When you hear the term blanket lien, don't let the legal jargon intimidate you. It's a surprisingly simple concept, but one with massive implications for your business financing.

A blanket lien is a lender's claim on nearly all of your business assets as collateral for a loan. Instead of securing the debt with a single asset, like a delivery truck, the lien "blankets" everything. This includes your inventory, equipment, accounts receivable, and even intellectual property.

Table of Contents

- What Is a Blanket Lien in Simple Terms?

- How a Blanket Lien Is Put into Place

- The Day-to-Day Impact on Your Business Operations

- What Happens When Your Business Defaults

- Proactively Managing and Removing a Blanket Lien

- Financing Alternatives That Avoid Blanket Liens

- Asset-Specific Financing

- Revenue-Based Financing

- Blanket Lien FAQs: Your Top Questions Answered

- Will a Blanket Lien Affect My Personal Assets?

- Can I Sell Business Assets if There's a Blanket Lien?

- How Long Does a Blanket Lien Last?

- Are Blanket Liens Common With SBA Loans?

- Can My Business Have More Than One Lien?

What Is a Blanket Lien in Simple Terms?

Forget the stuffy legal definitions for a moment. Think of a blanket lien as a lender's master key to your business. If a normal secured loan gives the lender a key to a specific room (like the garage where your truck is parked), a blanket lien gives them a key that opens every single door.

Lenders, especially for SBA loans or other types of small business financing, love this arrangement because it dramatically lowers their risk. By having a claim on everything you own, they feel much more secure. But what's security for them can create major headaches for you down the road.

The Legal Framework Behind the Claim

A blanket lien isn’t just some clause buried in the fine print; it's a formal legal process. When you sign the loan agreement, the lender files a document called a UCC-1 financing statement. This filing, usually with your state's Secretary of State, creates a public record that signals to the world that this lender has first dibs on your assets.

This public filing is crucial. It puts every other potential creditor on notice. It also typically covers "after-acquired property"—a tricky clause meaning any new assets you buy after signing the loan are automatically swept under the lien. That new forklift or computer system? The lender has a claim on it, too. You can dig deeper into the legal side of this at Cornell Law School's Legal Information Institute.

The real power of a blanket lien comes from this broad scope. It's the polar opposite of a specific lien, which is tied to a single asset. Understanding this difference is key to making smart borrowing decisions.

Blanket Lien vs. Specific Lien at a Glance

To really see the difference, it helps to put them side-by-side.

| Feature | Blanket Lien | Specific Lien |

|---|---|---|

| Scope of Assets | Covers nearly all business assets, current and future. | Tied to a single, specific asset (e.g., a vehicle or property). |

| Lender Risk | Very low. The lender has a claim on everything. | Higher. The lender can only claim the one specific asset. |

| Flexibility for Owner | Low. Selling assets or getting new loans is difficult. | High. Other assets remain free and clear for other uses. |

| Common Use Case | Working capital loans, lines of credit, SBA loans. | Auto loans, mortgages, equipment financing. |

As you can see, while a specific lien is like a lock on one box, a blanket lien is like putting your entire warehouse under lock and key.

This single clause impacts everything from your ability to sell old equipment to your chances of securing a second loan. Grasping how it works is non-negotiable for any savvy business owner. To see how this plays out in real-world lending, check out our guide on secured versus unsecured business lines of credit.

It's also worth noting that liens come in various forms, not just from lenders. For example, the government can place liens for unpaid taxes. Getting a handle on understanding tax liens provides a broader perspective on how these legal claims can affect your business.

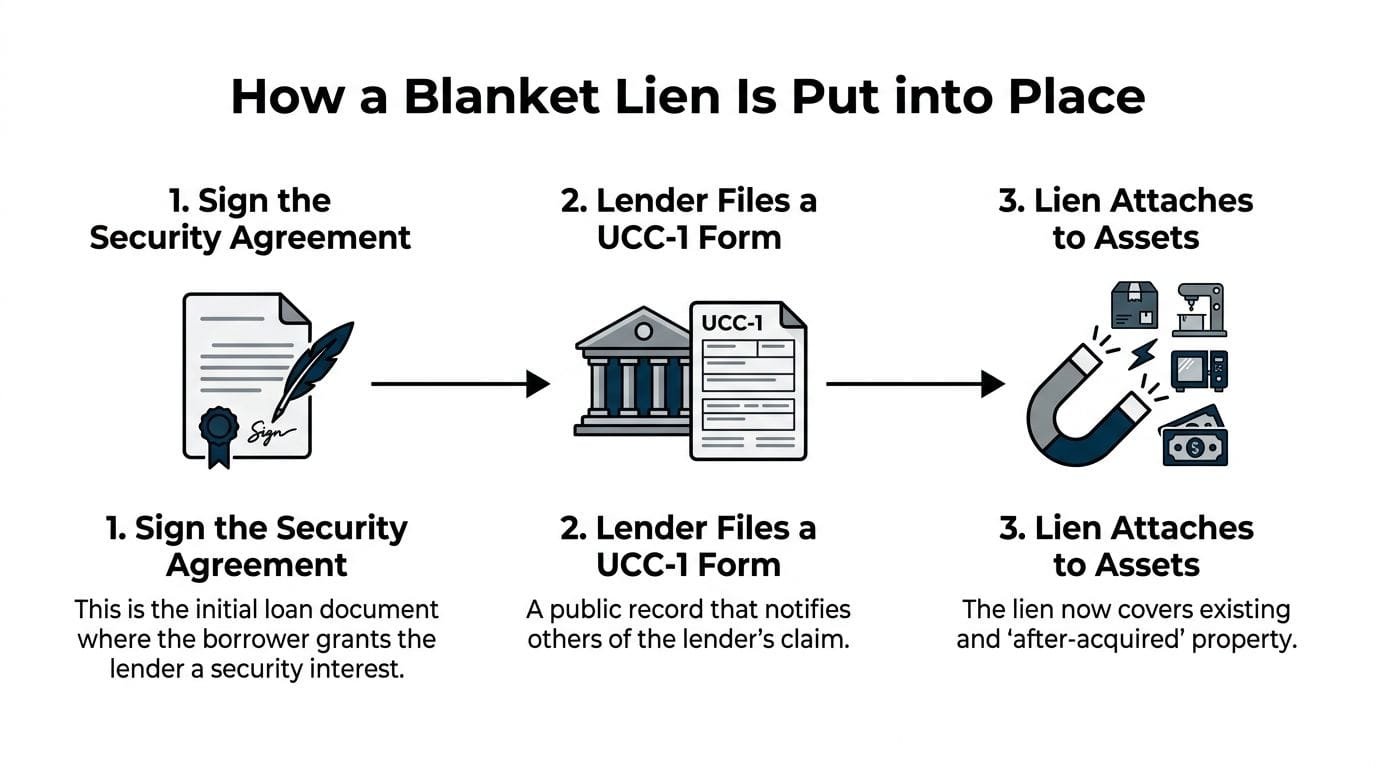

How a Blanket Lien Is Put into Place

A blanket lien doesn’t just appear out of nowhere. It’s the final step in a formal, public process that starts the moment you sign a loan agreement. For any business owner, understanding exactly how this happens is the first step in managing it.

It all begins with a critical document called the Security Agreement. Think of this as the legal foundation for the lien. By signing it, you are officially giving the lender a security interest in your business's assets. This contract spells out which assets are covered (in this case, almost everything), what you need to do as the borrower, and what counts as a default.

Perfecting the Lien with a UCC-1 Filing

Once you’ve signed the Security Agreement, the lender moves to “perfect” their lien. This isn’t just internal paperwork; they make it public by filing a UCC-1 financing statement. This document is filed with a state office, usually the Secretary of State where your business is legally registered.

"UCC" stands for the Uniform Commercial Code, which is the set of laws governing these types of commercial deals across the U.S.

This filing is basically a public announcement to the world. It tells every other potential lender or creditor that your lender has first dibs on your assets. Anyone who runs a background search on your business will see this filing and know exactly who is first in line to get paid.

This public record is what locks in lien priority. The rule of thumb is simple: first in, first out. The lender who files their UCC-1 first gets the first-position priority. If your business ever defaults and has to liquidate, they are the ones who get paid back before anyone else touches a dime.

The Ever-Expanding Reach of the Lien

One of the most powerful parts of a blanket lien is often buried in the fine print of the Security Agreement: the "after-acquired property" clause. It does exactly what it sounds like. This clause means the lien automatically grabs onto any new assets your business buys after you’ve taken out the loan.

Let’s walk through a quick example:

- You get a loan: You take out a $100,000 working capital loan that comes with a blanket lien.

- You buy new gear: Six months down the road, you use profits to buy a new $30,000 piece of equipment.

- The lien attaches: That blanket lien instantly and automatically attaches to the new machine. No new forms, no new signatures.

This clause ensures the lender’s collateral keeps pace with your business’s growth, protecting their investment over the entire life of the loan. It doesn’t stop you from running your business—you can still sell inventory and manage day-to-day operations—but it makes it crystal clear that the lender's claim covers everything you own, now and in the future.

The Day-to-Day Impact on Your Business Operations

A blanket lien isn't some abstract risk that just sits on paper. It creates real, tangible hurdles in your everyday business activities. While you can still sell inventory and run your company, the lien acts as a constant drag on your financial and strategic agility, slowing down your growth.

The first and most immediate challenge you'll run into is trying to get more funding. Imagine a fantastic expansion opportunity comes up, but you need a second loan to seize it. Any new lender will run a UCC search, discover the existing first-position blanket lien, and almost certainly pump the brakes. Why? Because the first lender already has dibs on all your assets, leaving nothing for the second lender to secure their loan against. It makes their loan far too risky.

The Operational Handcuffs a Lien Creates

Beyond just funding, the lien introduces friction into your daily operations. One of the biggest constraints is needing your lender’s approval before selling any major asset. This isn’t just for something huge like company real estate—it applies to upgrading equipment, selling a company vehicle, or even offloading old machinery you no longer use. This bottleneck can seriously slow down decisions that need to be made quickly.

A logistics firm, for instance, can’t just sell an old truck to help fund a new one without waiting for the lender's green light. For a small business, this delay can mean missing out on a great deal or falling behind a competitor. This is why maintaining strong cash flow is so important—it can help you avoid these situations in the first place, and learning how to get invoices paid faster can make a huge difference.

A blanket lien often requires you to get explicit lender approval before selling any major asset—whether it’s to upgrade equipment, expand your facility, or simply dispose of obsolete inventory. This can be a significant operational constraint.

This formal process is exactly why the lien carries so much legal weight.

From the security agreement you sign to the public UCC-1 filing, every step is designed to give your lender a legally enforceable claim over your business assets.

Navigating the Restrictions

Blanket liens are most common with short-term loans, especially when capital is needed fast or for businesses that lenders see as higher risk. To fight back against these restrictions, savvy business owners negotiate "mission-critical asset carve-outs" before signing the loan documents. This officially exempts essential items from the lien’s grip.

It’s also standard practice to renegotiate the agreement as you pay down the loan, working to convert the blanket lien into a more specific one that only covers certain assets.

Under a lien, keeping a meticulous record of your assets becomes absolutely vital, as this is tied directly to your borrowing base. For a deep dive on how to do this right, check out our borrowing base monitoring playbook to keep your records accurate and your lender happy.

What Happens When Your Business Defaults

Defaulting on a loan backed by a blanket lien is one of the most dangerous situations your business can face. This goes way beyond a ding on your credit score. A default flips a switch, giving the lender an arsenal of powerful rights that can put your company's survival in jeopardy.

When you default—and that could mean anything from a missed payment to breaking a loan covenant or filing for bankruptcy—the clock starts ticking. Your lender can move to get their money back, and they can do it with surprising speed.

The Lender's Powerful Rights After a Default

Thanks to the Uniform Commercial Code (UCC), a lender holding a perfected blanket lien has incredible power. In many cases, they don't need to waste time with a long, drawn-out court battle to start seizing your business's property.

Here's what they can do almost immediately:

- Asset Seizure: The lender can show up and take physical possession of your business assets. We're talking about everything from your delivery trucks and machinery to the desks and computers in your office. As long as they don't "breach the peace," they often don't even need a court order to do it.

- Accounts Receivable Collection: This one is a killer for cash flow. The lender has the right to contact your customers and legally instruct them to send payments directly to the lender, not to you. Your revenue stream can be shut off overnight.

- Liquidation of Assets: Once the lender has your assets, their next step is to sell them off to cover the debt.

The most critical risk of a blanket lien is that a default can lead to the lender seizing and selling all business assets. This isn't limited to a single item; it could mean the end of your business as they liquidate the very assets you need to operate.

The Role of Personal Guarantees

It's crucial to understand the difference between the blanket lien and a personal guarantee, even though lenders often demand both. The lien is tied to your business assets. A personal guarantee, on the other hand, puts your personal wealth on the line.

If the money from selling your business assets isn't enough to cover the loan, the personal guarantee gives the lender the right to come after your personal property—your house, your car, your savings account.

If your business is in this tight spot, you have to know all your legal options. It's essential to explore every possible path, which may include seeking professional guidance for businesses in financial distress. While the lender has immense power, they still have to play by the rules. The biggest rule is that they must act in a "commercially reasonable" manner when selling your assets. This means they can't just dump your equipment for pennies on the dollar; they have a legal duty to try and get a fair market price.

Proactively Managing and Removing a Blanket Lien

Just because a lender has a blanket lien on your business doesn’t mean you’ve lost all control. While it’s a serious agreement, think of it less as a permanent trap and more as a situation you can actively manage—and eventually, escape entirely.

Getting ahead of the game is your best strategy for keeping your financial options open.

The best time to push back is before you even sign on the dotted line. Never assume the lender's standard terms are set in stone. Instead, go into negotiations prepared to request asset "carve-outs" to shield your most critical assets.

For example, if you run a logistics company, you could fight to exempt your primary delivery fleet from the lien's reach, protecting the very heart of your operations.

Negotiating and Modifying the Lien

Even after a lien is filed, you’re not out of options. As you build a track record of consistent, on-time payments, your power in the relationship grows. Once you’ve paid down a good chunk of the loan, it’s the perfect time to go back to your lender and ask for a change.

A smart move is to renegotiate the blanket lien into a much less restrictive specific collateral lien. You can propose securing the smaller remaining balance with specific, high-value assets—like a key piece of machinery or a single property. This unlocks the rest of your assets, freeing you up to get other loans or sell equipment without asking for permission.

A blanket lien creates a 'first-dollar' claim on a business's entire asset base, often preventing the company from securing additional financing until the lien is terminated. While distinct from a personal guarantee, the lien provides the lender a comprehensive safety net covering inventory, equipment, and accounts receivable.

The Formal Lien Removal Process

Once you’ve made that final payment—congratulations!—your work isn’t quite done. The lien won't just vanish on its own. To officially remove it, the lender must file a UCC-3 Termination Statement with the same state office that recorded the original UCC-1 filing.

This is the crucial step that wipes the slate clean on your public record. Without it, the old lien can stick around like a "ghost," scaring away future lenders who see it during a search. It’s absolutely essential to follow up and confirm your lender has filed the UCC-3.

What if they drag their feet? The law gives you the right to file the termination yourself if the lender fails to act promptly. This is a critical protection that ensures a paid-off debt doesn’t hamstring your company forever. You can dig deeper into this process and your rights in this guide on legal resources for blanket liens.

Making sure that lien is officially terminated is the final step. It's how you truly reclaim your company’s financial freedom and get back to chasing growth without anything holding you back.

Financing Alternatives That Avoid Blanket Liens

If the idea of a blanket lien feels way too restrictive for your business, don't worry. You have other ways to get funded. Plenty of financing options exist that don’t demand you pledge every single asset you own, giving you much-needed flexibility, even if they come with different trade-offs.

These alternatives steer clear of the "all-or-nothing" approach a blanket lien takes. Instead, they secure the debt using more targeted methods. This leaves the bulk of your assets free and clear for future financing needs or just day-to-day operational freedom.

Asset-Specific Financing

The most straightforward alternative is financing that’s tied directly to a specific purchase. It's a common-sense way to acquire essential assets without putting your entire business on the line.

- Equipment Loans: Need a new piece of machinery? With an equipment loan, the machine itself serves as the collateral. The lien is only on that specific asset, leaving your inventory and accounts receivable completely untouched.

- Vehicle Financing: This works just like an equipment loan but for commercial vehicles. The financing is secured solely by the truck or van you're buying.

These options are perfect for funding growth when the value of the asset you're buying can directly secure the loan.

The core idea behind these alternatives is simple: the collateral should match the purpose of the loan. This stops a single loan for one truck from tying up every asset your business owns, from office computers to the payments your clients owe you.

Revenue-Based Financing

Another group of options looks to your future income for security, not your current hard assets. This can be a fantastic choice for businesses that have strong, consistent sales but not a lot of physical equipment to pledge.

Invoice factoring lets you sell your outstanding invoices to a factoring company for a small discount. You get cash in your hand almost immediately, and the factor takes on the job of collecting the payment from your customer. In this case, your accounts receivable secure the advance—not your whole company.

A Merchant Cash Advance (MCA) gives you a lump sum of cash in return for a slice of your future credit card sales. While MCAs are often more expensive, they typically don't involve a blanket lien. This makes them a fast, accessible option if you need capital right now. Just be sure you understand the total cost before you commit.

Choosing between these funding paths and more traditional loans depends on your specific goals and what you're comfortable with. You can dive deeper into these differences by reading our article on when to choose a secured line of credit over a term loan.

Blanket Lien FAQs: Your Top Questions Answered

When you're navigating business financing, legal terms like "blanket lien" can feel intimidating. Don't worry, they're more straightforward than they sound. Here are some plain-English answers to the questions we hear most often from business owners.

Will a Blanket Lien Affect My Personal Assets?

On its own, no. A blanket lien is designed to cover your business assets only. It doesn't touch your personal car or home.

However—and this is a big one—most lenders will also ask you to sign a personal guarantee. This is a separate agreement that acts as a backstop. If you default and selling the business assets doesn't cover the full loan amount, the personal guarantee kicks in, putting your personal assets on the line.

Can I Sell Business Assets if There's a Blanket Lien?

Yes, but it depends entirely on what you're selling. Lenders expect you to run your business, so selling inventory to customers as part of your normal day-to-day operations is perfectly fine.

The line gets drawn when you try to sell a major asset outside of that normal flow. Think selling a vital piece of machinery, a delivery truck, or your office computers. For a sale like that, you will absolutely need to get the lender’s written permission first.

A blanket lien is a formal legal tool used in business lending; it is not related to personal property like a crocheted blanket. The term "blanket" simply refers to its wide, comprehensive coverage over a business's assets.

How Long Does a Blanket Lien Last?

The lien stays in place for the entire life of the loan. It doesn't just disappear when you’ve paid off a certain percentage. The public record of the lien, known as a UCC-1 financing statement, is valid for five years and can be renewed by the lender if your loan term is longer.

Once you’ve paid back every last dollar, the lien isn't automatically removed. The lender has to file a UCC-3 Termination Statement to officially release their claim on your assets.

Are Blanket Liens Common With SBA Loans?

Yes, they are standard procedure. The U.S. Small Business Administration (SBA) almost always requires a blanket lien on all business assets as security for its government-backed loans. It's one of the main ways they protect taxpayer money in case of a default.

Can My Business Have More Than One Lien?

Absolutely. It's possible for a business to have multiple liens from different lenders. The critical factor is "priority," which is almost always determined by who filed their lien first.

The lender with the first-position priority has the strongest claim and gets paid back first if the business is liquidated. This makes it extremely challenging to get more financing, as new lenders are hesitant to take a backseat to an existing creditor.

At Business Loan Warrior, we demystify complex financing so you can make confident decisions. Compare tailored funding options, from SBA loans to lines of credit, all through a single, secure application. Find the right capital to fuel your growth at Business Loan Warrior.