You've built something that works. Revenue is steady, the team knows how to execute, and now the next move isn't opening another small location or adding one more salesperson. It's buying a competitor, a supplier, or a nearby operator with customers, staff, and cash flow already in place.

That's usually the moment a business acquisition loan stops looking like “just financing” and starts looking like strategy.

A first acquisition often feels bigger than it is. Not because the deal is simple, but because owners tend to focus on the headline number, the purchase price, and miss what determines whether the transaction works. The financing has to get you through closing, yes. But the structure also has to leave the business strong enough to handle payroll, vendor terms, customer transition, and the inevitable surprises that show up after signatures are dry.

Table of Contents

- Your Next Move Acquiring a Business

- Understanding the Acquisition Financing Mindset

- Comparing Your Acquisition Loan Options

- How Lenders Decide if You Qualify

- The Loan Timeline from Application to Closing

- Planning Beyond the Purchase Price

- Your Pre-Application Borrower Checklist

Your Next Move Acquiring a Business

A common scenario looks like this. An owner has spent years building a solid company, then sees an acquisition target that would change the business immediately. It might be a smaller competitor with loyal accounts. It might be a distributor that controls margin. It might be a service firm with a team and territory that would take years to build organically.

At that point, cash on hand usually isn't the right tool by itself. Using too much of it can weaken the buyer's core business right when management attention is about to split across integration, retention, and transition. That's where a business acquisition loan becomes useful. It lets you buy earnings, contracts, customer relationships, and operating infrastructure without draining all of your liquidity on day one.

The mistake I see most often is treating the loan as a finish line. It isn't. It's part of a broader deal design. A smart buyer asks different questions than a first-time borrower asks.

- Strategic fit first: Does this target add customers, geography, supply control, talent, or margin?

- Cash flow second: Will the combined business comfortably carry debt after a realistic transition period?

- Structure third: Are the loan terms aligned with what the business can support each month?

- Liquidity always: What cash stays in the company after closing?

The strongest acquisition buyers aren't just trying to get approved. They're trying to stay strong after approval.

That mindset changes how you negotiate. Instead of trying to finance the largest possible purchase price, you start building a capital stack that supports operations. You care about amortization, seller participation, collateral, closing conditions, and post-close cushion. That's how experienced buyers use debt. Not as a gamble, but as a controlled lever for growth.

Understanding the Acquisition Financing Mindset

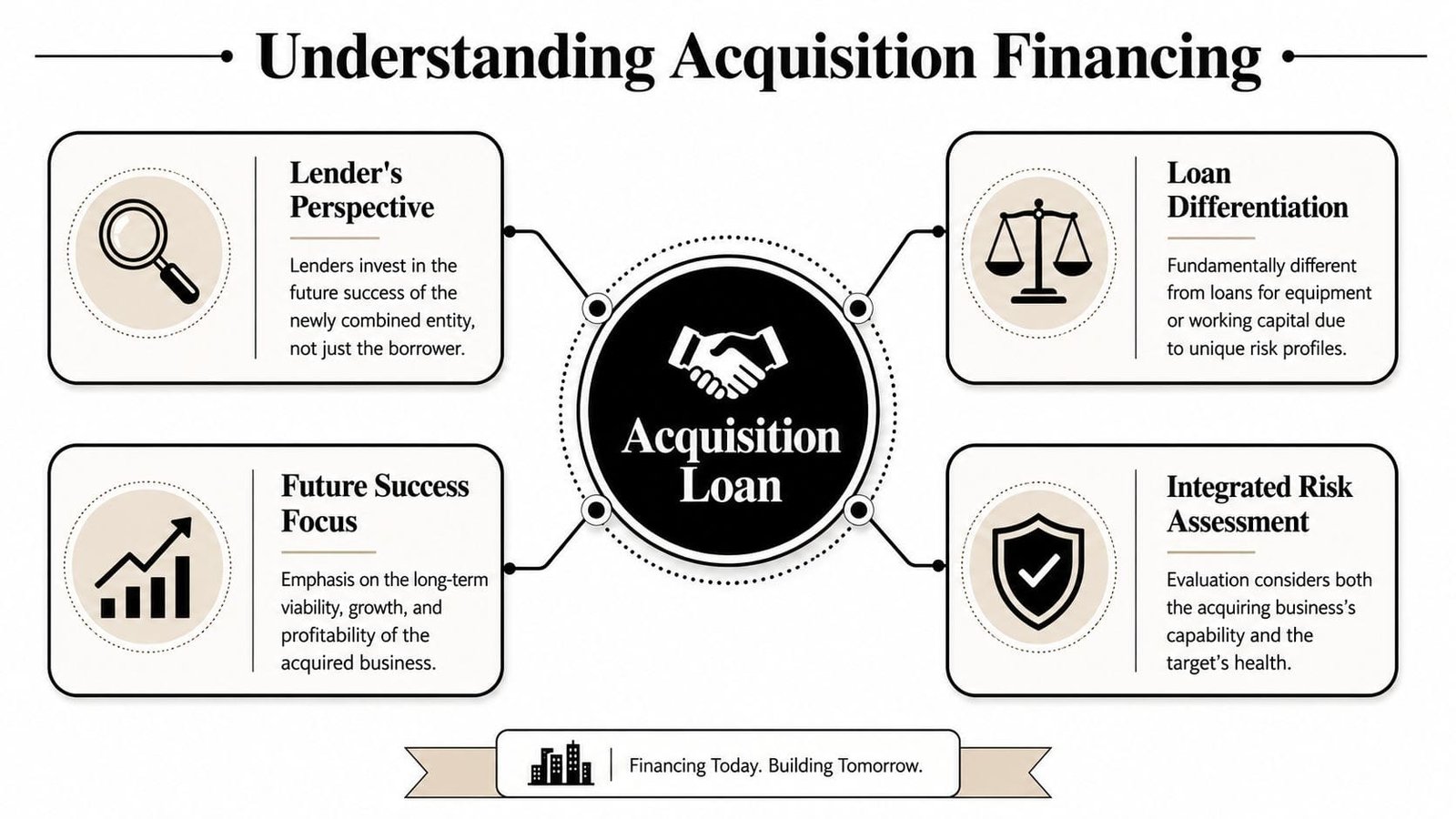

A business acquisition loan is different from an equipment note or a routine working capital facility. The lender isn't only evaluating whether you pay bills on time. The lender is asking whether the business you're buying, under your ownership, will produce enough cash to repay the debt.

That's why acquisition lending feels more like underwriting a new operating story than approving a simple asset purchase.

Why lenders look at two businesses at once

In a standard business loan, the lender may focus heavily on the existing borrower. In acquisition financing, the picture is wider. Lenders underwrite both the buyer and the target because repayment depends on the acquired company's post-close cash flow, and that makes debt service coverage ratio, or DSCR, and working-capital stability central to the credit decision, as explained in M&A Community's discussion of acquisition loan requirements.

DSCR matters because it answers one blunt question: after ordinary operating expenses, is there enough cash available to cover annual debt service?

If the seller's earnings are inconsistent, if customer concentration is too high, or if the buyer has no credible plan to run the operation, lenders get uncomfortable fast. Personal credit still matters. Experience matters. Liquidity matters. But the target's financial quality often carries equal weight.

What this means in practice

When buyers first approach lenders, they often talk about the opportunity in broad strategic language. That's useful, but it's not enough. Lenders want an operator's view.

They want to understand things like:

- Revenue quality: Are customers recurring, contract-based, or highly transactional?

- Margin durability: Can pricing and gross margin hold after ownership changes?

- Operational continuity: Will key employees stay, and will the seller help with transition?

- Cash conversion: How quickly does revenue become usable cash?

Practical rule: If you can't explain how the business turns sales into debt-paying cash, you're not ready to ask for acquisition financing.

This is why good borrowers present a deal in lender language. They don't just say the business is “great.” They show why the combined company should remain stable under debt. That's the mindset shift that moves a deal from hopeful to financeable.

Comparing Your Acquisition Loan Options

Most buyers end up considering three routes: SBA 7(a), conventional bank debt, and seller financing. Each can work. Each can also create problems if it's mismatched to the deal.

The right choice depends less on what sounds cheapest at first glance and more on what leaves the business workable after closing.

SBA 7 a for cash flow protection

In many small-business change-of-ownership transactions, SBA 7(a) is the default structure because it can support deals up to $5 million and can often amortize over as long as 25 years, which reduces required monthly debt service compared with conventional 3 to 5 year business loans. That longer schedule can improve DSCR and make debt-financed acquisitions more workable for buyers with solid operating experience and at least about 10% equity injection, as outlined in Seacoast Bank's business acquisition loan guide.

That longer repayment profile is a major advantage if the acquired company needs time to stabilize under new ownership. It can also help when the business has seasonality or when the buyer wants room to invest in systems, hiring, or customer retention after closing.

SBA financing isn't perfect. Documentation is heavier. Underwriting can feel slower and more procedural. If the seller wants a lightning-fast close, the process can create friction.

Conventional bank debt for cleaner deals

A conventional loan can be attractive when the buyer is financially strong, the target has clean books, and the bank already understands the industry. Conventional lenders can sometimes offer more flexibility around structure and fewer program-specific constraints.

The trade-off is usually pressure on monthly payments. Shorter amortization means the business has to carry more debt service sooner. That may be fine for a highly stable target with predictable cash flow. It's much less forgiving when integration risk is real.

Seller financing for alignment and gap-closing

Seller financing often solves problems that bank debt alone cannot. It can bridge a valuation gap, reduce the buyer's immediate cash requirement, or show that the seller has confidence in the durability of the business.

It can also help if the lender wants the seller to remain economically tied to the transition. That alignment matters in deals where customer handoff, training, or relationship continuity will determine post-close stability.

For buyers considering less traditional structures, this overview of unsecured business acquisition loan strategies is worth reviewing alongside secured options.

Business Acquisition Loan Comparison

| Feature | SBA 7(a) Loan | Conventional Bank Loan | Seller Financing |

|---|---|---|---|

| Best fit | Buyers who want lower monthly debt service and a more supportable post-close structure | Strong borrowers buying clean, bankable targets | Deals with trust between buyer and seller or valuation gaps |

| Repayment profile | Often longer amortization, which can ease cash flow pressure | Usually shorter repayment window, which raises monthly burden | Negotiated directly, often flexible |

| Use case strength | Good for leveraged acquisitions where DSCR needs room | Good for lower-risk situations with strong financial quality | Good as a supplement to senior debt or as a bridge |

| Process | More formal and document-heavy | Relationship-driven and credit-sensitive | Negotiation-driven |

| Operational impact after close | Often the most forgiving on monthly payment load | Can be tight if transition takes longer than expected | Helpful if payments are structured around business reality |

A financing package that looks efficient on closing day can become restrictive by the second payroll cycle if the amortization is too aggressive.

The best acquisition structures often combine these tools rather than forcing one source to do all the work.

How Lenders Decide if You Qualify

Lenders don't approve an acquisition because the target looks attractive in a broker memo. They approve it when they believe two things are true: the business can support the debt, and you can operate it without breaking what already works.

The target has to carry the story

Lenders review the company you're buying with unusual intensity. They're looking for stable earnings, understandable financial statements, manageable add-backs, and a business model that still makes sense after the seller leaves.

Many first-time buyers often stumble. They focus on the purchase multiple and don't pressure-test the operating engine. A lender will.

Pay special attention to:

- Financial statement quality: If the books are messy, every other part of underwriting gets harder.

- Customer concentration: Heavy dependence on one or two accounts raises concern.

- Owner dependence: If the seller is the rainmaker, technician, and relationship hub, transition risk rises sharply.

- Working-capital pattern: A business that regularly strains cash before payroll or inventory cycles will get extra scrutiny.

You have to look like the right operator

The other side of the file is you. Relevant management experience often matters more than buyers expect because lenders want evidence that you can preserve cash flow through transition. They're not just funding a purchase. They're backing execution.

The best borrower presentations usually include a concise operating plan, not a glossy pitch deck. Show how reporting will work, who keeps customer relationships, who handles finance, what changes immediately, and what stays untouched for the first phase of ownership.

If you're preparing for an SBA path, these top SBA loan qualification requirements provide a useful framework for organizing the borrower side of the package.

Buyers win approvals when they remove uncertainty. Clean records, clear experience, and a realistic integration plan do more than optimism ever will.

What strengthens an application

A lender's confidence improves when the buyer can demonstrate:

- Clear repayment logic based on the acquired business's actual cash generation.

- Operational credibility through direct industry or adjacent management experience.

- Thoughtful equity contribution that shows commitment and leaves the capital structure balanced.

- A sober transition plan that assumes some friction instead of assuming perfection.

A weak file usually has the opposite profile. Aggressive assumptions. Thin explanations. Unclear handoff from seller to buyer. No serious plan for managing cash after close.

The Loan Timeline from Application to Closing

Most acquisition financings don't fail because the idea is bad. They fail because the process loses momentum. Documents arrive late, diligence uncovers inconsistencies, the seller grows impatient, or the buyer mistakes lender silence for progress.

The financing market is also more selective than many buyers assume. In 2023, only 34% of SBA applicants received full approval, and approved SBA lending included 106,534 loans totaling $41.7 billion, with reported average loan sizes of $391,584 and $479,685 from the same broader lending dataset, according to Credit Suite's small-business lending statistics and trends. Those figures tell you two things. Approval is competitive, and these are meaningful credit decisions, not quick consumer-style approvals.

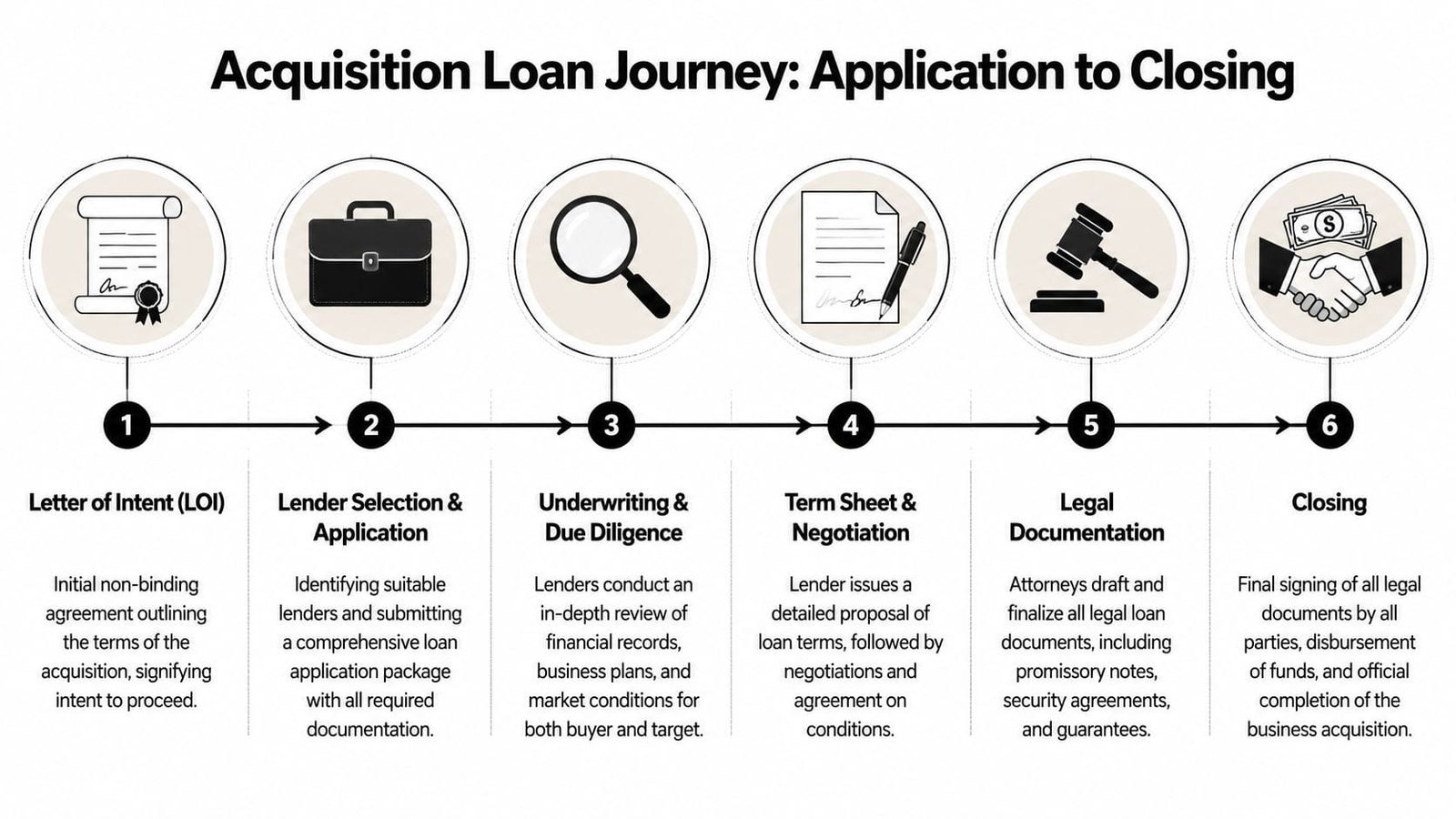

A visual timeline helps keep everyone aligned.

The six stages that matter

LOI signed

The letter of intent gives the lender a deal to underwrite. If the LOI is vague on price, structure, transition support, or assets included, financing questions multiply.Application package submitted

At this stage, organized buyers separate themselves. Personal financials, business financials, tax records, deal summary, and target information should arrive as one coherent package.Underwriting and diligence

The lender tests the file. Expect questions on earnings quality, customer concentration, debt service capacity, and your operating background.

Before moving deeper into the closing path, it helps to hear a lender-oriented overview of the process.

Where deals usually slow down

The next phase often stalls because buyers underestimate how much follow-up underwriters require.

- Inconsistent financials: If tax returns, P&Ls, and seller narratives don't align, the file slows immediately.

- Loose diligence responses: Partial answers create more questions instead of resolving them.

- Unclear legal structure: Asset purchase versus stock purchase issues can affect documentation and collateral analysis.

- Seller impatience: A seller who expected a quick close may need active communication to stay committed.

The final approach to closing

After diligence clears, the lender issues terms and conditions, counsel prepares documents, and the parties work through closing requirements. This stage is administrative but not casual. Insurance, entity documents, guarantees, security instruments, and closing funds all have to line up.

The buyers who close efficiently treat financing like a managed transaction, not a form submission.

A disciplined borrower keeps a checklist, names one point person, and responds quickly. That alone can preserve weeks of momentum.

Planning Beyond the Purchase Price

The most common financing mistake in acquisitions is simple. Buyers obsess over how to fund the purchase price and give far less attention to what the business will need in the first months after closing.

That's backwards.

Why the closed deal can still become a stressed deal

SBA-backed acquisition loans can finance goodwill and acquired assets, but buyers still need a separate plan for operating liquidity because the acquisition debt itself is typically a term structure, not a day-to-day buffer. That working-capital gap is one of the most underexplained parts of the process, as noted in Stearns Bank's guide to funding a business acquisition with a small business loan.

That issue becomes visible quickly in service businesses, thin-margin operators, and companies with uneven receivables cycles. You may own a profitable company on paper and still feel squeezed if customer payments lag, payroll runs weekly, or repairs hit early in the transition.

Questions smart buyers ask before they close

Use this short stress test before you lock the structure:

- If revenue dips early, what cash absorbs the shock?

- If one key employee leaves, what does replacement cost do to liquidity?

- If the seller's relationships don't transfer cleanly, how long can the business carry slower collections?

- If integration takes longer than expected, do you still have room to make debt payments without starving operations?

These aren't pessimistic questions. They're operating questions.

One useful concept here is capital stacking in business funding, where acquisition debt is paired thoughtfully with other funding tools rather than forcing one term loan to solve every capital need.

What tends to work better

A better structure often includes a financing plan that separates acquisition capital from operating capital. That might mean preserving more cash at closing, negotiating seller terms that reduce immediate pressure, or arranging an additional liquidity source that supports receivables, inventory, or transition costs.

Buy the business with enough money left to run it. That sounds obvious, but many acquisition problems start when buyers ignore it.

What doesn't work is stretching every dollar into the purchase and assuming the company will self-fund the transition immediately. Even strong businesses wobble during ownership change. Customers ask questions. Staff test the new leadership. Reporting may need cleanup. Vendors may tighten terms until confidence returns.

The loan should help you buy the company. The capital plan should help you keep control of it.

Your Pre-Application Borrower Checklist

Well-prepared buyers get better conversations with lenders. They also spot weaknesses earlier, which is often more valuable than speed. Before you approach financing sources, assemble a file that makes the deal easy to understand on first review.

Personal borrower documents

Start with the items that show who you are financially and operationally.

- Personal financial statement: Current and complete.

- Personal tax returns: Lenders usually want a clean record of your income picture.

- Resume or operating biography: Highlight industry leadership, integration experience, and management scope.

- Liquidity summary: Show what cash is available for equity injection and post-close support.

Target business documents

This package should let a lender evaluate the company without chasing basic information.

- Profit and loss statements: Organized and clearly labeled.

- Balance sheets: Current and historical.

- Business tax returns: A multi-year view is standard in most acquisition reviews.

- Accounts receivable and payable detail: Especially important where working capital swings matter.

- Customer and vendor concentration detail: If applicable, explain the relationships.

Deal documents and transaction support

A lender can't underwrite a vague idea. It needs a defined transaction.

- Letter of intent or purchase agreement: Include price, structure, and major terms.

- Business valuation or price support: If available, include the analysis behind the purchase price.

- Use of funds schedule: Show exactly where capital goes.

- Transition plan: Spell out seller involvement, key employee retention, and immediate operating priorities.

- Integration notes: Even a simple memo is helpful if it shows how the business will run on day one.

A good checklist does more than collect paper. It forces discipline. If you can't organize the file, you probably can't defend the deal under lender scrutiny.

Business Loan Warrior helps owners explore business acquisition financing without turning the process into a paperwork maze. Through a Business Loan Warrior funding platform, borrowers can check options through a single no-fee application, review customized funding paths, and move faster with support that fits real operating needs before and after closing.