You're probably here because the line between your money and your company's money already feels thinner than it should.

A client pays late. Payroll is due. Inventory has to ship. The easiest move is to grab the personal card, float the expense, and tell yourself you'll clean it up next month. That works right up until it doesn't. The short-term fix starts shaping how lenders, card issuers, and even insurers judge the business.

That's not a rare mistake. A 2017 U.S. Small Business Administration report noted that about 46% of small businesses use personal credit cards to finance business expenses. In practice, that means many owners are trying to grow a company while putting their own borrowing power, cash flow, and liability exposure on the same track.

The core issue in business credit vs personal credit isn't academic. It's operational. If you don't separate the two, funding gets harder, underwriting gets messier, and your business stays tied to your personal financial ceiling.

Table of Contents

- The Blurry Line Between Business and Personal Finance

- Defining the Two Credit Worlds

- Business Credit vs Personal Credit Side by Side

- Why This Separation Unlocks Business Growth

- Your Action Plan to Build Business Credit

- Real-World Scenarios When to Use Each

- How Lenders Like Business Loan Warrior Evaluate Both

The Blurry Line Between Business and Personal Finance

A lot of owners first mix credit for ordinary reasons, not reckless ones. The office printer dies. A vendor wants payment before releasing materials. You need a laptop, a hotel room, or a rush shipment today, not after a committee meeting with your accountant. So the owner uses a personal card and moves on.

That habit feels harmless because it solves a real problem. But over time, it creates a distorted financial picture. Your personal utilization rises because of business activity. Your bookkeeping gets harder. If the business hits a rough patch, the debt doesn't stay neatly inside the company.

A common pattern with real consequences

The SBA figure above matters because it confirms what lending teams see every day. Owners often use personal plastic as working capital. It's common, but common doesn't mean strategic.

Practical rule: If a purchase supports company operations, the cleanest long-term move is to route it through a business account or business credit facility whenever possible.

When people compare business credit vs personal credit, they often focus only on score ranges. The bigger issue is control. Personal credit is tied to you. Business credit is tied to the company's financial behavior. If those systems stay mixed, lenders can't clearly tell whether the business stands on its own.

What mixing credit usually breaks

A blurred setup tends to create three problems fast:

- Messy underwriting: The lender has to untangle owner spending from company spending.

- Weaker protection: Personal guarantees become more painful when everything is already commingled.

- Lower flexibility: Future financing options shrink because the owner's personal profile carries too much of the business load.

Owners don't need perfection on day one. They do need a wall between personal and business finances before growth, seasonality, or a cash crunch exposes the gap.

Defining the Two Credit Worlds

What personal credit actually measures

Personal credit is your individual borrowing record. It follows your behavior as a consumer and is typically tied to your Social Security Number. Mortgage lenders, auto lenders, personal loan providers, and card issuers use it to judge how you handle debt as a person.

In practical terms, personal credit answers questions like these: Do you pay on time? Do you carry high balances? Have you handled different types of obligations responsibly? It is fundamentally about your own financial habits and capacity.

That's why using personal credit for business spending can backfire so quickly. A business inventory purchase may be rational for the company, but the consumer reporting system doesn't care why the balance rose. It only sees your profile carrying more debt.

What business credit is built on

Business credit is the company's repayment reputation. It is attached to the business entity and generally built through the EIN, trade lines, business credit cards, vendor terms, and commercial borrowing activity. Commercial bureaus track whether the business pays suppliers and lenders on agreed terms.

Business credit is less about your grocery bill or car payment and more about whether the company honors invoices, manages trade relationships, and pays commercial obligations consistently. That difference matters in underwriting because commercial lenders want evidence that the business can operate as a stand-alone borrower.

If your team reviews reports at scale, tools for automated credit report data extraction can help organize bureau data and supporting documents into a format underwriters can effectively use. That's especially useful when a file includes both owner and business credit records.

Personal credit tells a lender how you've handled your own obligations. Business credit tells them whether the company has earned trust in the market.

Why the systems feel connected even when they're separate

Owners often get confused because the two systems do overlap in real lending. A business can have its own file and still trigger a personal review, especially if the company is newer, lightly capitalized, or applying for unsecured funding.

That doesn't mean they're the same thing. It means lenders use both when the business file alone doesn't answer enough questions. The cleaner your separation, the easier it is for the business to carry more of its own weight.

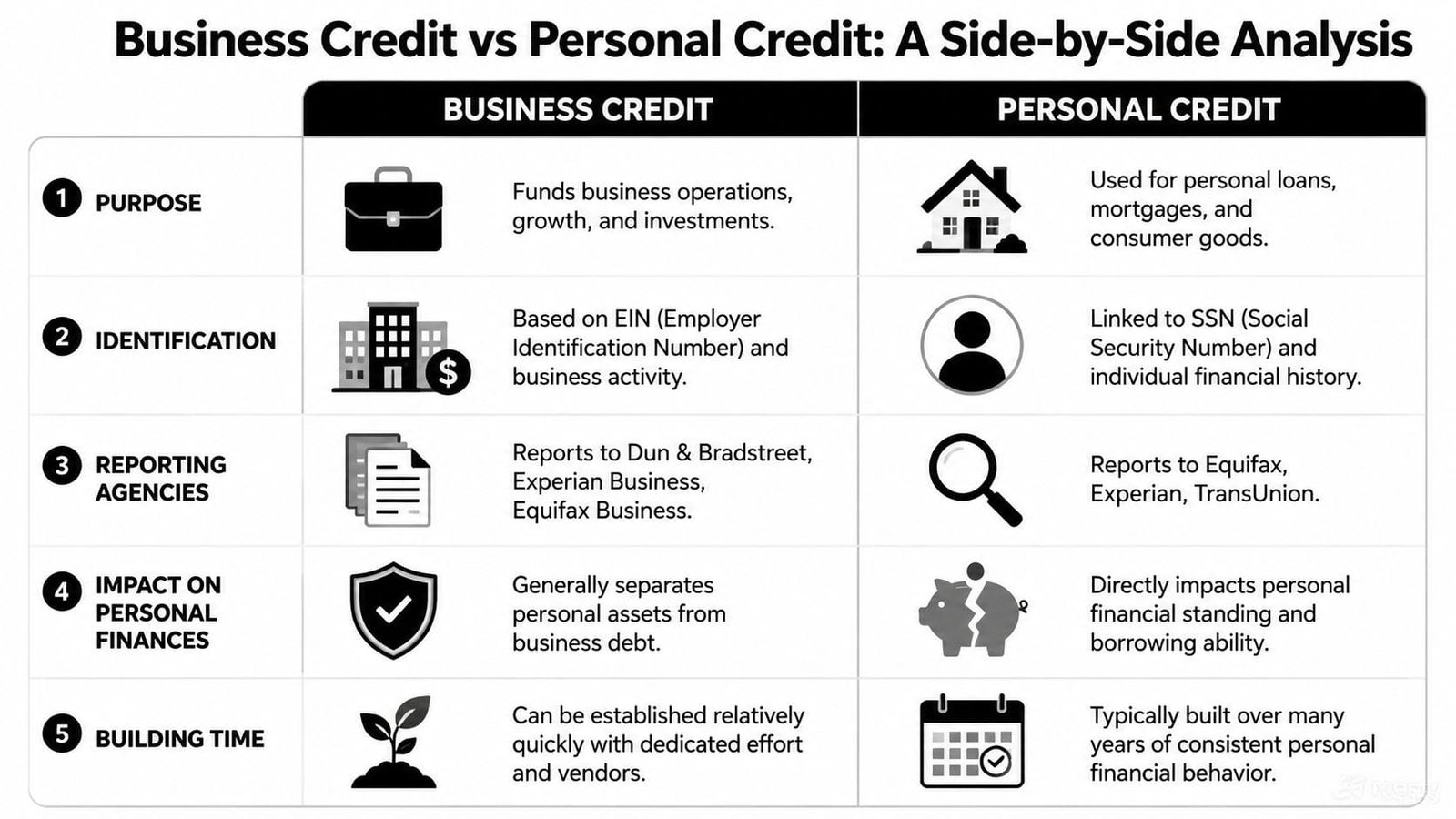

Business Credit vs Personal Credit Side by Side

A side-by-side view clears up most of the confusion around business credit vs personal credit. The systems look similar from the outside because both involve scores, reports, and repayment history. But they operate differently, and those differences affect limits, approvals, and risk.

Personal vs. Business Credit At a Glance

| Feature | Personal Credit | Business Credit |

|---|---|---|

| Identity tied to | Individual borrower | Business entity |

| Common identifier | SSN | EIN |

| Main use | Consumer borrowing and household purchases | Working capital, vendor terms, equipment, and commercial financing |

| Typical bureaus | Equifax, Experian, TransUnion | Dun & Bradstreet, Experian Business, Equifax Business |

| Score style | Consumer scoring model | Commercial scoring model |

| Legal exposure | Directly affects the owner | Can help separate company obligations from the owner, though guarantees may still apply |

| Core behavior tracked | Personal debt handling | Trade and business payment behavior |

| Strategic purpose | Supports personal borrowing power | Helps the company qualify as a business borrower |

Business scores and personal scores don't use the same scale. According to Inc Authority's overview of business credit vs. personal credit, business credit scores such as Dun & Bradstreet PAYDEX generally operate on a 0 to 100 scale, with 80 often used as a strong benchmark. Consumer FICO scores use a 300 to 850 range, with 670 to 739 generally considered prime.

Where owners get tripped up

The number itself is only part of the story. A PAYDEX-style score is heavily tied to trade payment timing relative to invoice terms. Personal scoring behaves differently and pays more attention to consumer-style borrowing behavior, including balance management.

That means an owner can be disciplined personally and still have weak business credit because vendors aren't reporting or invoices are paid loosely. The reverse can also happen. A company may build a decent commercial payment profile while the owner's personal report shows strain.

Here's what matters in real decisions:

- Use case matters: Personal credit helps with personal borrowing. Business credit supports supplier confidence and commercial financing.

- Reporting behavior matters: If no vendor or lender reports business activity, the company stays thin-file even when it pays perfectly.

- Liability matters: A company card used correctly is a business tool. A personal card used for company purchases is still your personal obligation.

A clean business profile doesn't happen because you formed an LLC. It happens because the business repeatedly pays obligations in ways the commercial system can actually see.

For most owners, the practical takeaway is simple. Don't just ask which score is “better.” Ask which file is being strengthened by each financial decision you make this month.

Why This Separation Unlocks Business Growth

Separation changes more than bookkeeping. It changes how the market sees the company.

When a lender reviews a business that runs through dedicated bank accounts, pays vendors in the business name, and maintains its own commercial profile, the file is easier to understand. That doesn't guarantee approval, but it does reduce confusion. Cleaner files make it easier to evaluate cash flow, obligations, and repayment discipline.

Separation changes how the business is viewed

A business with its own credit footprint looks more stable than one that depends on the owner's personal cards every time cash gets tight. It also creates room to pursue financing that fits business use, rather than forcing every need through consumer credit.

That distinction becomes more important as needs get larger or more specialized. Equipment, inventory, expansion, and working capital all benefit from being handled as business obligations instead of personal debt stacked on the owner's report.

If you want a practical benchmark for how lenders think about owner credit in commercial financing, this guide on business loan credit score expectations is a useful reference point.

Insurance is part of the credit conversation too

Most owners think about credit only in terms of loans and cards. That's too narrow. Credit can also affect the cost and structure of coverage.

According to Our Heritage Bank's explanation of how personal credit factors into business creditworthiness, insurers may cross-reference personal credit history and business credit profiles when setting premiums. Strong personal credit can indirectly lower business insurance costs, while a weak personal score can raise them, especially for firms under $10M in revenue.

That matters because insurance is often treated as a fixed overhead line. It isn't always fixed. If the business has a thin credit file and the owner's personal profile is also strained, insurers may see more risk than the owner expects.

The hidden cost of staying blended

A blurred setup can lead to problems beyond loan pricing:

- Higher insurance friction: Weak or unclear credit signals can affect premium and coverage conversations.

- More owner dependence: The business keeps borrowing credibility from the founder instead of building its own.

- Harder scaling: Each new funding ask circles back to the owner's personal ceiling.

Owners who separate credit early usually gain options. Options matter more than rate shopping alone.

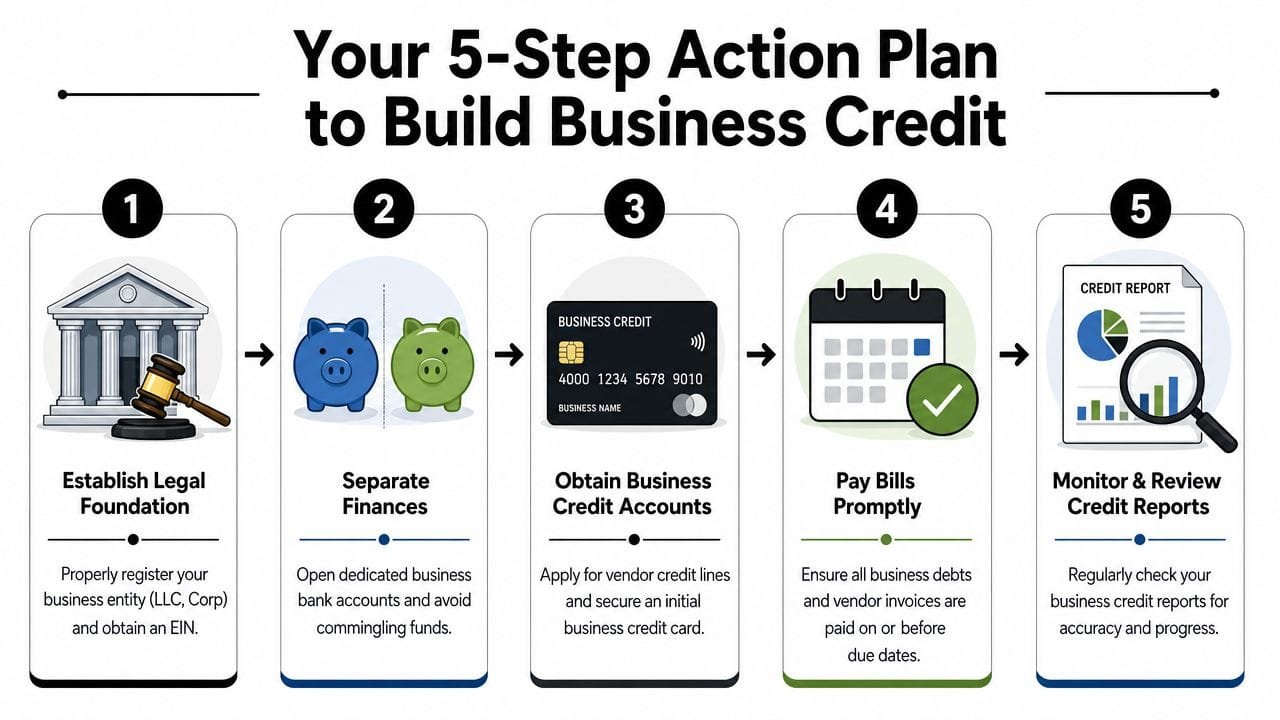

Your Action Plan to Build Business Credit

Building business credit is less glamorous than chasing a big approval, but it's the work that makes later approvals possible. Done right, it creates a file lenders and vendors can read without guessing.

Start with structure, not cards

A lot of owners try to build business credit by applying for financing too early. That's backwards. The first move is to make the business legible as a business.

- Form the entity properly. If you're operating informally, lenders and bureaus have less to anchor to. Register the business and keep the records current.

- Get the EIN and use it consistently. The business needs its own identity in applications, invoices, and account setup.

- Open dedicated business banking. Revenue should land in the business account, and expenses should leave from it. Owners often establish or undermine their credibility based on this practice.

Field advice: If your bank statements still look like a mix of groceries, software, fuel, owner draws, and client deposits, you haven't separated anything yet.

For owners who want an outside checklist, this MyOfficeOps financial advisory for credit lays out the foundational habits well.

Then build reporting activity

Once the structure is clean, the focus shifts to activity that commercial bureaus can observe.

- Add vendor relationships that report. Trade lines are the raw material of business credit. If suppliers extend terms but never report, your file may stay thin.

- Use a business credit card carefully. The point isn't to carry balances. The point is to create clean, reportable business payment history.

- Pay on or before terms. Commercial scoring responds strongly to payment timing. Sloppy invoice management hurts more than many owners realize.

- Review your reports. Missing accounts, wrong balances, and incomplete profiles can stall progress if nobody checks them.

A structured roadmap can help if you're trying to move quickly without creating a mess. This guide to the 90-day business credit blueprint lending partners actually trust is a solid way to think about sequencing.

What works and what doesn't

What works is boring. Consistent banking, vendor reporting, clean documentation, timely payment, and patient repetition.

What doesn't work is opening random accounts, mixing reimbursements with operating spend, or assuming an LLC alone creates a strong commercial profile. Legal formation is the shell. Reporting behavior is what gives the shell weight.

Real-World Scenarios When to Use Each

The right answer depends on the age of the business, the type of expense, and how much risk the owner should carry personally.

Four common situations

A new freelancer buying a laptop may still end up relying on personal credit if the business hasn't established commercial accounts yet. That can be reasonable in the very early stage, but it should be treated as temporary. The goal is to move recurring operational spending into business banking and business credit as soon as practical.

A retail business stocking seasonal inventory should lean toward business credit, not personal cards. Inventory is a core operating expense tied to revenue generation. If the owner puts that on personal credit, they're using consumer borrowing to absorb business cycle risk.

A construction company acquiring a truck should usually pursue a business financing structure tied to the company's use and cash flow. The asset serves the business. The paper trail should reflect that. If the owner uses personal financing for a company vehicle, it often complicates both underwriting and accounting later.

A software-heavy startup paying recurring subscriptions should route those charges through a business card and business bank account. Subscription stacks grow subtly. When those costs sit on an owner's personal card, they inflate personal balances and hide the company's true operating burden.

Use personal credit only when the business genuinely lacks access and the expense is necessary. Don't use it because it feels faster.

For owners weighing which financing lane makes sense for a specific need, this breakdown of business loan vs personal loan choices helps frame the trade-offs clearly.

The best test is simple. Ask which profile should benefit from this purchase and which party should carry the risk if revenue slows. That usually tells you which credit type belongs in the deal.

How Lenders Like Business Loan Warrior Evaluate Both

From an underwriting standpoint, business credit vs personal credit is rarely an either-or question. It's a combined risk picture.

A strong business file can carry a lot of weight. But when the company is newer, thin-file, or inconsistent, underwriters still look closely at the owner. That's not arbitrary. It reflects how small-business finance works in practical terms.

Research from the Consumer Financial Protection Bureau conference paper on small-business finance found that entrepreneurs in the United States often increase personal borrowing to fund their firms, including an average increase of approximately $9,178 over the period studied, with personal mortgage balances alone accounting for about $10,303. The paper also shows that when business credit tightens, owners increase their use of personal credit. That's one reason personal credit remains a gatekeeper in small-business underwriting.

Why underwriters still look at the owner

If the business doesn't yet have a deep repayment record, the owner becomes the fallback source of evidence. Underwriters look for signs of discipline, stability, and the ability to manage obligations under pressure.

That's also where the personal guarantee comes in. A guarantee connects the owner to the debt if the business can't pay. Owners sometimes treat that as a technicality. It isn't. It's a core part of how risk is allocated on many small-business deals.

What weakens a file fastest is inconsistency. Mixed bank activity, incomplete statements, unexplained transfers, and debt that appears personal in one place and business-related in another all create hesitation. If you want your package to read cleanly, your financial records have to read cleanly too. Teams preparing statements and signatures often benefit from tools like BoloSign for financial reporting when gathering organized, lender-ready documentation.

What strengthens an application

A lender generally gains confidence when these pieces line up:

- Clear separation: Business revenue and business expenses run through business accounts.

- Visible repayment history: Trade lines, cards, or loans show timely business payment behavior.

- Coherent documentation: Statements, entity records, and ownership details tell one consistent story.

- Owner support when needed: Strong personal credit can help bridge the gap while the business file matures.

Here's a useful overview of how commercial financing gets evaluated in practice:

The strongest applications don't pretend personal credit is irrelevant. They show that the business is steadily becoming less dependent on it.

If you want to explore funding options without turning the process into a credit guessing game, Business Loan Warrior gives business owners a practical way to check options, compare structures, and move toward financing that fits how the company operates.