You're probably in a familiar spot. Revenue is solid, the business is healthy, and a real growth opportunity is on the table. It might be a competitor acquisition, a new facility, a large equipment rollout, or a partner buyout. Then your bank gives you an answer that sounds encouraging until you read the term sheet closely: they'll participate, but they won't cover the full need.

That's where many strong companies stall. Not because the deal is bad, and not because the business is weak. The gap exists because one lender rarely wants to carry the entire risk profile of an ambitious transaction.

Capital stacking funding is the practical solution to that problem. Instead of asking one source to do everything, you assemble multiple layers of capital, each designed for a different level of risk, repayment priority, and return expectation. In plain English, you build the financing package the same way you'd build a structure. One layer handles stability, another fills the gap, and another absorbs the most risk in exchange for upside.

For operating businesses, this matters even more than it does in a textbook real estate example. A manufacturer, distributor, restaurant group, contractor, or multi-location retailer doesn't live on asset value alone. It lives on payroll timing, receivables, inventory cycles, and uneven monthly cash flow. A stack that looks elegant on paper can still become a burden if the payment structure doesn't match how the business earns money.

Table of Contents

- Your Next Big Move Needs More Than One Loan

- What Is Capital Stacking The Layer Cake of Funding

- The Building Blocks of Your Capital Stack

- Capital Stack Example A $2M Business Acquisition

- When to Use Capital Stacking for Your Business

- Risks Pitfalls and Key Negotiation Tips

- How to Assemble Your Capital Stack with Confidence

Your Next Big Move Needs More Than One Loan

A business owner sees an acquisition target that fits perfectly. The customer base overlaps. The back office can be combined. Purchasing improves. The owner goes to the bank expecting a straightforward expansion loan and gets partial approval instead.

That outcome is common in larger transactions. The bank may like the business but still cap its exposure. It wants first-position collateral, predictable repayment, and prudent debt levels. That leaves a funding gap between what the senior lender will provide and what the deal requires.

Capital stacking funding solves that gap by turning one financing request into a coordinated capital plan. You're no longer asking a single party to fund every layer of risk. You're pairing the right funding source with the right role in the deal.

Why one lender often says no to the full amount

Banks usually want to be the stable base of the structure. They're not designed to take every kind of risk in the same transaction. If the use of proceeds includes goodwill, integration risk, or a fast expansion timeline, the bank may step back even when the business itself is strong.

That doesn't mean the opportunity is unfinanceable. It means the opportunity needs a mix of capital.

- A senior lender may fund the part supported by hard assets and established cash flow.

- A subordinated or mezzanine piece may bridge the middle gap.

- An equity contribution may cover the top layer where risk is highest.

- A seller note can help when an acquisition seller wants to keep the deal moving.

Practical rule: If your deal is too big, too fast, or too intangible for one lender, the answer often isn't “no.” It's “not with one source.”

Owners sometimes hesitate because the word “stack” sounds complex. In practice, it's effectively a financing team. Each participant knows where they sit, how they get paid, and what risk they're taking. When structured well, that's what gets a serious growth move across the line.

What Is Capital Stacking The Layer Cake of Funding

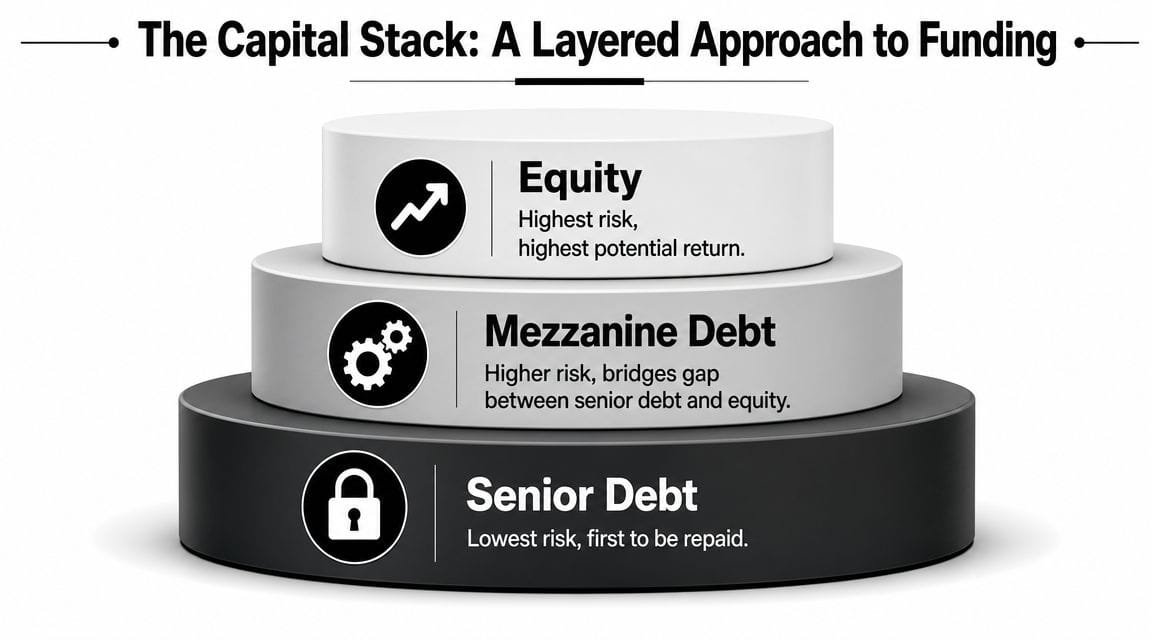

Think of a capital stack like a building foundation with layers above it. The bottom layer has the strongest protection and gets paid first. The layers above it take more risk, so they demand more return. That repayment order is the whole idea.

Industry guidance is clear on this hierarchy: senior debt is paid first, mezzanine or subordinated debt comes next, then preferred equity, and common equity last. Senior debt has first claim on cash flow, and common equity is paid only after all other layers are satisfied, as outlined by Feldman Equities' explanation of the capital stack.

Why the lowest layer is usually the cheapest

The lender at the bottom has the best protection. It gets paid first and often has a senior claim on assets and cash flow. Because that provider takes less downside risk, its pricing is usually the most favorable.

Move upward in the stack and the protection weakens. A mezzanine lender sits behind the senior lender. Equity investors sit behind both debt layers. If the business underperforms, losses are absorbed in reverse order. Origin Investments describes the same basic logic: senior debt sits at the bottom with first repayment priority, while mezzanine financing and equity sit above it with progressively higher risk and return in its overview of how the capital stack works.

Why operating businesses should care about the order

For a business owner, the stack isn't just a chart. It dictates who gets paid first every month and who has flexibility when things tighten up. That's where many owners miss the underlying issue.

A real estate investor may focus on project-level returns and exit value. An operating company has to survive weekly realities. Payroll clears. Inventory lands. Customers pay late. A stack that includes too many hard monthly obligations can create stress even when the business remains profitable on paper.

The stack determines more than cost. It determines how much room the business has to breathe when cash timing gets ugly.

That's why the hierarchy matters. It affects pricing, control, repayment pressure, and how much pain each layer can tolerate before the deal becomes unstable.

The Building Blocks of Your Capital Stack

A good stack isn't assembled from whatever money happens to be available. Each layer has a job. Some provide stability. Some provide flexibility. Some absorb the risk that nobody else wants.

How the core layers behave

The table below gives a practical view of the main layers. The cost column is qualitative because pricing varies deal by deal, and precise APR figures weren't provided in the verified data.

| Capital Type | Repayment Priority | Typical Cost (APR) | Risk Level for Provider |

|---|---|---|---|

| Senior Debt | First | Lower relative cost | Lower |

| Mezzanine Financing | After senior debt | Higher than senior debt | Higher |

| Preferred Equity | After debt, before common equity | Higher relative cost | Higher |

| Common Equity | Last | Highest expected return rather than fixed APR | Highest |

| Seller Note | Usually subordinated to senior debt | Negotiated | Moderate to high |

| Grants | No repayment in the usual debt sense | Not applicable | Program-specific |

| Tax Credits | Structure-dependent | Not applicable in APR terms | Program-specific |

Senior debt is the workhorse. It’s the most protected layer and usually the starting point in any stack. For operating businesses, this might be the bank loan, senior term debt, or an SBA-backed structure. It works best when the business can show reliable cash flow and collateral support.

Mezzanine financing sits in the middle. It exists because many deals outgrow what senior debt alone can cover. It’s useful when the opportunity is strong but the senior lender won’t advance enough against the transaction.

Preferred equity is more patient than debt but still expects priority ahead of common equity. It’s often used when the capital provider wants upside and stronger economics than debt, but not full control.

Common equity is the top of the stack and the first layer to absorb losses. It’s often the owner’s cash, investor capital, or retained capital committed to the transaction. It’s the most expensive money in economic terms because it bears the most risk and waits the longest to get paid.

Other pieces that often matter in business deals

Business acquisitions and expansions often use instruments that don’t get enough attention in simplified capital stack articles.

- Seller notes: In acquisitions, this can be one of the most useful tools in the entire structure. A seller note shows the seller still believes in the business and can reduce the amount of cash needed at closing.

- Grants: For certain projects, grants can reduce the amount of repayable capital in the stack. They won’t fit every business, but when they apply, they can materially improve feasibility.

- Tax credits: These are more specialized and more common in project finance and development-oriented transactions, but they can be part of a broader stack where the project qualifies.

The best stack is not the one with the most layers. It’s the one where each layer solves a specific problem without creating a new one.

In practice, what works is restraint. Owners get into trouble when they add expensive layers just because they can. A clean stack with a strong senior base, a limited gap-filling layer, and a realistic equity contribution usually performs better than a crowded structure full of conflicting agendas.

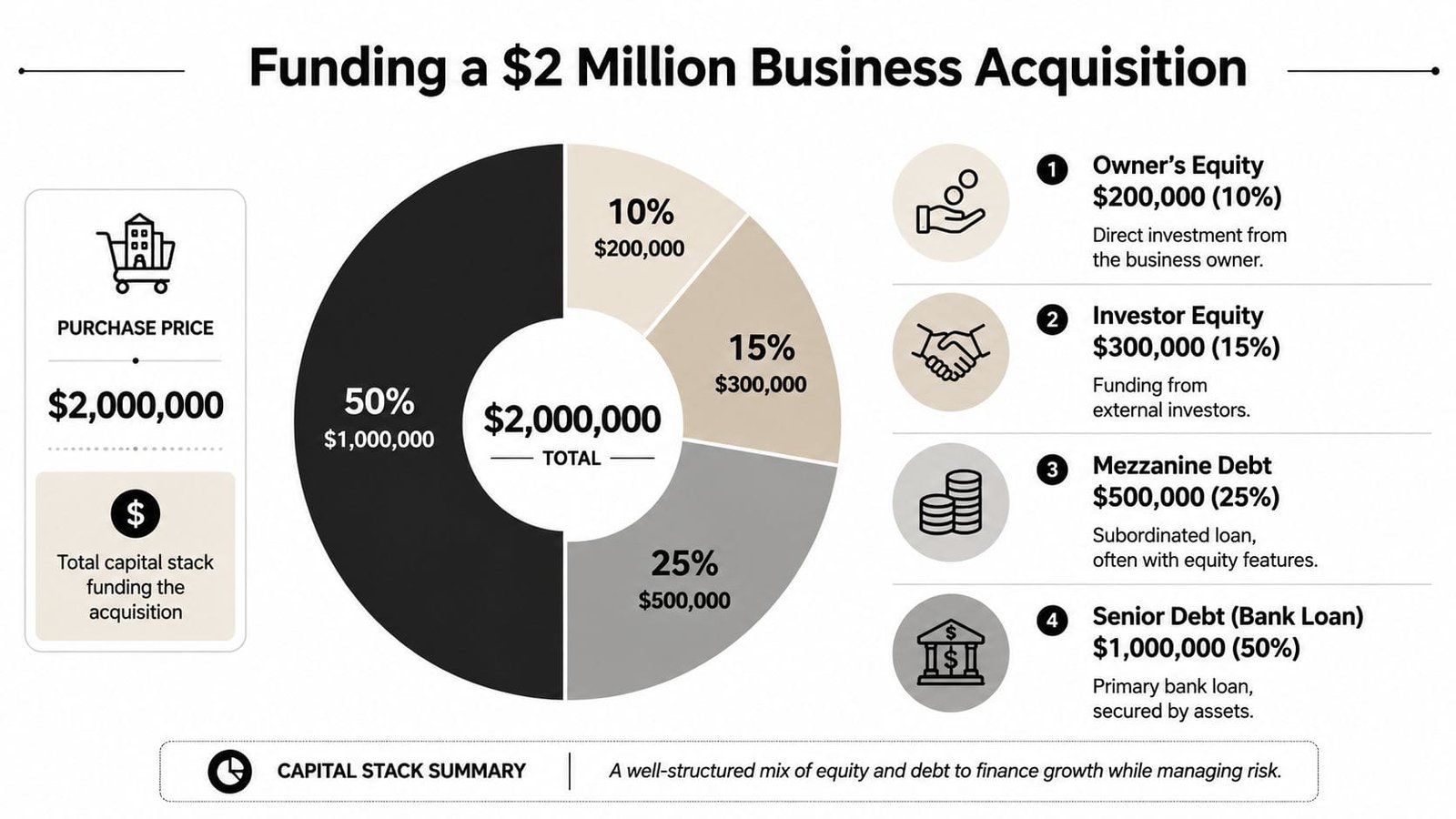

Capital Stack Example A $2M Business Acquisition

A business acquisition is one of the clearest ways to see capital stacking funding in action because the need is immediate and the funding gap is obvious. The buyer has a target company, the seller wants certainty, and the bank usually won’t finance the entire purchase by itself.

Here’s a visual model of a $2 million acquisition using multiple layers of capital.

A workable structure

This example follows the provided deal size and funding breakdown:

- Senior Debt (Bank Loan): $1,000,000

- Mezzanine Debt: $500,000

- Investor Equity: $300,000

- Owner’s Equity: $200,000

That totals the full $2,000,000 purchase price. The point isn’t that every acquisition should use this exact mix. The point is that one lender covers the foundation, while other capital sources fill the rest based on their risk appetite.

A structure like this can work when:

- the bank is comfortable with the core cash flow and collateral base,

- the mezzanine provider believes the acquisition creates additional value,

- the investor accepts junior positioning in exchange for upside,

- and the buyer contributes enough capital to show commitment.

For owners comparing structures, this is the practical value of a layered approach. It can turn a deal from underfunded to executable without forcing one lender to do a job it doesn’t want.

If you’re evaluating acquisition financing options more broadly, this guide to a business acquisition loan is a useful companion to stack planning.

A short walkthrough can also help make the structure more concrete.

What the example really shows

The key lesson isn’t the math alone. It’s the matching.

The senior lender funds the safest slice. The mezzanine piece fills the gap that the senior lender won’t touch. Equity covers the layer that has the least protection but the most upside. That’s exactly why capital stacking can improve funding feasibility when conventional debt by itself would be insufficient, as described in this overview of the power of capital stacking.

What doesn’t work is building the same stack without testing monthly payment pressure. An acquisition can look attractive at closing and still create trouble later if the combined obligations land before synergies show up, customers renew, or the acquired company’s working capital normalizes.

That’s why the smart question isn’t only, “Can we close?” It’s also, “Can this company comfortably carry the stack after closing?”

When to Use Capital Stacking for Your Business

You see this most often at an inflection point. Revenue is holding up, demand is real, and the opportunity is time-sensitive, but one loan by itself leaves a hole somewhere. The bank will fund the equipment, not the software rollout. The SBA lender likes the acquisition, but not the full seller note request. The investor will write a check, but only if senior debt carries part of the load.

That is when capital stacking starts to make sense for an operating business. The goal is not to pile on capital for its own sake. The goal is to fund a transaction completely while protecting day-to-day cash flow.

Situations where stacking makes sense

Capital stacking fits best when the business is healthy, the use of funds is clear, and different parts of the project carry different kinds of risk.

- Acquisitions and buyouts: One lender may support the senior debt, while a seller note or equity layer fills the gap between available financing and purchase price.

- Facility expansion: Real estate, tenant improvements, and added working capital often belong in different buckets. Trying to force them into one facility can weaken the structure.

- Equipment plus ramp-up costs: Asset-based financing may cover the machines, but not hiring, training, inventory buildup, or implementation costs tied to getting them productive.

- Partner buyouts or succession transactions: These deals often work best when term debt is paired with seller financing so the company keeps enough liquidity after closing.

- Multi-loan SBA structures: In the right situation, SBA programs can be part of a broader stack, especially if you are pairing government-backed debt with other capital sources. This guide on having two SBA loans strategically as part of a stacked capital plan explains where that can fit.

A simple way to picture it is building a house layer by layer. The foundation handles the heaviest load. The upper levels add function, but only if the base can carry them. Business capital works the same way. Senior debt should carry the cheapest, safest portion. Higher-cost layers should solve a specific gap, not cover a weak foundation.

What lenders are looking for

For an operating business, lenders care less about the elegance of the structure and more about whether the company can make the payments without starving operations.

They will look closely at recurring cash flow, margin stability, customer concentration, seasonality, collateral coverage, and post-close liquidity. They also want to see that each layer has a clear job. If one tranche is being used to plug losses or make the monthly debt burden look manageable on paper, the stack is probably too aggressive.

This matters most in companies with uneven cash flow. A contractor can have a strong year and still hit tight months because receivables lag. A retailer can post solid annual revenue and still get squeezed between inventory purchases and slow periods. In those businesses, the right stack is often the one that leaves room for working capital, even if it means raising less money or adding more owner equity.

A good stack should help the business grow and still let it breathe. If every layer demands payment before the new location opens, the integration is complete, or the acquired company starts producing expected cash flow, the structure is doing the opposite of what it should do.

Risks Pitfalls and Key Negotiation Tips

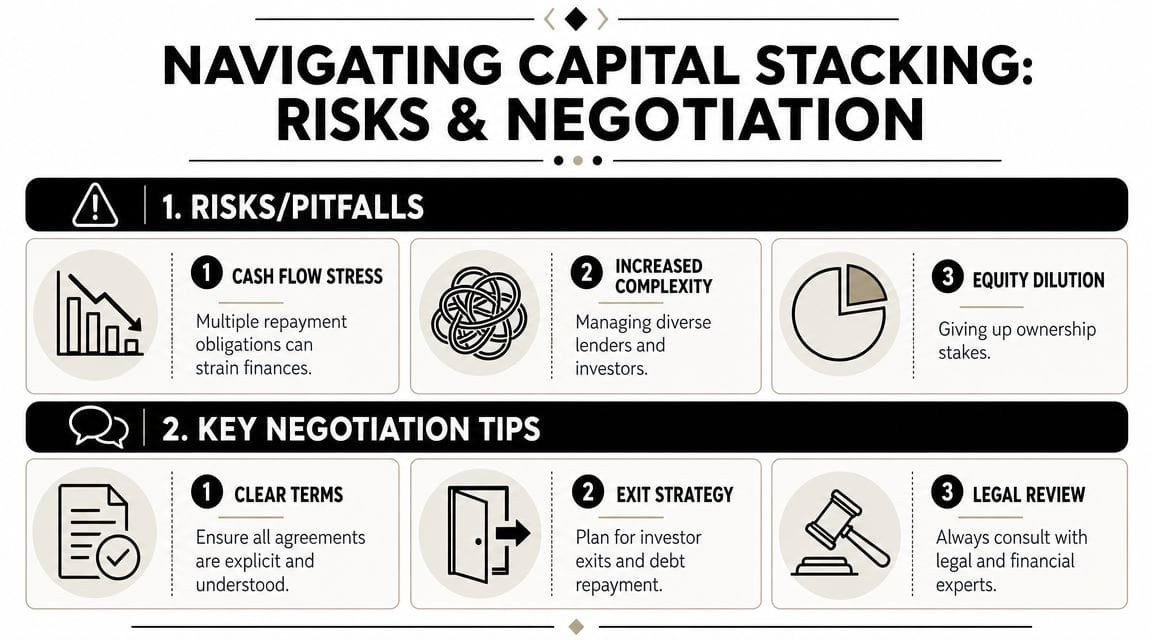

A lot of owners assume more funding sources create more safety. For operating businesses, that’s not always true.

In fact, one of the most important contrarian points in this topic is that a more diversified stack can become more fragile if it replaces flexibility with multiple fixed obligations. That concern is especially relevant where cash flow is irregular, as discussed in CRA Today’s analysis of how capital stacks work.

Where operating businesses get into trouble

The biggest issue is usually cash flow strain, not abstract debt ratios. An owner may have enough projected earnings to justify the deal and still run into trouble because repayment timing is stacked too tightly across senior debt, subordinated debt, and investor expectations.

Other common trouble spots include:

- Intercreditor friction: Multiple parties may disagree about what happens during stress, especially around defaults, cures, or collateral rights.

- Covenant mismatch: One lender may allow flexibility that another lender effectively blocks.

- Control leakage: Equity or quasi-equity capital can bring approval rights that owners didn’t fully appreciate at closing.

- Refinance pressure: If one junior layer matures too quickly, it can force a refinancing timeline the business didn’t plan for.

If you’re also considering whether multiple government-backed structures can coexist, this article on having two SBA loans simultaneously and stacking capital strategically adds useful context.

What to negotiate before closing

Don’t focus only on rate. In stacked deals, terms drive outcomes.

- Align payment expectations: If the senior lender requires aggressive amortization, don’t pair it with a junior layer that also demands tight monthly cash payments.

- Define cure rights clearly: If performance slips, you need to know who can act, how quickly, and on what terms.

- Review consent requirements: Expansion, asset sales, distributions, and refinancing should not require impossible multi-party approvals.

- Plan the exit early: Every capital provider eventually wants repayment, redemption, or liquidity. Know the path before the documents are signed.

Get the documents to tell one consistent story. If the stack works only in a spreadsheet and not in the legal agreements, it doesn’t work.

Strong stacks survive because the parties understand both upside and stress scenarios before money moves.

How to Assemble Your Capital Stack with Confidence

You are under contract to buy a company, the seller wants a fast close, and your bank likes the deal but will not fund the whole amount. That is the point where a lot of owners either force one loan to do too much or grab expensive junior capital without checking what the monthly payment load will do to the business after closing.

Confidence starts with a clear operating picture. Capital stacking only works when the structure fits how cash moves through the company, month by month. Revenue matters, but timing matters more. A business can look strong on an annual P&L and still get squeezed if receivables collect slowly, inventory turns lag, or integration costs hit before the new revenue shows up.

Start with the operating story

Build the file around the questions every lender will ask once they get past the headline numbers.

- What is the use of proceeds? Acquisition, expansion, equipment, partner buyout, or recapitalization.

- What supports the senior layer? Recurring cash flow, hard collateral, contracts, receivables, equipment, or real estate.

- Why does a junior layer belong in the deal? It should cover a gap tied to growth, seller support, earnout timing, or a temporary valuation mismatch.

- What absorbs the first loss if results come in light? Owner equity, outside equity, seller carry, subordination terms, and liquidity on hand.

I usually explain it like building a house layer by layer. The foundation has to carry the weight above it. If the senior loan is already stretched, adding mezzanine debt or a second lien may get the deal closed, but it can leave the operating company carrying a payment structure that belongs in a larger, more predictable business.

Build the package lenders can actually underwrite

A lender needs a file that answers practical questions quickly: current financials, tax returns, a debt schedule, ownership details, a sources-and-uses summary, and projections that show payment capacity under both normal conditions and a tighter quarter. If the plan depends on adding sales staff, raising prices, consolidating locations, or cutting overhead after closing, spell out who will do it, what it costs, and how long it will take.

Clarity wins deals.

Messy stacks often fail because the borrower explains the financing in one sentence and the repayment plan in another, but the two do not match. If one layer expects monthly amortization, another wants a balloon payoff, and a third assumes the line of credit stays fully available, the structure needs more work before you apply.

Before you move, compare how each facility affects cash flow, collateral, and lender consent rights. This guide on how to combine SBA loans, credit lines, and equipment funding wisely is a good starting point for pressure-testing the mix.

Business Loan Warrior helps owners sort through exactly this kind of complexity. If you’re evaluating a growth transaction and need a practical path to the right mix of debt and equity, explore Business Loan Warrior to review funding options, compare structures, and move toward a stack your business can support.