Revenue-based financing lets a business get capital now and repay it with a small share of future monthly revenue, often 5% to 15%, until a fixed total is reached, commonly 1.5x to 3x the original advance. It's non-dilutive, which means you don't give up ownership in your company.

If you're looking at your numbers and thinking, “Sales are coming in, demand is real, but cash is still tight,” you're in the exact situation where this funding option starts to matter. Maybe you need inventory before peak season, paid acquisition budget while returns are working, or hiring capacity before your current team burns out. The problem isn't always lack of revenue. Often it's timing.

Traditional choices can feel like a bad fit. A bank loan may come with fixed payments that don't care whether next month is strong or soft. Equity means someone else now owns part of what you've built. Revenue-based financing sits in the middle. It gives you growth capital tied to how your business performs.

Most guides stop there. They explain the pitch, but not the math. That's where business owners get tripped up. A product can be flexible and still expensive. It can be non-dilutive and still be the wrong fit. The useful question isn't just what is revenue based financing. It's whether the structure works for your cash flow, your margins, and your growth plan.

Table of Contents

- Your Business Is Growing Fast But So Is Your Need for Capital

- The Core Concept of Revenue Based Financing

- How RBF Repayments and Costs Are Calculated

- RBF vs Traditional Loans vs MCAs vs Equity

- The Ideal Candidate Profile for RBF

- Your Application Checklist for RBF Providers

- Is Revenue Based Financing Right for Your Business

- Frequently Asked Questions About RBF

Your Business Is Growing Fast But So Is Your Need for Capital

A lot of healthy businesses hit the same wall. Orders are coming in. Customers want more. Your marketing works well enough that you know where to put the next dollar. But cash is trapped between today's expenses and tomorrow's revenue.

A founder running a subscription software company might need budget for customer acquisition. An e-commerce operator may need to buy inventory before a major sales window. A service business may need to add staff before signed work turns into collected cash. None of those situations mean the business is broken. They mean the business is stretching.

The awkward middle between debt and equity

Many owners feel cornered. Traditional bank debt may ask for rigid monthly payments, hard collateral, or personal exposure. Venture capital solves the cash problem differently, but it changes the ownership story and often pushes the company toward a very specific growth path.

Revenue-based financing was built for companies stuck in that middle. It gives a business capital upfront and ties repayment to revenue performance instead of a flat installment. For owners who want growth money without selling part of the company, that trade-off can be attractive.

Practical rule: RBF tends to make the most sense when the business already knows how it will turn fresh capital into more revenue.

This isn't a fringe product anymore. The market was estimated at US$6.4 billion in 2023 and projected to reach US$15.86 billion by 2026, with a projected 39.4% compound annual growth rate, according to Allied Market Research's revenue-based financing market outlook. That growth is tied to recurring-revenue businesses such as SaaS and e-commerce, where revenue-linked repayment is easier to underwrite.

Why owners get interested so quickly

RBF speaks directly to a founder's instincts:

- Keep control: You don't hand over equity.

- Match payments to reality: Payments move with sales instead of ignoring them.

- Fund growth uses: Inventory, marketing, expansion, and hiring are easier to support when capital arrives upfront.

The appeal is real. So is the need for caution. Flexible payments don't automatically mean cheap capital, and fast funding doesn't automatically mean good funding. The mechanics matter.

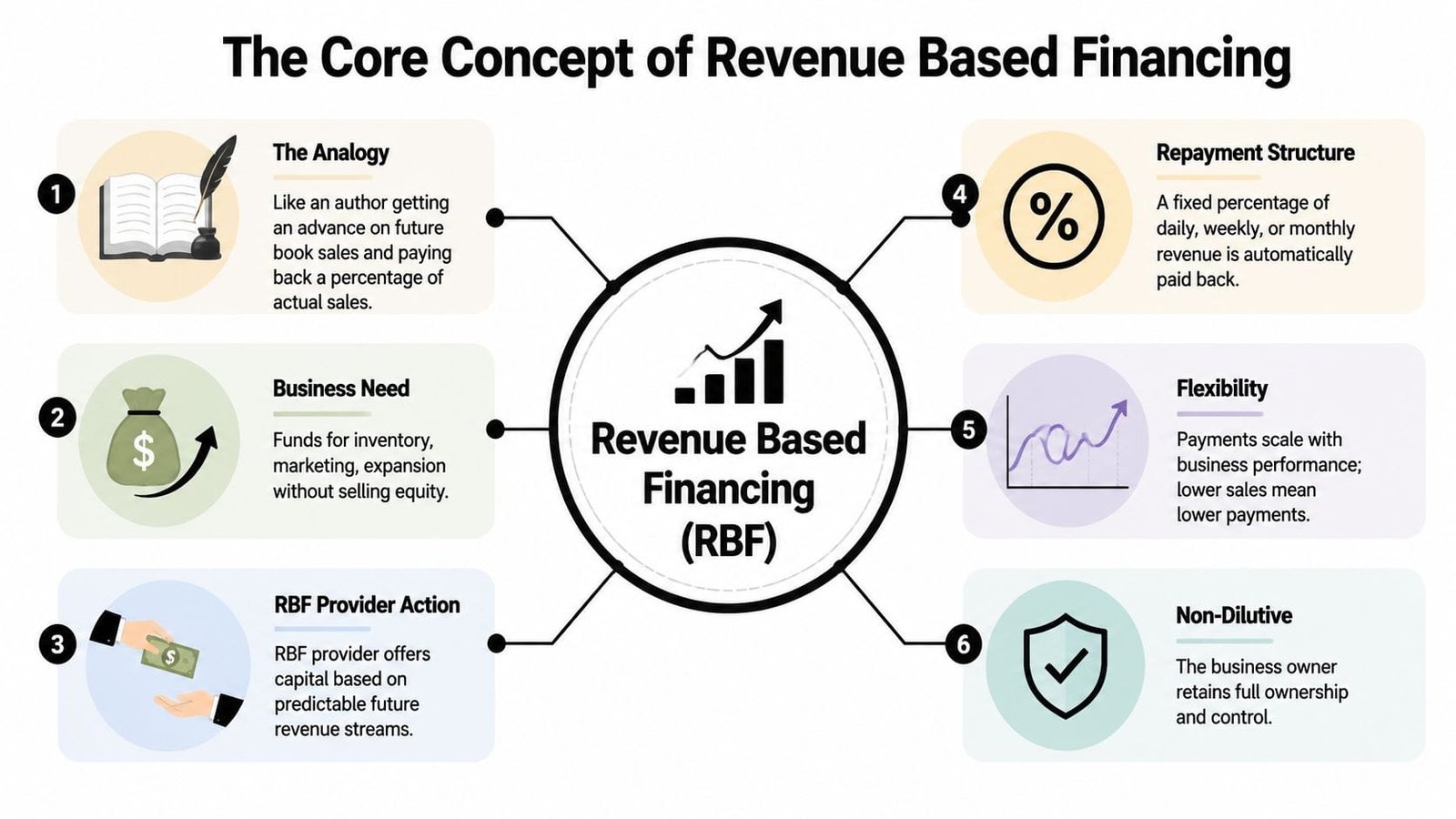

The Core Concept of Revenue Based Financing

Revenue-based financing is straightforward once you separate the mechanics from the marketing language.

A provider gives your business capital upfront. In return, the provider receives an agreed percentage of your future revenue until a set total has been repaid. The payment rises in strong sales periods and falls in slower ones, which is why RBF often feels easier on cash flow than a fixed monthly loan payment.

A helpful comparison is an author's book advance. The publisher pays the author before all the sales happen, then recovers that advance from future book revenue. If the book sells quickly, the advance is earned back sooner. If sales come in more slowly, recovery takes longer. RBF follows the same basic rhythm, except the revenue source is your business rather than book royalties.

The three moving parts

Every RBF deal depends on three terms, and each one affects what the financing will feel like in real life.

The advance

This is the lump sum your business receives upfront.The revenue share

This is the percentage of monthly revenue sent to the provider.The repayment cap

This is the total amount you agree to repay before the obligation ends.

Those pieces work together like a faucet, a bucket, and a fill line. The revenue share controls how fast money flows out each month. The cap sets the line where repayment stops. The advance is the amount you got at the start.

One source of confusion is the difference between the payment and the payoff target. The revenue share determines each month's payment. The repayment cap determines the total amount due over the life of the agreement. According to Re-cap's overview of revenue-based financing, revenue shares often fall in the mid-single-digit to mid-teen range, and repayment caps are commonly expressed as a multiple of the original advance.

That distinction matters because many owners focus on the flexible monthly payment and skip the harder question: how much capital am I giving up in total, and how quickly could this repay if revenue grows faster than expected? If you want a useful answer, build a cash flow forecast that helps shape your financing decision before you sign anything.

Below is a short explainer if you'd rather hear the concept first and read the details second.

Another phrase that causes confusion is "not a loan." Some providers use that label because the structure may not have a standard interest rate or a fixed installment schedule. For an owner deciding whether the offer is good, the better question is simpler: how much do you receive, how much might you repay, and how will those payments behave when sales rise or fall?

If you remember one thing, remember this: RBF ties payment timing to revenue, but the total repayment obligation is still set by the deal terms.

How RBF Repayments and Costs Are Calculated

Revenue-based financing then stops being a story and becomes a spreadsheet.

The basic formula is simple. First, identify the total amount the provider expects back. Then model how long it may take to repay based on the percentage taken from revenue each period. In many structures, the provider is effectively purchasing a slice of future revenue. Repayment percentages typically fall between 5% and 25% of gross revenue, standard maturity is often 3 to 5 years, and if the full cap isn't reached by maturity, the remaining balance may become due, according to Capchase's explanation of royalty-style revenue financing.

What actually changes month to month

What moves is the payment amount, not the cap.

If your agreement says the provider takes a fixed share of gross revenue, then the payment changes as revenue changes. Strong month, bigger payment. Soft month, smaller payment. That flexibility is the main operating advantage of RBF over a fixed-payment loan.

You can model it like this:

| Month | Revenue | Revenue Share | Payment |

|---|---|---|---|

| Month A | $20,000 | 10% | $2,000 |

| Month B | $50,000 | 10% | $5,000 |

That table is only an illustration of the math. The useful lesson is cash flow behavior. A fixed loan installment doesn't shrink when revenue dips. An RBF payment usually does.

To test whether that flexibility helps your business, build a downside case instead of only a growth case. A good cash flow forecast for loan strategy helps you see whether a revenue-linked payment still leaves enough room for payroll, rent, inventory, and ad spend in weaker months.

How to estimate the real cost

This is the part many explainers skip.

RBF is often sold using language like “no APR” or “not a traditional loan.” That may be legally or structurally relevant, but it doesn't answer the business question. Your real cost starts with this:

Total financing cost = total repayment cap minus the amount advanced

If you receive capital and agree to repay more than you received, that difference is your financing cost.

Use this checklist when reviewing an offer:

- Start with the total payback: What is the exact maximum dollar amount you will repay?

- Map the share of revenue: Is the provider taking monthly revenue, weekly revenue, or another cadence?

- Estimate the pace: If sales grow quickly, you'll likely finish repayment faster. If sales stall, the agreement may stay with you longer.

- Check the maturity clause: Some structures may require the remaining balance if the cap hasn't been reached by the end of the term.

- Ask about additional fees: The cap may not be the only economic cost.

Faster repayment can increase the effective annualized cost, even when the total cap never changes.

That point surprises owners. Two companies could have the same cap. The one that repays much faster may be giving up capital at a higher annualized cost because the provider gets repaid sooner.

RBF vs Traditional Loans vs MCAs vs Equity

The smartest way to evaluate funding isn't to ask which product sounds best. It's to ask which trade-offs your business can live with.

Revenue-based financing sits between several familiar products. A term loan gives certainty but usually expects fixed payments. A merchant cash advance often moves fast but can be expensive and operationally intrusive. Equity removes scheduled repayment but gives up ownership. RBF mixes features from all three.

Funding options at a glance

| Feature | Revenue-Based Financing (RBF) | Traditional Term Loan | Merchant Cash Advance (MCA) | Venture Capital (Equity) |

|---|---|---|---|---|

| Ownership dilution | No | No | No | Yes |

| Repayment structure | Percentage of revenue until cap is reached | Fixed scheduled payments | Sales-linked remittance structure | No scheduled repayment |

| Collateral or guarantee | Often based more on revenue profile than hard collateral | Often stronger emphasis on collateral, guarantees, and credit standards | Varies by provider | No collateral in the lending sense |

| Speed of funding | Often faster than bank processes | Often slower than fintech products | Often fast | Usually slow |

| Cost structure | Fixed repayment cap tied to revenue share | Interest-based repayment structure | Purchase or advance structure with its own fee model | Cost is dilution and loss of future upside |

The MCA comparison matters because many owners confuse the two. They can both pull from sales, but that doesn't mean they behave the same way in underwriting, structure, or economics. If you want a deeper side-by-side on that category, this guide to merchant cash advances for small businesses helps separate use cases.

How to compare true cost without getting fooled by wording

One of the biggest mistakes founders make is comparing product labels instead of economic outcomes.

RBF is often marketed as “not a loan” and “no APR,” but the economic cost can still be analyzed. Broader debate around sales-based financing disclosures has grown as state-level commercial financing disclosure rules have expanded, and many explainers still don't show how to compare repayment caps against loans or MCA-style products, as noted in Wikipedia's summary of revenue-based financing and disclosure treatment.

A practical comparison method looks like this:

- For RBF: Calculate total dollars repaid above principal, then estimate how quickly repayment is likely under conservative, expected, and strong revenue cases.

- For a term loan: Review total interest and fees over the actual repayment period.

- For an MCA: Focus on total payback, remittance pressure, and how daily or frequent withdrawals affect operating cash.

- For equity: Ask what percentage of ownership you're giving away and what that could be worth if the company performs well.

The cheapest capital on paper isn't always the safest capital for your cash flow. The most flexible capital isn't always the cheapest.

That's why “apples to apples” means comparing cash flow pressure, total dollars repaid, ownership impact, and downside risk together. Not one at a time.

The Ideal Candidate Profile for RBF

Revenue-based financing works best for a narrow kind of business. When it fits, it can be elegant. When it doesn't, it can create pressure at exactly the wrong time.

Businesses that usually fit well

The strongest RBF candidates tend to have predictable revenue and healthy margins. Qualification often requires $15,000 to $25,000 in monthly recurring revenue, roughly $200,000 to $300,000 annually, plus gross margins above 50%, with credit history often less important than revenue predictability, according to Flex's overview of revenue-based financing qualification.

That profile points to businesses such as:

- Subscription software companies: Monthly recurring revenue makes repayment easier to model.

- E-commerce brands with consistent demand: Especially when inventory turns and contribution margins are well understood.

- Tech-enabled services: Businesses with repeat clients, reliable billing, and strong unit economics.

- Companies with a clear use of funds: Customer acquisition, inventory expansion, or growth hiring can all fit when the capital is likely to produce more revenue.

Businesses with diversified revenue sources also tend to look stronger. If one customer or one sales channel carries too much weight, the revenue stream becomes harder to trust. This is why many operators benefit from doing revenue mix stress tests that lenders actually trust before they ever submit an application.

Businesses that should be careful or look elsewhere

RBF is usually a poor fit for a few groups.

- Pre-revenue startups: No revenue history means there isn't much for a provider to underwrite.

- Low-margin businesses: A percentage of top-line revenue can hurt if gross profit leaves little room after cost of goods sold.

- Project-based firms with lumpy billing: If cash comes in irregular bursts, repayment may become awkward even when annual sales look fine.

- Businesses already under strain: Flexible payments help, but they don't erase an underlying profitability problem.

Here's a useful filter. If you can't comfortably give up a slice of revenue during a slow month, you probably shouldn't take a revenue-linked product. If your growth engine is already working and you need fuel, RBF becomes more compelling.

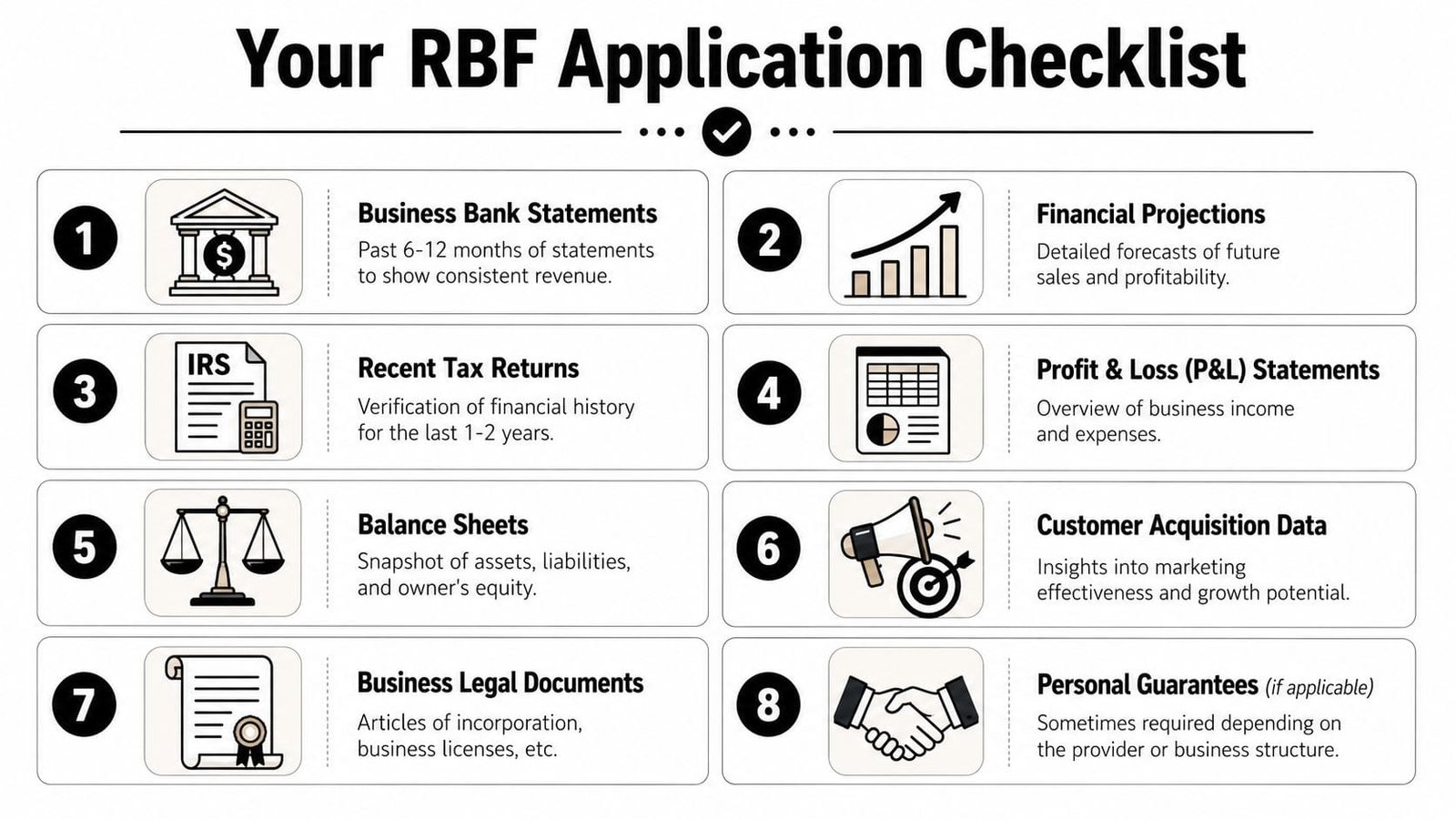

Your Application Checklist for RBF Providers

Founders often expect an RBF application to focus mostly on credit. In reality, providers usually care more about revenue quality, account visibility, and whether your business can absorb the repayment structure without choking growth.

What providers usually want to review

Expect a provider to ask for operating and financial records that show consistency, margins, and sales behavior.

A practical checklist usually includes:

- Bank statements: To verify deposits, timing, and revenue stability.

- Profit and loss statements: To see margin profile and operating performance.

- Balance sheets: To understand liabilities, cash position, and working capital.

- Tax returns: To confirm historical financial consistency.

- Revenue reports: Especially if the business runs through subscription platforms, payment processors, or e-commerce systems.

- Financial projections: To show how the capital will be used and how repayment may unfold.

- Legal documents: Formation records, ownership information, and core business registrations.

- Customer or channel data: Helpful when the provider wants to understand concentration risk.

The sharpest applications don't just dump files into a folder. They tell a story. The story is that revenue is predictable, margins are healthy enough, and the requested capital will likely produce more revenue than it consumes.

Questions you should ask before signing

A founder should do just as much diligence on the provider as the provider does on the business.

Ask questions like these:

How do you define revenue?

Gross sales, net sales, processor deposits, and recurring revenue are not the same thing.How often do you collect payments?

Monthly feels very different from more frequent remittance.What is the exact repayment cap?

Ask for the total dollar amount, not just the multiple.Is there a maturity date?

If there is, ask what happens if the cap hasn't been fully repaid by then.Are there fees outside the cap?

Documentation fees, platform fees, and servicing charges change the effective cost.What happens with early repayment?

Some products don't reward early payoff in the way a borrower expects.Do you require access to bank or payment data?

Know what systems are being connected and how long access remains in place.

Ask the provider to show your repayment under a weak month, a normal month, and a strong month. If they won't, that's a warning sign.

Clarity matters more than speed here. The right offer should be understandable before it's attractive.

Is Revenue Based Financing Right for Your Business

Revenue-based financing can be a strong option for a business that has real revenue, solid margins, and a clear plan to turn new capital into more sales. Its biggest strength is flexibility. Payments move with revenue, and founders keep ownership.

Its main trade-off is cost. Even when a provider avoids traditional loan language, you still need to measure total dollars repaid, timing of repayment, and what that does to cash flow. That comparison is what separates a useful growth tool from an expensive shortcut.

RBF usually fits growth-stage companies better than early-stage experiments. It tends to work best when revenue is predictable and the business can handle giving up a slice of top-line receipts while still operating comfortably.

If you're evaluating what is revenue based financing for your own company, don't stop at the headline promise. Model the repayment. Pressure-test the downside. Compare it with a term loan, an MCA, and the cost of giving away equity. The best capital choice is the one that still looks good when your most optimistic forecast is wrong.

Frequently Asked Questions About RBF

Is RBF a loan

It depends on whether you're asking a legal question or a practical one.

Some providers structure it as a purchase of future revenue or a non-dilutive advance rather than a traditional term loan. Practically, though, your business receives capital and repays more than it received under an agreed structure. That's why you should focus less on labels and more on total repayment, payment behavior, and contract terms.

What happens if revenue drops

Your payment usually falls with revenue because repayment is tied to a fixed percentage of sales rather than a fixed installment. That's the core advantage for cash flow management.

But lower payments don't erase the obligation. If revenue remains weak for too long, repayment may stretch out, and any maturity provision in the agreement becomes more important.

Can you repay early

Sometimes, but you need to read the agreement carefully.

With many RBF structures, the provider expects the full cap unless the contract explicitly offers an early payoff discount or another adjustment. Never assume that paying early automatically reduces the total amount owed. Ask for the exact payoff method in writing before signing.

What if the cap is not fully repaid by maturity

Some agreements include a maturity date. If the cap hasn't been fully reached by then, the remaining balance may become due. This is one of the most important clauses in the contract because it changes the downside case.

If the provider mentions a standard term, ask what happens operationally at the end of that period. Don't rely on marketing language. Read the actual agreement.

Does RBF work for every business model

No. It generally works better for companies with recurring or highly predictable revenue and healthy margins.

It tends to be a tougher fit for pre-revenue startups, seasonal operators with thin margins, or companies with highly irregular billing patterns. The test is simple. If a slice of revenue coming off the top would create stress in ordinary months, the product may not fit your business well.

If you're weighing RBF against loans, MCAs, or other working capital options, Business Loan Warrior can help you compare real offers without turning the process into a full-time job. You can submit one application, review funding paths that match your business profile, and evaluate options with a clearer view of repayment structure, cash flow impact, and total cost.