Loan approval can take anywhere from 24 hours to 90+ days. That range comes down to two things: the type of loan you choose and, most significantly, how complete your application is when you submit it.

You've probably already felt the tension. You hit submit, refresh your inbox, check your phone, and wonder whether this is going to move fast or drag out for weeks. Most owners assume the answer depends entirely on the lender. That's only half true.

The bigger lever is usually sitting on your side of the table. If your paperwork is tight, your numbers are easy to follow, and your use of funds makes sense, approval tends to move. If your documents are scattered across email threads, desktop folders, and last year's accountant requests, the process slows down fast.

That's why the question isn't only how long does approval take. It's also, “What can I do today to stop this from turning into a long, expensive wait?”

Table of Contents

- The Waiting Game You Can Actually Win

- The Loan Approval Timeline Spectrum

- Approval Accelerators And Hidden Delays

- Your Ultimate Pre-Application Checklist

- Sample Timelines From Application To Funding

- How Fintech Platforms Shorten The Waiting Game

- From Application To Approval On Your Terms

The Waiting Game You Can Actually Win

The worst part of borrowing money isn't always the rate, the paperwork, or the underwriting questions. It's the silence.

A business owner submits an application because something needs to happen now. Payroll is coming. Inventory has to be purchased. A truck is down. A buildout can't stall. Then the process turns into a black box, and every day feels longer than it is.

That anxiety is real, but I'll be blunt. Too many owners hand over control before the process even starts. They assume approval speed is a mystery. It isn't. It's more like airport security. If you show up organized, with everything ready and nothing questionable in your bag, you move through. If you're digging for documents at the checkpoint, everyone waits.

Practical rule: Lenders can only move as fast as the file in front of them makes sense.

That's the shift that matters. You're not just waiting for a verdict. You're managing a process.

Some loan products are naturally faster than others. That part is fixed. But within almost every category, prepared borrowers move better than messy borrowers. The lender still underwrites risk, but a clean file makes that risk easier to evaluate.

If you take one thing from this article, take this: approval speed is not random. It follows a pattern. Product choice sets the outer range. Preparation decides whether you land at the fast end or the slow end of that range.

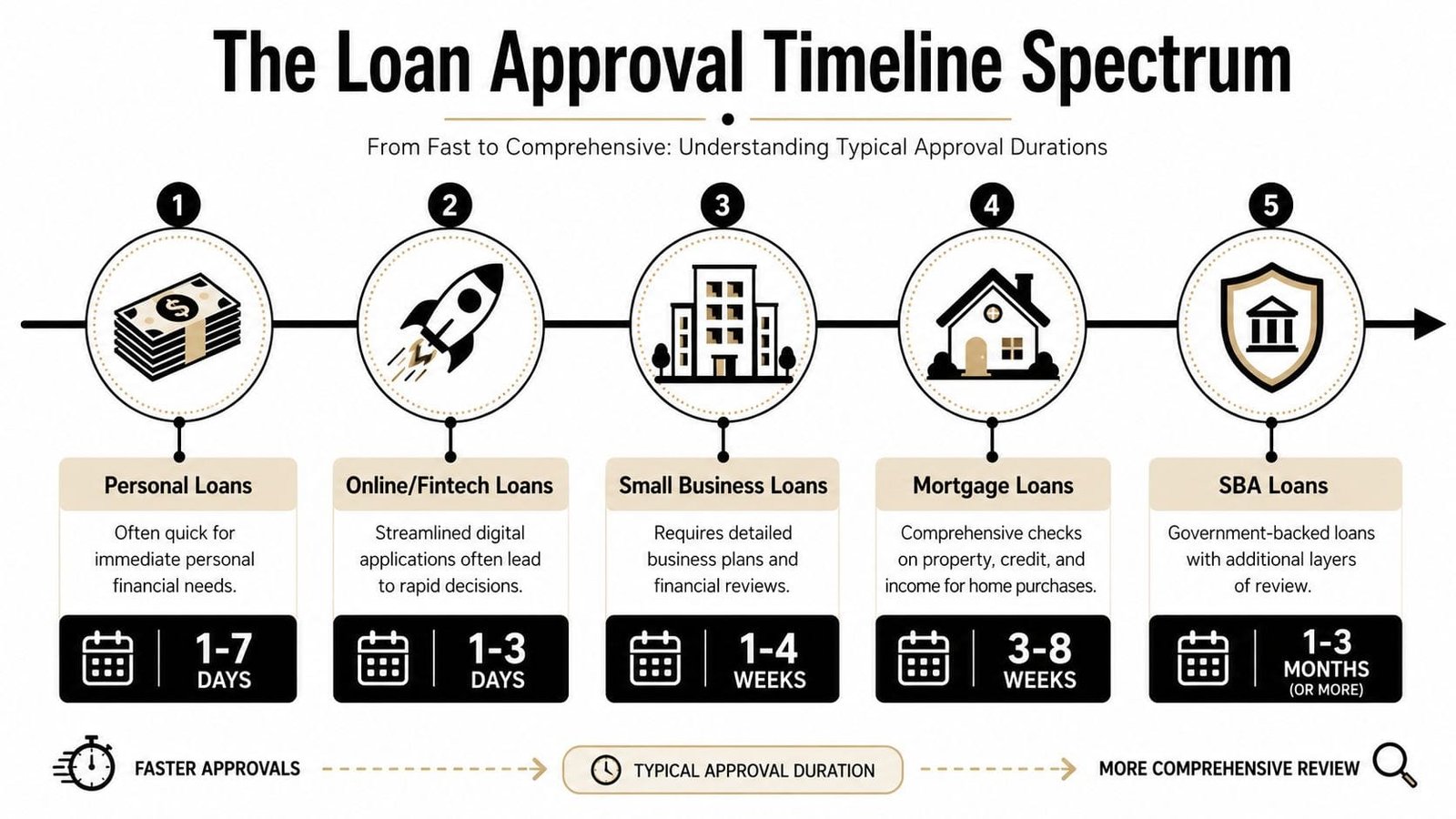

The Loan Approval Timeline Spectrum

A lot of approval frustration starts with a bad product match. If you need cash next week but apply for a loan built for layered underwriting, appraisals, and committee review, the delay was baked in from day one.

Fast money is built for speed

Online lenders sit at the fast end. Approval and funding can happen in 24 hours to 3 business days, according to Viking Funding's breakdown of business loan approval timing. Merchant cash advances and invoice factoring often move on a similar timetable because the review is narrower and the process has fewer handoffs.

That speed is useful, but don't miss the key lesson. Fast products stay fast when your records are ready. If your bank statements are messy, your revenue story changes from month to month, or your ownership documents do not match, even a quick lender slows down.

Traditional loans move slower because more people touch the file

Bank loans and SBA financing usually take longer. More review steps, more documentation, and more third parties mean more chances for delay.

For SBA 7(a) loans, the full path from application to funding often runs 30 to 90 days. Delegated authority can shorten that to 30 to 60 days. More complex transactions, especially real estate deals or SBA 504/CDC loans, often take 60 to 120 days. Some lenders target a 45-day close, while average funding after approval for SBA 7(a) can still take 60 to 90 days. Disaster loans can move faster, with approvals in 2 to 3 weeks and funding within up to five days, based on Swoop Funding's SBA loan timeline overview.

Here's the part owners overlook. The loan category sets the broad range. Your preparation decides where you land inside it.

A clean file works like an express lane. A sloppy file turns a reasonable timeline into a stop-and-go commute.

A simple way to choose

Use this rule:

| Need | Best fit mindset | Typical pace |

|---|---|---|

| Urgent working capital | Choose speed over perfect terms | Fast digital products |

| Planned growth financing | Balance cost, structure, and timing | Bank or non-bank options |

| Real estate or major expansion | Expect added review and longer processing | SBA and structured loans |

If the need is immediate, do not apply for a product that behaves like commercial real estate financing. If the project is large, asset-backed, and planned months in advance, do not force it into a speed-first product that solves the wrong problem.

One more practical point. If your team is scrambling to gather statements, tax returns, licenses, and ownership records, fix that before you apply. Lenders approve clearer files faster, and the same discipline you use to boost team productivity will shorten approval time here too.

A line cook does not use a smoker for a lunch rush. Loan products follow the same rule. Match the tool to the job, then show up prepared.

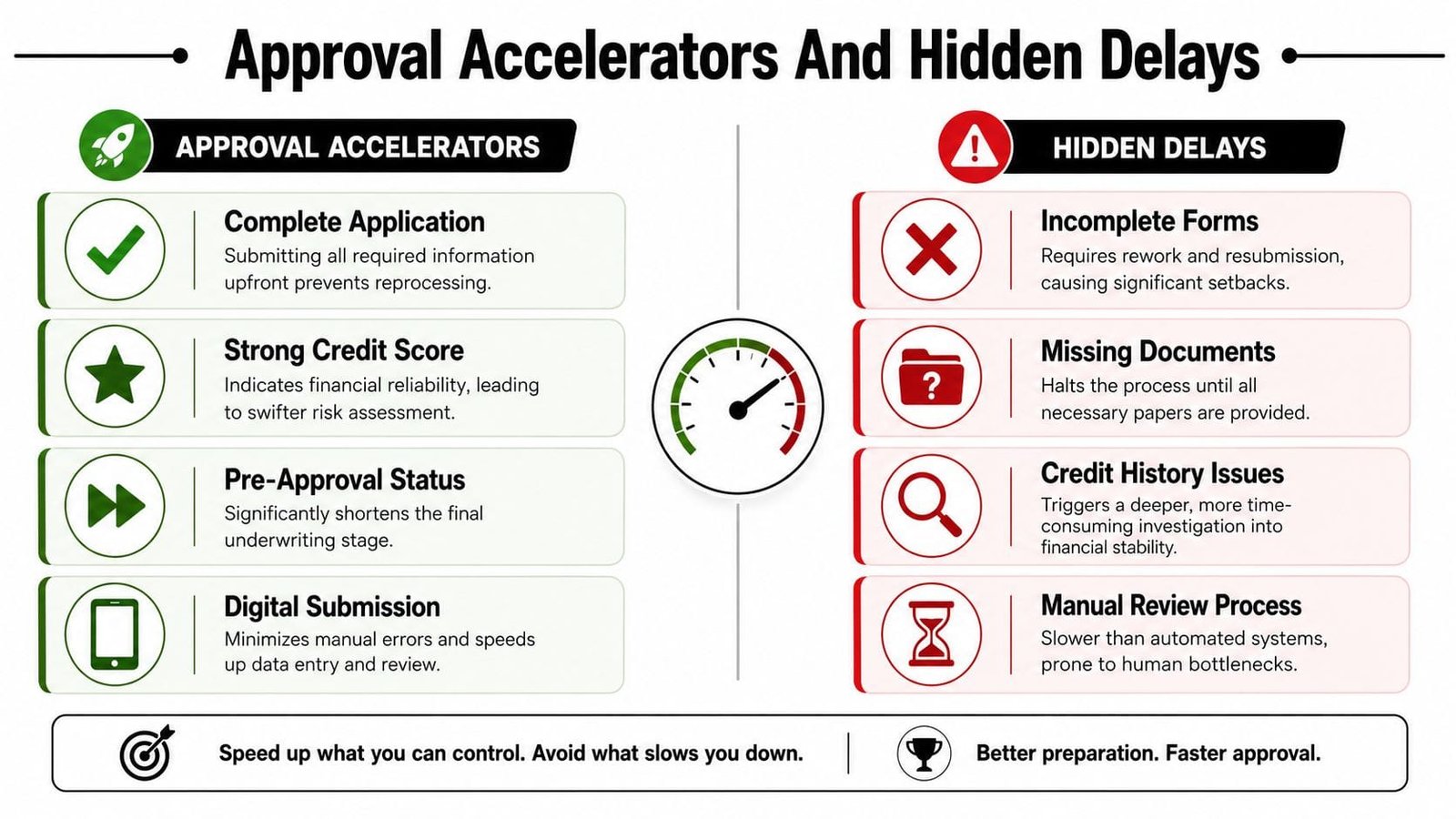

Approval Accelerators And Hidden Delays

Most owners blame the lender when a file stalls. Sometimes that's fair. Often it isn't.

The single biggest factor behind approval speed is documentation completeness. That's not a soft, motivational point. It's the mechanical reality of underwriting.

The biggest bottleneck is usually your file

Lenders report that prepared applicants can close underwriting in under 30 days, while unprepared applicants face delays of up to 60 days or more because missing files trigger re-underwriting cycles, according to Capital Bank's SBA loan process article.

That's the whole game. Not branding. Not clever timing tricks. Not wishful thinking.

A missing bank statement, unsigned form, unexplained deposit, outdated financial statement, or unclear ownership document can knock a file out of line. Then someone asks for clarification. You respond two days later. The underwriter has moved to another file. Your application goes back into review. That loop is what stretches time.

What actually creates delay

Here's what I see most often:

- Incomplete submissions: Owners upload some documents now and promise the rest later. That almost guarantees follow-up.

- Conflicting numbers: Tax returns, profit and loss statements, and bank activity tell different stories. Underwriters stop and ask questions.

- Weak use-of-funds explanation: “Working capital” is too vague when the lender needs to understand repayment logic.

- Multi-entity confusion: If money moves between related businesses, the file gets more complex fast.

- Slow response cadence: Even a strong file can stall if the borrower answers once every few days.

If your office is already juggling vendor calls, payroll, and sales, put one person in charge of assembling the loan file. That alone can boost team productivity because it reduces duplicate work, lost attachments, and internal confusion.

The underwriter is solving one question. “Can this business repay?” Every document should help answer that question faster.

The hidden delay is rarely dramatic. It's administrative friction. That's why organized borrowers often feel like they got “lucky” with timing. They didn't. They made the file easy to say yes to.

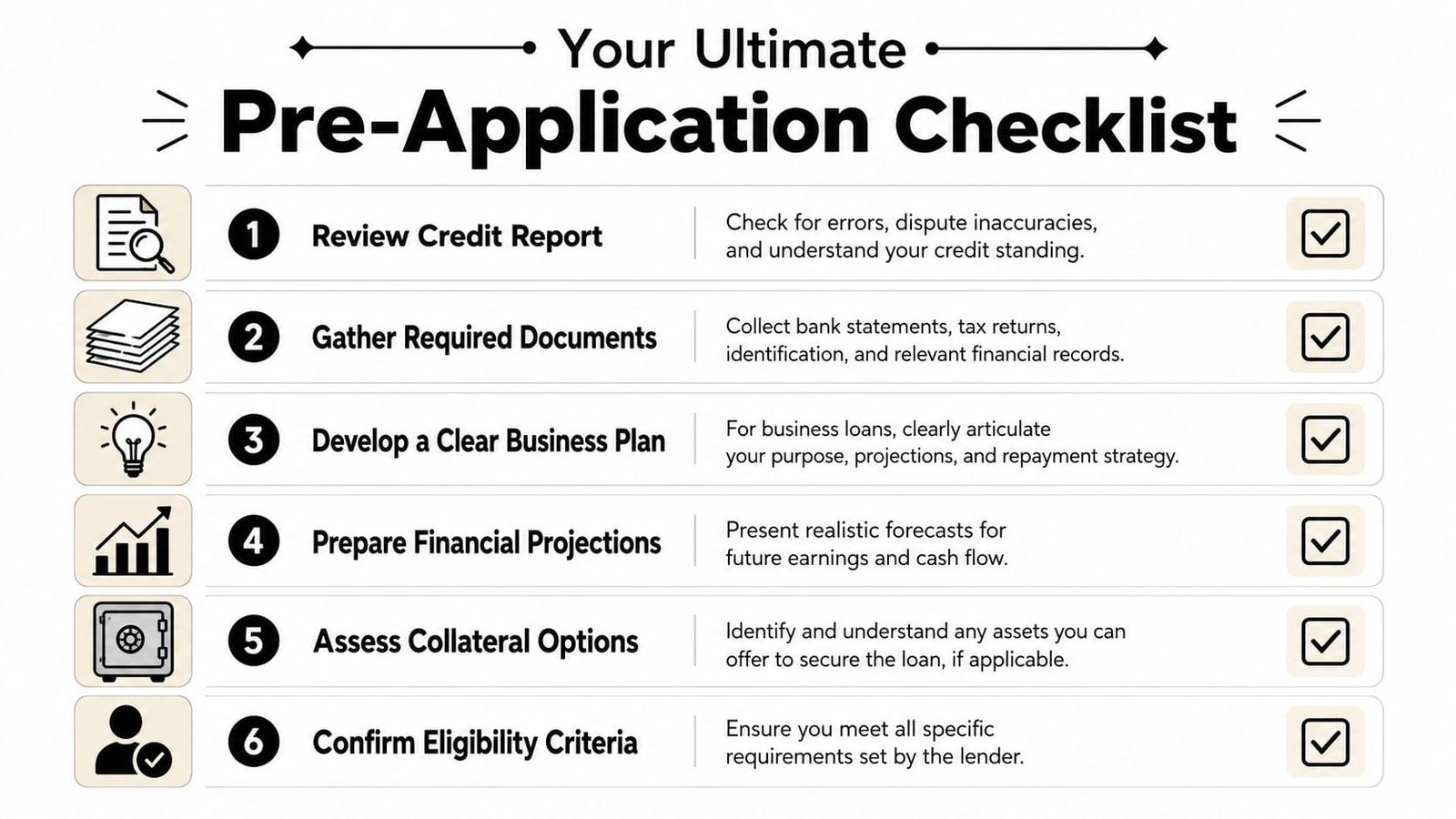

Your Ultimate Pre-Application Checklist

Before you apply, build your file like you're packing for a flight with strict baggage rules. If you wait until the airport to find your passport, you've already lost time.

A good checklist doesn't just gather papers. It tells a coherent story. If you want a useful companion resource on preparing a lighter, faster file, review this guide to minimal documentation for a quick small business loan.

Business records that should be ready first

Start with the documents that show how the business performs.

- Recent bank statements: These show cash flow behavior, not just reported income.

- Profit and loss statements: Make sure they're current and match the broader story your bank activity tells.

- Balance sheet: Lenders use this to spot debt load, liquidity pressure, and owner equity.

- Business tax returns: If they exist, keep them clean and easy to access.

- Accounts receivable or payable reports: Useful when cash flow timing is part of the story.

Don't hand over raw exports if they're messy. Label files clearly. Use dates in the filenames. If an underwriter has to guess which statement is the latest one, you're slowing the process.

Personal and legal documents lenders will ask for

Business borrowing often still touches the owner.

Personal tax returns

Many lenders want to understand the guarantor behind the business.Driver's license or government ID

Basic, but missing IDs stall files more often than they should.Formation documents

Articles of incorporation, operating agreement, or similar records help confirm who owns what.Business licenses

Especially important in regulated industries.Existing debt information

Have statements or summaries ready. Don't make the lender reverse-engineer your obligations.

If a lender asks for a document and you need three days to locate it, that's a warning sign that your internal records need cleanup before you borrow again.

Your use of funds needs a clean story

Many applicants grow complacent here. Don't.

“Need money for growth” is not a funding strategy. Say what the funds will do. Inventory purchase. Equipment replacement. Buildout. Hiring. Debt refinance. Bridge cash flow during a seasonal gap. The clearer the use, the easier it is for the lender to understand repayment.

A strong explanation usually answers three questions:

- What are you doing with the capital

- Why now

- How does that decision support repayment

That's the difference between looking prepared and looking desperate.

Sample Timelines From Application To Funding

Two borrowers can ask the same question, “How long does approval take?”, and get wildly different answers because they're solving different problems.

Scenario one urgent working capital

A service business loses a key piece of equipment on Monday morning. Revenue is going to suffer if the owner waits. This borrower doesn't need a long underwriting process or a highly structured facility. They need speed.

The owner gathers recent bank statements, current financial reporting, identification, and a simple explanation of the equipment issue. Because the request is straightforward and the file is organized, the application moves through a digital review path quickly. The rhythm is simple: submit, answer follow-up questions fast, verify information, sign, fund.

That kind of borrowing journey feels more like urgent care than elective surgery. The goal is fast stabilization.

For a realistic look at how that path compares with other funding journeys, this guide on small business funding timelines from application to cash in your account is worth reviewing.

Scenario two a larger expansion loan

Now take a manufacturer planning to buy or improve a facility. This borrower may be a good fit for a structured SBA or bank-backed transaction. The purpose is larger. The review is deeper. The lender isn't just evaluating revenue. They may also review collateral, property details, ownership structure, and the broader expansion plan.

Here, the timeline stretches because more people touch the file. Underwriters review financials. Third parties may need appraisals or valuations. Additional documentation requests are more likely because the transaction itself has more pieces.

A rough comparison makes the point clearly:

| Borrower type | Need | Typical process feel | Common friction |

|---|---|---|---|

| Service business with urgent need | Fast working capital | Short, direct, digital | Missing statements, slow borrower replies |

| Expansion borrower with asset-heavy deal | Facility or major growth project | Layered, document-heavy, structured | Appraisals, entity complexity, collateral review |

Neither path is wrong. The mistake is expecting them to behave the same way.

If your funding need is tactical, choose a tactical product. If it's strategic and asset-heavy, respect the longer process and prepare for it properly.

How Fintech Platforms Shorten The Waiting Game

Fintech platforms move faster because they remove handoffs, dead time, and document chaos. That matters more than flashy promises about speed.

A lender can only review what it can see clearly. If your bank statements are buried in email, your ID is missing, and your ownership documents come in one at a time, the process slows down no matter who you applied with. Fintech tools help by putting the file, the messages, and the status in one place. But the key accelerator is still your preparation. Good platforms reward organized borrowers.

Why digital workflows cut friction

The best fintech systems shorten approval time by reducing avoidable back-and-forth.

- One application flow: You submit core business details once, instead of repeating the same facts across calls, emails, and forms.

- Central file collection: Statements, tax returns, IDs, and entity documents stay in one secure portal.

- Live status tracking: You can see whether the file is under review or waiting on a specific item from you.

- Faster questions and answers: A quick message inside the platform beats a long email thread every time.

That structure works like a clean job site. When every tool is in the right place, the crew keeps moving. When tools are scattered, even simple work drags.

If you want a clearer look at how fintech platforms compare with banks on approval speed, review the tradeoffs before you apply.

The weekday myth is outdated

You do not need to time your application around a lucky weekday. You need to submit a clean file.

Digital platforms can intake applications at any hour, and many use automated checks to start reviewing basic data right away. Fora Financial notes this shift in its discussion of business loan timing through digital channels. The practical takeaway is simple. A complete application sent on Saturday beats a messy one sent on Tuesday.

The same logic shows up in other service systems. Faster turnaround usually comes from cleaner intake, fewer handoffs, and better visibility. AgentStack insights on AI support make the same point from a customer operations angle.

Use fintech for what it does best. Faster collection, clearer communication, and fewer process mistakes. Then do your part. Show up with documents ready, numbers that match, and responses that come back fast. That is how you cut the waiting game down.

From Application To Approval On Your Terms

Waiting feels awful when you think nothing is in your control. That's the wrong frame.

You do control the product you apply for. You control how clean your documentation is. You control how fast you answer follow-up questions. Those choices shape the timeline more than most borrowers realize.

If you run a business with any complexity, treat financing like an operational system, not a one-off event. Keep statements organized. Keep ownership documents accessible. Keep your story straight on why you need capital and how it gets repaid.

The companies that move best with lenders usually do one thing well. They reduce ambiguity. Underwriters don't like puzzles.

That same principle shows up in customer operations too. If you're interested in how better systems reduce delays and improve responsiveness, AgentStack insights on AI support offer a useful parallel. Faster service usually comes from cleaner workflows, not from pushing people harder.

If you want approval to move on your terms, stop asking only how long it takes. Start asking whether your file is built to move fast.

If you want a faster, clearer path to funding, Business Loan Warrior gives you one place to check pre-approval, upload documents, track progress, and connect with underwriters without the usual confusion. When your file is organized and the process is transparent, getting funded stops feeling like guesswork.