Orders are late. One supervisor is texting drivers, another is chasing invoices, and your bookkeeper is asking why cash is tight even though sales look fine. The team is busy all day, but the business still feels one bad week away from a problem.

That's where most owners start thinking about operations in a company. Not as a textbook topic, but as the daily reality of getting work done, getting paid, and not losing control while you grow. If your business is trying to add locations, buy equipment, hire ahead of demand, or qualify for better financing, operations stop being a back-office issue. They become the proof that the business can handle more capital without creating more chaos.

That matters because small businesses make up 99.9% of U.S. business entities and employ 45.9% of the private-sector workforce, yet the average small business lasts only 8.5 years, according to small business statistics compiled here. The businesses that last usually don't have perfect conditions. They have repeatable systems.

Table of Contents

- Your Company's Engine What Operations Really Mean

- The Core Functions of Company Operations

- Mapping Your Key Business Processes

- Essential KPIs to Measure Operational Health

- Identifying and Fixing Common Bottlenecks

- A Stepwise Strategy to Improve Your Operations

- How Strong Operations Make Your Business Loan Ready

Your Company's Engine What Operations Really Mean

A lot of owners hear “operations” and think about the warehouse, the floor, or the back office. That's too narrow. Operations in a company are the full set of systems that turn effort into delivered value and delivered value into cash.

If sales closes the deal but fulfillment misses the date, operations failed. If the team finishes the work but invoicing goes out late, operations failed. If inventory is sitting in the wrong place, labor is scheduled at the wrong time, or nobody can answer a simple status question without three phone calls, that's not bad luck. That's an operational design problem.

Practical rule: Operations are working when the business can deliver consistently without heroic effort from the owner.

In plain terms, operations are your company's engine. Sales brings fuel in. Finance watches consumption. People keep the parts moving. Systems keep timing tight. If one piece is off, the engine still runs, but it burns cash and scares lenders.

Owners who want growth capital should think about operations the same way an underwriter does. Can this business produce predictable results? Can it absorb a loan payment without tripping over preventable mistakes? Can it scale without doubling confusion?

One useful way to look at this is through a formal operational risk management process, especially if your team already feels stretched. It helps you sort normal daily friction from risks that can shut down delivery, damage margins, or disrupt collections.

If your current setup depends on a few people remembering everything, you're not running a system. You're running on memory. That's why a solid operating foundation matters so much, and why guides on business operations and why every business needs a solid system resonate with owners who are tired of solving the same problem twice.

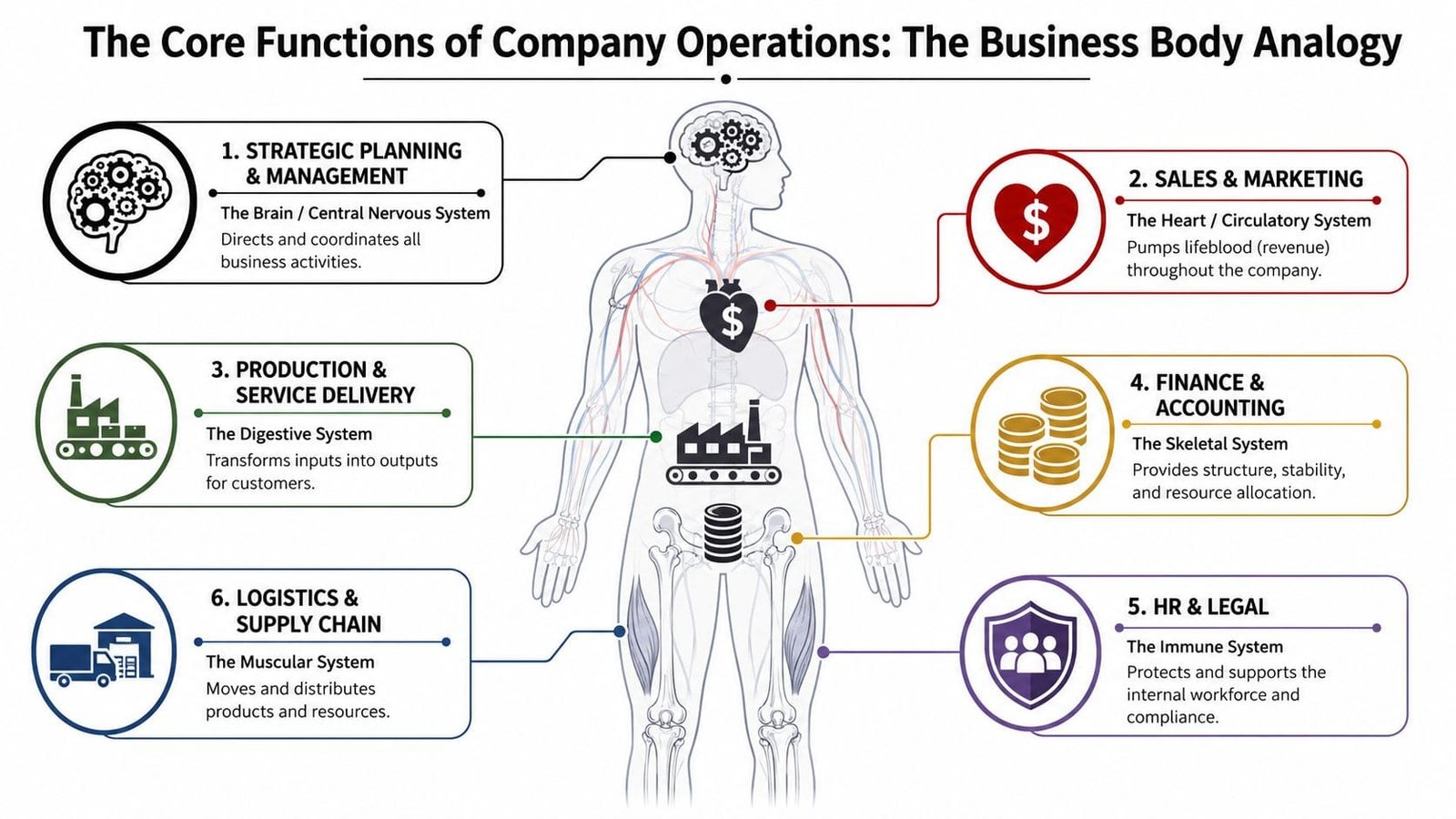

The Core Functions of Company Operations

Think of a business like a body. Each system has a job, but health comes from coordination, not isolated strength. A company with strong sales and weak fulfillment is like an athlete with a strong heart and a broken ankle. Motion stops anyway.

Why departments fail when they act alone

Most operating problems don't start inside one department. They start in the handoff between departments.

Sales promises a custom timeline. Purchasing doesn't hear about it. Production schedules standard work instead. Accounting invoices from the original quote. Customer service gets the angry call. Everyone thinks someone else caused the issue, and in a narrow sense they're all right.

That's why the modern view of operations includes people, finance, and technology alongside production. It also includes workforce design. Data from 2025 indicates that companies that integrated DEI metrics into operational dashboards reported a 23% reduction in operational downtime and a 15% increase in cross-functional coordination speed, according to this discussion of underserved employee needs in operations. If communication, onboarding, and team trust improve, handoffs improve too.

What each function actually does

Here's the practical map.

Strategic management keeps the whole company pointed in one direction. This is where goals, priorities, and trade-offs get decided. If leadership says “grow accounts” but doesn't define margin targets, service levels, or hiring limits, every team makes up its own rules.

Sales and customer acquisition bring in demand. Their operational job isn't just to close. It's to close work the business can actually deliver profitably.

Production or service delivery turns inputs into finished work. In a restaurant, that's kitchen flow and table turns. In a contractor, it's crews, materials, and job sequencing. In an agency, it's onboarding, project scope, approvals, and delivery cadence.

Supply chain and logistics move the right materials, products, or information at the right time. For a retailer, that means purchase orders, receiving, stock placement, and replenishment. For a field service company, it means trucks, tools, and route planning.

Finance and accounting keep structure under the business. They handle billing, payables, reporting, and cash discipline. Good finance doesn't just record the mess after the month ends. It helps prevent the mess.

HR and legal protect the business from internal breakdowns. Hiring, training, scheduling rules, compliance, and performance management all affect throughput more than most owners realize. If you need to Hire LATAM talent to fill operational gaps, treat that as a systems decision, not just a staffing one. Clear roles, onboarding, and communication standards matter more than geography.

IT and systems support keep information flowing. If your team retypes the same data into QuickBooks, spreadsheets, email, and a CRM, your systems aren't supporting operations. They're slowing them down.

A healthy business doesn't ask each department to work harder. It asks them to work in sequence.

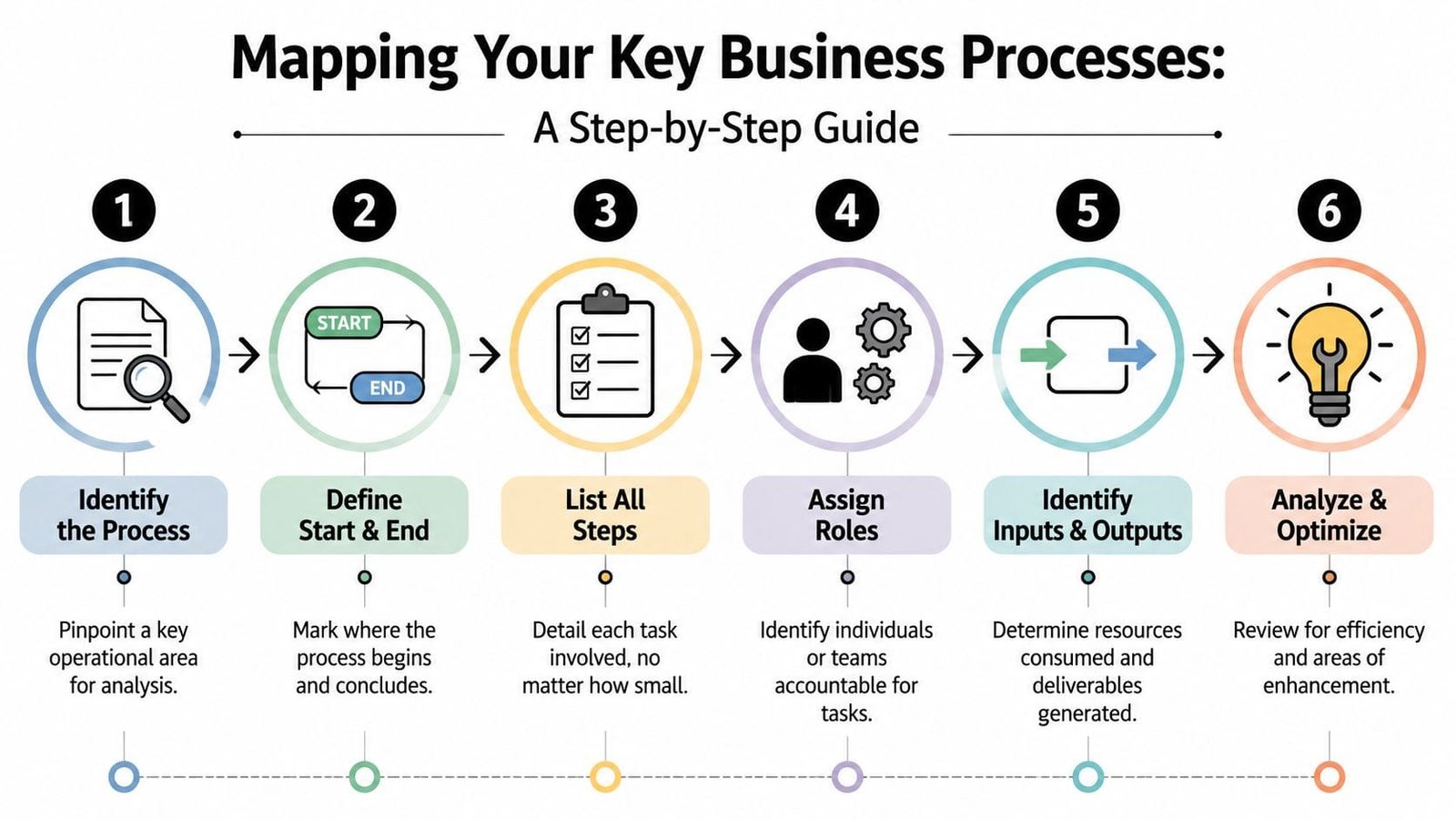

Mapping Your Key Business Processes

Most owners can describe their business in departments. Fewer can draw the actual path from customer request to cash in the bank. That path is where waste hides.

Start with one process. Not ten. Pick the one that touches revenue fastest. For most businesses, that's order to cash, estimate to job completion, or lead to signed contract and first invoice.

Start with one process that touches cash

Take a whiteboard, a Google Doc, or a sheet of paper. Then map the process in the order work happens, not the order you wish it happened.

- Choose the trigger: “Customer signs quote” is a better start point than “sales follows up.”

- Pick the endpoint: “Cash received and job closed” is better than “invoice sent.”

- List every step: Include approvals, waiting time, handoffs, rework, and follow-up.

- Name the owner for each step: Use job titles, not departments.

- Mark where delays happen: Waiting for signatures, missing materials, unclear pricing, or disputed invoices.

- Note what system holds the truth: Email, QuickBooks, a CRM, a spreadsheet, or someone's head.

A quick visual can help if your team has never done this before.

What a useful process map includes

A good process map isn't fancy. It's honest.

Use this simple table format:

| Step | Who owns it | Input needed | Output produced | Common delay |

|---|---|---|---|---|

| Quote approved | Sales | Final scope | Signed proposal | Missing pricing detail |

| Job scheduled | Operations coordinator | Signed proposal | Calendar slot | Crew availability unclear |

| Work completed | Field team | Materials and work order | Delivery confirmation | Material shortfall |

| Invoice sent | Accounting | Completion proof | Customer invoice | Missing paperwork |

| Payment collected | AR or owner | Invoice and terms | Cash received | Customer dispute |

What usually surprises owners is not one huge failure. It's the pile of small pauses. A job sits for approval. An invoice waits for backup. A customer asks for a revised document. Nobody owns the chase. Cash slows down one day at a time.

If you can't map the process on one page, the process is probably carrying extra weight.

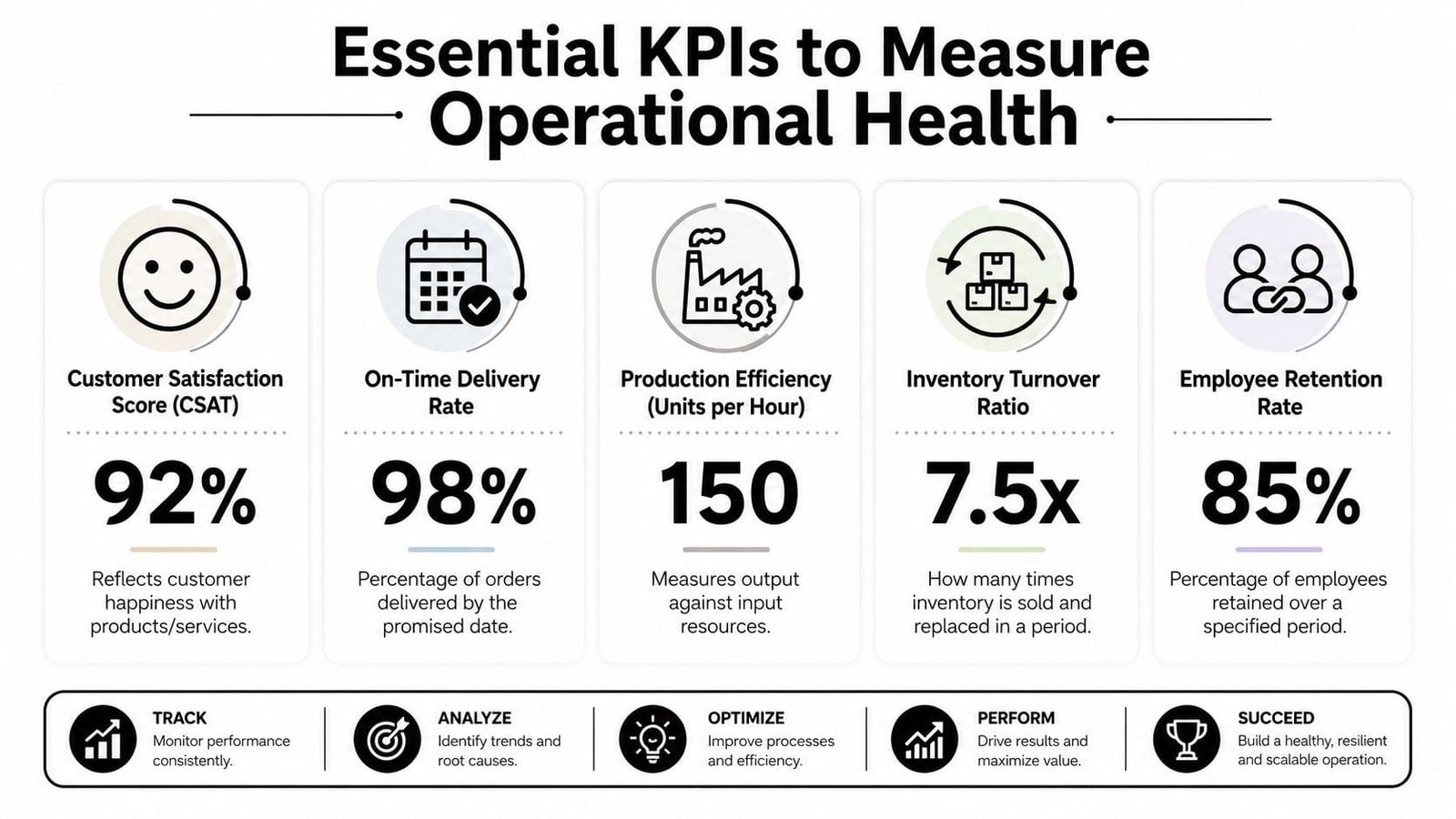

Essential KPIs to Measure Operational Health

A lender doesn't need every metric in your business. They need the right ones. So do you. The best KPIs for operations in a company show whether revenue turns into cash with control, whether labor is productive, and whether the business can recover when something breaks.

The numbers that tell a lender your story

Start with Operational Efficiency Ratio, or OER.

Formula: Operating Expenses / Total Revenue

According to NetSuite's overview of operational efficiency metrics, elite performers in mature markets often keep OER below 60%, while average firms often run above 75%. The same source notes that a 10% reduction in OER correlates with a proportional increase in net profit margins when revenue stays constant. That's why lenders care. Lower waste usually means more room for repayment.

Next is Revenue per Employee.

Formula: Annual Revenue / Total Employees

For U.S. small businesses in the $20M to $50M sales range, the same NetSuite resource says $150,000 to $200,000 per employee signals high operational maturity, while ratios below $100,000 often point to underutilization or overstaffing. That doesn't mean you slash headcount on sight. It means you ask whether labor is deployed correctly.

A third metric matters for tech-dependent firms, distribution-heavy companies, and any business that loses money when systems stall. That's Mean Time to Recovery, or MTTR.

Formula: Total Minutes from Failure to Recovery / Total Incidents

Keep the dashboard small and useful

If a system outage knocks out ordering, dispatch, payments, or communication, MTTR tells you how fast the business gets back on its feet. A practical lender takeaway is simple. Fast recovery suggests discipline. Slow recovery suggests risk. If you're building a tighter reporting package, a working capital scorecard for proving cash runway before renewal can help frame these numbers in a way financiers understand.

Use a short dashboard like this:

- OER: Shows cost control and margin discipline.

- Revenue per Employee: Shows labor productivity.

- MTTR: Shows resilience when operations depend on systems.

- A process-specific metric: For example, days from completed work to invoice sent, if billing lag is your issue.

Watch this: A dashboard should help you make decisions this week. If it only produces interesting charts at month-end, it's reporting, not management.

Identifying and Fixing Common Bottlenecks

Growing businesses usually don't break from lack of effort. They break where work piles up faster than information moves. You can spot the trouble by listening to recurring complaints. “We're waiting on approvals.” “The numbers don't match.” “Customer service didn't know.” “We had the inventory, just not where we needed it.”

The bottlenecks that show up in growing firms

One common bottleneck is manual data re-entry. The symptom is familiar. Staff copy information from email into a quote, then into an invoice, then into a tracking sheet. Errors creep in, and nobody trusts the final report.

Another is information silos. Sales keeps promises in the CRM. Operations tracks delivery in a spreadsheet. Accounting bills from QuickBooks. The customer gets three versions of the truth.

A third is inventory blindness. That doesn't just mean wrong counts in a warehouse. It also means service businesses that don't know what parts are on trucks, contractors that buy emergency materials because purchasing lagged, and restaurants that over-order one item while running out of another.

Then there's reactive maintenance and recovery. If your business depends on software, devices, or connected equipment, outages spill into labor waste and customer frustration quickly. NetSuite notes in its KPI guidance that a 50% increase in MTTR can lead to a 30% rise in total cost of ownership because downtime stretches labor, manual intervention, and related costs, as outlined in its article on operational KPIs and metrics.

Fix the cause, not the symptom

The cheap fix is rarely the right fix. Don't just tell people to be more careful. Change the system.

- For duplicate entry: Pick one source of truth. If customer details start in HubSpot, Salesforce, or Jobber, downstream tools should pull from there instead of relying on retyping.

- For siloed teams: Create one shared operating rhythm. A short weekly review with sales, ops, and finance beats long monthly arguments about what happened.

- For inventory issues: Tighten reorder points, receiving discipline, and location tracking. Even a simple barcode routine is better than memory.

- For recovery problems: Write a basic incident playbook. Who owns the response, who communicates internally, what gets restored first, and what manual workaround kicks in while systems are down?

The biggest mistake is fixing the loudest symptom. A late invoice may look like an accounting issue. In practice, it's often a completion-signoff issue from operations.

A Stepwise Strategy to Improve Your Operations

Owners often think operational improvement requires a full overhaul, expensive software, or a consulting project that nobody has time for. It doesn't. In smaller and mid-sized firms, the best gains usually come from three moves done in the right order: simplify, standardize, then automate.

Simplify first

Don't automate clutter. Remove it.

Take the process map you built and ask blunt questions. Does this approval protect margin, quality, or compliance? If not, why is it there? Does this report trigger a decision, or does it just satisfy habit? Why do two people check the same thing?

Look for:

- Duplicate approvals: Especially on repeat purchases or standard jobs.

- Rework loops: Work that returns upstream because requirements were unclear.

- Status chasing: Calls, emails, and messages that exist only because nobody can see the current state.

- Custom exceptions: Deals or workflows that sound profitable but consume disproportionate time.

Standardize what should not vary

Once you've cut the waste, lock in the better method. Standardization doesn't make a business rigid. It makes outcomes dependable.

That means short SOPs, checklists, templates, naming conventions, and clear ownership. A good SOP fits on one page for most recurring tasks. If your receiving process, onboarding flow, or invoice approval method changes by person, you don't have a process yet. You have preferences.

A few examples work well:

| Area | Standard to create | Why it helps |

|---|---|---|

| New customer setup | One intake form | Reduces missing billing and service details |

| Purchasing | Approval thresholds by role | Prevents delays and owner bottlenecks |

| Job closeout | Required completion packet | Speeds invoicing and dispute handling |

| Incident response | Recovery checklist | Cuts confusion during outages |

For operations tied to facilities, machinery, fleets, or uptime, it also helps to study what modern O&M for reliability leaders looks like in practice. The lesson is simple. Reliability comes from planned routines, not last-minute heroics.

Automate the boring parts

Now automate the steps that are repetitive, rules-based, and easy to break by hand.

Use tools your team will adopt. QuickBooks or Xero for cleaner accounting flow. Zapier or Make for moving routine data between systems. Asana, ClickUp, or Monday.com for assignment visibility. A CRM like HubSpot for lead handoff discipline. A scheduling platform if your crews or appointments create friction daily.

Good automation removes keystrokes and delay. Bad automation hides a broken process behind software.

Start small. Auto-create a task when a proposal is signed. Trigger invoice prep when completion docs arrive. Send internal alerts when inventory hits reorder status. Small wins build trust faster than a giant rollout.

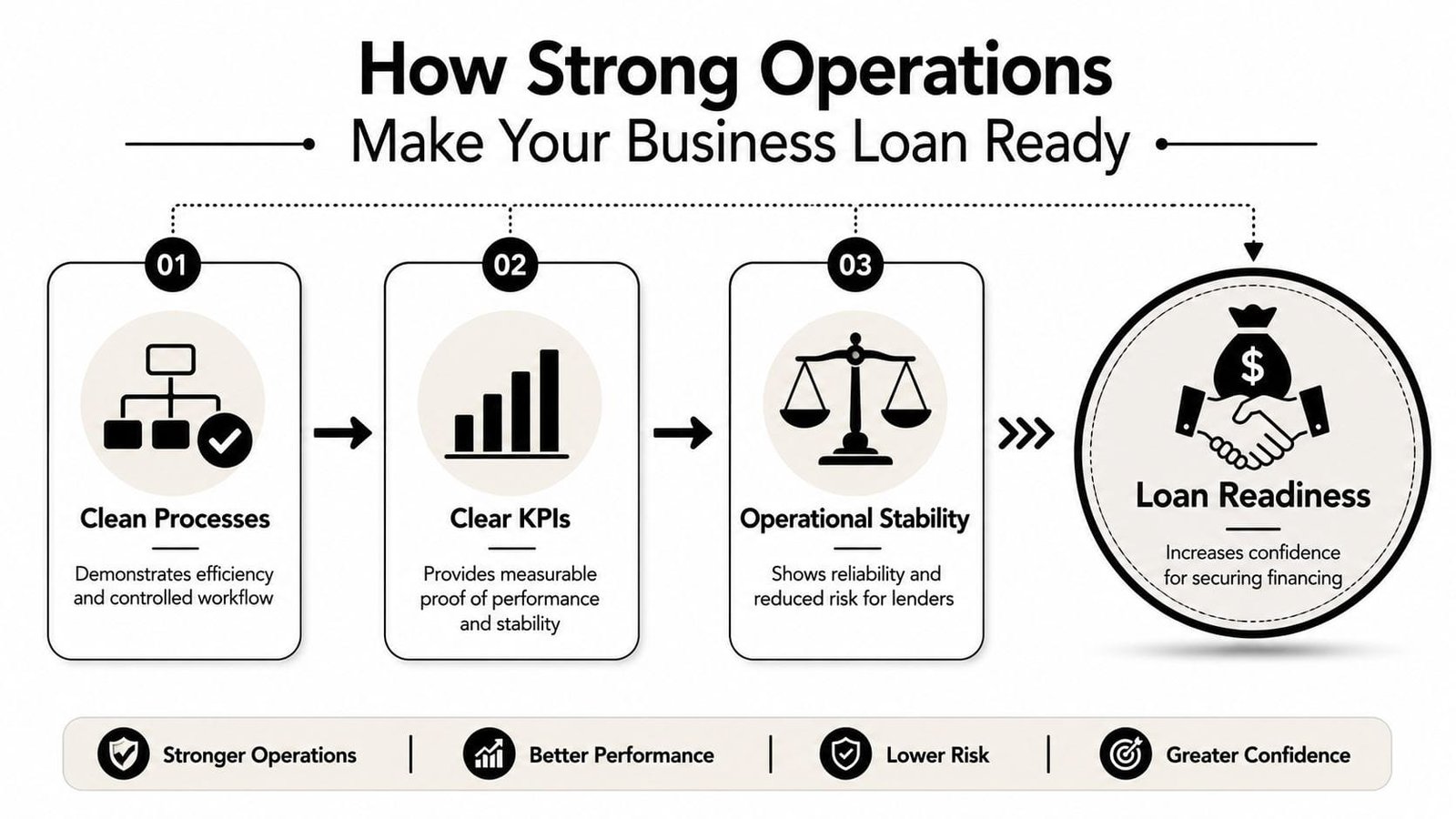

How Strong Operations Make Your Business Loan Ready

When lenders review a business, they're not only asking whether you need money. They're asking whether your company can use money well and pay it back on schedule. Strong operations answer that question better than a polished pitch deck ever will.

What lenders want to see

Lenders like predictability. Operational maturity creates predictability in ways owners can document.

If your process from order to invoice is clean, receivables are easier to trust. If inventory records are current, collateral and working capital are easier to assess. If staffing, purchasing, and scheduling follow standards, growth looks manageable instead of risky.

Operational discipline connects directly to cash flow. NetSuite notes that 43% of small firms cite cash flow as their top operational challenge, and it argues that operations managers should own cash flow forecasting by embedding repayment schedules into production and inventory planning in its article on operations management and funding alignment. That's exactly how a borrower becomes easier to underwrite. Payment obligations stop being separate from daily operations.

Turn operations into a financing advantage

If you want stronger financing options, bring lenders evidence, not optimism.

Use this checklist before you apply:

- Show process control: Document how work moves from sale to delivery to invoice to collection.

- Show metric discipline: Bring OER, labor productivity, and one or two process KPIs that matter in your business.

- Show operational stability: Explain how you handle interruptions, staffing gaps, and system failures.

- Show use of funds logic: Tie the loan to throughput, capacity, or working capital timing. “We need cash” is weak. “We need equipment to remove a scheduling bottleneck that delays billable output” is stronger.

- Show repayment fit: Match expected payments to actual operating cycles, not generic monthly hope.

If you need a practical framework, this funding-focused operations checklist for small business growth is the kind of tool that helps owners package operations and finance together instead of treating them as separate conversations.

A well-run company doesn't just look better on paper. It makes better use of capital once the money arrives. That's the primary goal. Not borrowing because operations are weak, but earning better funding options because operations are strong.

If you're tightening systems so your business is easier to fund, Business Loan Warrior is a practical next stop. You can explore funding options, check pre-approval through a no-fee application, and line up capital that fits the way your business operates, whether you need working capital, equipment financing, expansion funding, or a more flexible cash flow solution.