You're probably here because your business looks better on the ground than it does in a bank's credit box. You've got customers, invoices, maybe even steady growth. But the bank still says no, or drags the process out until the opportunity dies.

That's exactly where the SBA Community Advantage loan earns its place. It wasn't built for the easiest borrowers. It was built for viable businesses that traditional lenders often overlook. That includes newer companies, firms in underserved markets, veteran-owned businesses, and, in an important rule update many guides ignore, businesses with associates who were formerly incarcerated or on probation.

If you've been treated like your story is too complicated for funding, this program is worth a serious look.

Table of Contents

- Your Business Is Strong Why Cant You Get a Loan

- What Is the SBA Community Advantage Program

- Who Qualifies and What Are the Benefits

- Understanding Loan Amounts Terms and Uses

- Your Step by Step Application Checklist

- Community Advantage Compared to Other SBA Loans

- How Fintech Simplifies Your SBA Application

Your Business Is Strong Why Cant You Get a Loan

Banks like neat files. Small businesses rarely look neat.

Maybe your revenue is improving but uneven month to month. Maybe you're reinvesting every spare dollar into payroll, equipment, or inventory. Maybe your business is newer than a bank likes. None of that means your company is weak. It means conventional underwriting often misses real-world strength.

That's why the Community Advantage SBA program matters. In fiscal year 2024, it supported over $196 million in SBA lending nationwide, a 40 percent increase from the previous year, reflecting broader reach among underserved small businesses, according to this Community Advantage lending overview. That kind of growth tells you something simple. Owners are using it because the need is real.

Traditional banks reject patterns, not always potential

A banker might see one rough quarter and stop there. A mission-focused lender is more likely to ask what caused it, whether it's fixed, and how the business performs now.

That difference matters if you're financing:

- Working capital: To smooth payroll, inventory, or vendor timing.

- Equipment: To stop renting and start owning.

- Expansion: To open space, hire staff, or improve operations.

- A turnaround moment: To move from “barely keeping up” to “properly funded.”

If you're still getting denied, review the common mistakes in these top reasons SBA loans get denied and how to avoid them. Most denials aren't random. They come from gaps in documentation, weak repayment framing, or a story that doesn't match the numbers.

Practical rule: Don't walk into a lending conversation talking only about need. Talk about use of funds, repayment, and why the timing makes sense.

A lot of owners also underestimate how much lenders care about timing inside the business, not just total revenue. If your cash comes in lumpy waves, sharpen your understanding cash flow before you apply. Cash flow is the heartbeat of repayment. Profit on paper doesn't make loan payments. Collected cash does.

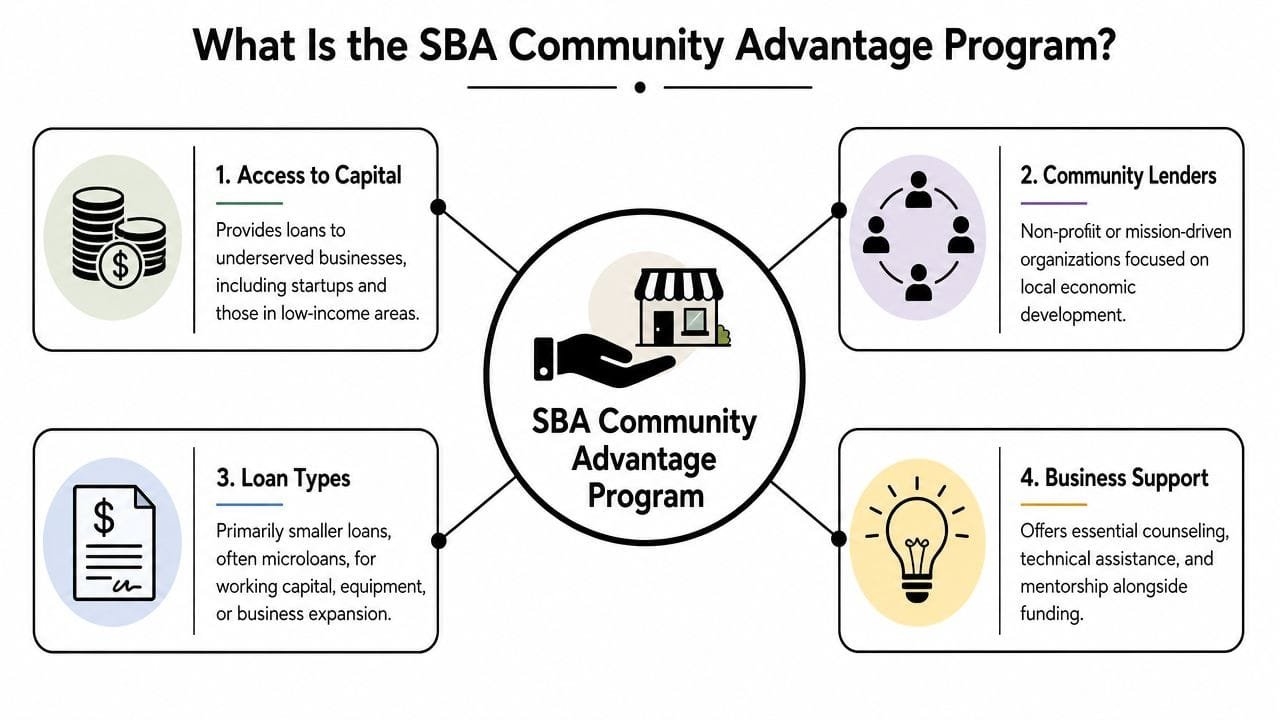

What Is the SBA Community Advantage Program

The easiest way to understand the SBA Community Advantage program is this. The SBA backs part of the risk, and mission-driven lenders do the front-line lending.

The SBA effectively deputizes community-focused lenders to serve borrowers who don't fit neatly inside a big bank's standard playbook.

Why this program exists

This program has a track record of over a decade helping underserved firms secure loans, and legislation was introduced in 2024 to make the pilot permanent, according to Representative Chu's release on the program. It targets mission-focused financial institutions serving low-to-moderate income communities, federally designated revitalization areas, and rural areas.

That mission matters because many banks don't want smaller, more nuanced deals. A community-based lender often does.

Here's who the structure is meant to help, in practical terms:

- Businesses in underserved communities

- Startups and newer businesses

- Borrowers who need guidance along with capital

- Owners whose file needs context, not just a score

How the structure works

The lender provides the money. The SBA provides a guarantee on qualifying loans. That guarantee reduces lender risk and gives the lender room to consider borrowers a conventional bank might brush aside.

The program also focuses on lenders that know local conditions. That's not a small detail. A lender tied to community development is more likely to understand why a contractor in a rural market, a service firm in a low-to-moderate income area, or a veteran-owned startup deserves a deeper review.

A good Community Advantage lender doesn't just ask, “Do you fit our box?” They ask, “Can this business repay if we structure this correctly?”

If you're weighing this against other SBA products, use this comparison of SBA 7(a), 504, and microloans to avoid chasing the wrong program. That saves more time than most owners realize.

Who Qualifies and What Are the Benefits

You can have real revenue, loyal customers, and solid margins, then still get rejected because a lender sees one weak spot and stops there. Community Advantage works differently. It still requires a credible borrower, but it gives lenders more room to judge the full story instead of killing the file at the first sign of complexity.

Start with the basics. Your business must meet standard SBA small business rules, operate for profit, and show a reasonable ability to repay. Beyond that, lenders usually focus on five practical questions: Do you handle credit responsibly? Do you understand your industry? Have you put some of your own money into the deal when needed? Can you support the request with collateral if the structure calls for it? Does the cash flow story make sense?

Here is the cleanest way to size up your file before you apply:

| Area | What lenders want to see |

|---|---|

| Credit | A track record of paying obligations with reasonable consistency |

| Experience | Enough industry knowledge to run the business well |

| Equity | Owner investment when the deal requires it |

| Collateral | Available support for larger or riskier requests |

| Repayment ability | Cash flow or a clear path to making the payments |

If one box is weaker, fix it before you apply. Do not assume a mission-based lender will ignore it. A better approach is to document the weakness, explain it plainly, and strengthen the rest of the file so the lender can defend the approval.

The biggest eligibility shift, and the one many articles miss, is inclusion. The SBA removed restrictions that had blocked some businesses from qualifying based on an associate's incarceration or probation status, as explained in the Bipartisan Policy Center's review of the Community Advantage rule changes. That change matters for veteran-owned firms, family businesses, and second-chance entrepreneurs who were often screened out before a lender even reviewed the business itself.

That does not mean the lender stops caring about risk. It means the conversation can finally center on repayment, operations, and management instead of ending with an automatic no. If your company has a strong operating plan and one person connected to the business has a record, do not self-reject. Ask directly how the lender evaluates associate background under current SBA rules.

That is a real advantage.

The benefits also go beyond the money. A good Community Advantage lender can help you structure the request, identify documentation gaps, and pressure-test your numbers before submission. For a small business owner, that support matters because SBA lending is often less about filling out forms and more about presenting a file that makes sense.

Technology helps here too. Digital application tools, secure document portals, and cash flow analysis software can cut out a lot of the back-and-forth that slows SBA deals down. Red tape is still part of the process, but it no longer has to mean fax-machine chaos and week-long email chains.

If you want a sharper baseline before talking to lenders, review these top four requirements to qualify for an SBA loan. It will help you spot problems early and walk into the process prepared.

Understanding Loan Amounts Terms and Uses

This part is straightforward, and it should shape your strategy before you fill out a single form.

What the funding can look like

The SBA states that the Community Advantage program offers a maximum loan size of $350,000 and that the unsecured loan limit increased from $25,000 to $50,000 to reduce collateral barriers for underserved borrowers, as described in the SBA announcement on the program expansion.

That unsecured limit matters.

For many service businesses, startups, and owner-operators, collateral is the choke point. They may have good margins, solid contracts, and industry experience, but not enough hard assets to satisfy a conservative lender. Raising the unsecured threshold gives those businesses a cleaner shot.

Here's the practical takeaway:

- Need a smaller amount and don't have much collateral? This program becomes more realistic.

- Need more capital but still below the cap? You may still qualify, but expect collateral review on larger requests.

- Own real estate or equipment? Your structure may be stronger, but those assets aren't the only story.

What you can use the money for

Community Advantage loans can support a wide range of business needs. The permitted uses commonly include working capital, equipment purchases, business acquisition, leasehold improvements, expansions, and property renovations, based on the verified program descriptions already discussed.

That flexibility makes the loan useful in situations like these:

Stabilizing operations

If receivables are slow and payroll is constant, working capital can stop short-term pressure from becoming a long-term problem.Buying tools that increase output

Equipment financing inside an SBA structure can be smarter than patching together high-cost short-term debt.Improving a location

Leasehold improvements can turn a marginal space into one that supports sales and staff efficiency.Funding a transition

Acquiring an existing business or adding a location often needs patient capital, not fast expensive money.

Borrow only for a use that clearly improves operations, revenue capacity, or stability. “General growth” is too vague. Lenders want a purpose they can underwrite.

Loan terms can extend up to 10 years for general funding and up to 25 years for real estate, based on the eligibility source cited earlier. Longer repayment can ease monthly pressure, but don't use term length as an excuse to overborrow. Cheap monthly payments still become expensive if the capital doesn't solve a real business problem.

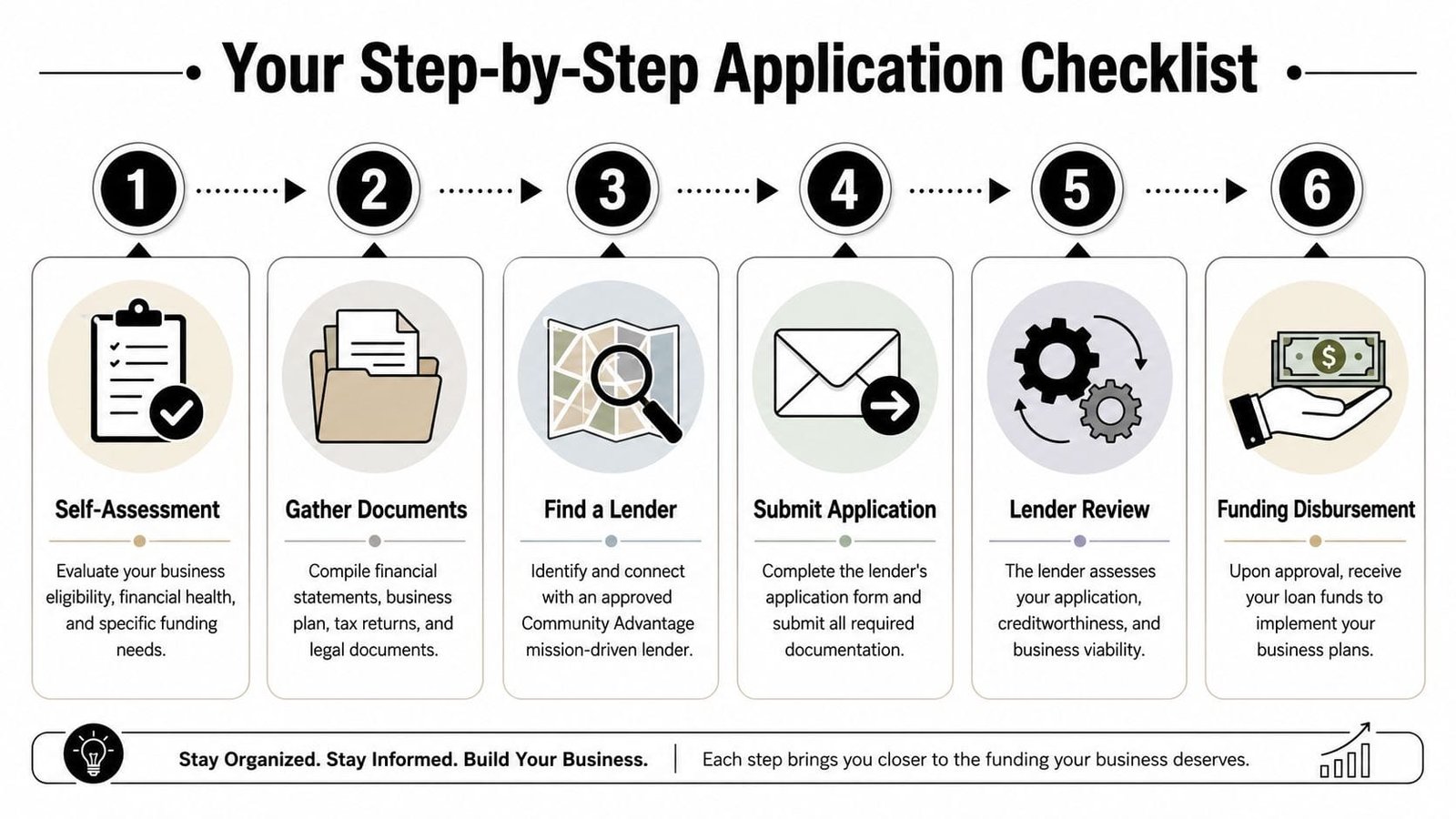

Your Step by Step Application Checklist

You sit down to apply on Friday thinking the hard part is over. By Tuesday, the lender is asking for missing tax returns, ownership details do not match across forms, and the explanation for a past legal issue is vague. Good businesses get stalled this way every week.

Treat this application like an audit file. Clean, consistent, and ready before you press submit.

Start with the underwriter's three questions

Write out your answers before you talk to any lender:

- How much do you need

- What exactly will you use it for

- What cash flow repays the loan

Be specific. “Growth” is not a repayment plan. A lender wants to see how the money turns into revenue, savings, or stability. Signed contracts, steady customer demand, better margins, or lower operating costs all help.

This matters even more if your file needs context. Community Advantage has been one of the more inclusive SBA paths for borrowers who do not fit a bank's narrow template, including veteran-owned businesses and some businesses with formerly incarcerated associates that may now qualify under updated rules. That does not mean lower standards. It means your explanation has to be organized and credible.

Build the file before you start shopping lenders

Do not begin with a dozen applications. Begin with one complete package.

At minimum, prepare current business financials, business and personal tax returns, ownership information, a business plan or written summary, debt schedule, and documents that support the use of funds. If there is a past credit issue, a legal history question, or a gap in operations, add a short written explanation now. Waiting for the lender to discover it wastes time and weakens trust.

Use this sequence:

Review your eligibility and story

Confirm basic SBA fit, ownership structure, and any background issues that need explanation. If your business includes an associate with a prior conviction, address it directly and accurately instead of hoping it gets overlooked.Collect every required document in one place

Incomplete files create avoidable delays. A messy package signals weak controls.Match with the right lender

Community-focused lenders are often better at underwriting stories that need explanation, especially for underserved founders, veterans, and borrowers with nontraditional histories.Check for consistency across every form

Business name, ownership percentages, revenue figures, and use of funds must match everywhere. Underwriters notice small mismatches fast.

One practical way to streamline document collection is to use a secure intake system instead of chasing files across email threads. That saves time and cuts down on version errors, which are a common reason applications drag.

Lender mindset: If the file arrives incomplete, the answer is rarely “yes, and we will figure it out later.”

This overview helps if you want a visual of the process in motion:

Keep underwriting simple

Once the lender starts reviewing your file, stop selling and start answering.

| Stage | What you should do |

|---|---|

| Initial review | Reply quickly, answer the question asked, and keep explanations short |

| Underwriting follow-up | Send the exact document requested, clearly labeled and complete |

| Closing prep | Confirm the final terms, verify the use of funds, and understand how disbursement will happen |

Strong borrowers usually do three things well:

- They respond fast

- They explain anomalies clearly

- They keep the narrative and numbers aligned

If revenue dipped for one quarter, explain why and show what changed. If an owner has a background issue, disclose it accurately and provide context the first time. If your loan request is $150,000, your documents should not read like a $300,000 plan.

That is how you keep a promising application from turning into a slow, expensive paperwork problem.

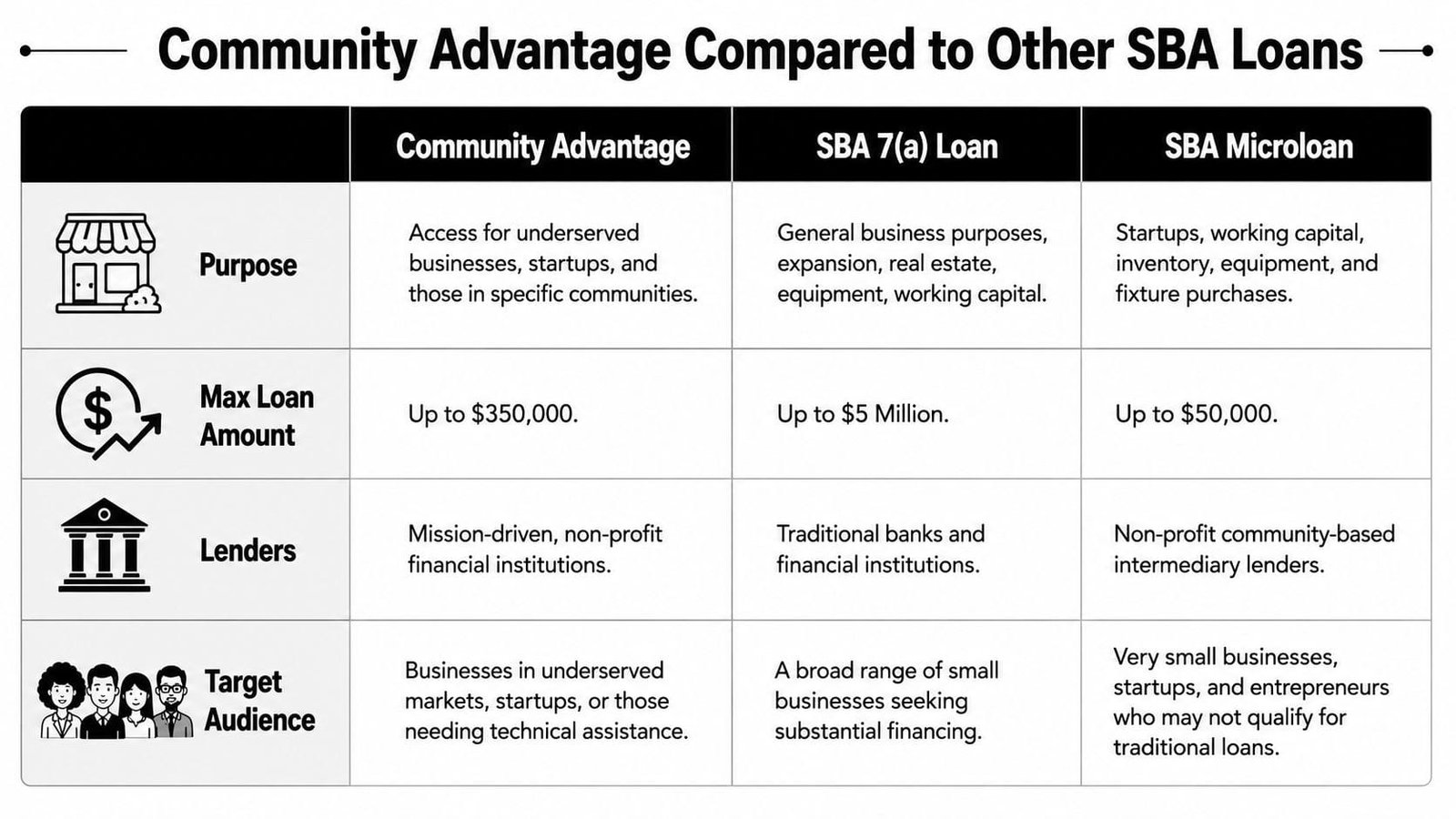

Community Advantage Compared to Other SBA Loans

Not every borrower should use Community Advantage. Some should. Some absolutely shouldn't.

The decision gets easier when you stop treating all SBA products as interchangeable.

When Community Advantage is the better fit

Community Advantage is usually the stronger choice when you need a moderate loan amount, your story needs context, or you want a lender that works with underserved markets as part of its mission.

Use it when:

- You need up to $350,000

- You're a startup or newer business

- You operate in an underserved or rural market

- Your file needs human review, not pure automation

- You value guidance alongside funding

A standard SBA 7(a) often works better for larger, more conventional borrowers dealing with banks that want stronger documentation, more scale, or a cleaner credit picture.

When another SBA option may be smarter

An SBA Microloan can make more sense if your capital need is small and basic. If the request is modest and the business is very early, a microloan may be enough without the heavier structure of Community Advantage.

A traditional 7(a) may be smarter if:

| Loan type | Best fit |

|---|---|

| Community Advantage | Underserved borrowers, newer firms, moderate requests |

| SBA 7(a) | Broader business use, larger financing needs, stronger bank-ready files |

| SBA Microloan | Very small businesses, startups, limited capital requests |

Don't choose based on brand name. Choose based on fit. The wrong loan wastes time even if it sounds prestigious.

How Fintech Simplifies Your SBA Application

The hardest part of an SBA loan usually isn't deciding to apply. It's surviving the paperwork, follow-up, and lender matching without losing weeks.

The old process wastes time

The old way is clumsy. You call multiple lenders, repeat your story over and over, upload the same files in different formats, and wait for replies that may never come.

That isn't just annoying. It creates friction at the exact point where small business owners already have the least spare time.

A digital workflow fixes the worst part

A good fintech workflow does three things better than the traditional process.

- It centralizes documents: One secure place beats emailing statements back and forth.

- It improves visibility: You can track status instead of wondering whether anyone touched the file.

- It reduces repetition: You shouldn't have to rebuild the same application for every conversation.

If you want a practical look at how software can streamline document collection, that's the exact bottleneck modern tools solve best. For SBA borrowers, that means fewer missing files, cleaner handoffs, and less chasing signatures and statements across email threads.

Good technology doesn't replace underwriting. It removes the administrative clutter that keeps underwriting from happening quickly.

For borrowers pursuing Community Advantage SBA financing, that matters. A cleaner process means less confusion, faster lender responses, and fewer preventable delays.

If you're considering an SBA loan and want a faster way to get organized, Business Loan Warrior is worth a look. You can start with a single no-fee application, check pre-approval without affecting credit, and manage documents and updates in one place instead of chasing lenders manually.