Accounts receivable financing lets you turn unpaid invoices into cash now, usually by receiving 70% to 90% of an invoice's face value instead of waiting the U.S. average 36.7 days to collect. In plain terms, it's a way for businesses to get an advance on unpaid invoices and convert future revenue into present-day cash when working capital gets tight.

If you're staring at a stack of receivables while payroll, inventory, or vendor bills keep moving closer, this is the kind of financing that can feel less like borrowing and more like accessing cash you've already earned. The key point is that the actual value doesn't come from the headline advance rate. It comes from the contract details, the quality of your customers, and whether one slow-paying account can throw your whole borrowing base off balance.

That's where many business owners get tripped up. They hear “fast cash against invoices” and assume the product is simple. The mechanics are simple. The economics are not. A concentrated customer base, disputed invoices, broad recourse language, or a lender with aggressive reserves can make a workable facility feel expensive fast.

Used well, accounts receivable financing can steady cash flow and support growth. Used carelessly, it becomes a patch for deeper collections or customer mix problems.

Table of Contents

- Turn Your Unpaid Invoices into Immediate Cash Flow

- How Accounts Receivable Financing Works

- Invoice Financing vs Factoring A Detailed Comparison

- Is AR Financing Right for Your Business

- Understanding Costs Terms and Lender Eligibility

- Managing Risks and Choosing the Right Partner

- Frequently Asked Questions About AR Financing

Turn Your Unpaid Invoices into Immediate Cash Flow

A common small business problem looks like this. Sales are strong, invoices are out, and the business is technically profitable. But cash is tight because customers haven't paid yet.

That gap is exactly where accounts receivable financing comes in. Instead of waiting through customer payment terms, you use those unpaid invoices to access working capital now. For a business owner, that can mean covering payroll without delay, buying materials for the next job, or taking on a larger order without draining the operating account.

Accounts receivable financing isn't some fringe workaround. One market projection estimates the market will reach $182.63 billion in 2026 and grow at a projected 11.0% CAGR through 2030, which tells you demand is broad and still rising among businesses trying to improve working capital and reduce the pain of long payment cycles, according to The Business Research Company's accounts receivable financing market report.

Why owners reach for it

The businesses that usually consider this tool aren't failing. They're often growing.

They've already delivered the product or service. The revenue is booked. The customer is legitimate. The only problem is time. Cash is arriving on the customer's schedule, while expenses arrive on the business's schedule.

Practical rule: If your cash flow problem is timing, receivables financing can help. If your cash flow problem is weak margins or chronic disputes, it usually won't fix the real issue.

For owners trying to stabilize short-term liquidity, the broader issue is working capital discipline. That's why it helps to understand smart financing tactics for small business stability before choosing any one product.

Where the opportunity and risk meet

At its best, AR financing lets a healthy business move faster. At its worst, it covers up a dangerous dependence on a few customers who pay slowly, dispute invoices, or squeeze terms whenever they want. That's why the right question isn't just “Can I get an advance?” It's “What happens to this facility when my biggest customer pays late?”

How Accounts Receivable Financing Works

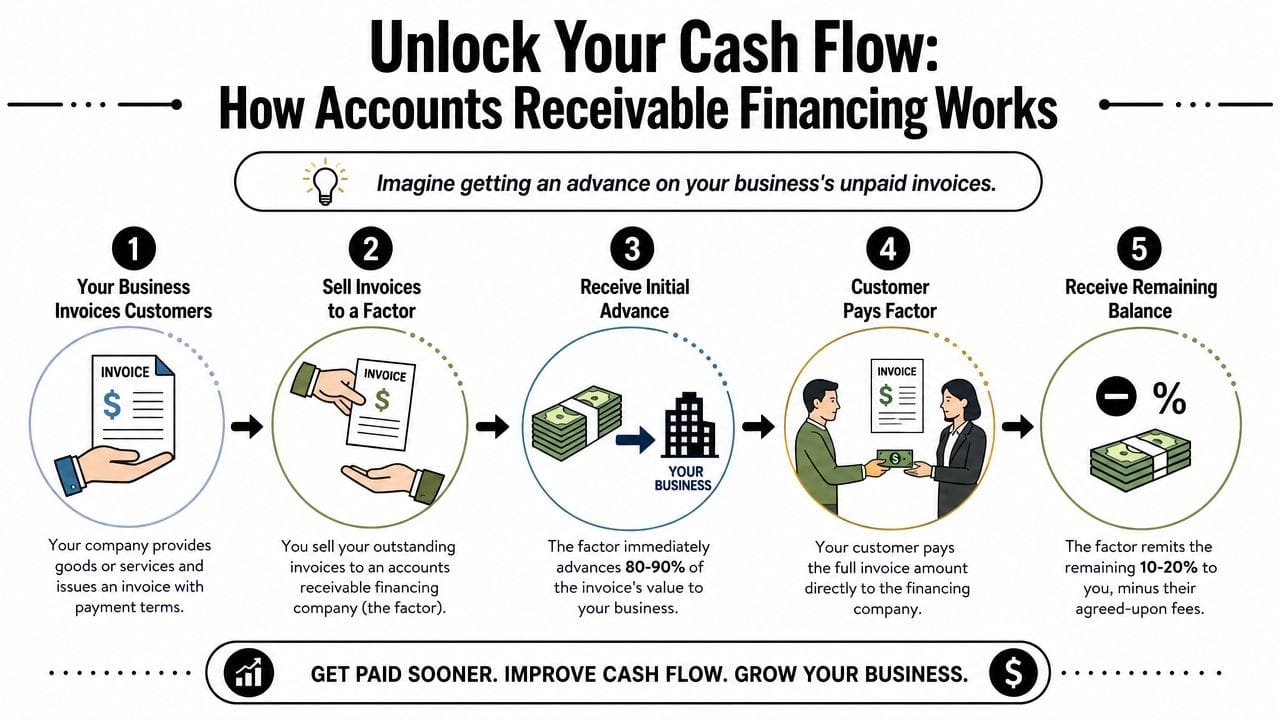

A simple way to read AR financing is this. You are turning completed work into usable cash before your customer gets around to paying.

You deliver goods or services, send the invoice, and a financing company advances part of that invoice value. NetSuite explains that businesses can often receive 70% to 90% of the invoice face value, sometimes higher for strong receivables, rather than waiting the U.S. average 36.7 days to collect, as described in NetSuite's guide to accounts receivable financing.

The mechanics are straightforward. The economics are not. The actual cost depends on who collects, how much of the invoice gets held in reserve, how your contract handles disputes, and how exposed you are if one major customer makes up too much of your receivables.

The five-step cash cycle

Here's the flow most owners need to understand:

-

You invoice the customer

The receivable starts with a completed B2B sale. Documentation decides a lot here. Signed delivery receipts, approved timesheets, clear milestone acceptance, and matching purchase orders all make an invoice easier to finance and harder for a lender to discount. -

You submit eligible invoices

The finance company reviews the invoice, its aging, and the credit quality of the customer. It also looks at concentration. If one customer represents a large share of your borrowing base, you may get less availability than you expected, even if that customer usually pays. -

You receive the advance

Once approved, you get an upfront portion of the invoice value. That cash usually goes straight to payroll, inventory, fuel, or subcontractor payments. It can solve a timing problem fast, but only if the advance rate and fees leave enough margin in the job. -

The customer pays

Depending on the structure, your customer pays either you or the finance company. At this point, contract language becomes significant. If the invoice can be offset, rejected, or delayed because of a service dispute, the lender may reduce the advance or charge back the invoice later. -

The balance is released, less fees and reserves

After payment clears and deductions are applied, you receive the remainder. The reserve sounds minor on paper, but it affects cash flow in a real way when customers stretch terms or pay inconsistently.

A receivable is only as financeable as it is collectible. Weak paperwork, broad offset rights, recurring disputes, or heavy dependence on one account will either raise the cost or shrink the credit you can use.

Two structures sit underneath the same label

Many owners use “AR financing” as a catch-all term. Contracts do not.

The two core forms are:

-

AR loan or invoice financing

The invoice serves as collateral. You still own the receivable and usually keep collections in-house. -

Factoring

The invoice is sold to the finance company. Collections often shift to the factor.

That distinction affects more than customer communication. It changes accounting treatment, control over collections, and how much friction you may create with customers who are used to paying your team directly. It also changes how lenders handle reserves, concentration limits, recourse, and ineligible invoices. If you want a broader look at how factoring stacks up against other fast-cash products, compare short-term loans, MCAs, and invoice factoring for quick capital.

One practical point gets missed all the time. A low stated fee can still be expensive if your largest customer pays on day 75, your agreement charges weekly or monthly while the invoice is outstanding, and your reserve stays trapped until every deduction clears. That is why experienced owners read the concentration limits, dispute language, and repayment triggers before they focus on the headline advance rate.

Invoice Financing vs Factoring A Detailed Comparison

The operational difference that matters

The biggest mistake I see is owners focusing only on speed of funding. The better filter is control.

If you want to keep customer contact and collections in-house, invoice financing usually fits better. If you want faster liquidity and are comfortable with a third party stepping into collections, factoring may be the cleaner option. American Express notes that in factoring, invoices are sold to a third party that often takes over collections and the transaction can be treated as an asset sale, while in asset-based invoice financing, the business uses receivables as collateral for a line of credit and keeps control of collections, paying interest on drawn funds, as outlined in American Express's comparison of receivables financing structures.

If you're weighing factoring against other fast-capital products, it also helps to compare short-term loans, MCAs, and invoice factoring for quick capital.

Invoice Financing vs. Invoice Factoring

| Feature | Invoice Financing | Invoice Factoring |

|---|---|---|

| Invoice ownership | You keep the receivable and borrow against it | You sell the receivable to the factor |

| Collections | Your business usually keeps handling collections | The factor often handles collections |

| Customer visibility | Often lower customer involvement | Customer usually knows the invoice was assigned |

| Balance sheet effect | Commonly functions more like borrowing | Can be treated more like an asset sale |

| Control of relationship | Higher control over tone and timing with customers | Less control once the factor manages payment flow |

A practical way to choose is to ask who you want calling your customer when payment runs late.

What works better in the real world

Invoice financing tends to work better for companies with disciplined internal collections, strong back-office processes, and customers they want to manage closely.

Factoring often works better when speed matters more than privacy, or when the business would benefit from outsourced collections administration.

Neither model is automatically cheaper or safer. The better structure is the one that matches how your customers pay, how your contracts read, and how much control your team needs to keep.

Is AR Financing Right for Your Business

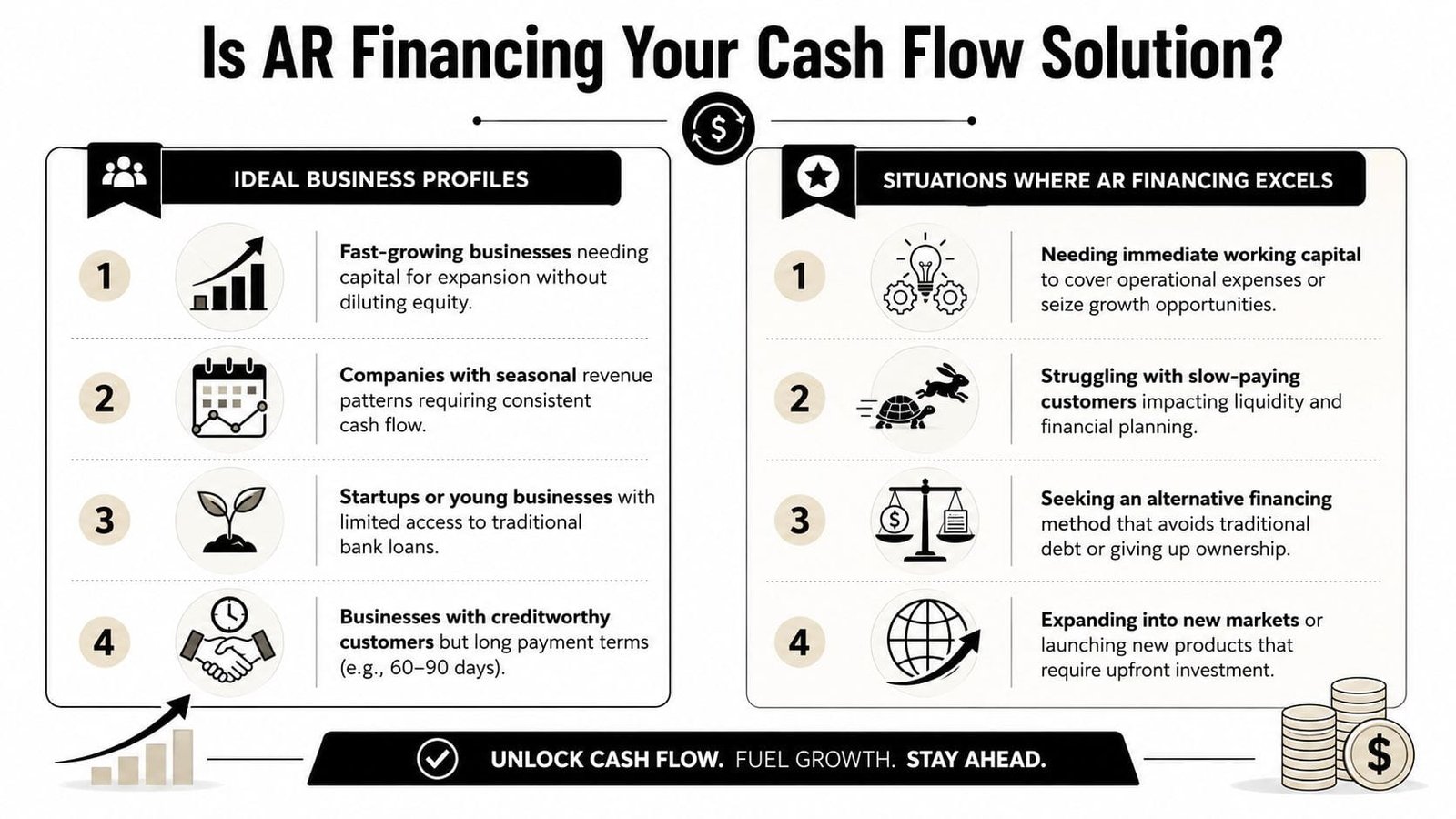

The right fit usually has less to do with industry labels and more to do with how your cash cycle behaves.

When it fits well

AR financing tends to make sense when your business checks several of these boxes:

- You sell B2B on terms. If customers routinely pay well after delivery, receivables become a real working capital asset.

- Growth is outpacing cash. You may be profitable and still short on cash because every new contract requires labor, materials, or inventory before collections catch up.

- Seasonality creates a gap. Some businesses need liquidity before the busy cycle converts into collected cash.

- Large orders strain operations. A solid receivables facility can help bridge execution costs while invoices age.

A short explainer may help if you want another angle on the product before talking to lenders:

Strong AR financing candidates usually have one thing in common. Their customers are worth financing, even if the business itself is still smoothing out its cash cycle.

When it usually does not

This product often disappoints owners in a few predictable situations:

- You sell mostly to consumers. Consumer receivables usually don't fit the model well.

- Your invoices get disputed often. Lenders don't like financing arguments.

- Your margins are too thin. Even a workable facility can hurt if every dollar of fee pressure bites into already narrow profit.

- Your books are messy. Missing backup, unapplied credits, or unclear aging reports can make a fundable receivable look weak.

A practical self-check

Before applying, ask three blunt questions:

- Are my invoices clean and enforceable?

- Do my customers usually pay, even if they pay slowly?

- Would faster cash create a return, or just cover recurring disorder?

If the answer to the third question is “just cover disorder,” pause. Financing helps timing. It doesn't cure poor billing discipline, weak contracts, or underpriced work.

Understanding Costs Terms and Lender Eligibility

A common scenario looks like this. A contractor has $400,000 in open invoices and gets offered an AR facility that sounds straightforward on the phone. Then the term sheet shows concentration caps, aging exclusions, a reserve, and recourse language tied to disputed invoices. The headline fee did not change. The usable cash did.

That is why cost needs to be judged in context, not as a single percentage.

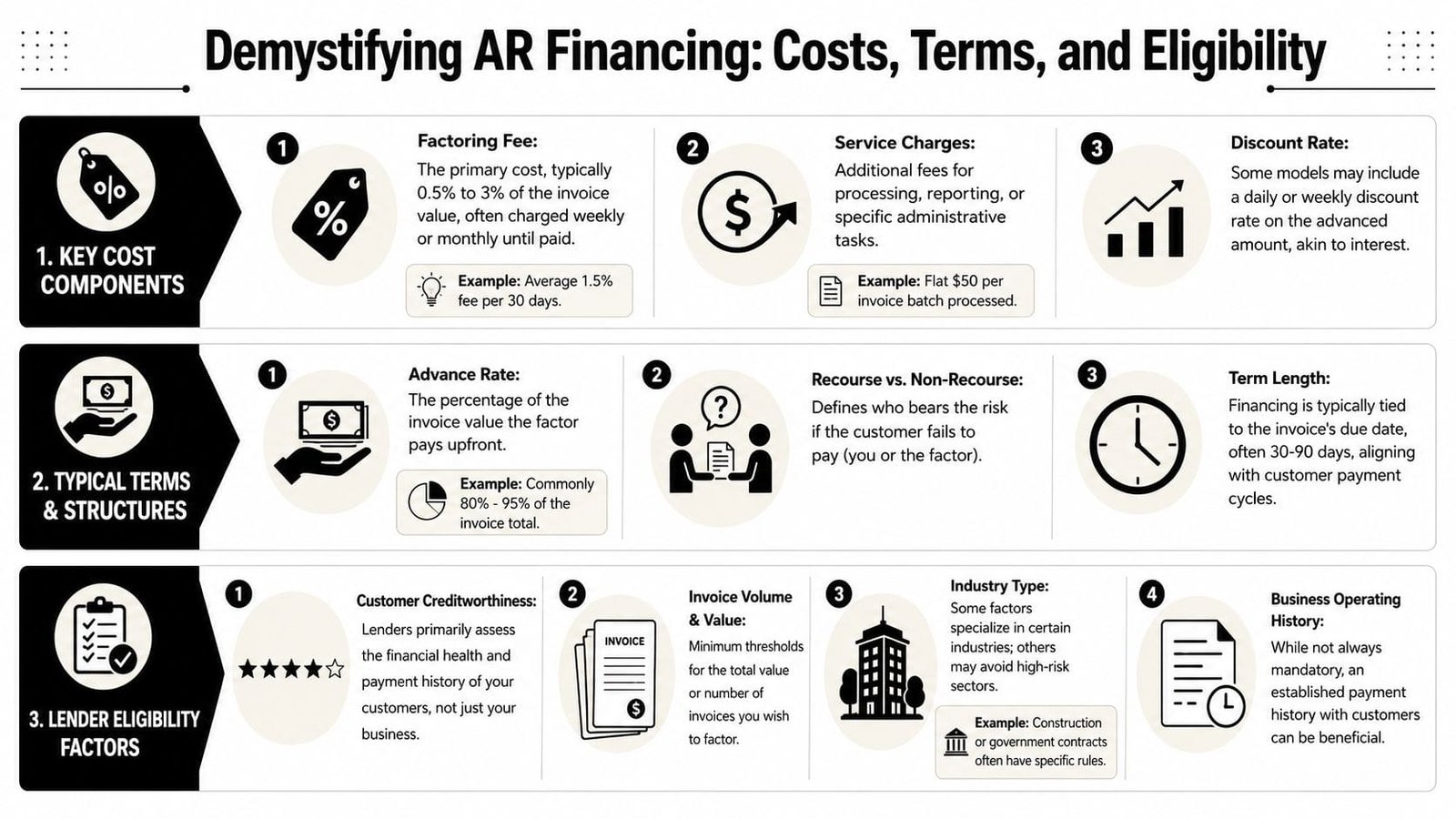

What drives your terms

Fora Financial describes AR financing as collateralized working-capital lending where lenders often advance a portion of invoice value, with terms shaped by borrower quality, invoice aging, and customer concentration risk. Its overview also notes that underwriting focuses heavily on receivables quality and enforceability, which you can see in Fora Financial's explanation of accounts receivable financing.

Two companies can post similar revenue and receive very different offers because lenders underwrite the receivables, not just the top line.

They are looking at a few practical questions:

- Who owes the money

- How old the invoices are

- Whether the customer has a history of deductions or disputes

- How much of the ledger sits with one account

- Whether the contract allows offsets, retainage, pay-if-paid terms, or broad acceptance rights

That last point gets missed all the time. An invoice can look collectible in your aging report and still be weaker collateral if the underlying contract gives the customer several ways to delay payment or reduce the amount due.

The contract points that change the effective cost

Owners usually focus on the rate. I pay closer attention to availability, dilution rules, and repurchase triggers, because those are the terms that decide whether the facility solves a cash gap or creates a new one.

Here are the clauses that deserve a slow read:

-

Advance rate

This is the cash you receive up front. A strong advance rate helps, but it matters less if a large share of your invoices gets screened out. -

Borrowing base rules

Lenders may exclude older invoices, cross-aged accounts, foreign receivables, government receivables, or balances above a concentration limit. If one customer represents a large portion of sales, that cap can shrink availability fast. -

Reserves

Reserves protect the lender against dilution, disputes, and timing risk. For the borrower, reserves are cash you expected to use but cannot access yet. -

Recourse terms

Under recourse structures, unpaid invoices can come back to you. If your customer stretches payment because of internal approval delays or partial disputes, that buyback risk matters more than the advertised fee. -

Dilution treatment

Short pays, credits, rebates, and returns reduce what the lender views as eligible collateral. Businesses with regular post-invoice adjustments often discover their borrowing base is smaller than their receivables total suggests. -

Notification and control terms

Some facilities require customer notice, redirected payments, or tighter control over collections. That may be manageable, but it can affect how your customers experience your billing process.

Watch this first: A low quoted rate can still produce an expensive facility if concentration caps, ineligibles, and reserve mechanics cut monthly availability.

What improves lender eligibility

Lenders respond well to receivables that are easy to verify, easy to assign, and unlikely to be disputed.

A stronger file usually includes:

- Customer diversity that keeps one account from dominating the borrowing base

- Current receivables aging with limited spill into older buckets

- Low dispute frequency and clear proof of delivery, completion, or acceptance

- Consistent billing and collections procedures inside your company

- Contracts with clear payment terms and limited offset language

- Records that explain aging anomalies clearly, which is where a solid AR aging narrative your lender wants to read can help

Systems matter too. J.P. Morgan describes receivables financing as a tool to “simplify internal billing and collections” and manage counterparty exposure in its receivables financing overview. In practice, clean ERP data, organized backup, and a consistent collections cadence make underwriting easier and reduce avoidable delays.

If you're comparing lenders, one option in the market is Business Loan Warrior, which offers a no-fee application, pre-approval checks, and access to funding options including invoice financing. That can be useful if you want to compare structures side by side instead of accepting the first AR proposal that lands in your inbox.

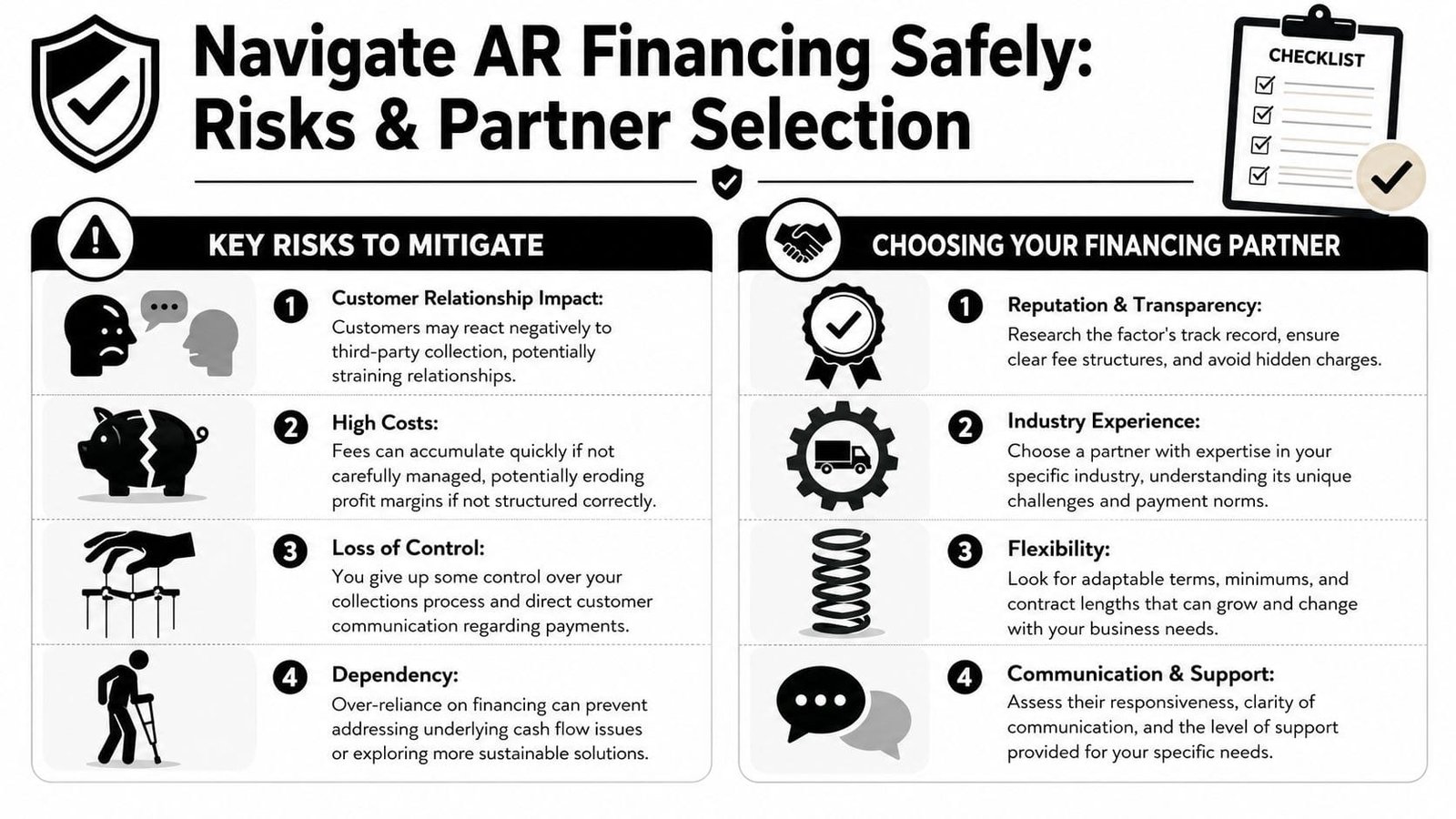

Managing Risks and Choosing the Right Partner

Customer concentration is the risk most owners underestimate

The sharpest trade-off in accounts receivable financing isn't always price. It's dependency.

If a large share of your receivables comes from one or two customers, your lender sees a fragile borrowing base. TabBank highlights customer concentration as a major risk and notes that the Federal Reserve's 2024 Small Business Credit Survey found 55% of small-employer firms had 1–4 weeks of cash on hand, which means even a delay or dispute from a major customer can trigger a severe liquidity crunch, as discussed in TabBank's guidance on AR financing risk.

That's why concentration limits matter so much. A business can post strong sales and still have weak financeability if too much of the ledger sits with one buyer. Add slow payment habits or frequent deductions, and the advance becomes less useful than it looked on day one.

Aging quality matters too. If your biggest account always pays late but eventually pays, that may be manageable for your business and still uncomfortable for the lender. Those are not the same standard.

For owners preparing to talk with underwriters, it helps to tighten the story your receivables report tells. This guide on writing the AR aging narrative your lender wants to read is useful prep work.

How to vet a lender before you sign

Use this checklist before accepting a term sheet:

- Ask about concentration caps. Find out what happens if one customer exceeds the limit or if another debtor drops out of eligibility.

- Clarify recourse language. You need to know exactly when an unpaid invoice becomes your problem again.

- Review reserve triggers. Late payments, disputes, or documentation issues can all increase holds.

- Check collection style. If the lender interacts with customers, ask how they communicate and escalate.

- Read termination and minimum-use provisions. A flexible facility can become restrictive if the contract pushes volume commitments you don't need.

Slow-paying customers don't just create cash flow stress. They can shrink your borrowing base, increase reserves, and make yesterday's quoted availability meaningless.

The right partner gives you transparency before problems show up, not after.

Frequently Asked Questions About AR Financing

Will my customer know I'm using accounts receivable financing

Sometimes they will.

In a factoring arrangement, customers are often notified because payment goes directly to the factor. In an invoice financing structure, you may keep control of collections, so the change is less visible. The specific terms are outlined in the notice, assignment, and payment instructions in your agreement. If keeping the customer relationship tight matters, review those clauses before you sign, not after the first remittance goes out.

Does accounts receivable financing affect my credit

It can, but the impact depends on the provider and the structure.

Many lenders focus more on receivables quality, customer payment history, and documentation than a bank would in a standard term loan review. That does not mean your credit is irrelevant. Ask whether the provider pulls personal credit, reports to business credit bureaus, or treats a default as a broader credit event.

How fast can funding happen

Speed depends on how clean your file is.

Well-documented invoices, consistent aging reports, clear proof of delivery, and responsive customers usually lead to a faster process. Missing paperwork slows everything down. So do disputed invoices and customers with complicated approval chains.

What is the biggest mistake owners make

They treat the quoted advance rate as the whole deal.

The contract drives the outcome. A high advance can still leave you short on cash if concentration caps exclude your largest customer, reserves rise after slow payments, or recourse terms push old invoices back onto your balance sheet. Owners with one dominant account need to pay especially close attention here, because a facility that looks affordable can get expensive fast when that customer falls outside the lender's comfort zone.

Is non-recourse always better than recourse

Non-recourse only helps if the coverage matches the risk you face.

Some agreements cover customer insolvency but not disputes, offsets, dilution, or documentation problems. For many businesses, those exceptions are where losses show up. Read the trigger language carefully and compare it with how your customers really pay under their contracts.

If you are comparing AR financing with other working capital options, Business Loan Warrior offers a no-fee application and lets you review funding paths side by side. That kind of comparison is useful when you need to weigh contract terms, customer concentration risk, and the true cash flow impact before you commit.