The most common advice around a line of credit no credit check is also the most misleading: “If they don't check credit, it's easier.” Sometimes it is easier to qualify. It is rarely simpler, and it is almost never cheaper.

What changes is the type of scrutiny. Instead of pulling a traditional credit report, many lenders dig into your bank activity, income deposits, and account behavior. For a small business owner under cash pressure, that can feel like a lifeline. It can also become an expensive trap if you mistake “no credit check” for “low risk.”

If you're trying to cover payroll, inventory, repairs, or a short-term cash gap, speed matters. So does clarity. Before you chase fast money, it helps to understand when startup financing with no credit check is a workable bridge and when it becomes the wrong kind of emergency solution.

Table of Contents

- The Truth About No Credit Check Funding

- How Lenders Approve You Without a FICO Score

- Understanding the Risks and Red Flags

- How These Revolving Accounts Actually Work

- Smarter Alternatives for Business Funding

- Your Action Plan to Get Funded Safely and Quickly

The Truth About No Credit Check Funding

A no-credit-check credit line isn't the absence of underwriting. It's a shift in underwriting.

That distinction matters because many owners search this term when they've already been turned down by a bank, don't want a hard pull, or need money faster than a traditional lender can move. In that moment, “no credit check” sounds like relief. In practice, it often means the lender stops asking, “How have you handled debt in the past?” and starts asking, “What can we see in your bank account right now?”

That can help owners with bruised credit or thin files. It can also feel more invasive than a standard credit review because the lender may want direct visibility into deposits, balances, and transaction patterns.

Practical rule: If a lender says “no credit check,” assume they still need a way to measure risk. Your cash flow becomes the report card.

For business owners, that trade-off can be reasonable when the need is real and short term. It gets dangerous when the loan is being used to cover a structural problem, like consistently weak margins or recurring payroll shortfalls. A fast credit line can patch a leak. It can't fix a sinking boat.

The key question isn't whether you can get approved. It's whether the terms leave your business better off after the urgency passes. If the answer is unclear, slow down long enough to read the fees, repayment triggers, and account access requirements.

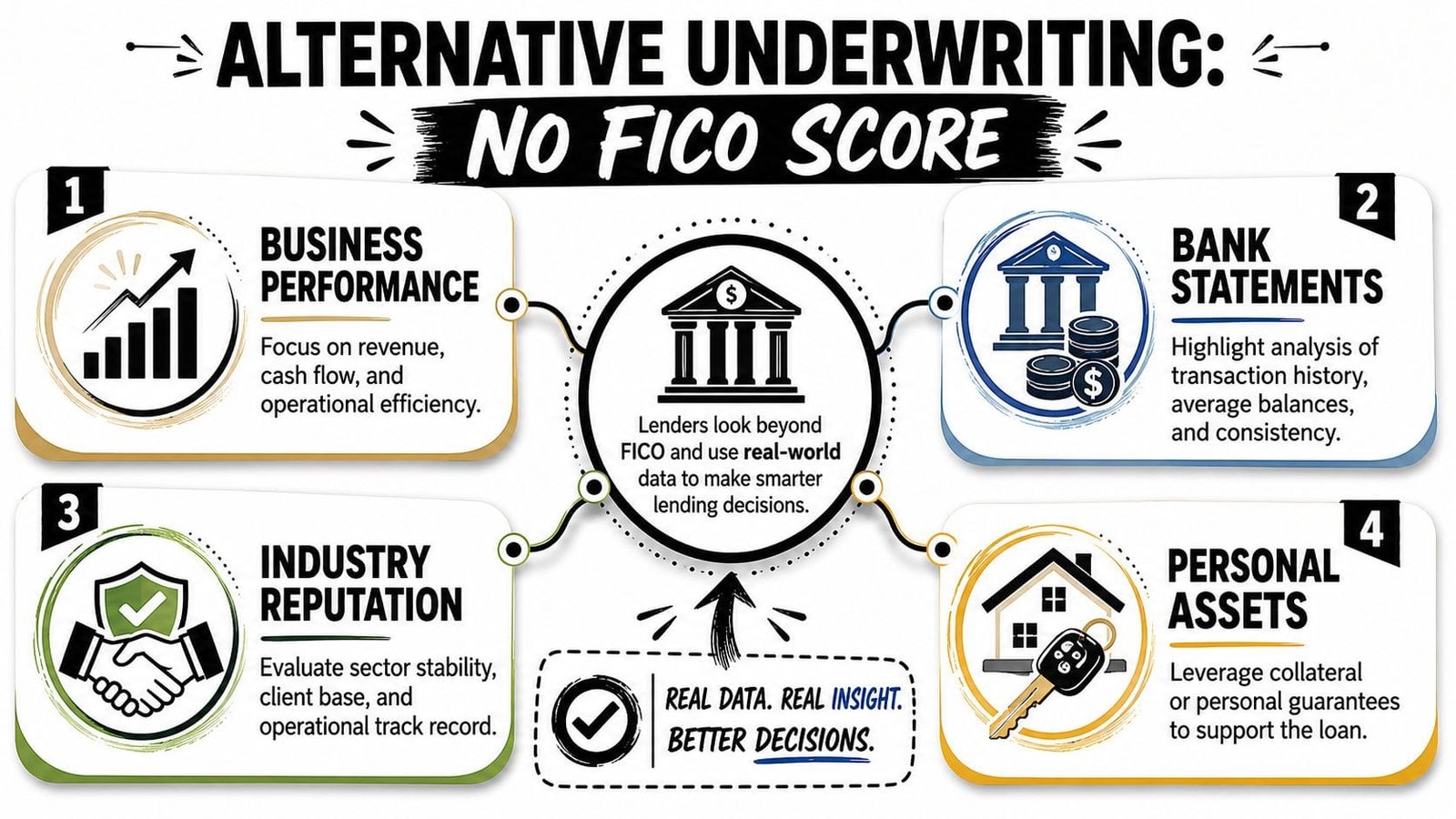

How Lenders Approve You Without a FICO Score

A traditional credit score works like a report card. It summarizes past borrowing behavior into one number. Alternative underwriting works more like a diary. It looks at what your money is doing day by day.

It is a different filter, not no filter

A line of credit with no credit check typically doesn't require a FICO score of 670 or higher. Instead, lenders may use bank transaction history, employment verification, and direct-deposit income data. LendingTree's overview notes examples such as Possible Finance requiring a Plaid-compatible checking account with at least 3 months of positive balance and recent income deposits, while OppLoans requires minimum annual income of $18,000 and a valid checking account, as described in LendingTree's guide to no-credit-check personal loans.

That should sound familiar to anyone who has worked with newer business lenders. They often want connected bank data because it helps them evaluate cash flow in real time instead of relying only on older bureau data.

For borrowers, this can be useful. A past credit issue doesn't always reflect current operating strength. If your business deposits are steady and your account behavior is clean, that may carry more weight than an old score.

What lenders usually look for

In practice, lenders using this model often focus on patterns like:

- Deposit consistency: Are sales or receivables landing regularly, or is cash flow erratic?

- Balance behavior: Do you maintain a cushion, or does the account repeatedly run near empty?

- Payment strain: Are there signs that current obligations already stretch the business?

- Account history: Many lenders want enough transaction history to see habits, not just one strong week.

That last point matters. A lender that reviews connected banking data isn't just checking revenue. They're checking stability.

If you want a useful comparison point, this is similar in spirit to asset-based or collateral-driven lending. The lens changes depending on the product. A borrower reviewing a hard money loan qualification guide will notice the same broad theme: when a lender relaxes one standard, it tightens attention somewhere else.

A soft inquiry may spare your credit file, but it doesn't spare you from scrutiny.

For a business owner, the practical takeaway is simple. Clean up your operating account before you apply. Reduce avoidable overdrafts, separate business and personal spending, and make sure deposits tell a coherent story. When lenders underwrite from bank activity, messy records weaken your case even if revenue is decent.

Understanding the Risks and Red Flags

The speed of no-check funding is real. So is the cost.

Why the price gets so steep

Lines of credit without a credit check typically carry APRs of 400% or more, and some payday loans can exceed 400% APR. By contrast, federal credit unions offer Payday Alternative Loans with a 28% interest cap, which LendingTree highlights in its discussion of safer borrowing options.

That gap tells you exactly how the market prices risk. When a lender skips a hard credit review and approves weaker borrowers faster, it usually protects itself with much higher pricing, tighter terms, and more fees.

For a small business, that creates a hard math problem. Expensive capital only works when it solves a problem with a fast, reliable payoff. A short inventory buy that turns quickly might justify higher-cost funding. Covering ordinary operating losses usually won't.

Red flags checklist

Use this list before signing anything. If you see several of these at once, step back.

- Pressure to sign today: A lender that won't give you time to review terms is counting on urgency.

- Vague fee language: If draw fees, maintenance charges, or payoff rules are hard to pin down, the actual cost is probably higher than the headline suggests.

- Confusing contract wording: If you need a translator to understand repayment mechanics, the agreement is too opaque.

- Account access without context: Some lenders want broad bank access. Ask what they can view, what they can debit, and when.

- Repayment that ignores cash timing: Daily or aggressive withdrawals can punish businesses with uneven receivables.

- No clear total-cost explanation: If the lender can't explain what repayment looks like in plain English, keep shopping.

Owners who've never had to decode lending paperwork often benefit from learning how consumer agreements hide obligations in plain language. This primer on how to understand credit card agreements is useful because the reading habit is the same. Slow down, isolate the fees, and identify what triggers extra cost.

A second smart move is to review your broader credit profile before applying for any new financing. If there are reporting issues you can address, resources on tradelines and credit-building context can help you understand how lenders may view your file over time.

High-cost borrowing should buy time for a fix, not become the fix.

How These Revolving Accounts Actually Work

Many borrowers hear “line of credit” and think “loan.” That's close, but not close enough.

A line of credit is a revolving account. You're approved for a limit, draw only what you need, repay, and may be able to draw again. It behaves more like a reusable tool than a one-time lump sum.

The two phases that matter

No-credit-check lines of credit are generally unsecured and may come with a draw period of up to 5 years, when borrowers often make interest-only payments, followed by a repayment period of up to 10 years with full amortization, according to NerdWallet's explanation of personal lines of credit.

That structure matters because the payment can feel manageable at first and then rise later when principal repayment begins. Owners get into trouble when they budget around the early payment and forget the account will eventually demand more.

A good business line should match the cash cycle it supports. If you use it for inventory, receivables gaps, or seasonal swings, a revolving structure can make sense. If you need a fixed amount for a single project, an installment loan is often cleaner.

Where borrowers get surprised

The biggest surprises usually come from fees and variable pricing. These accounts often carry origination fees, annual maintenance fees, and transaction costs. Monthly cost can also move if the rate is variable.

That means your forecasting has to be tighter than with a plain fixed-rate term loan. Don't just ask, “What's the limit?” Ask:

- What do I pay to open it?

- What do I pay each year to keep it?

- What does each draw cost me?

- Can the rate change while I'm carrying a balance?

If you need a clearer grounding in business-use mechanics, this guide on how a line of credit works for a business is worth reviewing before you compare offers. It helps separate flexible working capital from expensive misuse.

Smarter Alternatives for Business Funding

The problem with many no-check products isn't alternative data. The problem is how some lenders price and structure the deal after using that data.

Why alternative data is not the problem

More than 45 million Americans are classified as credit unserved or underserved. The same TransUnion research also notes that alternative credit scores based on shopping behavior can increase approval rates for people without credit history from 15.6% to 47.8%, as covered in TransUnion's research on credit inclusion.

That's the important distinction. Non-traditional data can expand access. It doesn't have to lead to predatory terms.

For small businesses, this is already common sense. If a lender can see stable deposits, healthy receivables, and disciplined account management, that's useful information. The better lenders use it to make a sharper decision. The worse lenders use it to justify expensive money.

Better underwriting should widen access and improve fit. It shouldn't become an excuse for punishing terms.

Funding options at a glance

| Feature | Traditional Bank LOC | “No Credit Check” LOC | Fintech Lender (e.g., Business Loan Warrior) |

|---|---|---|---|

| Approval focus | Strong credit history, financial statements | Bank activity and alternative checks, often with less emphasis on traditional credit | Bank data, revenue trends, and broader risk review |

| Speed | Often slower | Often fast | Usually faster than banks, with streamlined review |

| Cost profile | Usually lower if you qualify | Often the highest-cost option | Varies by borrower and product, but typically structured to be more transparent |

| Best use case | Established businesses with strong profiles | Emergency-only situations when other options are closed | Businesses needing practical access without relying only on a traditional score |

| Main risk | Tough approval standards | Very high pricing, fees, and rigid repayment | Quality varies by platform, so offer comparison still matters |

That middle column is why many owners should pause before typing “line of credit no credit check” and clicking the first ad. Access alone doesn't equal suitability.

A more balanced approach is to look for lenders that use modern underwriting but still present terms clearly, offer soft-pull or no-hard-pull prequalification where available, and align repayment with business cash flow instead of forcing a one-size-fits-all structure.

Here's a useful explainer if your receivables are strong but your immediate cash position is tight. HireAccountants' invoice factoring insights can help you evaluate whether selling invoices is cleaner than taking on a costly revolving product.

Later in the process, it also helps to see how modern funding platforms present options visually and operationally.

When another structure fits better

A line of credit is strongest when the amount needed changes over time. If your need is fixed, another product may fit better.

Consider alternatives when:

- You know the exact amount needed: A term loan is often easier to price and budget.

- Your invoices are the bottleneck: Factoring or receivables financing may align better.

- You need equipment, not general cash: Equipment financing keeps the purpose and repayment tied together.

- You only need a bridge: Short-term funding can work if the exit is clear and near certain.

The right funding product should match the shape of the problem. That is more important than whether the lender advertises “no credit check.”

Your Action Plan to Get Funded Safely and Quickly

Urgency is where bad lending thrives. A short checklist protects you better than optimism.

A practical funding checklist

Define the exact use of funds.

Write down what the money is for before you apply. Inventory bridge, payroll gap, equipment repair, seasonal marketing push. If the need is vague, the borrowing decision will be vague too.Decide whether revolving credit is the right tool.

Use a line of credit for uneven or recurring needs. Use a fixed loan when the cost and timing are known up front.Gather clean bank records.

Since alternative underwriting often leans on bank data, make sure your statements reflect your business's activity. Separate personal spending if you haven't already. Clean records improve your options.Ask how the lender reviews you.

“No credit check” should trigger follow-up questions, not relief. Ask whether they use connected bank access, what account permissions they need, and whether they perform a soft or hard inquiry at any stage.Price the full cost, not just the payment.

Look beyond the minimum due. Focus on total fees, draw charges, annual costs, variable-rate exposure, and what happens if repayment stretches longer than expected.Stress-test repayment against a weak month.

Don't model repayment using your best month. Use a conservative month. If the payment still works, the offer is sturdier.Compare at least a few funding paths.

Even under pressure, compare. A business credit line, term loan, invoice-based option, or fintech platform may produce a better fit than the first “instant approval” lender you find.Read the debit and default language carefully.

Know when the lender can pull funds, what counts as default, and whether fees accelerate after a missed payment.Only borrow for a clear outcome.

Good debt should support a definable business purpose. If the money only delays an unresolved operating problem, borrowing won't help for long.Use prequalification where available.

A safer process gives you visibility before commitment. That lets you compare options without unnecessary damage to your credit profile.

If you remember one thing, remember this: a line of credit no credit check is not “free access” to capital. It is a financing product with a different screening method, a different risk model, and often a harsher price for getting the answer fast.

If you want to explore funding without rushing into a costly offer, Business Loan Warrior gives business owners a no-fee way to check options, review pre-approval without affecting credit, connect accounts securely, and compare practical paths to working capital with real human support.