Today, strong borrowers can still find bank business loans in the 6.8% to 11% range, while SBA 7(a) loans generally run from 9.75% to 13.25% variable or 11.75% to 14.75% fixed. If you drift into online lending without a clean profile or a comparison process, costs can jump fast, with online term loans reaching 14% to 99% APR and merchant cash advances climbing to 40% to 350% effective APR.

Many owners face this situation right now. You need capital for inventory, equipment, expansion, payroll cushioning, or a renovation. But before you can decide whether the loan is smart, you need to know the price of money today, and just as important, what it takes to get approved for the better end of the rate range.

Most articles stop at a rate list. That’s not enough. Rates are not a menu board where you point and order the cheapest option. They’re closer to insurance premiums. The lender prices your deal based on how risky you look on paper, how clean your numbers are, and how easy you make underwriting.

That means two business owners can apply for what looks like the same product and get very different offers. One gets bank pricing. The other gets shoved toward expensive fast cash.

This guide cuts through that. You’ll see the business loan interest rates today, what drives those numbers, how lenders judge your file, how to lower your rate before you apply, and how to compare offers without getting fooled by factor rates, teaser payments, or vague fee language.

Table of Contents

- Your Guide to Business Loan Interest Rates

- Current Business Loan Interest Rates in 2026

- Key Factors That Determine Your Interest Rate

- Actionable Steps to Lower Your Business Loan Rate

- How to Compare Loan Offers and Find the True Cost

- Secure Your Best Rate Fast with Business Loan Warrior

- Frequently Asked Questions About Business Loan Rates

Your Guide to Business Loan Interest Rates

If you’re shopping for capital, the first mistake is asking only one question: “What’s the rate?” The better question is: “What rate can my business realistically qualify for, on the right product, with terms that don’t choke cash flow?”

That’s because business loan interest rates today sit on a wide spectrum. Traditional banks are still the cheapest lane for qualified borrowers. SBA loans remain strong for owners who want lower-cost financing but don’t fit a plain-vanilla bank box. Online products can be useful when speed matters, but they can also become very expensive very quickly.

Here’s the practical view:

- Bank loans are the benchmark. If your business is established, profitable, and well-documented, they are the ideal place to begin.

- SBA loans are often the best backup to bank financing. They work well when you need flexibility for working capital, expansion, equipment, or owner-occupied real estate.

- Online products are a tool, not a default. They can solve timing problems. They should not be your first choice if cheaper money is available.

Practical rule: Don’t shop for financing by speed alone. Fast money often behaves like rush shipping. Convenient now, expensive later.

A lot of owners also treat approval and pricing as separate issues. They aren’t. The same file that gets you approved is the file that often determines whether you get a decent offer or a punishing one. Clean financials, reliable cash flow, strong credit, and a clear use of proceeds don’t just improve the odds of a yes. They improve the quality of the yes.

So when you review business loan interest rates today, read the numbers as a range tied to borrower quality. The rate isn’t just about the market. It’s also a scorecard on how a lender views your business.

Current Business Loan Interest Rates in 2026

The rate gap between products is wide enough to materially change whether a loan helps your business or drains it. That’s why product choice matters as much as negotiation.

What rates look like right now

Current data shows bank business loan rates averaging 6.8% to 11%, while SBA 7(a) loans run 9.75% to 13.25% variable. Borrowers with excellent credit often have the best shot at getting below 8%, and online alternatives can run much higher, with online term loans at 14% to 99% APR and merchant cash advances at 40% to 350% effective APR, according to NerdWallet’s April 2026 business loan rate guide.

That spread is not academic. It changes your monthly payment, your debt service cushion, and whether the financing creates value or just plugs a hole at a bad price.

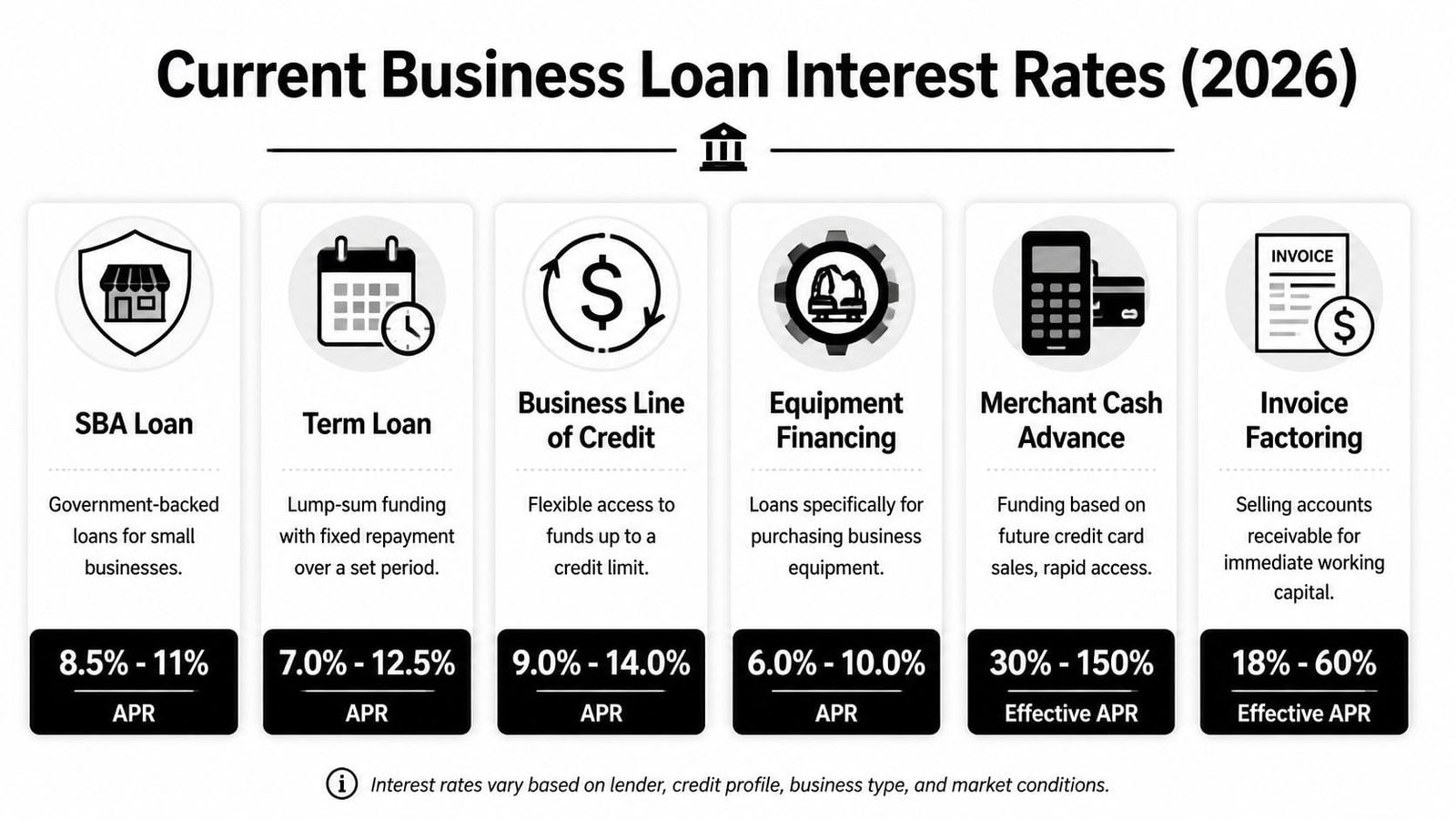

2026 Business Loan Interest Rates & Terms by Type

| Loan Type | Typical APR Range | Best For |

|---|---|---|

| Bank term loan | 6.8% to 11% | Established businesses financing expansion, working capital, or large one-time needs |

| SBA 7(a) | 9.75% to 13.25% variable or 11.75% to 14.75% fixed | Flexible funding for working capital, acquisitions, refinancing, and general growth |

| SBA 504 | 5.65% to 5.82% | Equipment purchases and owner-occupied real estate |

| Online term loan | 14% to 99% APR | Faster access when bank or SBA timing doesn’t work |

| Equipment financing | 4% to 45% | Machinery, vehicles, tools, and revenue-producing equipment |

| Invoice factoring | 25% to 200% APR or fee-based pricing depending on structure | Unlocking cash tied up in receivables |

| Merchant cash advance | 35% to 350% effective APR | Emergency cash when other options aren’t available |

| Business line of credit | Bank lines vary by lender structure, often lower than online options | Managing uneven cash flow, payroll timing, or short-term working capital needs |

A few takeaways matter more than the table itself.

First, SBA 504 is the standout for fixed assets. If you’re buying equipment or real estate, it’s often one of the cheapest serious options available. Second, bank term loans remain the gold standard for operating businesses with strong fundamentals. Third, the jump from bank or SBA pricing to online cash products is massive. That jump can erase the benefit of the capital if you use the wrong tool.

If you’re specifically financing a buildout or expansion project, it’s smart to review how rates differ by structure, collateral, and project type in this breakdown of construction loan rate options for business borrowers.

What the spread really means

A loan product is like a vehicle class. The rate is the sticker price for that class. Your approval profile determines whether you’re shopping economy, premium, or something painfully overpriced.

Use cases matter:

- Working capital with ongoing flexibility: a line of credit or SBA 7(a) can make sense.

- One-time expansion need: bank term loan first, SBA 7(a) second.

- Equipment that holds value: equipment financing or SBA 504.

- Receivables gap: invoice financing may solve the timing issue, but only if the cost still leaves margin.

- Emergency cash with weak documentation: MCA is usually the last resort, not the first call.

A cheap loan on the wrong structure can still be expensive. A line for a long-term asset is a mismatch. A short-term cash advance for a project with a long payoff cycle is worse.

When owners ask about business loan interest rates today, I tell them this. Don’t just hunt for the lowest number. Match the loan type to the job, then compete lenders inside that category.

Key Factors That Determine Your Interest Rate

A lender can quote the same product at two very different rates on the same day. The gap comes from one thing. How hard your file is to approve.

The market sets the starting line

Your rate starts with the broader rate environment. Treasury yields, prime rate, and lender cost of capital all influence the floor before your business ever enters the conversation.

Earlier in this guide, we noted that SBA 504 rates in early 2026 sat in the mid-5% range. That matters because it shows how much the base market can move pricing before underwriting adds its own spread. “Business loan interest rates today” is not just a research question. It affects what you can realistically get approved for right now.

That is also why timing matters. If market rates are up, a weak file gets punished faster. If market rates ease, a strong file gets rewarded faster.

Your approval profile determines the spread

Once the lender sets its base price, underwriting decides how much extra risk premium to add. That premium is where good borrowers save money and sloppy borrowers overpay.

Lenders usually focus on five things:

- Credit strength. Strong personal and business credit tells the lender you manage obligations well.

- Cash flow coverage. They want enough room in monthly cash flow to handle the new payment without strain.

- Time in business and revenue consistency. Stable operations beat a recent spike followed by uneven deposits.

- Collateral and personal guarantee support. If the lender has a clearer recovery path, pricing usually improves.

- Documentation quality. Clean financials, organized bank statements, and a clear use of funds make approval easier and cheaper.

Documentation gets ignored too often. That is a mistake.

A lender reviewing messy books has to assume the risk is higher than it looks. Unclear add-backs, unexplained transfers, stale financial statements, and revenue that does not match bank activity all create doubt. Doubt raises rates.

Lenders price clarity almost as much as performance.

Here is the practical takeaway. Two businesses can have similar sales and still get very different offers because one owner submits a lender-ready package and the other submits a stack of files that forces the underwriter to do detective work.

That approval gap is where a fintech platform helps. Instead of applying blind, you can compare lender fit, see which products match your profile, and submit one organized application instead of repeating the same mistakes across five portals. That saves time, cuts avoidable declines, and improves your shot at the better tier of pricing.

If your current debt is already hurting your numbers, fix that before chasing a new offer. A smart first move may be to review whether SBA loan refinancing can lower your existing business debt payments so your next application shows stronger coverage and less strain.

Actionable Steps to Lower Your Business Loan Rate

You don’t lower borrowing costs by hoping the lender is generous. You lower them by reducing uncertainty before the application hits underwriting.

Clean up the file before you apply

Start with credit and reporting hygiene. If your personal or business credit file has errors, old issues that should’ve aged off, or utilization that can be brought down quickly, deal with that first. A lender won’t price you based on your intentions. They’ll price you based on the snapshot they pull.

Then look at cash flow from the lender’s perspective. In a tighter credit market, lenders often require a Debt Service Coverage Ratio of 1.25x to 1.5x, meaning the business needs to produce $1.25 to $1.50 in cash flow for every $1 of debt payment, according to Calder Capital’s market update on debt service requirements.

That means you should know your repayment capacity before the lender tells you. If your current debt load is already squeezing coverage, your next move may not be a new loan. It may be restructuring, refinancing, or reducing existing obligations first. If that’s your situation, review this guide on when SBA loan refinancing can lower business debt payments.

Make underwriting easy

Underwriting is not just analysis. It’s pattern recognition. The easier you make the story to understand, the less risk the lender feels.

Bring these items in ready-to-go condition:

- Current financial statements. Profit and loss, balance sheet, and a sensible explanation for any swings.

- Business bank statements. Lenders want to see cash behavior, not just reported income.

- Debt schedule. Show what you already owe and how the new debt fits.

- Use of proceeds memo. One page is enough if it’s specific.

- Ownership and entity documents. Don’t make the lender chase signatures, structures, or authority.

Short version: don’t submit a scavenger hunt.

Choose the right loan for the use

A lot of rate pain comes from product mismatch. Owners ask for “the cheapest loan” when they should ask for “the cheapest suitable loan.”

For example:

- Equipment purchase: use equipment financing or a fixed-asset structure.

- Working capital cushion: use a revolving product or flexible SBA option.

- Expansion with a longer payoff period: avoid short-term financing that forces repayment before the growth shows up.

- Temporary receivables delay: solve the timing problem without locking yourself into a habit of expensive advances.

If you walk into the market with the wrong request, even a good lender may steer you into a more expensive lane. The right structure lowers risk. Lower risk usually helps pricing.

How to Compare Loan Offers and Find the True Cost

A lot of owners compare loan offers the way people compare airline tickets. They look at the first number they see and assume they’ve found the deal. Then fees, repayment frequency, and hidden pricing show up like baggage charges.

APR is the only honest comparison

If one lender quotes an interest rate, another quotes a factor rate, and a third quotes a weekly payment, you do not yet have three comparable offers. You have three different languages describing cost.

That’s why APR matters. It forces every offer onto the same field.

According to SaaSrise’s guide to debt capital pricing and APR conversion, invoice factoring with a 10% fee on a 60-day receivable can translate to over 60% APR, and a 1.30 factor rate on a $100,000 loan repaid over 12 months equals a 42% APR. That’s exactly why “only a 30% fee” can be a trap.

If you want help translating confusing offers into apples-to-apples numbers, this explainer on calculating the real cost of a small business loan is worth bookmarking.

The cheapest monthly payment is not always the cheapest loan. Slow payments can hide a high total cost. Fast payments can crush cash flow even when the quoted fee sounds modest.

Questions to ask before you sign

Use this checklist when offers arrive:

- What is the APR? If the lender won’t state it clearly, calculate it or walk away.

- How often do I pay? Daily or weekly repayment changes the cash flow burden.

- Are there fees beyond interest? Origination charges and servicing costs matter.

- Is the rate fixed or variable? Predictability matters if margins are tight.

- What happens if I repay early? Some products don’t reward early payoff the way owners expect.

Plain advice. Don’t buy financing the way you buy office supplies. Slow down enough to translate the cost. Ten extra minutes on comparison can save months of regret.

Secure Your Best Rate Fast with Business Loan Warrior

You need funding this week. One lender asks for three months of statements. Another wants six. A third gives you a teaser rate, then stalls once underwriting starts. Meanwhile, the good offer expires, and you are still uploading the same files to different portals.

Why the old process wastes time

The problem is not just lender speed. It is the way owners shop.

Too many business owners go lender by lender, wait for answers, and only start comparing options after time has already been lost. Then the file is incomplete, underwriting drags, and the strongest rate is out of reach. Low-cost lenders tend to reward clean applications and clear documentation. If your package is messy, you usually do not get their best pricing.

Rate shopping should work like bidding out a major vendor contract. You do not ask one supplier, hope for the best, and sign blind. You gather options, line them up, and push for terms you can defend.

How a modern process changes the outcome

Business Loan Warrior cuts out the duplicate work that slows borrowers down. You fill out one no-fee application, check pre-approval without affecting credit, and review offers in one place instead of chasing separate lender portals.

That improves more than convenience.

- Less repeated work. You submit your business information once instead of retelling the same story to every lender.

- Faster rate comparison. Side-by-side options make it easier to spot which offer is actually competitive.

- Stronger applications. Secure account connections and organized document collection reduce underwriting delays.

- Better approval strategy. You can judge rate, structure, and fit at the same time, before you waste days on the wrong lender.

A good platform does not manufacture a cheap loan. It helps you get to the lenders and loan structures that match your profile faster, with fewer mistakes and less back-and-forth.

That is a significant advantage. Better rates are tied to better process. If your application is organized, your comparison is faster, and your lender match is tighter, you have a better shot at approval and a better shot at the rate you came for.

Frequently Asked Questions About Business Loan Rates

Can I get a business loan with bad credit

Yes, but your choices narrow and the price usually worsens. Lenders that move faster and ask for less documentation often charge more for that flexibility. If your credit profile is weak, focus on improving the file, tightening financial statements, and choosing a loan request that is easy to defend.

Are rates higher for newer businesses

Usually, yes. Newer businesses have less history, fewer statements, and a shorter track record of repayment capacity. That doesn’t mean financing is impossible. It means documentation, bank activity, and a sensible use of funds become even more important.

Should I choose a fixed or variable rate

Pick fixed when predictability matters more than flexibility. Pick variable when you understand how changing benchmarks can affect payments and your cash flow can absorb movement. If your margins are thin, fixed is often easier to manage because surprises are expensive.

What’s the smartest first move if I need funding soon

Get your documents organized before you apply anywhere. Most delay comes from missing information, not just lender speed. A borrower who can produce clean statements, a clear debt schedule, and a precise use of proceeds usually gets better traction than the borrower who starts applying first and organizing later.

If you want to see what your business qualifies for without wasting days on duplicate applications, Business Loan Warrior is a practical place to start. You can complete one no-fee application, check pre-approval without affecting credit, compare customized options in a secure dashboard, and move faster from rate shopping to funded capital.