You're probably here because the money has a job already.

Maybe it's a piece of equipment that would remove a bottleneck. Maybe it's inventory before a busy season. Maybe it's payroll pressure that keeps showing up a few days before receivables clear. Most owners don't start by wondering how lenders score applications. They start by needing capital fast, then discover that the lending process feels opaque, slow, and full of rules nobody explained upfront.

What separates an approval from a rejection usually isn't the form itself. It's whether your application answers the lender's real question: if we lend this business money, what makes repayment likely and predictable? That answer comes from your numbers, your documents, and the way the whole file fits together. If you want to understand how to qualify for business loan options that fit your company, you need to think less like a borrower asking for help and more like an underwriter measuring risk.

Table of Contents

- Thinking Like a Lender Before You Apply

- The Five Pillars of Business Loan Qualification

- Gathering Your Loan Application Toolkit

- Matching the Right Loan to Your Business Profile

- Strategic Moves to Boost Your Approval Odds

- Common Pitfalls and Your Pre-Application Checklist

Thinking Like a Lender Before You Apply

A lender isn't reading your application the way you do. You're focused on need. The lender is focused on durability.

Take a common scenario. A business owner wants funding for a second location because the first one is doing well and demand is there. From the owner's side, that feels like a growth story. From the lender's side, it becomes a series of harder questions. Is the first location producing steady cash, or did it have one good stretch? Will the new debt be supported by existing operations, or does repayment depend on a future plan that hasn't happened yet? If sales dip for a period, does the business still stay above water?

That's why so many owners feel blindsided by rejection. They think they applied for opportunity financing. The lender reviewed it as a stress test.

A loan file gets stronger when the repayment story is obvious without explanation.

This is also why surface-level advice doesn't help much. “Have decent credit” or “bring your paperwork” isn't wrong, but it misses the point. Lenders are trying to see whether your business behaves in a stable, verifiable way. Clean records matter because they prove consistency. Clear use of funds matters because it shows discipline. A realistic repayment path matters because lenders don't want guesses.

If you need a practical primer before assembling your package, this guide to understanding business loan applications is useful because it frames the process from the borrower's side without pretending every loan works the same way.

The right mindset is simple. Don't ask, “What do I need to say to get approved?” Ask, “What would a cautious lender need to see to get comfortable?” That question leads to better decisions before you ever submit anything.

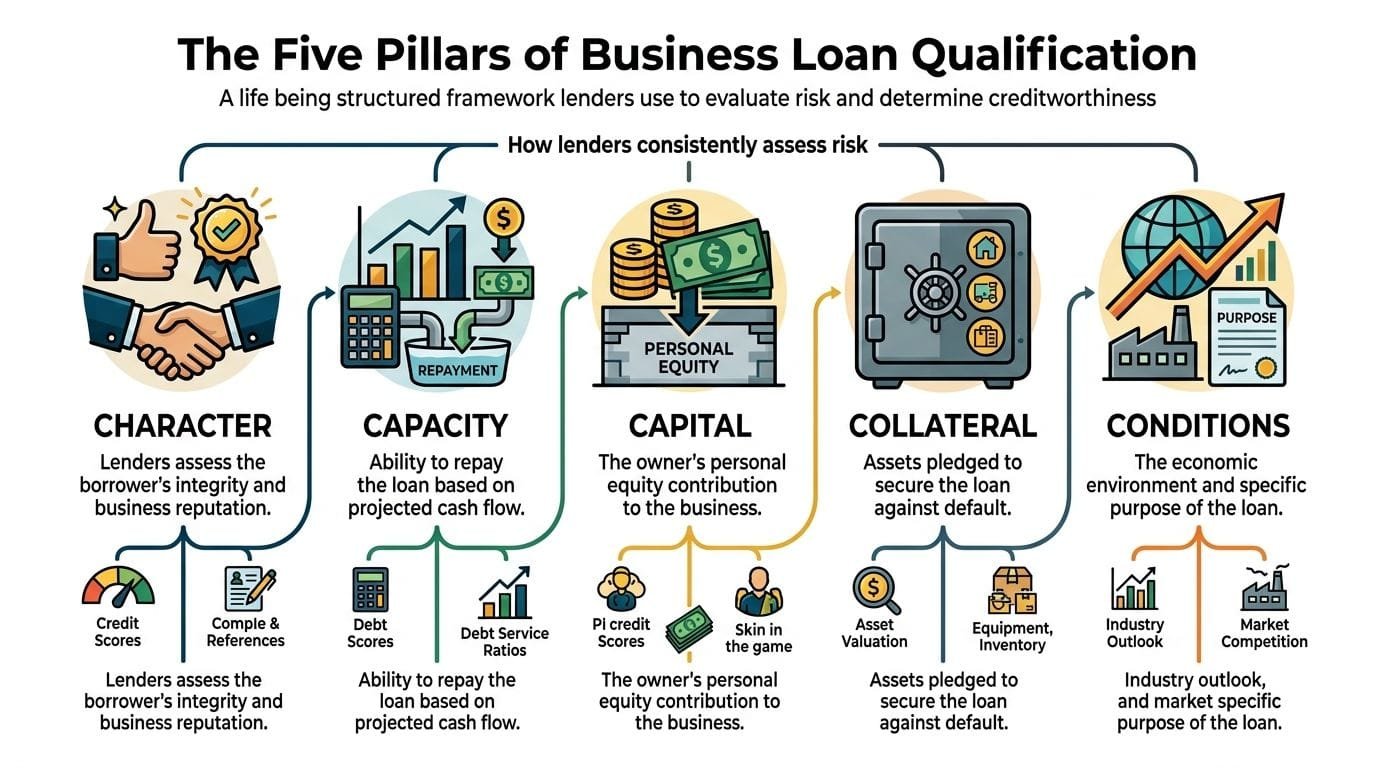

The Five Pillars of Business Loan Qualification

A lender can overlook one weak spot. Two weak spots can still work if the strengths are clear and documented. But when the whole file depends on hope, approvals get hard fast.

These five pillars are the checks lenders keep coming back to. They are not scored in isolation. They are weighed together. That trade-off matters. A borrower with average credit but strong cash flow may be easier to approve than one with good credit and weak repayment capacity.

Character

Character is the lender's trust test. It shows up in personal credit, business credit, payment history, tax compliance, overdrafts, liens, and how well the owner explains the business.

Credit often decides which lenders will even review the file. Banks usually expect stronger personal credit than online lenders do, and lower scores often push borrowers toward higher-cost products or smaller approvals. If you want a clearer sense of where you stand, this guide to business loan credit score requirements breaks down how lenders tend to tier applicants.

A lower score does not always kill the deal. It does change what the lender needs to see elsewhere. If credit is bruised, cash flow usually has to be cleaner, reserves usually have to be stronger, or collateral has to reduce the lender's downside.

Capacity

Capacity is the repayment test.

This is the pillar owners misunderstand most often because they lead with revenue. Underwriters care about the money left after payroll, rent, taxes, existing debt, and normal operating costs. Strong deposits help, but they do not fix thin margins or erratic account activity.

Many lenders use debt service coverage to judge whether the business can carry another payment with room to spare. In plain English, they want to see a cushion, not a break-even story. If the new payment only works when sales stay high every month, the file is fragile.

I have seen this trade-off play out constantly. A company with modest sales but steady margins can qualify more easily than a higher-revenue business that burns cash and juggles obligations.

Capital

Capital is the owner's financial commitment to the business and the business's ability to absorb stress. Lenders look for retained earnings, cash on hand, reasonable liquidity, and evidence that the owner did not build the company entirely on borrowed money.

This matters most when the loan purpose involves growth. Expansion requests get tougher when the business has no reserves and the owner is putting in nothing. The lender starts asking a fair question. If the plan is so sound, why is every dollar of risk being shifted to the lender?

Capital rarely carries a weak file by itself. It does make a lender more comfortable when another area is only average.

Collateral

Collateral gives the lender a second way out if repayment fails. Equipment, vehicles, inventory, receivables, or real estate can all help, depending on the lender and the loan type.

Owners often assume unsecured financing is automatically better. Sometimes it is. Sometimes it just means the lender tightens every other requirement. No collateral usually leads to more pressure on credit, cash flow, pricing, or personal guarantee strength.

That is the trade-off. Pledging assets can improve approval odds or terms, but it increases what you stand to lose if the business cannot perform.

Conditions

Conditions are the facts around the request. Why do you need the money, why now, how will it be used, and does that use fit the way the business operates?

Lenders tend to get more comfortable when the purpose is easy to verify and tied to repayment. Buying equipment that increases production is easier to underwrite than asking for a large lump of working capital with no clear explanation. Expansion can make sense. It usually works best when the current operation is already stable enough to support the added risk.

Time in business and revenue also sit under this pillar because they help establish context. The Small Business Administration's guidance on lender and loan eligibility reflects a basic truth across commercial lending. Lenders want operating history they can review and business performance they can verify.

The practical takeaway is simple. Approval is rarely about checking every box perfectly. It is about showing enough strength across the file that a lender can live with the weak spots. That is how borrowers with imperfect credit still get approved, and why some clean-looking applications still get declined.

Gathering Your Loan Application Toolkit

A file gets declined in quiet ways before anyone says no. The numbers may be good enough, but the bank statements are incomplete, the entity name does not match across documents, or the financials raise questions the owner did not answer up front.

That is why document prep matters more than many owners expect. Underwriters do not approve stories. They approve files they can verify.

Build the file a lender can actually use

Expect to provide business and personal tax returns, recent business bank statements, a year-to-date profit and loss statement, and a current balance sheet. Many lenders also ask for formation documents, your EIN confirmation, business licenses if they apply, and debt schedules showing what the business already owes.

The exact stack changes by lender and loan type, but the goal stays the same. The lender is trying to verify three things. The business exists as presented, the cash flow is real, and the request fits the company's current capacity.

If your records live across email, accounting software, and a desk drawer, fix that first.

For a practical look at what underwriters notice in transaction activity, review these business bank statements before you submit your package.

Know what each document is doing for you

Tax returns establish history. They carry more weight when a lender wants proof that earnings were not just a short recent spike.

Bank statements test that history against real cash movement. I have seen owners show a decent profit on paper and still run into trouble because deposits were inconsistent, transfers were masking weak revenue, or low balances kept showing up at the wrong times. That does not always kill the deal. It does shift the burden to cash flow support, reserves, or a stronger explanation.

The profit and loss statement shows current performance. The balance sheet shows whether the business has enough liquidity and financial stability to absorb the new debt. If the P&L looks solid but the balance sheet is strained, a lender may still proceed, but expect tighter terms, a lower loan amount, or more focus on recent bank activity.

That trade-off matters. Weak credit can sometimes be offset by strong cash flow. Thin collateral can sometimes be offset by clean financial reporting. Missing or sloppy documents do not offset anything. They usually make every weak spot look worse.

Missing paperwork does not just slow underwriting. It makes risk harder to measure, and harder-to-measure risk rarely gets the benefit of the doubt.

Larger requests and many SBA loans may also require a business plan or written use-of-funds explanation. For newer businesses, projections can help, but only if they are tied to real assumptions such as signed contracts, purchase orders, capacity increases, or documented demand. Optimistic spreadsheets without support do not help much.

Use this checklist before you upload anything:

- Check recency first: Make sure statements, financials, and entity documents are current.

- Match names exactly: The legal business name should appear the same way on tax returns, bank accounts, and formation records.

- Explain the use of funds clearly: “Working capital” is usually too broad by itself. Spell out inventory, payroll support, equipment, hiring, or another specific use.

- Include a debt schedule: List existing loans, monthly payments, and remaining balances so the lender does not have to piece it together from credit reports.

- Add brief notes for unusual items: A revenue dip, one-time expense, ownership change, or temporary disruption is easier to underwrite when you explain it plainly and document it.

The cleanest file does not always belong to the strongest business. It often belongs to the owner who made verification easy and answered the obvious questions before the lender had to ask.

Matching the Right Loan to Your Business Profile

A lot of denials happen before underwriting ever gets to the hard part. The owner picked the wrong loan category.

If you apply for a traditional bank term loan when your business is young, your credit is only fair, or your documentation is still thin, you may get rejected even if another loan type would have been realistic. Qualification isn't one universal standard. It changes with the product, the lender, and what part of your file is strongest.

Where owners get mismatched

Traditional loans reward strength across the whole file. That usually means established operating history, stronger credit, and clean documentation. SBA options can sometimes work for borrowers who need structure and flexibility but can still document the business clearly. Startups or younger companies may need to lean on alternative documentation when tax history is limited.

Some newer businesses can bypass the usual time-in-business issue for certain SBA 8(a) or microloan paths by providing proof of reliability such as vendor contracts or utility payments instead of historical tax returns, based on The Credit People's startup loan overview. The same source notes that some alternative lenders may approve startups with credit scores as low as 600 when bank statements and projections are strong.

That's why product matching matters more than many owners realize. If your file is light on history but strong on current activity, you need a lender and loan type that respects current evidence.

For a useful side-by-side look at government-backed options, review SBA loan comparisons across 7(a), 504, and microloans.

Business Loan Qualification Requirements at a Glance

| Loan Type | Typical Credit Score | Time in Business | Best For |

|---|---|---|---|

| Traditional bank loan | Usually stronger credit expectations | Usually better for established businesses | Expansion, major planned purchases, borrowers with clean full documentation |

| SBA loan | Often flexible when the file is otherwise solid | Better for businesses that can document operations well | Long-term growth, owner-occupied real estate, structured working capital |

| Microloan | Can suit borrowers who don't fit conventional bank standards | Can work for newer businesses with alternative support documents | Smaller capital needs, early-stage businesses |

| Online lender loan | May fit lower-score borrowers depending on cash flow | Can work for younger businesses | Faster working capital, bridge needs, borrowers who need flexibility |

| Equipment financing | Credit still matters, but asset support can help | Can be easier when the equipment itself supports the deal | Machinery, vehicles, production equipment |

Use the table the way an underwriter would. Don’t ask which product sounds best. Ask which product matches the profile you can prove.

A business with uneven credit but reliable deposits may be a better fit for an online lender than a bank. A startup with vendor contracts and a lease may have a path through a microloan program even without full tax history. A company buying a hard asset may find equipment financing easier to justify because the lender can anchor the deal to the asset itself.

The wrong application can make a decent borrower look unqualified. The right one can make the same borrower financeable.

Strategic Moves to Boost Your Approval Odds

You apply for a loan on Monday. By Friday, the lender asks two questions that decide the file. Why do you need this amount, and what repays it if sales dip for a month? Owners who can answer both cleanly get farther, even with a few weak spots.

Approval odds improve when the file gives the underwriter a clear reason to say yes. That means presenting strengths in the order the lender is likely to value them, and addressing weaknesses before they become discoveries.

Lead with your strongest approval story

The key trade-off in many business loan files is credit versus cash flow. If personal credit is average but the business shows stable deposits, controlled expenses, and enough room to cover the new payment, lead with operating performance. If revenue is uneven but credit is strong and the business has assets, structure the request so the lender can get comfortable with that support.

This is not about hiding a weakness. It is about giving it context. A lender can work with imperfect credit more easily when bank statements show disciplined cash management. A lender can overlook a thinner operating history more easily when there is strong collateral, repeat customer revenue, or a signed contract that supports repayment.

The opposite is also true. A borrower with a good score can still get declined if recent cash flow does not support the debt. Owners often overestimate how much credit can carry a weak business file. In practice, repayment capacity usually wins.

Another move that helps is choosing lenders whose credit box matches your profile. The Federal Reserve Banks’ small business credit survey shows approval outcomes vary widely by lender type, with banks, online lenders, and finance companies each underwriting risk differently, as noted in the 2024 Small Business Credit Survey.

A strong application does not try to look perfect. It makes the risk easy to understand and easier to price.

This walkthrough gives a useful lender-side view of how owners can tighten their approach before submitting anything:

Act before underwriting finds the problem

Underwriters get cautious when they find an issue the borrower should have explained upfront. Fix what you can. Frame what you cannot.

Use this before the first application goes out:

- Correct credit report errors early: Small inaccuracies can drag down a file for no good reason.

- Ask for an amount the business can carry: A larger request increases payment pressure. A request that is too small can signal weak planning if it does not solve the problem you are borrowing to fix.

- State the repayment source in one sentence: For example, monthly receivables from service contracts, recurring customer deposits, or savings from replacing expensive short-term debt.

- Offer collateral where it changes the decision: Asset support can improve terms or move a borderline file into approval.

- Answer underwriting requests quickly and completely: Delays create doubt about recordkeeping and can push closing farther out.

- Clear up tax problems before they appear in diligence: If lines, payment plans, or unresolved balances are in the background, understand them first. This guide to small business tax liabilities is a practical place to start.

Strong files rarely win because everything is perfect.

They win because the owner understood the trade-offs, presented the strongest compensating factors first, and removed avoidable reasons for concern.

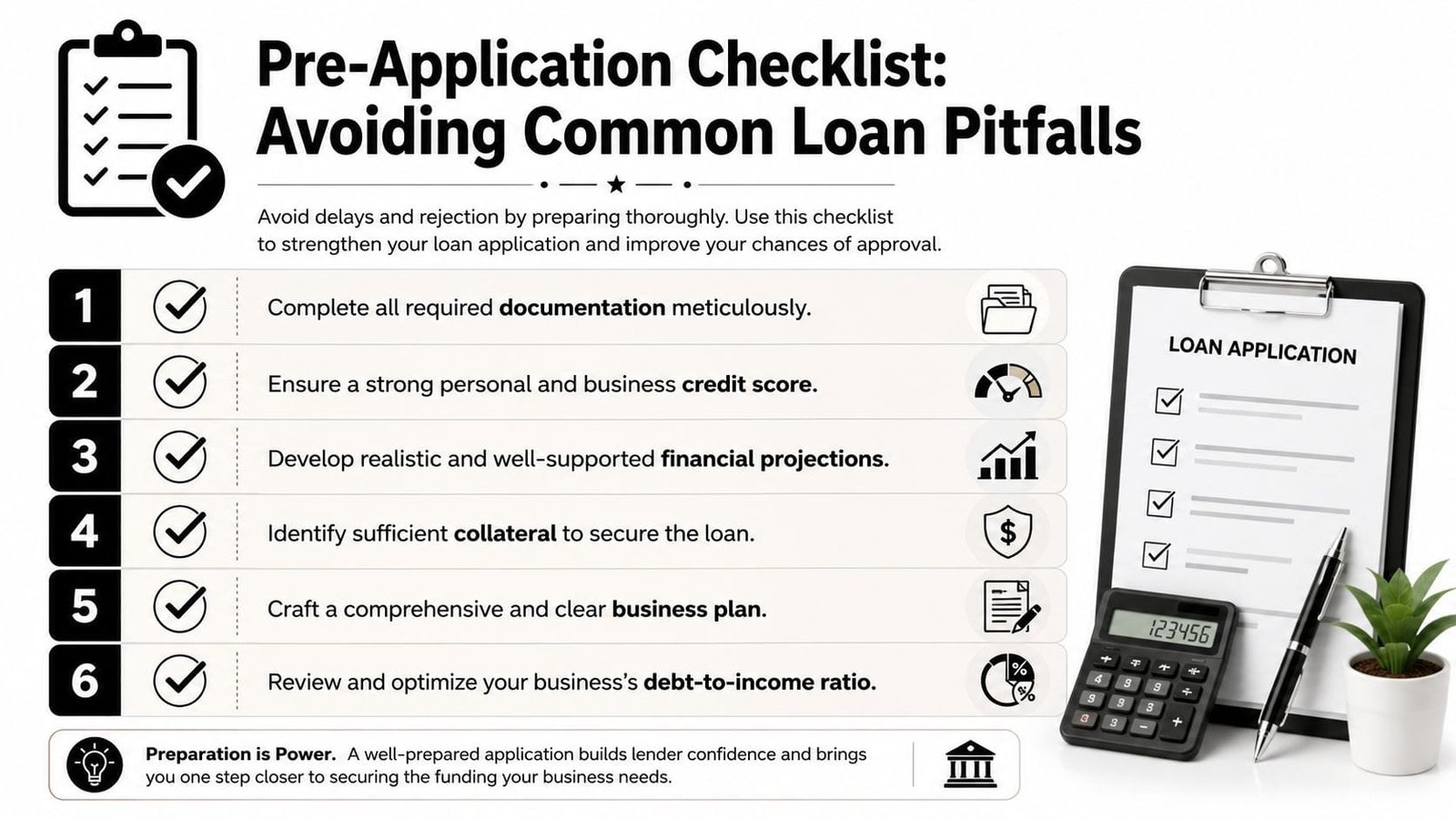

Common Pitfalls and Your Pre-Application Checklist

Most bad outcomes don’t come from exotic underwriting formulas. They come from preventable mistakes.

A primary cause of immediate rejection is an incomplete package with missing or outdated documentation, and common mistakes also include failing to correct credit report errors, underestimating the loan amount needed, or not defining a clear repayment source, according to the U.S. Chamber’s guide to applying for a small business loan.

A few pitfalls deserve special attention. If your business has unresolved tax issues, don’t assume a lender will ignore them. Tax debt can complicate approvals because it raises questions about lien risk, payment priority, and cash strain. If that applies to you, get clear on your position first.

Run this checklist before you apply anywhere:

- Confirm every required document is current: Old statements and incomplete returns make the file look unmanaged.

- Review your credit before the lender does: Fix obvious errors and be ready to explain legitimate blemishes.

- State the exact use of funds: Vague requests weaken confidence.

- Tie the loan to repayment: Show what income services the debt.

- Decide whether collateral helps your case: Don’t rule it out automatically.

- Check for hidden issues: Tax problems, entity mismatches, and unexplained cash swings should be addressed upfront.

A clean application doesn’t guarantee approval. A messy one almost guarantees resistance.

If you approach the process this way, you stop applying like someone asking for a favor. You start applying like a business that’s ready for credit.

If you want to explore funding options without turning the process into a guessing game, Business Loan Warrior can help you review customized loan paths, check pre-approval options, and compare financing that fits your business profile without a no-fee application becoming another paperwork dead end.