If your payables feel like a moving target, you're not running a sloppy business. You're running a busy one. In a lot of SMBs, accounts payable lives in inboxes, text threads, sticky notes, and one overworked employee's memory. Then a vendor calls about a missed payment, your controller says cash is tighter than expected, and you realize the issue isn't the bills. It's the system.

That matters more than most owners think. Accounts payable management isn't back-office housekeeping. It's one of the clearest indicators of whether you control cash, or whether cash controls you. When AP is messy, planning gets distorted, vendor trust erodes, and lenders see noise instead of discipline. When AP is clean, you get timing, advantage, and options.

Table of Contents

- Why Your AP Process Is More Than Just Paying Bills

- Building Your Accounts Payable Policy Foundation

- Designing Your Invoice Capture and Approval Workflow

- Selecting the Right AP Automation Software

- Tracking Performance with Key AP Metrics

- How Strong AP Management Unlocks Better Funding

Why Your AP Process Is More Than Just Paying Bills

Most owners treat AP like janitorial work. Get invoices in, get checks out, keep vendors quiet. That mindset is expensive.

A weak AP process creates the same kind of drag as driving with the parking brake half on. The business still moves, but slower, hotter, and with more wear than necessary. You pay late because approvals stall. You miss opportunities because you don't know what cash is already spoken for. You make decisions based on your bank balance instead of your real obligations.

That's why I push owners to stop calling AP an admin function. It's a cash control system. If you know what's due, who approved it, when it should be paid, and which vendors matter most, you stop reacting and start steering.

Cash visibility beats cash guessing

Good accounts payable management gives you a forward view of cash, not just a rearview mirror. You can see upcoming obligations before they hit. That changes how you buy, how you negotiate, and when you pull financing.

If you operate across regulated environments or have cross-border compliance pressure, expense governance matters too. A practical reference on that side of the house is this DORA and NIS2 expense guide, especially if your team mixes procurement, expenses, and vendor payments in one workflow.

Practical rule: If one person has to “remember what's due,” you don't have an AP process. You have a dependency risk.

There's also a direct link to working capital. Owners who tighten AP usually discover cash leaks they've normalized. Duplicate invoices, rushed payments, unclear terms, and poor timing all chip away at liquidity. If you want a broader operating view, this guide on improving cash flow fits naturally beside a stronger AP process.

AP shapes relationships and leverage

Vendors don't just care whether you pay. They care whether you pay predictably. Predictability gives you credibility. Credibility gives you room to negotiate terms, resolve disputes calmly, and protect supply when things get tight.

That same discipline helps internally. Department heads stop tossing invoices over the wall. Finance stops firefighting. You get a cleaner month-end close because the liabilities are already organized instead of being discovered late.

In plain English, AP is where operating discipline shows up in cash form.

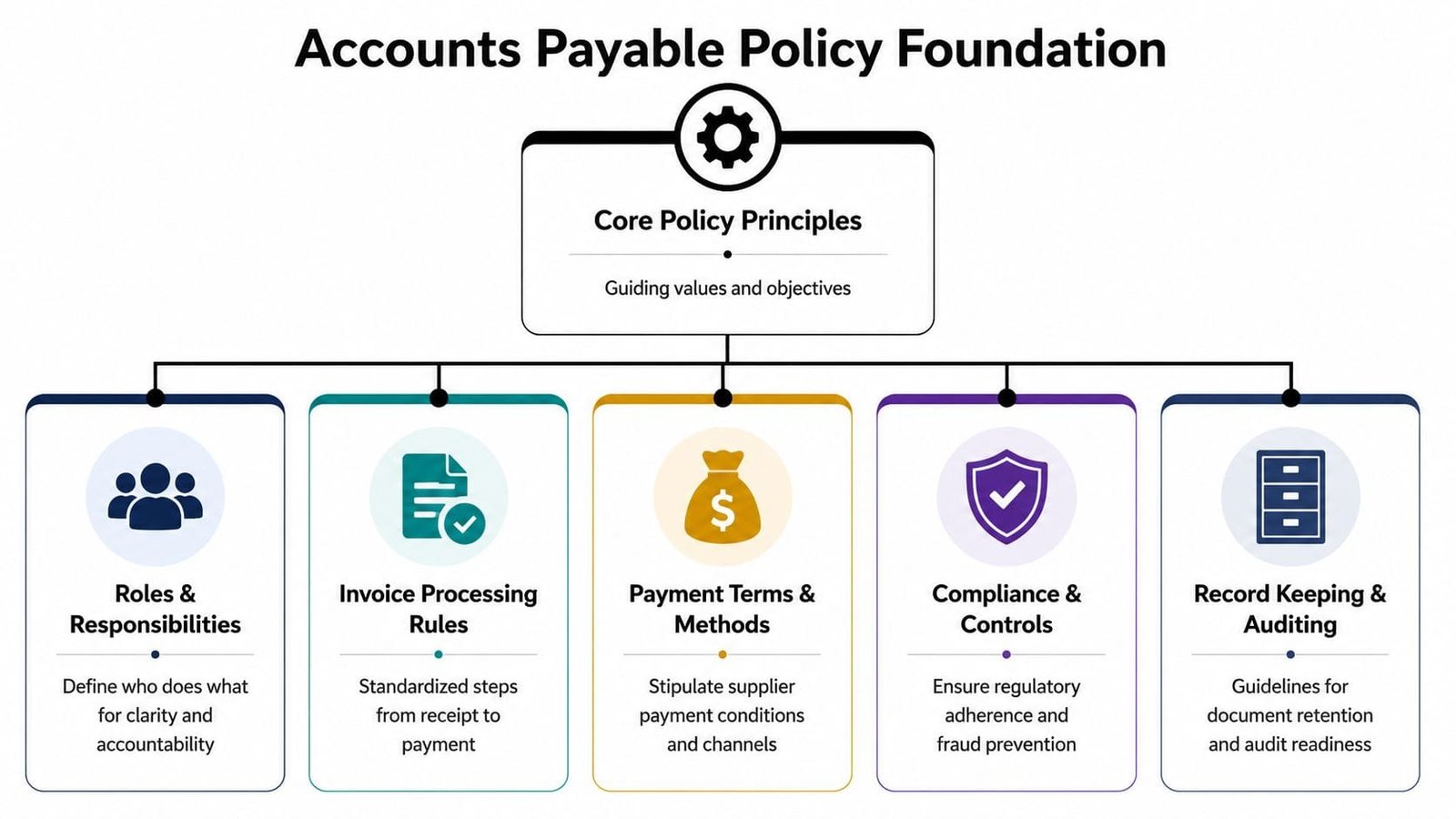

Building Your Accounts Payable Policy Foundation

You can't automate chaos. You can only speed it up.

Every business needs an AP policy, even if the finance team is small. An AP policy is like the foundation under a warehouse. Nobody praises the concrete, but if it's weak, everything above it cracks. A documented policy tells your team what must happen before money leaves the company. It removes guesswork, reduces arguments, and protects you from paying the wrong vendor, the wrong amount, at the wrong time.

According to the Association for Financial Professionals, businesses with formal, documented AP policies experience 60% fewer instances of duplicate payments and payment fraud than businesses using informal processes, according to AFP. That's not a paperwork win. That's real risk reduction.

Start with authority and separation

The first job of policy is deciding who can do what.

In smaller companies, owners often let convenience override control. The same employee receives invoices, enters them, updates vendor banking, and prepares payments. That may feel efficient. It's not. It's fragile. If that person makes a mistake, gets pressured, or goes around the process, you have no brake pedal.

Your policy should define:

- Who receives invoices: Use one AP inbox or one intake path. Don't let invoices scatter across sales reps, project managers, and branch admins.

- Who codes expenses: Someone has to assign the invoice to the correct general ledger account, class, job, or department.

- Who approves spending: Match approval authority to business responsibility. A plant manager should approve plant spend. A department lead should approve department spend.

- Who releases payment: Keep payment execution separate from invoice approval whenever possible.

The principle is simple. No single person should control the entire chain from vendor setup to payment release.

Separate custody, approval, and payment. Even in a lean finance team, split the risk where you can.

Build rules vendors can't bypass

A good AP policy also governs the front door. If vendor onboarding is loose, the rest of the process stays vulnerable.

Set a standard onboarding checklist and use it every time. Verify the legal business name, tax documentation, remittance details, contact information, and agreed payment terms before the vendor enters your accounting system. If a vendor asks to change banking instructions, require independent confirmation through a known contact. Never rely only on an email request.

Your policy should also address invoice standards. Require invoices to include the agreed billing entity, invoice number, service or product description, dates, and any supporting documents your team needs. If you accept incomplete invoices, you train vendors to send more of them.

A practical AP policy usually includes these five rule groups:

Approval hierarchy

Spell out which roles approve which types of spend. Keep it clear enough that nobody asks, “Whose signoff do I need?”Invoice intake rules

One intake channel. One naming convention. One place to store documents.Vendor onboarding controls

Standard verification before activation, and controlled handling of banking changes.Payment scheduling rules

Define payment run timing, exceptions, and who can authorize out-of-cycle payments.Record retention and audit trail

Keep invoices, approvals, vendor records, and payment evidence in a searchable system.

If you don't write the rules down, your team will invent them on the fly. That's how AP turns into folklore instead of process.

Designing Your Invoice Capture and Approval Workflow

Most AP bottlenecks begin at the first touchpoint. Not payment. Intake.

Invoices arrive by email, PDF, vendor portal, mail, and sometimes a phone photo forwarded by a site manager. If you don't control capture, the rest of the workflow never gets clean. You'll keep paying for rework, confusion, and approval delays.

Capture invoices in one lane

Your first move is centralization. Every invoice should enter through one managed channel, usually a dedicated AP email inbox or an AP module inside QuickBooks, Xero, NetSuite, Sage Intacct, or Microsoft Dynamics.

The workflow should look like this:

Receipt

The invoice lands in one place. Not ten.Data extraction

A team member or OCR tool captures vendor name, invoice number, date, amount, due date, and line details.Validation

AP checks whether the invoice is complete, tied to a valid vendor, and supported by a purchase order, contract, or internal approval when required.Coding

The cost gets assigned to the right ledger account, department, class, location, or project.Approval routing

The invoice goes to the correct approver based on rules, not on whoever happens to be online.Payment scheduling

Once approved, the invoice gets queued for payment based on terms and cash priorities.

If your team is evaluating tools or process ideas, this practical guide on how to automate invoice processing is useful because it focuses on the mechanics owners have to solve.

Approve by rule, not by chasing people

The old manual approach is familiar. AP receives an invoice, prints it, emails someone, waits, follows up, waits again, then escalates because the due date is close. That isn't a workflow. It's organized begging.

Approval rules should be predefined. Route by vendor, amount, department, location, or expense type. If the primary approver is out, the system should escalate or reroute. If an invoice doesn't meet requirements, it should be flagged before approval, not after payment.

Here's where many SMBs get this wrong. They make every invoice follow the same path. That clogs the system. A recurring utility bill should not move like a one-off capital expenditure. A contract-backed software invoice should not need the same detective work as a surprise consulting charge.

Use a tiered logic:

- Routine recurring invoices can follow a lighter path if they match known terms.

- PO-backed invoices should be matched before approval.

- Exception invoices need extra review because they carry more risk.

Fast AP doesn't mean rushed AP. It means the routine items move without drama, and the unusual items get real scrutiny.

When this workflow is working, your finance team spends less time chasing signatures and more time deciding when to pay. That's where AP starts affecting strategy. If you want to connect payment timing with broader financing decisions, this article on streamlining vendor payments using financing tools is the right next read.

Selecting the Right AP Automation Software

At a certain size, manual AP becomes a tax on growth. More invoices mean more keying, more forwarding, more follow-ups, more exceptions, and more month-end cleanup. Owners often delay software because they don't want another subscription. That's the wrong lens. The greater cost is keeping a weak process in place.

A 2025 Goldman Sachs report found that businesses automating their AP processes can lower invoice processing cost from an average of $15 per manual invoice to under $3 per automated invoice, a reduction of over 80%, according to Goldman Sachs. If your invoice volume is climbing, that gap stops being academic very quickly.

What good software must do

Don't buy AP software because the demo looks polished. Buy it because it removes friction from the exact points where your team gets stuck.

Your shortlist should answer these questions:

Does it integrate with your accounting stack?

If you run QuickBooks, Xero, NetSuite, Sage Intacct, or Microsoft Dynamics, the AP system should sync cleanly with your general ledger, vendor records, and payment status.Can non-finance managers use it without training fatigue?

Department approvers won't become process champions if the tool is clunky. Approval should be simple on desktop and mobile.Does it support rule-based routing?

You need approval workflows based on amount, vendor, entity, location, and expense category.Can it capture invoice data reliably?

OCR matters, but reliability matters more. If the software creates a mess of exceptions, you haven't solved anything.Does it preserve a clean audit trail?

Every action should be traceable. Who approved, when, what changed, and what document supported it.Does it support digital payments?

Look for ACH, virtual card options, and payment scheduling controls that fit your cash plan.

The strongest AP platforms don't replace judgment. They enforce policy consistently so your people can focus on exceptions.

How to judge the return

A lot of owners ask the wrong question. They ask, “What's the monthly fee?” Ask this instead: “What does staying manual cost me?”

Manual AP creates hidden expense in several ways:

- Labor drag from rekeying and chasing approvals

- Late fees and rushed payments when invoices surface too late

- Missed discounts or poor timing because approvals arrive after the best payment window

- Control failures that create duplicate or questionable payments

- Weak reporting that makes forecasting less reliable

This walkthrough is worth watching if your team is comparing software and process design in practical terms:

I tell owners to run a simple test. Pull a recent month of invoices and ask how many required manual follow-up, how many sat waiting for approval, and how often someone had to “fix” the coding before close. That gives you your answer. You don't need perfect AP software. You need software that removes repeated friction from the same places, every month.

Tracking Performance with Key AP Metrics

If you don't measure AP, you'll judge it by noise. The loudest vendor complaint, the latest payment scare, the month-end scramble. That's a terrible management system.

Strong accounts payable management runs on a short list of metrics that tell a story. Not a vanity story. An operating story. You want to know whether invoices are moving cleanly, whether your team is paying on purpose, and whether cash timing matches business reality.

The story behind the numbers

One metric in isolation can mislead you. A long Days Payable Outstanding figure might mean smart cash preservation, or it might mean your approvals are jammed. A low cycle time might mean efficiency, or it might mean your team is paying too quickly without enough control.

That's why you need a small dashboard, not a single hero metric.

Track metrics that answer these questions:

- Are invoices entering the system quickly?

- Are approvals stalling in specific departments?

- Are we paying according to terms, not emotion?

- Are we keeping processing effort under control?

- Are we catching opportunities to pay strategically?

The point of AP metrics isn't reporting. It's intervention. Good metrics tell you where to act before cash gets tight or suppliers get angry.

Essential Accounts Payable KPIs

| KPI | Formula | What It Measures |

|---|---|---|

| Days Payable Outstanding | Average accounts payable ÷ cost of goods sold or purchases per day | How long the business takes to pay suppliers on average |

| Cost Per Invoice | Total AP processing cost ÷ number of invoices processed | The efficiency of your payable operation |

| Invoice Cycle Time | Invoice receipt date to approved or paid date | How quickly invoices move through your workflow |

| Early Payment Discount Capture Rate | Discounts captured ÷ discounts available | How well AP converts available terms into savings |

| Exception Rate | Invoices requiring manual intervention ÷ total invoices | How often your process breaks from the standard path |

| On-Time Payment Rate | Invoices paid by due date ÷ total invoices due | How consistently you meet agreed supplier terms |

A practical dashboard doesn't need to be fancy. It can live in your ERP, AP platform, or even a disciplined spreadsheet if you're not yet automated. What matters is consistency. Review it monthly. Then ask where the friction sits. Is it intake, coding, approvals, exceptions, or payment release?

The owners who get value from AP metrics don't drown in reporting. They use trends to force better decisions.

How Strong AP Management Unlocks Better Funding

Here, AP stops being an internal process and starts becoming a financing advantage.

Lenders don't just look at revenue. They look at whether your business behaves like a controlled operation. Sloppy AP raises questions fast. Are liabilities complete? Are vendor obligations current? Is cash forecasting reliable? Can management produce clean payables data without a scramble? If the answer is no, financing gets harder, slower, or more expensive.

Lenders trust clean payable systems

A disciplined AP function tells a lender several important things at once.

First, it shows that management knows what the business owes and when. That supports confidence in cash flow projections. Second, it shows internal control. If vendor onboarding, approvals, and payment release follow rules, the lender sees less operational risk. Third, it makes underwriting faster because your payables aging, vendor obligations, and recurring expense patterns are easier to verify.

This matters whether you're seeking a line of credit, short-term working capital, equipment financing, or a broader growth facility. Underwriters want clarity. AP quality contributes to that clarity more than most owners realize.

Clean AP records don't guarantee funding. But messy AP records absolutely complicate it.

There's also a direct working capital effect. When you schedule payments intentionally instead of reactively, you improve your cash conversion rhythm. You keep cash available longer without damaging supplier trust. That gives you more flexibility before you draw on outside capital.

Better AP expands your financing playbook

Here's the bigger strategic point. Strong AP management doesn't just help you qualify for capital. It helps you choose the right kind.

If your payable schedule is accurate, a revolving line of credit becomes easier to use properly because you know when short-term gaps occur. If your receivables are strong but timing is uneven, invoice financing becomes more practical because the rest of your working capital picture is organized. If you're expanding, lenders can underwrite with more confidence when your back-office controls support the growth story.

That's why owners should look at AP and funding together, not separately. One controls cash leaving the business. The other fills gaps or funds opportunities. If the first is weak, the second gets more expensive and more reactive.

A strong AP system also helps you identify when you don't need as much financing as you thought. That's just as valuable. Borrow for growth, inventory, equipment, or strategic timing. Don't borrow because your payables process is disorganized.

If you want to think about this through a working-capital lens, this guide on turning your cash conversion cycle into a borrowing base advantage is worth your time.

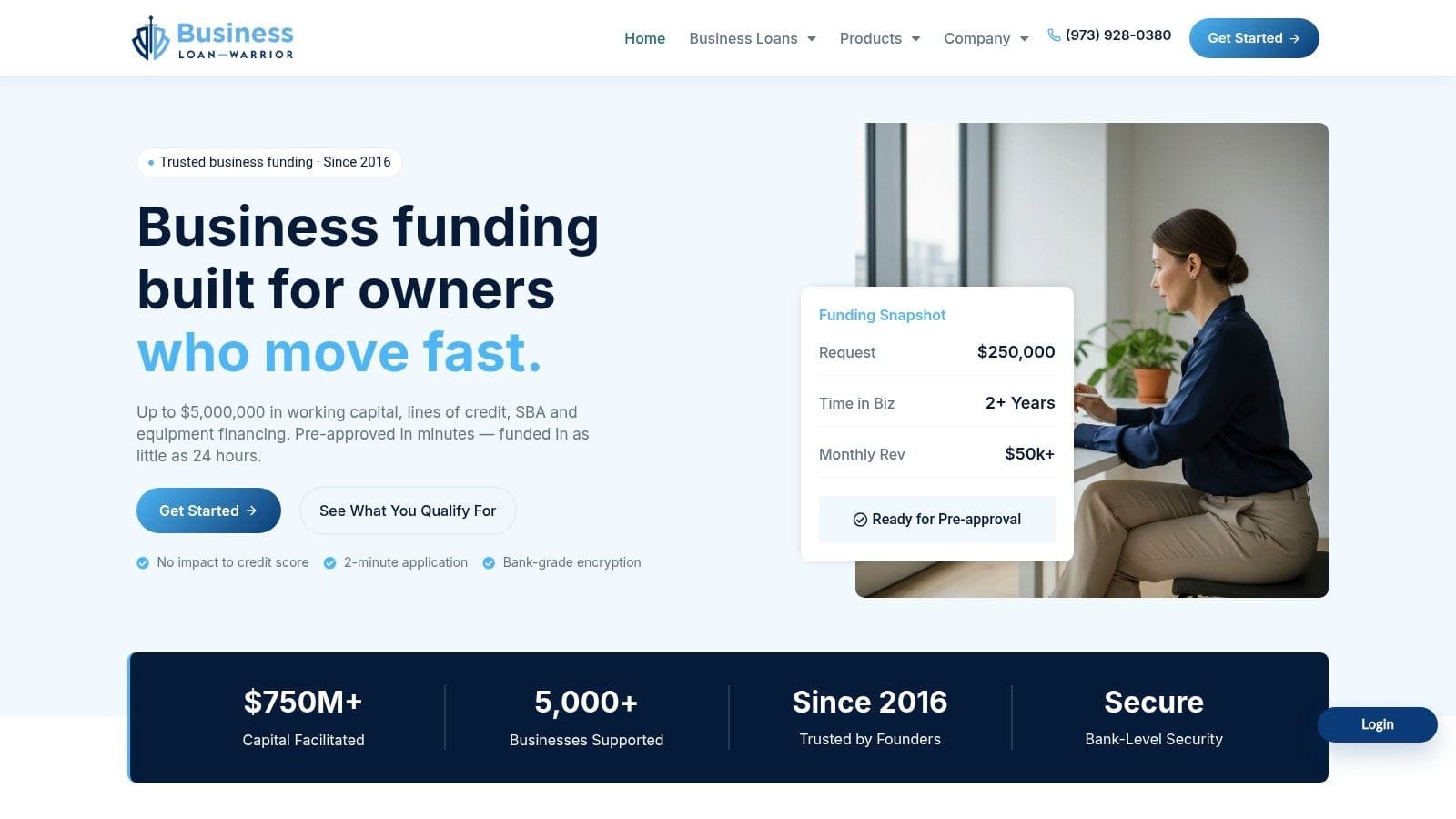

If your business needs funding to stabilize cash flow, smooth vendor payments, or support expansion, Business Loan Warrior is worth a serious look. You can check options through a single no-fee application, explore structures like lines of credit or invoice financing, and move faster with a platform built for operators who need clear answers, not more runaround.