most owners don't need a complex model. They need a forecast they'll use.

Build a weekly view first

The most practical operating tool is a 13-week cash flow forecast. It's long enough to spot pressure early and short enough to stay grounded in reality. You're not trying to predict the year perfectly. You're trying to avoid surprises and make better decisions this week.

Recent operator-focused guidance summarized by Ramp's article on improving cash flow highlights a gap in mainstream advice. Instead of repeating generic tips, it points to working-capital mechanics like weekly cash forecasting, role-based spending limits, inventory aging, and using a credit line only when cash is strong. It specifically recommends mapping expected income by week and setting spending limits by role.

That's the right frame. Weekly beats monthly when cash is tight because timing matters more than averages.

A useful 13-week forecast includes:

| Weekly input | What to capture |

|---|---|

| Opening cash | What's actually available at the start of the week |

| Expected customer receipts | What should come in, based on real invoice dates and likely payment timing |

| Payroll | Gross timing and amount due |

| Rent and fixed overhead | Scheduled obligations that won't move |

| Supplier payments | What must be paid, what can be timed |

| Taxes, debt service, and other commitments | Anything that creates a known cash drain |

| Closing cash | Opening cash plus inflows minus outflows |

Add spending discipline to the forecast

Forecasting alone won't fix sloppy execution. If the business has no spending guardrails, the forecast turns into a historical document instead of a management tool.

Set approval limits by role. Give department heads room to operate, but define what needs review before money leaves the account. This is especially important for software renewals, inventory buys, rush freight, marketing tests, and discretionary hiring.

A second discipline is account structure. Many operators prefer not to let excess cash sit in the main operating account. Keeping operating cash tight enough to force awareness can reduce impulse spending and make weekly reviews more honest.

A forecast works when it changes behavior. If nobody delays a purchase, speeds up a collection call, or revises an order plan because of it, it's just a spreadsheet.

If you want to connect forecasting to borrowing decisions, this guide on building a cash flow forecast that supports your loan strategy is a strong next read.

Watch the indicators that change decisions

You don't need a dashboard full of vanity metrics. Track a handful that show whether working capital is tightening or loosening.

Use a short operating review each week:

- DSO trend. Are customers taking longer to pay?

- DPO trend. Are you using supplier terms intentionally or just drifting into late payments?

- Inventory aging. Which items are absorbing cash without moving?

- Forecast variance. What came in later than expected, and what went out sooner than planned?

The point isn't perfect precision. The point is pattern recognition. If three large payments consistently arrive later than forecast, adjust the assumption. If inventory grows while demand softens, purchasing needs to change before the bank balance forces the issue.

That's how to improve cash flow in a durable way. You stop managing from last month's statements and start managing from next week's likely reality.

Using Smart Financing as a Strategic Tool

Financing gets a bad reputation because many businesses first seek it when they're already under pressure. At that point, options narrow, terms get less attractive, and the money often goes toward plugging holes created by weak operations.

Used properly, financing does something different. It protects working capital, smooths timing, and gives you room to make better decisions instead of rushed ones.

Recent guidance from business.gov.au on improving cash flow emphasizes a more practical view. Businesses should focus on profitable customers, consolidate debt, and consider leasing or refinancing assets. It also notes that many practitioners recommend securing credit when cash is healthy and using it as a bridge between receivables and payables, not as emergency rescue capital.

Match the tool to the problem

The first question isn't “What financing can I get?” It's “What cash problem am I trying to solve?”

If the issue is timing volatility, a line of credit is often the cleanest tool. It gives you flexibility when receivables are uneven or inventory needs rise before cash comes back.

If the issue is long customer payment terms, invoice financing may fit better. It directly addresses the lag between completed work and collected cash.

If you need equipment but want to avoid draining operating cash, leasing or equipment financing can preserve liquidity better than an outright purchase. If debt payments are scattered across expensive products, consolidation can simplify outflows and reduce pressure.

Choosing the Right Cash Flow Financing

| Financing Tool | Best For | Typical Speed | Key Consideration |

|---|---|---|---|

| Business line of credit | Short-term working capital gaps and seasonal swings | Often faster than term financing | Works best when arranged before cash gets tight |

| Invoice financing | Slow-paying customers and long receivable cycles | Can be relatively quick once invoices qualify | Costs and customer fit matter |

| Short-term loan | Defined need with near-term payoff plan | Often quick | Don't use it for a chronic operating deficit |

| Equipment financing or leasing | Preserving cash while acquiring needed equipment | Varies by lender and asset | Match term length to useful life of the asset |

| Debt consolidation | Simplifying multiple obligations | Varies | Only helps if the new structure actually improves cash pressure |

A deeper operating perspective on this sits in this guide to layering multiple financing tools without over-leveraging your small business.

When financing helps and when it hurts

Financing helps when three conditions are true.

First, the business understands its cash timing. Second, the borrowed funds solve a specific working-capital problem. Third, management has enough discipline to avoid filling the gap with fresh discretionary spending.

Financing hurts when it covers an unprofitable customer base, stale inventory, poor pricing, or unchecked expenses. In that case, borrowed money can delay the reckoning but rarely fixes the root problem.

Use a blunt test before taking on any facility:

- Can you name the exact cash bottleneck?

- Will this tool shorten or bridge that bottleneck?

- Have you already tightened the operational leaks within your control?

- Do you know how and when the balance gets repaid?

If the answers are fuzzy, pause. Solve the operational issue first.

If the answers are clear, financing can be a smart part of a resilient cash system. It can help you buy inventory for a proven demand window, keep payroll steady during long receivable cycles, refinance a cash-draining asset structure, or reduce pressure while you renegotiate customer and vendor terms.

That's a very different mindset from “debt as last resort.” It's debt as a planned tool, used carefully, with a specific job.

Making Cash Flow Your Competitive Advantage

The businesses that handle stress best usually aren't the ones with the fanciest reports. They're the ones that built habits around cash before conditions got difficult.

That means invoices move out fast. Collections follow a process. Purchasing has guardrails. Inventory gets reviewed with discipline. Leadership looks at a weekly forecast and uses it to make decisions. Financing is lined up while the company is still healthy enough to choose, not beg.

Strong cash flow gives you options. Options let you negotiate better, buy smarter, and grow without panicking every time timing turns against you.

If you're serious about how to improve cash flow, don't try to fix everything at once. Pick one lever from each layer. One operational cleanup. One forecasting habit. One financing decision to prepare before you need it. That's how control starts.

Cash flow management isn't just defense. It lets you act faster than competitors who are constantly waiting on receivables, overstocked inventory, or last-minute funding. The owner with clear weekly visibility can hire sooner, negotiate harder, and move on opportunities with more confidence.

Start with the part you can change this week. Then build from there.

If you need funding options to support that system, Business Loan Warrior is worth a look. It helps small businesses explore working-capital solutions through a single no-fee application, with options that can fit lines of credit, invoice financing, equipment needs, short-term funding, and other cash flow use cases. The best time to line up financing is before a cash crunch forces your hand.