A subordinated loan is a type of debt that gets repaid only after all senior loans are paid, and lenders often charge 3 to 5 percentage points above senior term loans because they're taking that extra risk. In practice, it acts like a cushion under your bank debt, which can help you secure more traditional financing when your business has outgrown what a bank will lend on its own.

You're probably here because your business is doing well, but not neatly enough for a standard bank package to solve the next problem. Maybe you want to acquire a competitor, open a location, invest in equipment, or fund a product launch. Your bank may like your company, your cash flow, and your plan, yet still stop short because you've hit its senior debt limit.

That's where many owners get stuck. They assume the only options left are to give up equity, delay the opportunity, or accept expensive capital without understanding how it fits. A subordinated loan can be the middle path.

The important point is strategic. This isn't just “riskier debt with a higher rate.” Used well, subordinated debt can serve as catalytic capital. It can absorb more risk in the middle of your capital stack, which can make a larger senior loan possible. In other words, the junior piece may be what enables the safer, cheaper senior piece above it.

That's why smart owners ask not only, “What is a subordinated loan?” but also, “Why would I use one instead of more equity or another bank facility?” The answer usually comes down to control, timing, and structure.

Table of Contents

- Introduction Beyond the Standard Bank Loan

- The Capital Stack Where Subordinated Debt Sits

- Unlocking Growth When Your Business Should Use a Subordinated Loan

- The Price of Position Understanding Risk Rates and Returns

- The Lenders View Covenants and Senior Debt Relations

- How to Negotiate Your Subordinated Loan Agreement

- Frequently Asked Questions About Subordinated Loans

Introduction Beyond the Standard Bank Loan

You find the right acquisition target, the seller is ready, and your bank supports the deal in principle. Then the credit box shows up. The bank will fund part of the purchase, but not enough to get the transaction done.

That gap is where many owners first hear the term subordinated loan.

At a basic level, subordinated debt is a loan that gets repaid after senior debt and before equity. But that definition only tells you where it sits, not why it matters. Its real strategic role is to act as catalytic capital. It helps complete a financing structure that a bank would not support on its own, which can let you pursue growth without bringing in more equity partners.

A good way to frame it is this. The bank covers the portion of the deal it views as safest. Subordinated debt can cover part of the remaining need when the opportunity makes business sense but falls outside standard bank limits. If you want a clearer picture of how those layers work together, this guide to capital stacking in business funding gives useful context.

Owners often hear junior debt, sub debt, and mezzanine debt used almost interchangeably and assume they all mean expensive emergency financing. In practice, healthy companies use subordinated loans for deliberate reasons. They may be buying a competitor, funding an expansion, recapitalizing the business, or closing a deal where senior financing stops short.

Here is the practical point many borrowers miss.

The value of a subordinated loan is not that it is cheap. It usually is not. The value is that it can enable a larger senior loan and create a capital structure that fits the transaction. In other words, you are not only getting more dollars. You are creating a financing package that can carry the deal.

Take a simple example. A bank may lend against receivables, equipment, and proven cash flow, yet still refuse to fund the full purchase price of an acquisition. A subordinated lender may accept that middle position because it is underwriting the company's future cash generation and the strength of the combined business, not only the liquidation value of assets.

That is why subordinated debt deserves a place in growth planning. It is often less about stretching for money and more about building the missing layer that makes the rest of the capital stack work.

The Capital Stack Where Subordinated Debt Sits

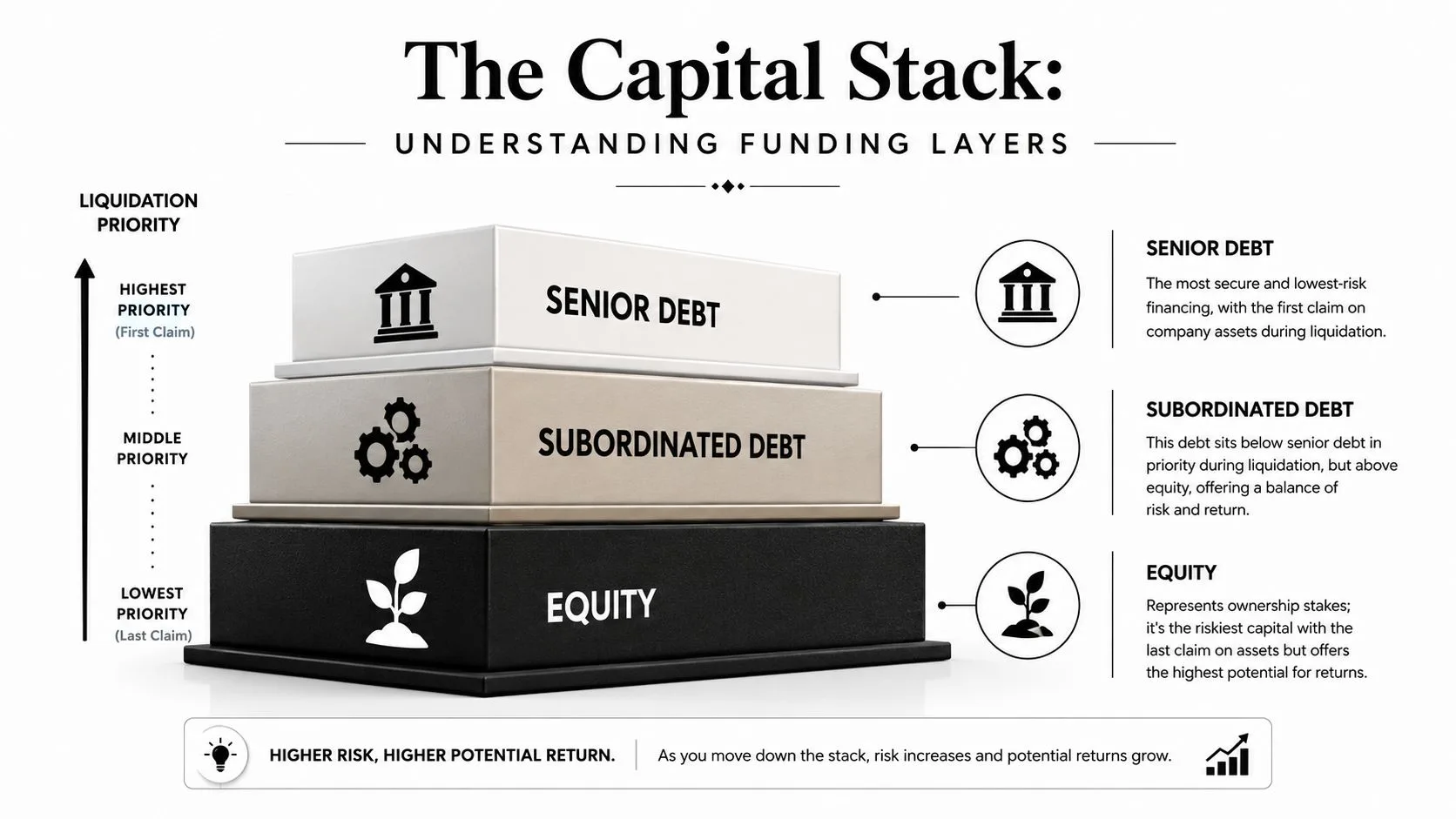

To understand a subordinated loan, you first need to understand the capital stack. That is the repayment hierarchy inside your business. It shows who gets paid first, who waits behind them, and who absorbs losses first if a deal underperforms.

Subordinated debt sits in the middle of that order. Senior debt sits above it. Equity sits below it.

That middle position is the whole story.

A bank or other senior lender has the first claim on repayment and usually the strongest claim on collateral. Owners are last because equity takes the first loss but keeps the upside if the business does well. A subordinated lender accepts the space between those two positions. It is still debt, so it expects repayment on agreed terms. But it accepts that senior lenders get paid first if the company runs into trouble.

Here is why that matters strategically. Subordinated debt often acts as catalytic capital. It fills the layer that lets the rest of the financing structure hold together. In plain English, it can help a business get the full funding package needed for an acquisition, recapitalization, or expansion when a senior lender will support only part of the deal.

If you want a broader primer on how these layers interact, this guide to capital stacking for business funding explains how multiple financing sources fit into one structure.

The capital stack determines more than repayment order. It shapes how much a senior lender will advance, how much risk each party accepts, and whether a transaction can close at all.

Senior debt vs subordinated debt at a glance

| Feature | Senior Debt (e.g., Bank Loan) | Subordinated Debt (e.g., Mezzanine Loan) |

|---|---|---|

| Repayment priority | First in line | Paid after senior debt |

| Risk to lender | Lower | Higher |

| Typical collateral position | Often secured with stronger claim | Often behind senior lender's claim |

| Pricing | Lower relative cost | Higher relative cost |

| Role in a deal | Core financing layer | Gap-filling or growth-enabling layer |

| Position in liquidation | Paid before junior claims | Paid before equity, after senior debt |

What “subordinated” means in real life

During normal operations, this ranking can feel invisible. Payments go out on schedule, financial reporting gets delivered, and each lender watches performance through its own set of loan terms.

The ranking becomes very real in a workout, default, or sale of assets. Senior debt gets repaid first from available proceeds. Only after those obligations are satisfied can subordinated lenders recover value. Equity receives whatever remains, if anything remains.

That payment order explains why subordinated lenders price differently from banks and ask harder questions about future cash flow. They are not relying on first claim status to protect them. They are relying more heavily on the company’s ability to grow, refinance, or generate enough earnings to support every layer above equity.

A useful way to read the stack is this: senior debt protects the downside, equity absorbs the first loss, and subordinated debt connects the two. That connecting role is why it can make a larger transaction possible even though it costs more than bank debt.

Unlocking Growth When Your Business Should Use a Subordinated Loan

You find a strong growth opportunity. The numbers make sense. Your bank is willing to lend, but only up to the amount its credit box can support. You still need one more layer of capital to finish the deal without bringing in a large new equity partner.

That is the point where a subordinated loan often earns its place.

When the bank is supportive, but capped

A senior lender may like your business, your repayment history, and your plan. It may still stop short of the full amount you need because its rules are tied to collateral value, cash flow coverage, or concentration limits. That gap does not always signal a bad transaction. Often, it reflects the bank’s need to stay in a safer position.

A subordinated loan fills that middle layer.

It works like the extra support beam in a building plan. The project may already be sound, but one added structural element lets the rest of the financing hold together.

That makes subordinated debt useful when the business has a clear use for capital and a credible path to repay it, but the senior facility alone will not carry the whole load.

Situations where it can make sense

Owners usually consider subordinated debt when timing matters and giving up more equity would be expensive, disruptive, or unnecessary.

Common examples include:

- Buying a business or competitor: The bank may lend against equipment, inventory, and receivables, but not against the full value of customer relationships, earnings potential, or expected synergies. In those cases, a layered structure that includes a business acquisition loan can help complete the purchase.

- Funding expansion ahead of revenue: You may need capacity now for a new product line, location, or contract, even though the cash flow will show up later.

- Handling an ownership buyout: A subordinated loan can help finance a partner exit or management buyout while limiting dilution.

- Restructuring the balance sheet: Some companies use it to support a recapitalization when they want more flexibility than a senior lender will provide on its own.

The strategic reason owners use it

The plain definition of subordinated debt focuses on repayment order. The more useful business definition is different. It is capital that helps you secure a larger senior facility than you could likely obtain with only bank debt and equity.

That distinction matters.

If your financing plan is a stack of blocks, senior debt sits at the top of what a bank feels comfortable carrying. Equity sits at the bottom and absorbs the first hit if results disappoint. Subordinated debt sits between them and gives the stack more depth. That added layer can make the full structure workable without requiring the owner to write a much larger equity check.

For a business owner, the strategic question is usually not, “Is this loan expensive?” The better question is, “What does this layer allow me to do that I could not do with senior debt alone?”

Sometimes the answer is simple. It lets you close the acquisition. It lets you expand before a competitor does. It lets you complete an ownership transition while keeping control concentrated with the existing team.

A practical way to evaluate the fit

A subordinated loan tends to fit best when four things are true:

- The opportunity has a clear business purpose, not just a desire for extra cash.

- Senior debt is already part of the structure, but it does not cover the full need.

- Future earnings are expected to support both layers of debt.

- Preserving ownership or completing the transaction now has real strategic value.

If one of those pieces is missing, subordinated debt can create strain instead of flexibility.

A short visual explanation can help if you’re evaluating this structure with a leadership team.

Owners often treat subordinated debt as a backup option. In many growth transactions, it is the layer that helps the full financing package come together.

The Price of Position Understanding Risk Rates and Returns

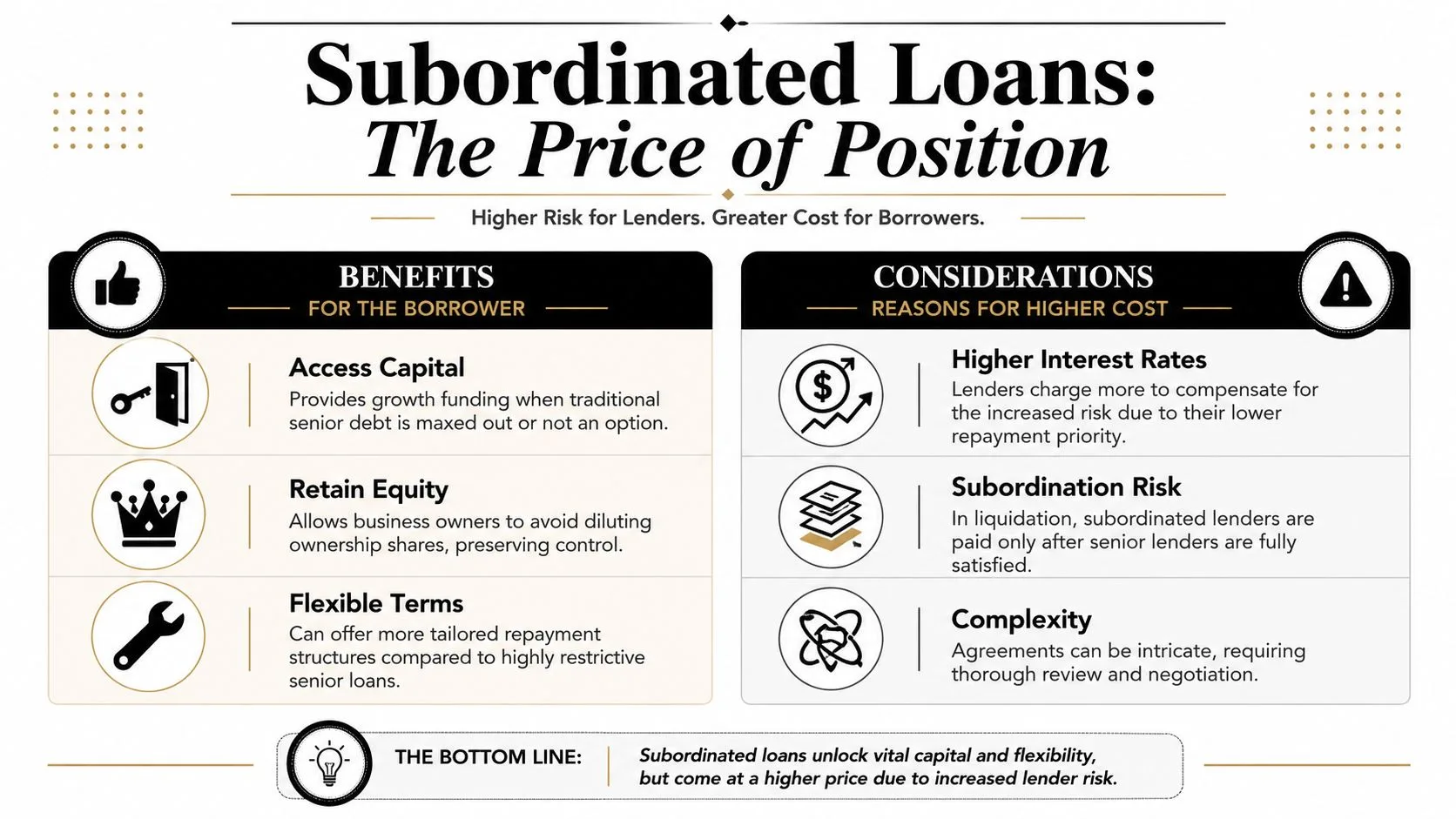

A business owner usually feels the cost of subordinated debt at the exact moment it solves a problem. The bank is willing to lend a meaningful amount, but not enough to finish the acquisition, fund the expansion, or complete the buyout. A subordinated lender steps in to fill that gap, and the price is higher because that capital is doing a specific job. It is making the rest of the financing package possible.

Why the pricing runs higher

Subordinated lenders sit behind the senior lender in the repayment line. In plain terms, they get paid after the bank if the deal goes badly. That lower place in the capital stack means more risk, so they ask for more return.

The useful way to view that premium is not as a penalty. It is the price of adding a layer of capital that can help you get a larger senior facility than the bank would extend on its own. Senior lenders often want first claim on collateral, sometimes through a blanket lien on business assets, and they size their loans conservatively because of that position. Junior capital gives the structure more support below the bank.

That is why subordinated debt often shows up in transactions where speed, ownership retention, or deal size matter more than getting the lowest possible rate.

The stated rate is only one part of the cost

A subordinated loan is priced more like a package than a plain bank note. Two term sheets can look similar at first glance and produce very different outcomes for your cash flow and exit flexibility.

You may see:

- Cash interest: Scheduled interest paid during the term.

- Payment-in-kind interest: Interest added to the loan balance instead of paid now, which preserves cash today but increases what you owe later.

- Warrants or an equity kicker: A small right to share in upside if the company performs well.

- Fees and prepayment terms: Costs that affect what happens if you refinance, sell, or repay early.

A simple comparison helps. One lender may quote a lower cash rate but add PIK interest and a stiff prepayment charge. Another may quote a higher current rate with fewer strings attached. The second offer can be cheaper in practice if your plan is to refinance quickly after the business grows.

That is why strong borrowers ask for the full economic picture, not just the coupon.

Measure price against what the capital helps you accomplish

Subordinated debt raises your overall financing cost. That part is real. The more important question is whether it creates enough value to justify that cost.

If the extra layer lets you complete an acquisition with strong cash flow, keep more ownership, or close a transaction before the opportunity disappears, the higher rate may be rational. If it is funding a weak plan or covering a cash shortfall with no clear payoff, the same pricing can become a burden fast.

Banks look at that distinction closely. Their underwriting still centers on repayment capacity, collateral, and deal quality, which is why it helps to understand what banks consider for loans before you add junior debt to the structure.

The strategic test is simple. Subordinated capital should do more than add money. It should help create a financing structure that gets a worthwhile transaction done on terms your business can realistically carry.

The Lenders View Covenants and Senior Debt Relations

Once subordinated debt enters the deal, you no longer have a simple borrower-bank relationship. You now have a borrower, a senior lender, and a junior lender, all operating under an agreed order of rights.

This is a three party relationship

The central document is usually the subordination agreement or intercreditor arrangement. That agreement spells out who gets paid first, what the junior lender can do if the borrower defaults, what actions require senior lender consent, and when payments may be blocked.

For the owner, this matters because the legal language shapes daily flexibility. A subordinated loan may look helpful on the term sheet, but the intercreditor terms determine how much room you have if the business hits a rough patch.

Subordinated debt is also a mature instrument in formal capital frameworks. In regulatory systems such as the EU’s KMG 2019 and Basel standards, subordinated loans can qualify as Tier 2 capital, meaning they can absorb losses up to the point of insolvency while still ranking ahead of hybrid securities and common equity, according to the FMA summary of subordinated capital treatment.

That doesn’t make the product simple. It does mean lenders and regulators understand where it fits.

What changes once junior debt enters the picture

Senior lenders usually care about cash flow coverage, collateral, and downside control. Junior lenders care about those things too, but they also care about whether the company can grow enough to justify the extra risk they’re taking.

That often shows up in covenant design. You may see restrictions tied to debt levels, distributions, additional borrowing, capital expenditures, or asset sales. The junior lender may accept more flexibility than the bank in some areas, but the combined package can still be tight.

A useful way to prepare is to review what banks consider for loans before discussions get advanced. It helps you think like the credit committee, not just like the borrower.

You should also understand how collateral rights intersect with existing liens. If your bank already has a blanket claim on business assets.

A subordinated loan doesn’t replace your bank relationship. It makes that relationship more complex, and that complexity lives in the documents.

How to Negotiate Your Subordinated Loan Agreement

Owners sometimes focus too heavily on rate and ignore the terms that create trouble later. That’s a mistake. In subordinated debt, the non-rate provisions can change the economics of the deal just as much as the coupon.

Terms worth pushing on

Start with the points that most affect cash flow, control, and exit flexibility.

-

Interest structure

Ask how much must be paid currently and how much can accrue. A payment-in-kind feature can help during an integration or growth period, but it also compounds what you owe. -

Repayment profile

Match the amortization and maturity to the business plan. If the company needs time to digest an acquisition or complete an expansion, a short fuse can create refinancing pressure at the worst moment. -

Prepayment penalties

This clause matters more than many owners expect. If the business performs well, you may want to refinance out of the junior debt. Make sure the penalty doesn’t erase the benefit of paying it off early. -

Covenants and default triggers

Read beyond the headline events of default. Some agreements define default broadly enough to create problems over technical issues, not just missed payments. -

Warrants or equity participation

If the lender wants an upside kicker, negotiate the percentage, exercise mechanics, and what happens on a sale or recap.

What to do before you sign

Bring experienced counsel into the process before the term sheet hardens into documentation. You’re not just reviewing a loan. You’re reviewing a layered legal relationship with priority rules, restrictions, and negotiated remedies.

If you want a refresher on the basic building blocks behind enforceable documents, this overview of understanding legal agreements for CLM is a practical starting point.

Use this short checklist in lender meetings:

- Model the downside: Show what happens if growth is slower than planned.

- Test the refinance path: Ask when and how you can take the loan out.

- Clarify blocked payment terms: Know when payments to the junior lender can be suspended.

- Review cure rights: Understand what time you get to fix a covenant breach.

- Get definitions in writing: “Cash flow,” “default,” and “material adverse change” shouldn’t be left vague.

A well-negotiated subordinated loan supports the business. A poorly negotiated one can box you in right when you need options most.

Frequently Asked Questions About Subordinated Loans

Some of the biggest decisions come down to a few practical questions. Here are the ones owners usually ask after they understand the basic structure.

Common questions on subordinated loans

| Question | Answer |

|---|---|

| Is subordinated debt the same as equity? | No. It's still debt, which means it has repayment terms and lender rights. But it sits closer to equity in the capital stack because it gets paid after senior debt. |

| Why would I use it instead of raising equity? | Usually to preserve ownership and control. The tradeoff is a higher cost of capital and tighter legal terms. |

| Can I prepay a subordinated loan? | Often yes, but not always cheaply. Many agreements include prepayment penalties or negotiated make-whole style protections. |

| Is this only for distressed businesses? | No. Healthy companies use subordinated debt when they're pursuing growth and senior lenders won't fund the full need on their own. |

| What happens in a default? | The answer depends on the documents, but the junior lender's rights are usually limited by the subordination agreement and the senior lender's priority. |

| Does subordinated debt usually have collateral? | It may be unsecured or effectively junior in claim. What matters most is that it sits behind the senior lender in repayment priority. |

| Is mezzanine financing the same thing? | Mezzanine financing often uses subordinated debt as its base structure, sometimes with added equity features like warrants. |

| When does this financing make the most sense? | When you have a credible growth use for the capital, a clear repayment path, and a senior lender willing to participate if a junior layer supports the deal. |

One more practical distinction matters. If your business needs routine working capital, a subordinated loan may be too complex and too expensive for the job. It tends to fit best when the transaction itself creates value, such as an acquisition, recapitalization, or major expansion.

The best borrowers for this structure usually know exactly why they need it. They aren't filling a random cash hole. They're building a deal stack that supports a specific outcome.

If you're weighing senior debt, subordinated financing, or a blended package, Business Loan Warrior can help you compare funding paths and find a structure that fits your growth plan without wasting time on the wrong lenders.