You're probably looking at a property you own, want to buy, or need to refinance, and the loan conversation keeps coming back to one question: what is it worth?

That number drives more than paperwork. It shapes how much a lender may advance, how much cash you need to bring in, how the deal is structured, and whether the file feels financeable at all. A business owner often sees valuation as an appraiser's issue. An underwriter sees it as the backbone of the credit decision.

If you understand commercial real estate valuation from the borrower's side, you make better moves earlier. You gather the right records, pressure-test weak assumptions, and avoid walking into a financing request with a value opinion that won't survive review.

Table of Contents

- Why Commercial Real Estate Valuation Matters for Your Loan

- The Three Core Approaches to Property Valuation

- Calculating Value with the Income Approach Step by Step

- How Lenders Use Valuation in Underwriting Decisions

- Avoiding Common and Costly Valuation Pitfalls

- A Borrower's Due Diligence and Valuation Checklist

- When to Hire an Appraiser or Use Valuation Tools

Why Commercial Real Estate Valuation Matters for Your Loan

When a lender reviews a deal, valuation isn't a side note. It's the number that connects the property to the loan structure. If the valuation comes in lower than expected, the borrower usually feels it in one of three places: lower proceeds, tougher terms, or a larger equity requirement.

That's why smart borrowers don't wait for the appraisal report to tell them what happened. They work backward. They ask what an underwriter will look at, what assumptions will get challenged, and where a value conclusion could break down.

What valuation changes in practical terms

A valuation affects more than the final approval memo.

- Loan size: The lender uses value to test collateral coverage.

- Deal structure: A soft value can push a borrower toward more bridge-like or short-term options. If you're comparing timing and structure, this breakdown of business line of credit vs. bridge loan for real estate deals gives useful context.

- Negotiating position: If you know where value comes from, you can defend strong assumptions and fix weak ones before closing gets delayed.

Practical rule: Don't treat valuation as a mystery number delivered at the end. Treat it as a set of inputs you can prepare for.

A borrower who understands valuation usually submits a cleaner package. Leases tie out. Expenses make sense. Deferred maintenance is disclosed instead of discovered. That doesn't guarantee a perfect outcome, but it gives the file a better chance of holding together once the lender starts testing it.

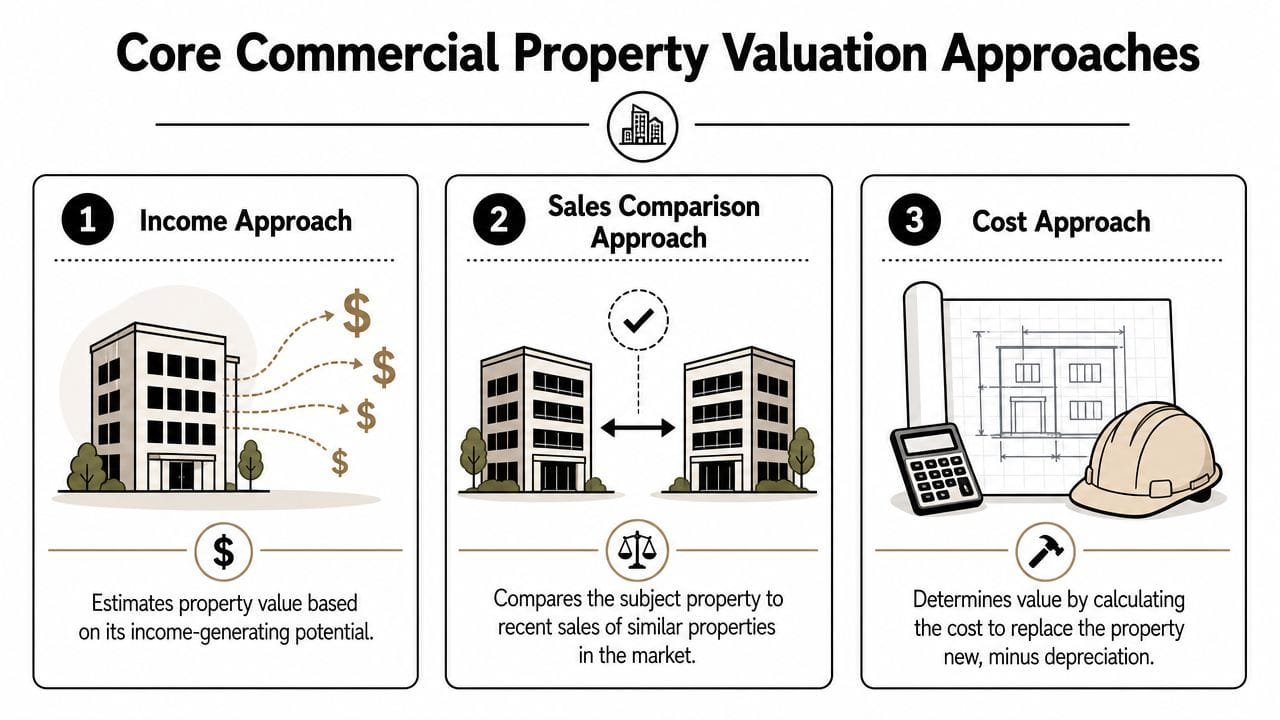

The Three Core Approaches to Property Valuation

Commercial real estate valuation rests on three standard methods. The income approach, the sales comparison approach, and the cost approach are the core framework appraisers use to cross-check value, as described by Lowery Property Advisors' overview of commercial valuation methods.

Three ways to answer the same question

Think of these approaches as three experienced people evaluating the same asset from different angles.

The income approach asks, “What cash flow does this property produce, and what is that income stream worth today?” For leased retail, office, industrial, or multifamily property, this is often the anchor because lenders care greatly about repayment support.

The sales comparison approach asks, “What have similar properties sold for?” Appraisers review comparable sales and adjust for differences such as location, age, size, and condition. In practice, metrics like price per square foot, price per unit, or price per key help normalize unlike deals.

The cost approach asks, “What would it cost to build this asset today, then adjust for depreciation and add land value?” It tends to matter more for special-use properties, newer improvements, or situations where recent sales are sparse.

One method can point the way. A second method tells you whether the first one still makes sense.

If you want a broader industry-level comparison, this roundup of real estate property valuation methods is a solid companion read because it lays the approaches side by side in plain language.

Which method usually carries the most weight

Borrowers often ask which method “wins.” The better answer is that the property type decides the weighting.

For a stabilized, income-producing building, the income approach usually gets the most attention. For a generic building in an active market with recent comparable sales, sales comparison can be persuasive. For a unique facility with few good comps, cost may become more important than owners expect.

A weak borrower move is trying to force every property into the same valuation story. A lender won't do that. If the building is a machine shop in a rural market, the review won't look like a suburban strip center with multiple recent sales. Borrowers who understand that early tend to prepare more realistic expectations.

Calculating Value with the Income Approach Step by Step

For lending, the income approach is often the main event. The industry standard formula is Value = NOI / Cap Rate, and FNRP's commercial investing data notes that typical investment returns in major markets range from 6% to 12% annually, with the average commercial real estate return measured at 9.5%. That same framework treats property value as the present value of future income, which is why underwriters scrutinize both NOI and the cap rate so closely.

Start with the income the property can realistically produce

The first mistake many owners make is starting with the income they hope to achieve. Underwriting starts with income the property can support.

A simple flow looks like this:

Potential Gross Income

This is the scheduled rental income if all rentable space performs as expected under the current or supportable lease structure.Less vacancy and credit loss

Not every dollar billed becomes a dollar collected. Even strong properties need a realistic vacancy and collection assumption.Effective Gross Income

This is the income left after those reductions.

Here's a simple example for illustration.

| Line Item | Amount |

|---|---|

| Potential Gross Income | $1,000,000 |

| Less Vacancy and Credit Loss | $50,000 |

| Effective Gross Income | $950,000 |

| Less Operating Expenses | $300,000 |

| Net Operating Income | $650,000 |

The table isn't a market claim. It's just a clean way to see the mechanics.

Subtract operating expenses to reach NOI

Net Operating Income, or NOI, is the number lenders care about because it reflects the property's income after normal operating expenses. This typically includes items such as property taxes, insurance, repairs, maintenance, and management.

What doesn't belong in NOI causes a lot of confusion. Debt service doesn't belong there. Owner-specific income taxes don't belong there. One-time personal or discretionary costs usually don't belong there either. The point is to measure the property's operating performance, not the owner's individual accounting style.

For owners preparing their own estimate, discipline is most important.

- Use actual leases, not handshake assumptions: If rent bumps aren't documented, don't expect full credit for them.

- Normalize expenses: If the owner deferred repairs for years, the lender may still underwrite a realistic repair burden.

- Separate operating costs from capital items: Replacing a roof isn't the same thing as paying monthly janitorial expense, but both still matter to credit.

For owners dealing with a local appraisal process, this guide for Texas commercial property owners is useful because it shows how property records, condition, and market support can influence the final opinion.

Borrowers get into trouble when they present cash flow like a sales pitch. Underwriting wants a durable income stream, not a best-case forecast.

Apply the cap rate carefully

Once you have NOI, the cap rate converts that income into value. Lower cap rates generally indicate lower perceived risk and push values higher. Higher cap rates signal more risk and pull values down.

The formula is straightforward:

Value = NOI / Cap Rate

If the NOI in the sample table is $650,000 and the cap rate used is 0.08, the indicated value would be $8,125,000.

That math is simple. Choosing the right cap rate isn't.

Cap rates carry the market's view of risk, property quality, tenant strength, lease durability, and location. Two properties with similar income can land at very different values if one has stronger tenancy, better condition, or a market with better liquidity.

In valuation, borrowers sometimes over-focus on the arithmetic and under-focus on the judgment. The spreadsheet won't save a valuation if the assumptions are weak. A lender will usually spend more time debating the sustainability of NOI and the reasonableness of the cap rate than checking whether you can divide one number by another.

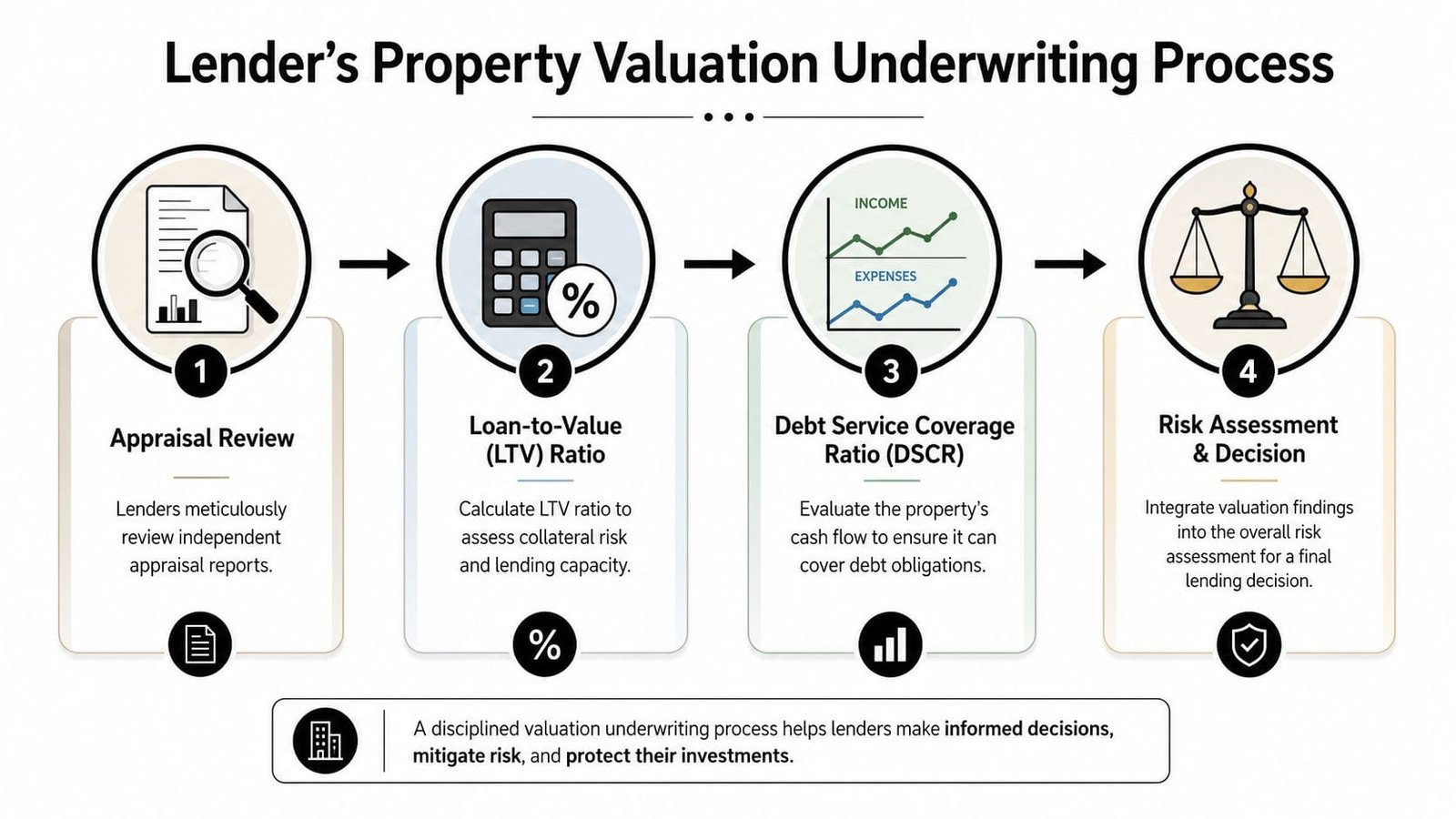

How Lenders Use Valuation in Underwriting Decisions

An underwriter doesn't read a valuation report for curiosity. The report feeds the credit decision. The lender wants to know whether the property supports the requested loan amount and whether the property's income supports repayment.

Collateral support and cash flow support

Two underwriting ideas dominate the conversation.

First is Loan-to-Value, or LTV. The lender compares the requested loan to the appraised value to judge collateral risk. If the value comes in lower than expected, the same loan request suddenly looks more aggressive.

Second is Debt Service Coverage Ratio, or DSCR. That test asks whether the property's income can cover the proposed debt payments with room to spare. A property can have decent collateral value and still struggle on cash flow, or the reverse.

That's why valuation and underwriting are tied together, not handled in separate silos.

To see how that review fits into a broader project finance file, this overview of construction project financing is helpful, especially when value depends partly on completion, lease-up, or cost control.

A short visual explanation can help if you want to see how lenders think through the sequence.

Why values can fall while income looks stable

This is one of the most frustrating parts of the borrowing process for owners. The property may be operating about the same, but the value still drops.

That can happen when cap rates move. Altus Group's discussion of major valuation methods notes that cap rates for office and retail have widened by 100 to 150 basis points since 2022, which can lower values even when NOI stays stable. For borrowers, the practical result is reduced refinance proceeds or tighter financing eligibility as lenders adjust for current debt costs.

Stable rent doesn't guarantee stable value. If the market demands a higher return, the same income stream is worth less.

That's why borrowers need to prepare for lender questions beyond trailing revenue. Underwriters will ask whether leases are near rollover, whether tenants are durable, whether expenses are climbing, and whether the market now requires a different risk premium than it did when the property was last financed.

Avoiding Common and Costly Valuation Pitfalls

Most valuation problems in loan files don't come from obscure technical issues. They come from ordinary borrower assumptions that don't hold up under review.

The mistakes that weaken a file fast

The most common one is overstating income. Owners count space as fully rentable when it isn't, treat temporary occupancy as permanent, or assume future rents without support. If the file depends on perfect performance, the lender will haircut it.

Another mistake is understating operating expenses. Taxes get estimated too lightly. Repairs get buried. Management gets ignored because the owner self-manages. Underwriting usually normalizes those items because a property has to work as real estate, not only under one owner's habits.

A third problem is forgetting major physical issues that can change how a lender sees value. Roofs, HVAC systems, parking lots, drainage, and deferred maintenance may not always hit NOI directly in the way owners expect, but they can still reshape the lender's risk view and reduce proceeds.

Consider this quick borrower-side screen before you submit numbers:

- Check lease quality: Are rent rolls matched to executed leases and current payment behavior?

- Check expense realism: Do your reported operating costs reflect how an outside owner would run the asset?

- Check physical condition: Would a site visit reveal repairs you haven't budgeted for?

If a value estimate only works when every assumption goes right, it probably won't survive underwriting.

What to do when comps are thin or missing

Many small business owners often get stuck, especially in rural markets, niche property types, or unusual owner-user facilities.

When direct comparables are scarce, value can still be developed using loan constants and stabilized income potential rather than market sales, as explained in JDM Partners' guide to valuing commercial real estate without comps. That approach matters in SBA and acquisition lending because a borrower can't always wait for a perfect set of comparable sales to appear.

What doesn't work is pretending weak comps are strong comps. A distant sale, a different asset class, or a distressed transaction may still inform the story, but it shouldn't be treated as clean support. In thin markets, borrowers are better served by a sober stabilized-income case than by forcing a market-sales narrative that won't persuade the lender.

A Borrower's Due Diligence and Valuation Checklist

Before a lender orders anything, a borrower can do a meaningful pre-underwriting review. Good valuation prep isn't fancy. It's organized, documented, and skeptical of easy answers.

Documents that matter before the lender asks

Start with the paper trail. An underwriter wants to reconcile the property story quickly.

- Gather leases and amendments: Make sure rent rolls match signed documents, renewal options, and current occupancy.

- Pull operating statements: Year-to-date and historical statements should clearly show recurring income and recurring expenses.

- Collect property records: Tax bills, insurance, surveys, environmental reports, and service contracts often answer questions before they become conditions.

A borrower who submits partial records usually triggers more lender conservatism, not more flexibility.

Stress test your story before underwriting does

Best practice in the field is not to rely on one method alone. Appraisers often average two or more approaches and stress test variables like cap rates and rental growth, as noted in Rentana's write-up on commercial real estate valuation methods. Borrowers should think the same way.

Run a simple internal challenge process:

- Lower your expected rents and ask whether the deal still works.

- Raise likely expenses and see what happens to property cash flow.

- Review physical risks such as near-term repairs that could affect lender comfort.

- Compare more than one valuation lens instead of betting everything on a single number.

The cleaner your own downside analysis is, the fewer surprises you'll have once the lender starts asking hard questions.

This doesn't mean you need to produce a formal appraisal on your own. It means you should know where your value conclusion is sturdy and where it's vulnerable. Borrowers who do that tend to present more credible requests and negotiate from a stronger position.

When to Hire an Appraiser or Use Valuation Tools

Borrowers often ask whether they can shortcut the process with online tools. Sometimes they can. Sometimes that's a costly mistake.

When software is enough

Valuation tools are useful for early-stage screening. If you're deciding whether to pursue a site, testing rough deal assumptions, or comparing scenarios, software can save time. It can also help borrowers avoid paying for a full appraisal on a deal that clearly doesn't pencil out.

If you're sorting through options, this overview on selecting valuation software is a practical starting point because it frames what these tools can and can't do well.

Use software for preliminary judgment. Use it to ask better questions. Don't use it as proof that a lender should accept your number.

When a professional appraisal is worth paying for

A certified appraiser becomes important when the property is unusual, the market is thin, the structure is more complex, or the loan request leaves little room for valuation error. The more your deal depends on a precise value conclusion, the less sense it makes to lean on broad estimates.

This is especially true when the property has mixed uses, specialized improvements, irregular tenancy, or a weak comparable-sales set. In those cases, a detailed appraisal does more than satisfy a requirement. It helps frame the credit story in a way a lender can underwrite.

Borrowers also need to remember that some loan products will expect more than a quick estimate. If you're exploring higher-speed or asset-based funding paths, this review of hard money business loans can help you understand where valuation speed matters and where lender caution still shows up.

A good appraisal won't rescue a weak deal. But it can prevent a financeable deal from stalling because the borrower relied on a rough estimate long after the file needed real support.

If you're preparing to buy, refinance, or access equity from commercial property, Business Loan Warrior can help you evaluate financing options before valuation issues derail the process. You can start with a single application, review funding paths that fit your deal, and move into underwriting with a clearer picture of what lenders will care about.