Most advice on merchant cash advance leads is outdated the moment it tells you to solve volume problems by buying cheaper lists.

That playbook worked when competition was looser, contact channels were less saturated, and brokers could hide weak process behind brute-force dialing. It doesn't hold up in a market where lead quality, borrower trust, and compliance discipline decide whether you fund deals or burn cash. If your acquisition strategy starts and ends with “who has the lowest CPL,” you're not building a pipeline. You're renting volatility.

The opportunity is still real. The U.S. merchant cash advance market exceeded $15 billion in 2023 and is projected to reach between $18 billion and $25 billion annually by 2026, with the average deal size around $65,000 according to the merchant cash advance industry report. But that growth cuts both ways. More providers are chasing the same merchants, more merchants are comparison-shopping, and more regulators are watching how offers are marketed, disclosed, and sold.

The firms that win in 2026 won't be the ones with the biggest spreadsheet of names. They'll be the ones with a lead engine that filters for intent, moves fast, documents everything, and keeps sales process aligned with compliance from first touch to funding.

Table of Contents

- The High-Stakes Game of MCA Lead Generation

- Your Lead Sourcing Blueprint Build vs Buy

- Separating Signal from Noise Qualifying High-Intent Leads

- The Compliant Conversion Playbook

- Building Your MCA Tech Stack for 2026

- Measuring for Profit The KPIs That Drive Growth

The High-Stakes Game of MCA Lead Generation

The biggest mistake in this space is treating merchant cash advance leads like a commodity.

That mindset ignores what's changed. Brokers that still rely on low-cost, poorly vetted lead sources are running straight into a quality problem and a compliance problem at the same time. Existing industry content often treats lead generation as a static buying exercise, but the more urgent issue is building a sustainable system that doesn't expose your shop to reputational damage or enforcement pressure. The warning is clear in the DFPI advisory to small businesses about merchant cash advances, which is also cited for the claim that 60% of new MCA failures are tied to compliance violations rather than credit risk.

A lot of shops still confuse activity with traction. They buy a batch of leads, hand them to reps, and hope persistence fixes everything. It usually doesn't. Bad data creates bad outreach. Bad outreach creates complaints, opt-outs, and wasted time. Then owners think they have a close-rate problem when the problem is sourcing.

Cheap leads usually create expensive problems

A lead isn't valuable because it's inexpensive. It's valuable because it's reachable, fundable, and sourced in a way your business can defend.

That changes how you evaluate every channel. If a vendor can't explain how consent was captured, how data was verified, or how old the record is, you're not buying opportunity. You're buying cleanup work for sales, operations, and legal.

Practical rule: If the lead source can't survive a basic audit of origin, consent, and data fields, don't load it into your CRM.

There's also a merchant-side shift that too many funding companies ignore. Business owners looking at fast capital products are no longer just asking, “Can you fund me?” They're asking whether the provider is transparent, responsive, and credible. That's one reason broad education around products like short-term business financing matters. Merchants compare options more carefully than many brokers assume.

Winning now means building a system

The 2026 playbook is different. You need:

- Clear sourcing standards so reps aren't calling junk.

- Fast qualification so urgency becomes an advantage.

- Compliant communication so your sales floor doesn't create avoidable exposure.

- Measurement discipline so you know which channels produce funded deals, not just conversations.

The old buy-only model breaks because it outsources too much of the part that matters most. The winning model combines channel strategy, qualification logic, speed to contact, and compliance controls into one operating system.

Your Lead Sourcing Blueprint Build vs Buy

You've got three ways to source merchant cash advance leads. Build your own pipeline, buy leads directly, or work through a broker or outsourced partner. None is automatically best. Each fits a different stage, team structure, and risk tolerance.

The mistake is picking one based on price alone. The right question is simpler. Which model gives your team the best mix of speed, control, and fit for the merchants you fund?

Three ways to fill the pipeline

Build in-house works best when you want control over message, targeting, and brand reputation. This usually means a lender-focused SEO program, paid search campaigns tied to high-intent landing pages, form routing, CRM automation, and a sales team that can respond immediately. It's slower to set up, but you own the asset. Over time, it tends to create cleaner data and a more consistent story from ad click to funding call.

Buy direct from lead vendors works when you need volume now. This is the fastest route to getting reps on the phones, but it's also where many shops get sloppy. Vendor-bought leads can range from fresh, exclusive inquiries to recycled records that have been hit by half the industry. If you buy, ask hard questions about source channel, age, exclusivity, required data fields, and whether the lead came in through a speed-driven inquiry flow.

That last point matters because high-intent MCA leads don't behave like traditional loan shoppers. They're driven by urgency and need for immediate working capital, not shopping for the best long-term rate. The analysis of MCA lead intent and live inquiry behavior frames this well, noting that ideal leads often show monthly revenue between $50k and $500k, need funding in less than 48 hours, and frequently come through live inquiry platforms where speed is the primary KPI.

Use a lead broker or outsourced partner when your team is strong at sales but weak at top-of-funnel execution. This model can help if you need campaign management, vendor oversight, intake handling, or appointment-setting support without building a full internal marketing department. If your operation is lean, it can make sense to outsource your lead generation rather than force underwriters or closers to manage acquisition channels they don't have time to optimize.

A good sourcing model doesn't just deliver names. It delivers leads in a format your sales team can work within minutes.

A practical decision table

Here's the side-by-side view operators use.

| Model | Cost Per Lead | Lead Quality | Speed to Implement | Scalability |

|---|---|---|---|---|

| Build in-house | Higher upfront, more controllable over time | Highest control if forms and targeting are strong | Slower | Strong if systems are in place |

| Buy from vendors | Varies by freshness and exclusivity | Can be excellent or terrible, depends on vetting | Fast | Strong if vendor quality holds |

| Brokered or outsourced | Typically blended into service structure | Good when partner understands MCA qualification | Medium | Strong if reporting and handoff are tight |

A few trade-offs matter more than many realize:

- If you need immediate conversations, bought or brokered leads are usually faster.

- If you care about message control, in-house wins.

- If your reps can't handle mixed lead quality, don't buy broad volumes.

- If compliance oversight is loose, avoid any source you can't document clearly.

The build-versus-buy rule that actually works

Early-stage shops often need a hybrid. They buy enough flow to keep reps productive while they build owned channels in the background. Mature shops usually move the other direction. They rely less on random vendor inventory and more on sources they can control, audit, and improve.

That's the blueprint. Don't choose based on ideology. Choose based on your team's ability to contact quickly, qualify accurately, and convert without creating unnecessary risk.

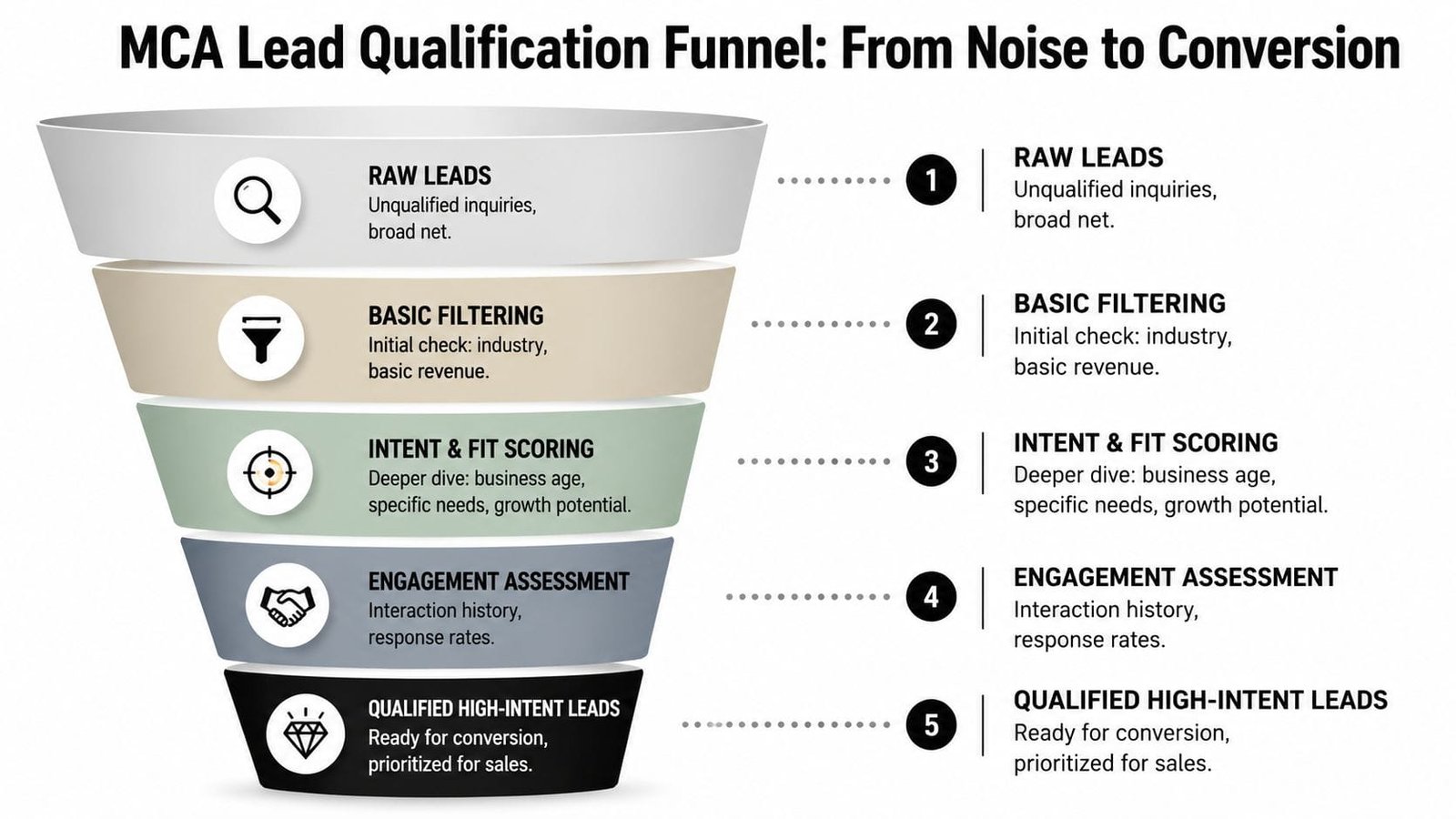

Separating Signal from Noise Qualifying High-Intent Leads

Buying more leads does not fix a weak pipeline. Tighter qualification does.

A lot of MCA shops blame volume, seasonality, or vendor quality when the actual problem sits on the sales floor. Reps are burning prime call blocks on merchants with no deposit strength, no urgency, no owner contact, or no clear use of proceeds. In 2026, that is not just inefficient. It creates compliance exposure because every extra touch on a bad record increases the chance of a sloppy script, a consent problem, or a documentation gap.

Four required checks before a lead hits the queue

Good qualification starts with gatekeeping, not optimism. The guide to generating MCA leads points to four baseline screens: the business should have 6 to 12 months in operation, show consistent monthly revenue of at least $10,000, have a clear purpose for the funds, and involve direct contact with the owner or decision-maker.

Treat those as pass-fail checks. Do not turn them into soft positives inside a scoring model. If one is missing, the file stays in verification or gets recycled.

Here is how experienced funders read those checks in practice:

- Business maturity means enough operating history to support underwriting and reduce first-month fallout.

- Revenue consistency means the deposits match the story. Stated revenue without bank activity is noise.

- Use of funds shows whether the request is tied to a real business need such as payroll, inventory, repairs, or a short cash gap.

- Decision-maker access determines whether the file can move at the pace MCA requires.

A lead that misses one of those checks can still become workable later. It should not get first-priority rep time today.

Close rates improve when reps stop treating every inbound form as a live funding opportunity.

Product fit matters here too. Some merchants want speed but are better served by another structure, and your reps should be able to explain the difference between short-term loans, MCA, and invoice factoring for quick capital without forcing every inquiry into the same box.

Before going deeper, watch how a practical qualification flow works in the field:

A simple scoring model that sales teams use

Once a lead clears the gate, the next job is priority. Reps need to know who gets called now, who gets a same-day follow-up, and who goes into recycle.

That is where lead scoring earns its keep. If your team is refining intake and handoff rules, this overview of optimizing lead qualification processes is useful because it explains how teams separate early-stage interest from true sales readiness.

Keep the model simple enough that reps and managers use it the same way every day:

- Urgency comes first. A merchant facing payroll, inventory deadlines, or a near-term cash crunch deserves immediate outreach.

- Deposit stability comes next. Clean, repeatable cash flow beats one strong month with no pattern behind it.

- Use-of-funds clarity raises confidence. “Need working capital” is weak. “Need to restock ahead of a seasonal run” is far easier to underwrite and sell.

- Owner responsiveness changes the odds. Fast replies, completed docs, and reachable contacts usually point to real intent.

- Data completeness affects risk. Missing phone numbers, mismatched business details, or vague application fields lower priority fast.

Use score bands to drive action, not just reporting:

| Score band | Meaning | Sales action |

|---|---|---|

| High | Fundable, urgent, reachable | Immediate rep follow-up |

| Medium | Potential fit, needs verification | Same-day nurture and document request |

| Low | Weak fit or incomplete file | Recycle, remarket, or disqualify |

One warning from the field. Shops that score on revenue alone usually clog their pipeline with files that look big but do not close. The better approach is to score for fundability, timing, responsiveness, and document readiness together. That is how you build a lead engine that scales without turning into a compliance mess.

The Compliant Conversion Playbook

Converting merchant cash advance leads is where a lot of shops create their own losses.

Not because reps can't sell. Because they improvise. They overspeak, promise too much, text too aggressively, or skip basic disclosure habits. Then management has to unwind complaints, scrub records, and retrain people who should've had tighter scripts from the start.

How to open the conversation without creating risk

A good opening call does three jobs at once. It confirms identity, establishes need, and keeps the rep from making claims that underwriting hasn't approved.

A clean first-touch script sounds like this:

“Hi, this is [name] calling about your business funding inquiry. I want to make sure I'm speaking with the owner or the person who handles financing. If that's you, I'd like to confirm a few business details and see whether there's a fit for fast working capital.”

That script works because it's controlled. It doesn't guarantee approval. It doesn't imply terms. It doesn't force urgency with fake scarcity. It starts by verifying authority and permission to continue.

From there, the rep should move through a short sequence:

- Confirm authority by asking whether the contact is the owner or financial decision-maker.

- Confirm business basics including time in business, average monthly deposits, and business purpose for funds.

- Clarify timing with a direct question about when capital is needed.

- Set expectations by explaining that any offer depends on review of submitted information.

The tone matters. MCA merchants often need speed, but speed doesn't require pressure. Reps who sound calm and precise usually outperform reps who sound desperate to close.

What compliant follow-up looks like

The safest sales process is the one that's documented before a complaint ever happens.

Every shop should have written rules for calls, SMS, email, disclosures, consent handling, and record retention. That's especially true when you're dealing with contact data and application information that includes sensitive business details. Teams reviewing their workflows should pay attention to resources on avoiding PII leaks and penalties, because the risk isn't only in what you say to a merchant. It's also in how you store, route, and expose their information inside your stack.

Here's the outreach structure that tends to hold up best:

- Phone first for fresh leads. A live conversation lets you verify details quickly and hear whether the request is real.

- Email for recap and documentation. Keep it factual. Summarize the next step and list what you need.

- SMS only under clear internal rules. Text can move deals faster, but only if your process for consent, timing, and opt-out handling is tight.

Sales discipline: Never let a rep promise pricing, terms, or approval timing that hasn't been cleared by your actual process.

A compliant email follow-up is straightforward. It confirms that the merchant requested information, restates what documents are needed, and avoids language that sounds like a guaranteed offer. If your templates use words like “approved,” “lowest rate,” or “instant funding” before underwriting review, rewrite them.

One more hard truth. Compliance doesn't slow conversion. Sloppy process does. Tight process usually helps the close because merchants trust shops that communicate clearly, answer directly, and don't oversell the product.

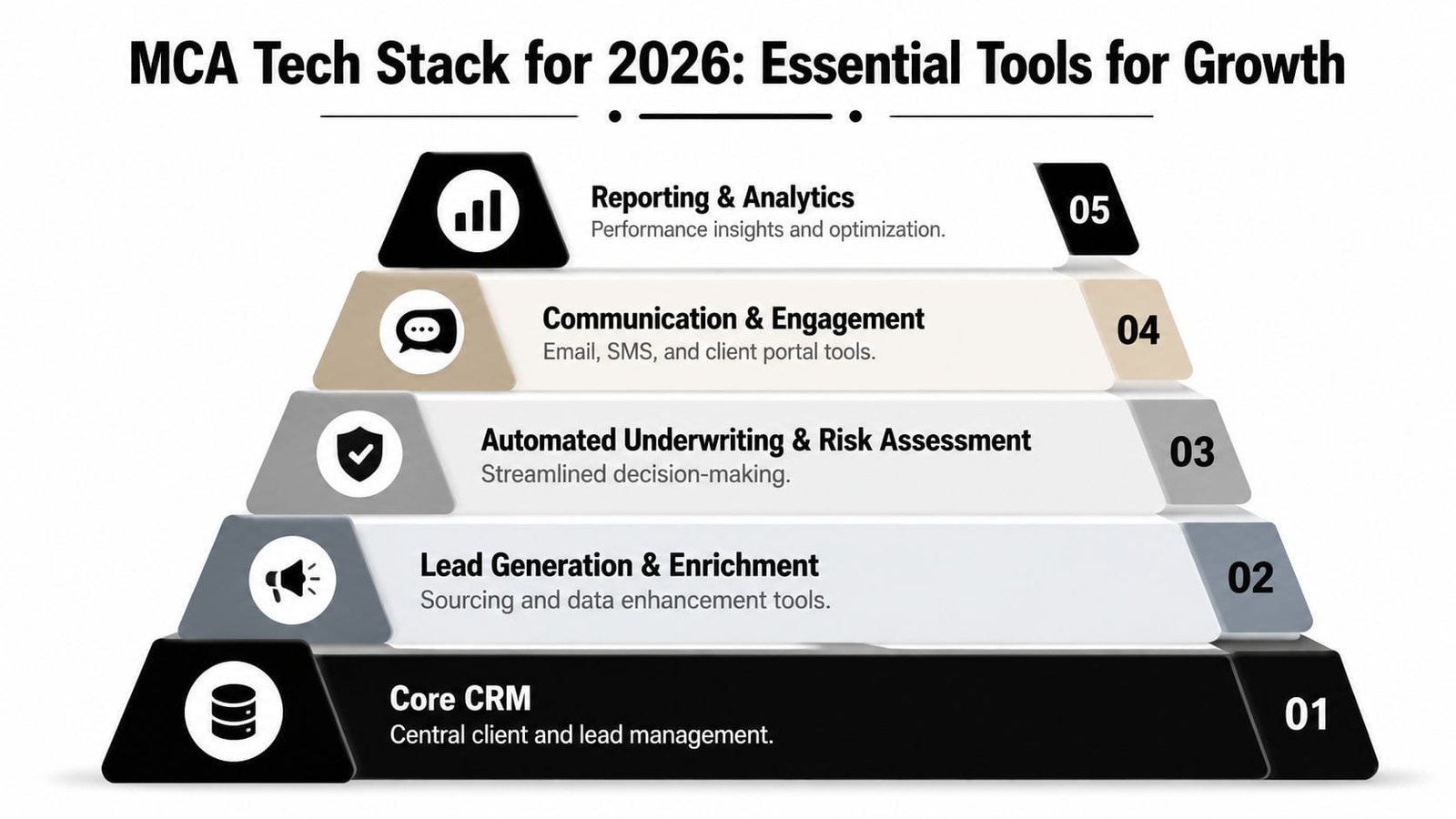

Building Your MCA Tech Stack for 2026

Most MCA teams don't need more software. They need a stack that matches how deals move.

A bloated stack creates duplicate records, missed handoffs, and sales reps working from partial information. A smart stack does the opposite. It gives marketing, sales, underwriting, and operations one version of the file and one history of the merchant conversation.

The core systems

Start with the CRM. This is the center of the operation. It should track lead source, contact attempts, qualification notes, document status, underwriting updates, and funded outcome. If your reps still keep critical notes in personal spreadsheets, the CRM isn't configured correctly.

Add a dialer and communication layer next. Reps need click-to-call, call recording where lawful and appropriate, SMS controls, and email logging tied back to the merchant record. Speed matters in MCA, but so does context. Every contact attempt should be visible in one place.

Then add marketing automation. This handles form routing, auto-response logic, nurture sequences for unready merchants, and source tagging. Good automation doesn't replace reps. It makes sure reps only spend time where human contact adds value.

You also need document collection and e-signature tools. If a merchant wants capital quickly, your intake process can't rely on scattered attachments and manual chasing. The handoff from application to document request to signed agreement should be simple and easy to audit.

How the stack should work together

Think of the system as one operating loop:

- Lead enters through a landing page, live transfer, referral form, or imported source.

- CRM tags the source and triggers the right intake workflow.

- Sales engages with call, email, or text based on channel and status.

- Documents are requested through a secure workflow, not ad hoc messages.

- Underwriting reviews a complete file, not a pieced-together thread.

- Operations tracks outcome so marketing can see which sources fund.

That last step gets missed all the time. Shops invest in acquisition tools but fail to connect funded outcomes back to source quality. Then they keep spending on channels that create noisy pipelines and slow underwriting.

Use fewer tools, but make sure each one owns a real job in the lead lifecycle.

If you're reviewing systems that support growth more broadly, this roundup of small business essential tech tools is a useful reference point for how operators evaluate software by workflow, not by hype.

The 2026 stack doesn't have to be expensive. It has to be integrated, visible, and disciplined enough that no lead disappears between first contact and final decision.

Measuring for Profit The KPIs That Drive Growth

A lot of MCA shops still score performance by activity. That is how teams stay busy and lose money at the same time.

Lead count, dial count, and app count have their place, but they are weak management metrics on their own. The numbers that matter are the ones tied to funded revenue, acquisition cost, margin, and repayment quality. If a source fills the CRM but burns rep time, creates document drag, or produces merchants that never clear underwriting, it is not helping growth. It is taxing the operation.

As noted earlier, the market is big enough to punish sloppy attribution and reward disciplined operators. In 2026, that gap gets wider because compliance costs are rising, state scrutiny is rising, and low-quality purchased traffic is getting harder to convert profitably. Teams that still buy leads in bulk and judge success by volume usually find out too late that their economics broke upstream.

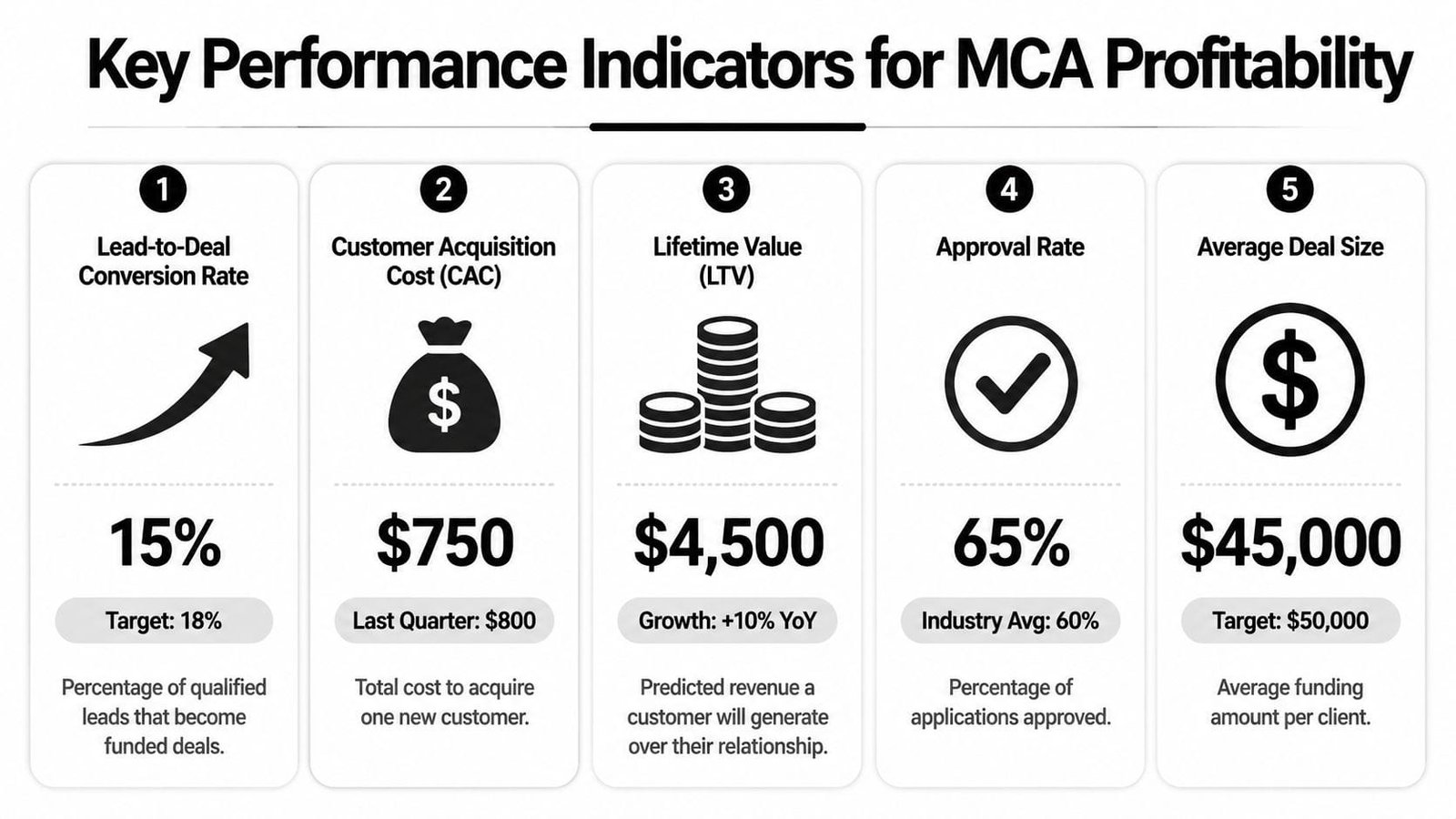

The numbers that matter

Start with a KPI set that connects marketing, sales, underwriting, and operations:

- Cost per lead shows what you paid for raw inbound opportunity.

- Cost per funded deal shows what it took to produce booked business.

- Funded deal ratio shows how well your sourcing and qualification process are aligned.

- Average funded amount shows whether your channels are bringing in the merchant profile you want.

- Speed to contact shows whether your intake operation can capitalize on intent before it cools.

- Approval-to-funding rate shows whether files are dying in sales, docs, or closing.

- Source-level default or performance trend shows whether funded volume is turning into durable revenue.

That last one gets missed. A channel can look great on CPL and still be expensive if it sends files that force exceptions, create heavy collection work, or underperform after funding. Sustainable growth in MCA comes from tracking the full path from lead source to portfolio result, not just from lead source to signed contract.

How operators use KPIs to fix bottlenecks

A metric only matters if it changes a decision.

If CPL is low and the funded deal ratio is weak, the source is probably too loose. Tighten filters, change the offer language, or cut the vendor. If contact rate is strong but approvals are weak, reps are booking conversations with merchants who never met baseline criteria. Fix qualification early. If approvals are healthy but files stall before funding, the problem usually sits in docs, follow-up discipline, or closing friction.

Here is a practical diagnostic table:

| KPI pattern | Likely issue | First move |

|---|---|---|

| Low CPL, weak funded ratio | Bad lead quality | Tighten source filters and intake fields |

| Strong contact rate, weak approvals | Poor qualification | Retrain reps on gate checks |

| Good approvals, weak closes | Sales process friction | Review scripts, follow-up, and document flow |

| Healthy closes, low average deal size | Targeting drift | Narrow channel targeting and messaging |

Review these by source, by rep, and by stage. Blended dashboards hide bad economics. One traffic source may produce cheap names but consume twice the talk time, twice the follow-up, and far more dead files than a referral channel that costs more upfront.

I also separate vanity volume from usable volume. Usable volume means the merchant is reachable, meets baseline requirements, submits documents, and has a real chance to fund under current credit policy. That is the number to build around.

The shops that keep margin in 2026 are not the ones buying the most leads. They are the ones tracing every funded file back to source quality, conversion path, compliance risk, and downstream performance, then cutting anything that adds noise without adding profit.

If you're weighing fast capital options or want a clearer path to funding, Business Loan Warrior gives business owners a practical way to explore suitable financing through one no-fee application, with transparent options, secure account connectivity, and support across products including merchant cash advances, short-term financing, lines of credit, equipment loans, and more.