Bridge financing is a short-term loan designed to cover a funding gap until longer-term capital is secured, and it's commonly structured with an initial maturity of one year or less or, in traditional forms, 6 to 24 months. In practice, it works like a temporary bridge: you use it to cross from where your cash is today to where your permanent financing, sale proceeds, or larger transaction will land.

You probably don't need a lecture on capital structure. You need to know whether bridge financing solves a real business problem without creating a worse one.

The usual moment looks like this. A supplier offers a rare inventory buy. A landlord wants proof of funds before locking a location. An acquisition is close, but the senior facility hasn't closed yet. Or you've got a growth plan that makes sense now, not after a slow underwriting cycle. The opportunity is real, but the cash arrives later than the deadline.

That's where bridge financing earns its name. It's a short-term loan built to span a specific gap until a defined, longer-term funding source takes over. Think of a temporary bridge over a river while the permanent road is still being built. You don't plan to live on the bridge. You plan to cross it, quickly, and get off.

This isn't a niche corner of finance. The global bridge financing market was valued at approximately USD 76.8 billion in 2023 and is projected to reach USD 158.3 billion by 2033, with a 7.5% CAGR from 2024 to 2033. Businesses use it because timing gaps are common, and waiting can be expensive in ways that don't show up neatly on a loan quote.

The critical question isn't what bridge financing means in a textbook. It's whether it fits your timing, your risk tolerance, and your exit plan.

Table of Contents

- Introduction Bridging the Gap to Your Next Big Opportunity

- Understanding the Mechanics of a Bridge Loan

- When to Use Bridge Financing Key Business Scenarios

- Decoding Bridge Loan Costs Terms and Fees

- The Strategic Benefits and Real Risks of Bridge Loans

- Your Step-by-Step Guide to Obtaining Bridge Financing

- Bridge Loans vs Other Funding The Right Tool for the Job

Introduction Bridging the Gap to Your Next Big Opportunity

A strong business can still hit a timing problem.

A distributor may have signed customers and healthy margins but need cash before receivables convert. A contractor may have equipment lined up and labor scheduled while a larger facility is still in final approval. An owner buying out a partner may have a sound long-term plan but need immediate funds to keep the transaction moving.

That's what bridge financing is for. It's a short-term loan designed to cover a financial gap until a long-term funding source is secured. The bridge analogy matters because it keeps the decision clear. This money is meant to get you across a defined gap, not become a permanent part of your capital stack.

The best use is specific, not vague

Bridge loans work best when the destination is visible. You know what event should repay the loan. That could be a refinance, sale proceeds, a closed financing round, incoming acquisition capital, or another committed source of funds.

They work poorly when owners use them to postpone a deeper problem. If the business doesn't know how it gets to stable cash flow, short-term debt can magnify the pressure instead of relieving it.

Practical rule: If you can't point to the likely repayment event in one sentence, you're probably not ready for bridge financing.

Why this matters to a small business owner

Owners often think of bridge loans as something only real estate developers or dealmakers use. That's too narrow. Small and midsize businesses use them for expansion, transactions, and short-duration working capital needs when speed matters more than headline cost.

The useful lens is strategic, not academic. Ask three things:

- What am I trying to protect? Ownership, timing, margin, or deal certainty.

- What am I waiting for? A refinance, sale, investor capital, or contractual inflow.

- What happens if that event slips? That answer determines whether the bridge is smart or dangerous.

Bridge financing can be a sharp tool. Used correctly, it buys time without giving up control. Used casually, it creates expensive urgency.

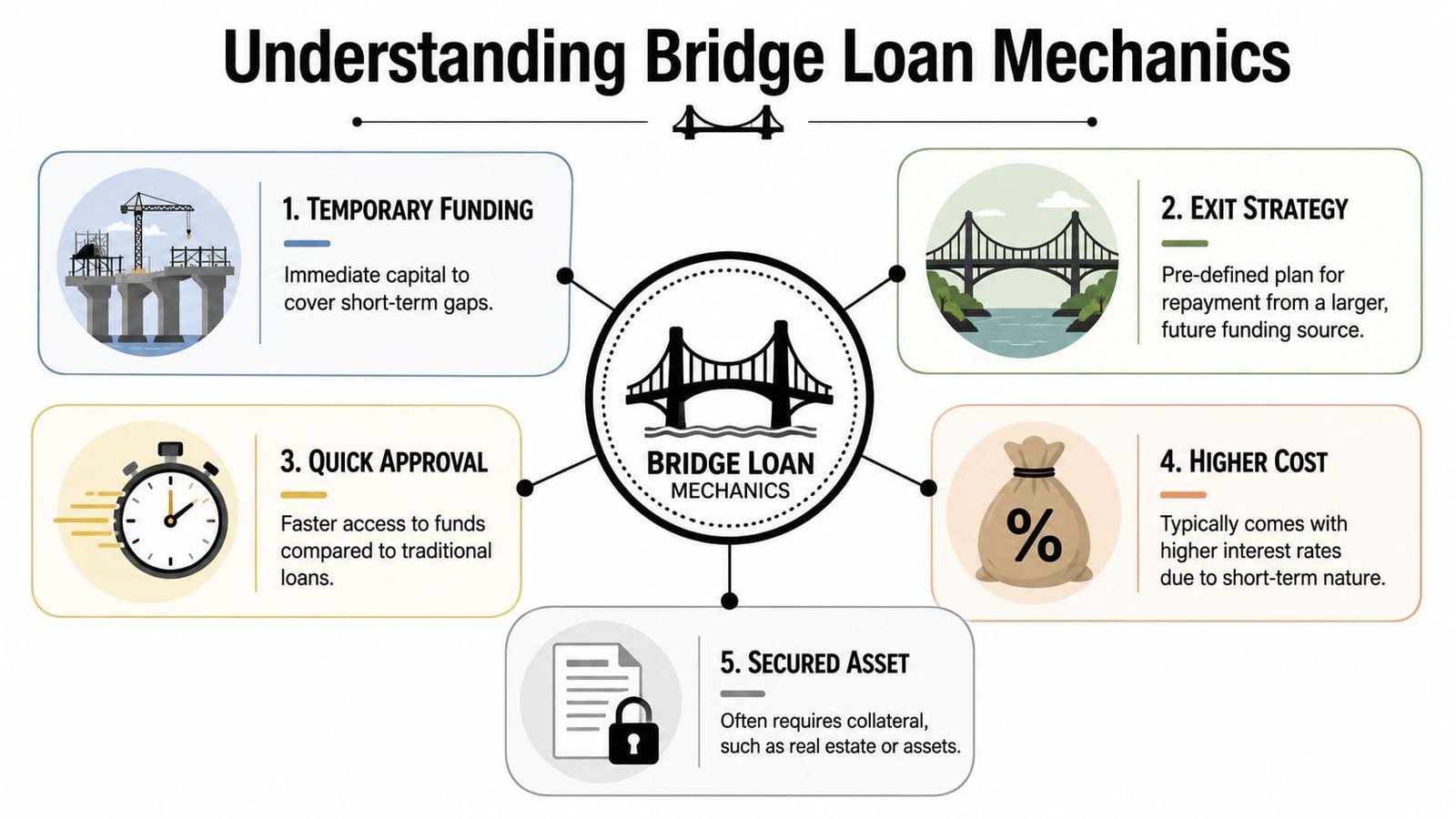

Understanding the Mechanics of a Bridge Loan

Bridge loans make more sense when you stop thinking about finance jargon and think about construction.

There's a gap in front of you. You need a structure that carries your business across it. And you need confidence that the road on the other side will indeed be there when you arrive.

The gap comes first

The first step is identifying the exact shortfall. Not “we need more flexibility.” Something tighter than that.

Examples include a down payment before a mortgage closes, acquisition funding before permanent debt is issued, or operating cash needed until a defined capital event lands. The gap has a purpose, a size, and a likely duration.

A workable bridge loan usually has these ingredients:

- A temporary need: The money covers a short interval, not a recurring weakness.

- A known trigger: There's a future event expected to replace the bridge.

- A lender comfort point: Assets, receivables, enterprise value, or deal structure support the risk.

- A backup plan: If timing slips, you know what happens next.

The loan is built around the exit

Bridge financing is often short-term by design. Revera Capital explains bridge financing as a short-term instrument typically structured with an initial maturity of one year or less, often used between the announcement of a major transaction and permanent financing, with pricing designed to push borrowers to refinance quickly.

That last part matters. Some bridge structures don't just charge for the use of money. They pressure the borrower to get out of the loan fast. If the borrower doesn't refinance by the end of the initial term, some agreements can extend into a longer-term instrument at a punitive “Cap” rate. In plain English, the bridge can become expensive permanent debt if the exit fails.

A bridge loan is less about borrowing money and more about buying time, under a contract that assumes you won't need much of it.

That's why experienced borrowers start with the exit, not the rate sheet. The loan itself can be structured in several ways, including traditional debt, convertible debt, or equity-linked forms. The right structure depends on what sits on the other side of the bridge.

For a business owner, the practical sequence looks like this:

- Define the timing gap. Be precise about what cash event you're waiting on.

- Match the loan structure to that event. A property refinance and a venture round are not the same.

- Document the repayment path. Lenders care less about your optimism than your evidence.

- Stress test the delay scenario. If the exit is late, know the cost before you sign.

When to Use Bridge Financing Key Business Scenarios

Bridge financing earns its keep when delay costs more than short-term borrowing. That doesn't mean every urgent need deserves one. It means the business case has to be tied to a specific outcome.

Commercial property before permanent financing closes

A business finds a location that fits operations, brand, and customer flow. The seller won't wait for a long conventional approval cycle. The company uses bridge financing to secure the property now, then pays off the bridge when the longer-term mortgage closes.

This works well when the property is central to the growth plan and the permanent loan is in motion, not just hoped for. It works badly when the buyer hasn't sorted out what permanent financing looks like.

Inventory and fulfillment when the order is bigger than your cash cushion

A retailer or wholesaler wins a large order that requires upfront inventory purchases, shipping commitments, and labor costs before customer payment arrives. A bridge loan can fund that short window so the company can fulfill the contract instead of watching the opportunity pass to a competitor.

The key is quality of demand. Confirmed purchase orders, repeat customer history, and realistic delivery timing make this much safer than borrowing against a vague sales forecast.

Don't use bridge capital to “test” demand. Use it when demand already exists and timing is the problem.

Deals and transitions that can't wait for slow money

A small company in acquisition talks may need cash for transaction expenses, integration costs, or payroll continuity between signing and permanent funding. The same logic applies to partner buyouts, recapitalizations, or a temporary mismatch between a strategic transaction and long-term capital.

These are classic bridge situations because the business isn't borrowing to solve ordinary operations. It's borrowing to keep a valuable transition from stalling.

A few situations where bridge financing can fit:

- A contractor mobilizing for a major project: Funds cover materials, crews, or equipment deposits before milestone payments begin.

- A founder awaiting a committed financing round: Cash preserves momentum in product, hiring, or customer delivery while legal closing finishes.

- A business managing a merger transition: The bridge supports working capital while the larger capital structure settles.

- An owner moving on a narrow-timeframe asset purchase: Timing, not long-term affordability, is the core issue.

What doesn't fit? Chronic payroll shortages, inconsistent margins, or using short-term debt to avoid making a hard operating decision. If the hole keeps reopening, the bridge won't fix the road.

Decoding Bridge Loan Costs Terms and Fees

Bridge financing is useful because it's fast and flexible. It's expensive for the same reasons.

If you're asking what is bridge financing from a cost perspective, the honest answer is this: it's rarely just an interest rate. It's a package of term, fees, repayment pressure, and sometimes equity-related economics.

What the term sheet usually tells you

University Lab Partners notes that traditional bridge loans typically carry maturity terms of 6 to 24 months, fixed interest rates ranging from 13% to 16%, and origination fees of 2% to 5%. Those ranges alone tell you this isn't cheap capital.

That same source also notes that bridge loans are often structured as convertible debt, equity, or traditional debt, and may include warrant coverage of 0.5% to 2% of fully diluted shares. For an owner, that means the cost can include more than cash interest. In some cases, the lender may also get upside if the business performs well.

Here's the practical breakdown:

| Cost item | What it means in plain English | Why it matters |

|---|---|---|

| Interest rate | The stated price of borrowing | High short-term pricing can still make sense if the opportunity is time-sensitive |

| Origination fee | Upfront setup cost paid to close the loan | This changes the true cost immediately |

| Maturity term | How long you have before repayment is due | Short windows create discipline, but also pressure |

| Convertible feature | Debt may convert to equity in a future event | Useful in some venture situations, sensitive for owners focused on control |

| Warrant coverage | Lender may receive a small equity upside | Easy to overlook, important if valuation rises |

What business owners often miss

The biggest mistake is comparing offers on rate alone. A loan with a slightly lower stated rate can still be worse if the fee stack is heavier, the maturity is tighter, or the repayment terms are less forgiving.

Another miss is failing to calculate total borrowing cost under the most likely repayment date, not the ideal one. If you want a cleaner framework for that math, this guide on how to calculate the real cost of a small business loan without the headache is worth reviewing before you sign anything.

Important: The headline rate tells you the price of money. The term sheet tells you the price of uncertainty.

Ask lenders direct questions. Is interest paid monthly or accrued? Is there a balloon payment? Are there extension fees? What happens if the expected refinance slips? Those answers matter more than polished marketing language.

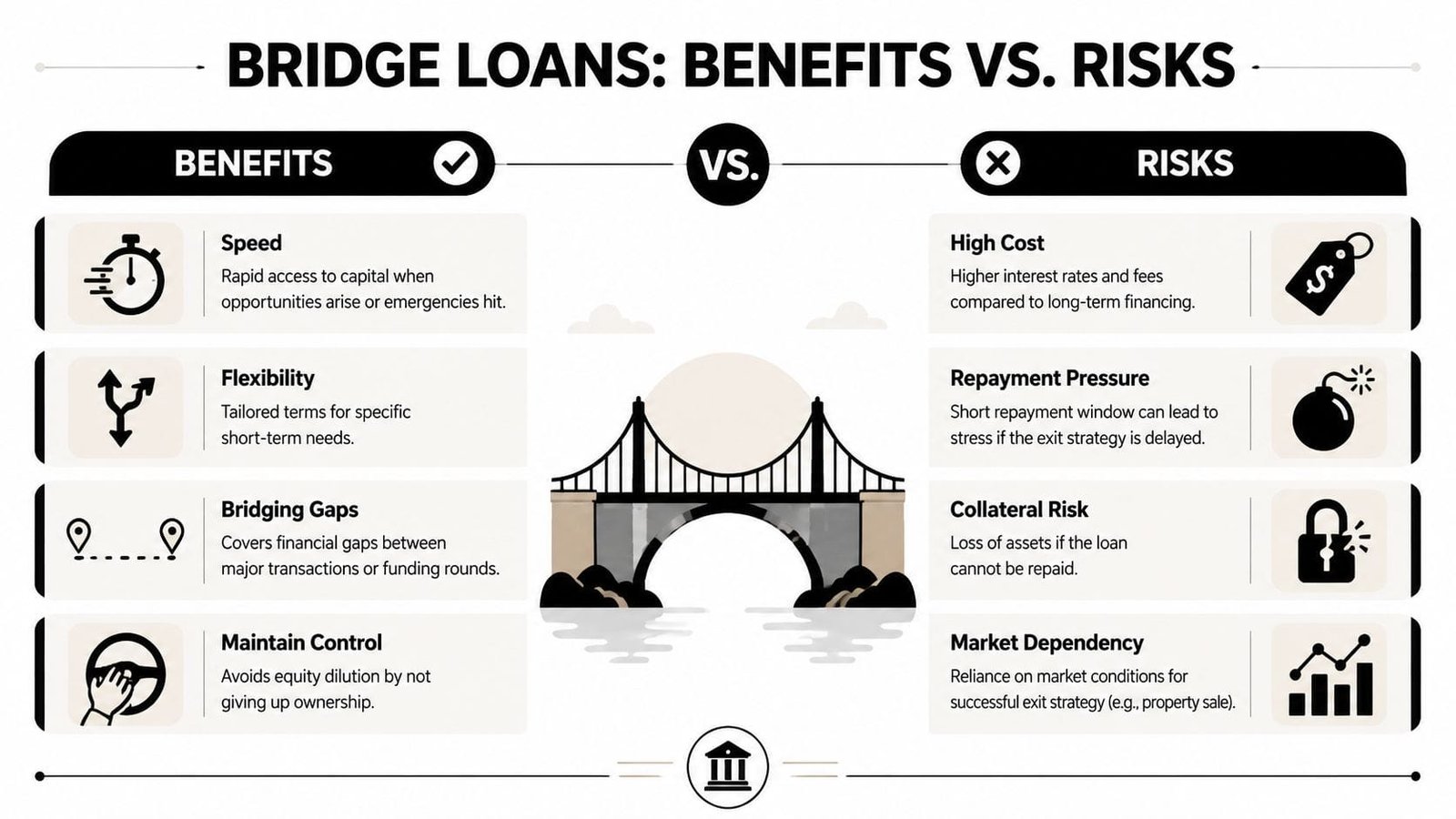

The Strategic Benefits and Real Risks of Bridge Loans

Bridge loans can be excellent capital. They can also be unforgiving.

The difference usually comes down to whether the owner is using them intentionally, with a defined objective and a believable exit, or using them out of pressure and hope.

For a quick visual of that trade-off, this summary is useful.

Why owners use bridge loans on purpose

The strongest benefit is timing control. You can move on an opportunity while slower capital catches up. In business, that often means preserving a deal, securing inventory, protecting a location, or maintaining bargaining power in a negotiation.

There's also a strategic ownership angle that many owners underestimate. The U.S. Chamber article notes that 34% of small business owners consider bridge financing specifically to protect valuation and avoid premature equity dilution. That's not a trivial point. Giving up equity because cash is late is often far more expensive than using short-term debt well.

Some owners benefit because bridge capital is purpose-built. It can be aligned to a transaction or a narrow growth window rather than forced into the box of a conventional long-term facility.

A short explainer can help frame the trade-offs before you make a decision.

Where bridge loans go wrong

The obvious risk is cost. Short-term money priced for urgency will usually cost more than conventional debt.

The more serious risk is failed repayment timing. If the refinance, sale, or capital event slips, the bridge doesn't politely wait. It keeps charging, and some structures become more punitive if the borrower can't take them out on schedule.

That's why collateral risk and repayment pressure aren't side notes. They are central to the decision. If the business has weak visibility on the exit event, bridge financing can create stress at exactly the wrong time.

Use this lens before saying yes:

- Good candidate: The business has a clear purpose for funds and a credible path to repayment.

- Weak candidate: The owner is counting on several things going right at once.

- Strong strategic use: The loan protects ownership, margin, or deal certainty.

- Bad strategic use: The loan masks an operating problem that needs restructuring instead.

The right bridge loan feels temporary on day one. The wrong one feels necessary because there was no better plan.

Your Step-by-Step Guide to Obtaining Bridge Financing

Getting a bridge loan approved is less about telling a compelling story and more about making the lender believe your timeline. You need a crisp use of funds, a credible repayment path, and documents that support both.

Start with the use of funds and the repayment path

Before contacting any lender, write down two sentences. First, what the money is for. Second, how the loan gets repaid.

If either sentence is fuzzy, the application will be too. Bridge lenders expect specificity.

Your preparation list should usually include:

- Recent financials: Lenders want to see how the business performs, not just how it pitches.

- Cash flow support: Show where the temporary gap appears and when it should close.

- Transaction documents: Purchase agreements, term sheets, refinance discussions, or customer contracts can matter.

- Collateral information: If assets support the deal, package that evidence cleanly.

- Management explanation: Keep this short and practical. What's happening, why now, and what resolves the bridge.

A strong application doesn't drown the lender in paper. It anticipates the lender's core fear, which is that the bridge becomes the permanent solution by accident.

Choose the lender process that matches your timeline

A frequent struggle for many small businesses is losing momentum. Traditional banks can be a fit when the timeline is generous, the borrower profile is pristine, and the deal fits a conventional credit box. But that's not every situation.

The discussion at Elevate Health notes that bank bridge loans often carry interest rates exceeding 8%, that approval can be lengthy, that some fintech-enabled alternatives can fund within 30 days, and that 28% of small businesses report rejection from traditional lenders because of high credit requirements. For time-sensitive transactions, that difference in process can matter as much as the loan itself.

Here's the practical contrast:

| Lender type | Typical experience | Best fit |

|---|---|---|

| Traditional bank | More documentation, slower credit path, stricter box | Cleaner profiles with more time |

| Alternative or fintech lender | Faster review, more flexible process, narrower-use short-term products | Owners solving a real timing problem |

This kind of platform experience is what many owners now expect from financing tools.

If you're tightening your application process, this walkthrough on the ultimate guide to business loan applications is a helpful checklist.

A few closing moves improve your odds:

- Lead with the exit strategy. Don't bury the repayment source on page seven.

- Show timing, not just need. Urgency alone doesn't get approved.

- Be honest about delays. Lenders would rather price a known risk than discover a hidden one.

- Ask what would kill the file. Good lenders will tell you quickly.

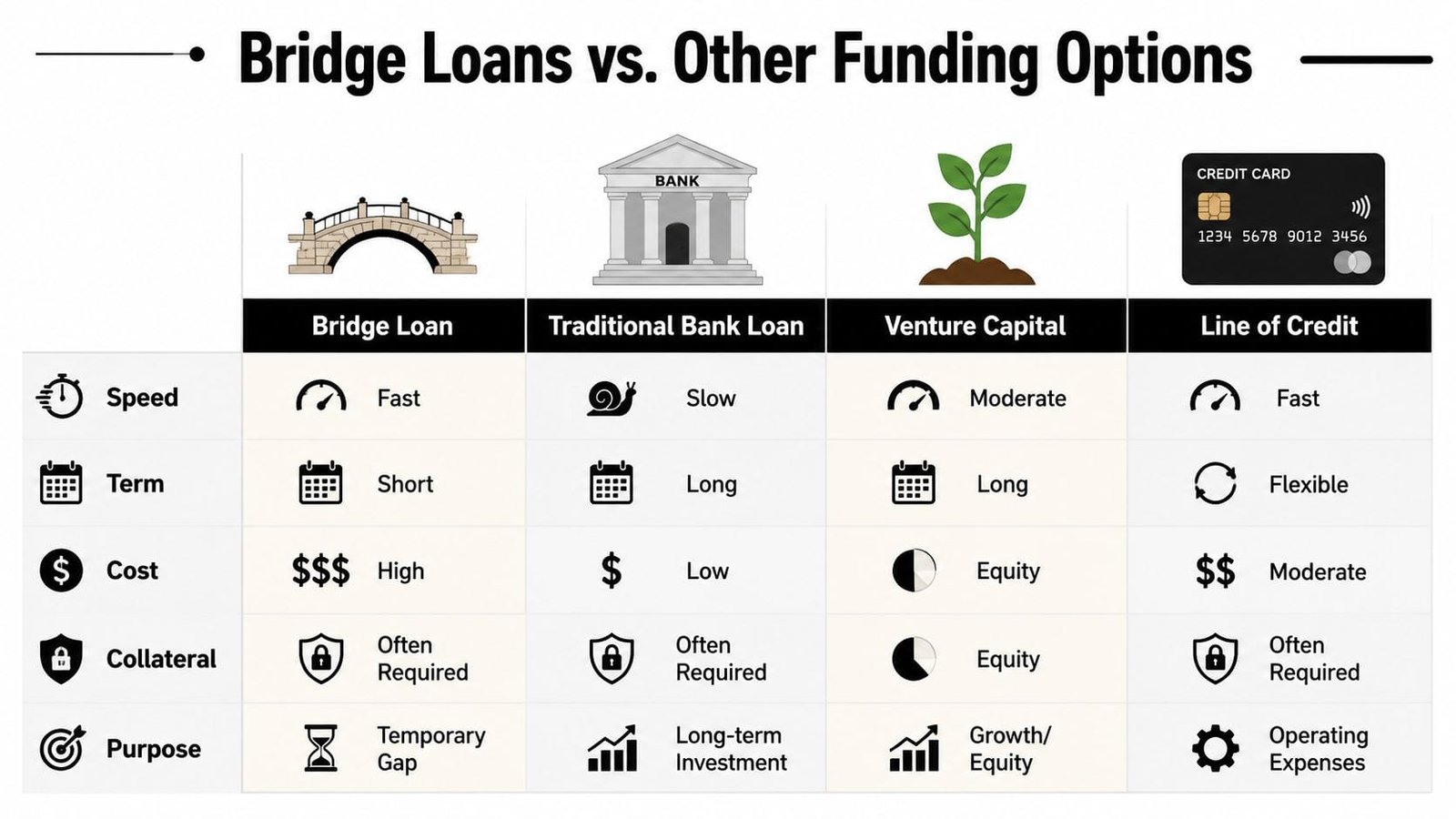

Bridge Loans vs Other Funding The Right Tool for the Job

Bridge financing is a specialized tool. Useful, sharp, and sometimes exactly right. But it isn't automatically the best option.

A business owner should compare it against other funding forms based on speed, flexibility, ownership impact, and whether the need is temporary or ongoing. If you want a broader perspective on capital planning, these strategies for profitable business funding offer a useful framework for thinking beyond one product type.

A practical comparison

Here's the simplest way to think about the situation.

| Funding option | Speed | Cost profile | Best use case | Qualification reality |

|---|---|---|---|---|

| Bridge loan | Fast | Higher short-term cost | Defined timing gaps tied to a known event | Works best with a clear exit path |

| Traditional term loan | Slower | Usually lower than bridge debt | Long-term investment, expansion, equipment, stable use cases | Better for borrowers who fit standard credit criteria |

| Venture capital | Moderate | Equity instead of interest | High-growth businesses willing to trade ownership for growth capital | Strong fit only for a narrow set of companies |

| Line of credit | Fast once established | Moderate and flexible | Recurring working capital swings | Good for ongoing needs, less ideal for one-off transactions |

A few decision rules help:

- Choose a bridge loan when the problem is timing and the payoff event is visible.

- Choose a term loan when the need is long-term and doesn't depend on a near-term capital event.

- Choose a line of credit when cash flow moves in cycles and you need repeat flexibility.

- Choose equity when the business can support dilution and needs patient growth capital more than repayment discipline.

If your decision sits between revolving flexibility and transaction-specific funding, this comparison of business line of credit vs bridge loan which is better for real estate deals in 2025 is a useful next read.

A bridge loan is the right tool when you know where you're going, why you can't wait, and how you get off the bridge.

If you need short-term capital for a time-sensitive deal, Business Loan Warrior gives you a faster way to explore options without wandering through a slow bank process. You can review funding paths built for small business realities, compare structures, and move toward a bridge solution that fits your timeline instead of fighting it.