Your revenue is strong. Orders are moving. Payroll is covered. Then a large inventory buy, equipment replacement, acquisition opportunity, or project delay hits your cash cycle at exactly the wrong time.

You ask your bank for speed and get a document list instead. Statements. tax returns. internal financials. committee review. more questions. For an established company, that process can feel backward. The business is healthy now, but the lender is still staring at old paperwork.

That’s why business loan no bank statements searches aren’t just coming from startups anymore. Mature companies use these products when they need capital tied to current business performance, not a slow file review. The key is understanding what lenders are really evaluating, what documentation still matters, and where strong companies accidentally create risk for themselves.

Table of Contents

- Why Smart Businesses Now Look Beyond the Bank

- How Lenders Verify Your Income Without Statements

- Loan Types and Alternative Documentation

- Understanding the True Costs and Modern Risks

- How to Prepare Your Application for Fast Approval

- Choose the Right Offer with Business Loan Warrior

Why Smart Businesses Now Look Beyond the Bank

A lot of owners still assume no-bank-statement financing is a niche option for weak borrowers. That’s outdated. Many established businesses use it because the underwriting matches how they operate: fast deposits, multiple revenue channels, and constant working capital decisions.

The market has moved in that direction for a reason. Non-bank lenders’ share of the small business loan market grew from 19% in 2016 to approximately 32% today, and their approval rates of nearly 25% often double the 15-20% rates seen at traditional banks, according to Capital Bank’s summary of FDIC and SBA lending data.

Speed changed the definition of a strong application

Traditional banks often reward a tidy historical file. Alternative lenders often reward current operating strength. Those are not the same thing.

A company can produce substantial revenue and still look awkward inside a bank process if it has:

- Multiple banking relationships tied to different divisions or locations

- Processor-driven deposits from platforms like Stripe or Square

- International payment flows that don’t land neatly in one domestic statement trail

- Seasonal cash movement that makes old-period statements less useful than current transaction data

That shift has turned alternative lending into a practical tool, not a fallback.

Strong businesses don't always lose at banks because the company is weak. They often lose because the documentation format doesn't match the lender's workflow.

Why established firms are using these loans strategically

For a larger operating company, timing matters more than theory. If you need to secure inventory, bridge receivables, replace equipment, or move on a location, waiting weeks for a conventional review can cost more than the financing itself.

That’s the primary appeal of no-bank-statement lending. It prioritizes verification methods built around live business activity. If you want a broader read on how that shift is changing commercial finance, alternative lenders are redefining business financing in ways many owners now treat as normal.

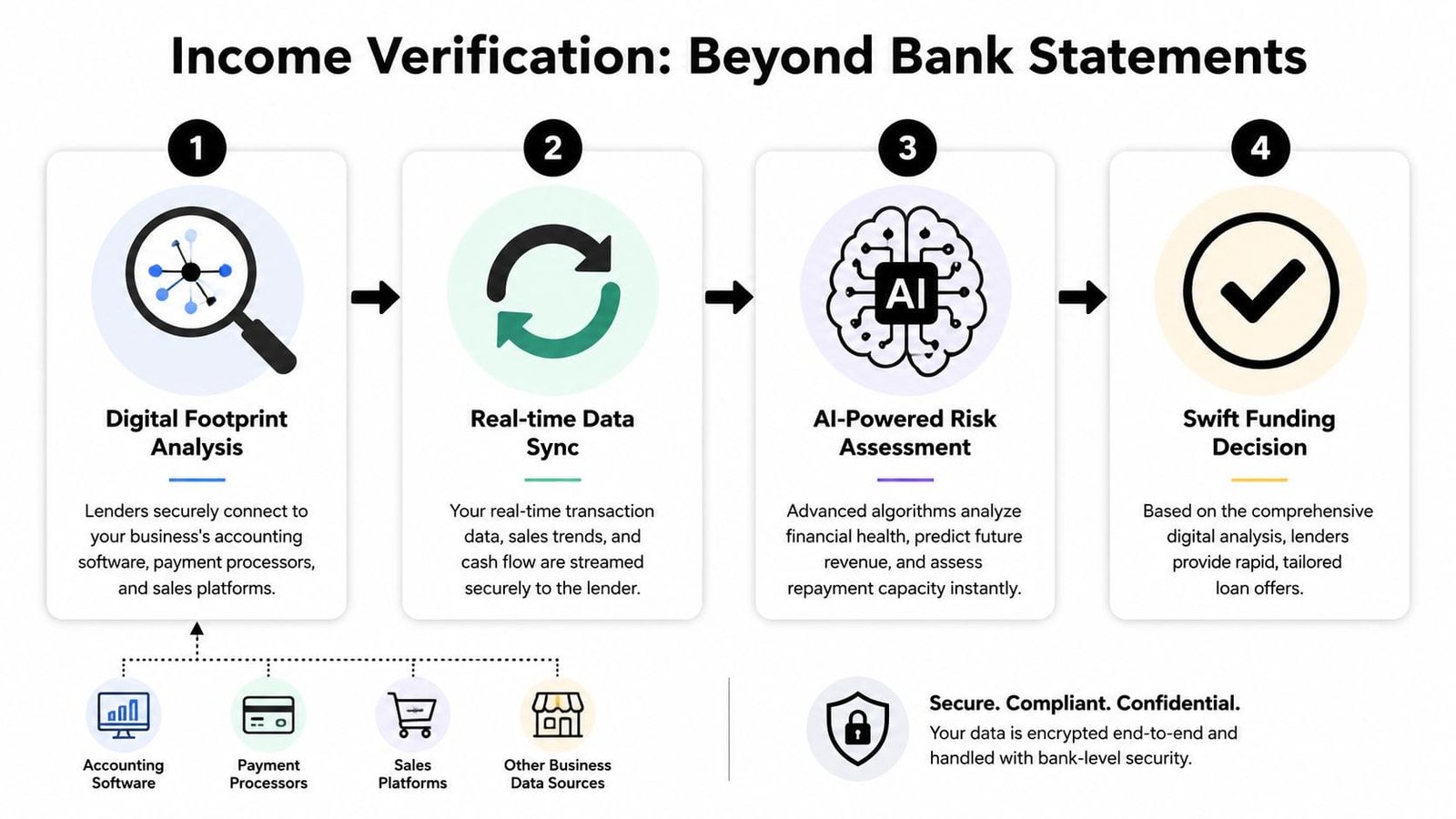

How Lenders Verify Your Income Without Statements

“No bank statements” doesn’t mean “no verification.” It means the lender may verify income through direct data connections and alternative records instead of asking your staff to export PDFs and assemble a package by hand.

Old underwriting is like reading a coroner’s report. Modern underwriting is closer to reading a live monitor. The lender wants to know how cash is moving through the business right now, whether deposits are stable, and whether repayment fits the current rhythm of operations.

What lenders actually pull and score

Many lenders use secure API connections to pull transaction-level banking data directly from connected accounts. Instead of reviewing static statement files, they analyze live or recent activity through systems that can map deposits, withdrawals, balances, and recurring payment behavior.

According to Crestmont Capital’s guide to no-doc business loans, lenders use algorithms to score metrics such as Monthly Gross Deposit Average (MGDA) and Revenue Volatility Index (RVI). The same source notes that low volatility and consistent deposits can lead to funding in under 24 hours, with approval rates up to 70% for qualified businesses.

That matters because algorithms often look for patterns a manual reviewer may miss, including:

- Deposit consistency across recent operating periods

- Cash flow stability rather than just total revenue

- Payment timing on recurring obligations

- Sector-specific cycles such as retail peaks or restaurant seasonality

Why some businesses get approved fast

If your data is clean, the lender doesn’t need to wait for a human underwriter to rebuild your business from a stack of files. The system can already see the main signals.

A clean file usually looks like this:

- Revenue lands predictably through identifiable channels.

- Cash flow stays positive consistently enough to support repayment.

- Volatility is manageable rather than erratic.

- Data sources match each other across banking, accounting, and processor records.

Practical rule: If your deposits are spread across five systems and none of them reconcile neatly, your problem isn't revenue. It's readability.

That’s why preparation still matters. “Minimal documentation” often means fewer uploads, not less scrutiny. In many cases, it’s worth reviewing what lenders expect for a fast decision before you apply. This breakdown of minimal documentation for a quick small business loan captures the operating logic well.

Loan Types and Alternative Documentation

“Business loan no bank statements” is really an umbrella term. Several products fall under it, and each one relies on a different substitute for traditional statements.

For established companies, the best fit depends less on the marketing label and more on what data your business can present clearly. A processor-heavy company may fit one structure. A business with strong accounting records and trade credit may fit another. A contractor buying equipment may need a different lane entirely.

Alternative Funding Products and Their Documentation

| Loan Product | Primary Alternative Document | Typical Use Case | Common Repayment Structure |

|---|---|---|---|

| Merchant cash advance | Card processing history or merchant processor data | Short-term working capital tied to sales activity | Automated remittance tied to sales or fixed daily/weekly payments |

| Short-term business loan | Connected banking data, accounting software data, or revenue records | Inventory, payroll support, project gaps, urgent operating needs | Fixed daily, weekly, or monthly payments |

| Business line of credit | Accounting platform data, banking connection, business credit profile | Ongoing access to working capital for uneven timing needs | Draw-based repayment |

| Equipment or construction financing | Asset information plus operating data and credit profile | Equipment purchases, specialized tools, project-related financing | Scheduled installments tied to term |

| Invoice financing | Accounts receivable records and customer invoice data | Bridging slow-paying receivables | Repayment tied to collected invoices |

What high-revenue companies often use instead of statements

Lenders may accept a mix of records that tell the same story a statement normally would. That can include:

- Processor reports from Stripe, Square, or merchant service providers

- Accounting software data from systems like QuickBooks or ERP platforms

- Business credit information that shows payment behavior with vendors

- Receivables records if a large portion of revenue sits in invoices rather than settled deposits

- Asset data for equipment-related lending

Larger firms run into what I think of as the bank statement paradox. The business is not under-documented. It is over-distributed. Revenue is real, but it lives across accounts, processors, entities, and systems.

If your company has strong cash generation but weak document consolidation, the lender won't automatically say no. They will ask for a format they can score.

What lenders look for in statement-free models

For established firms, some lenders now use bank data-only models that combine business credit and personal credit signals. According to Biz2Credit’s comparison of no-doc and bank-statement loans, lenders may combine business credit scores such as PAYDEX above 80 with personal FICO scores of 600+, enabling approvals up to $250K with factor rates of 1.15-1.4, often closing in 1-2 days.

That’s useful context for owners who assume every no-bank-statement product is loose or complex. Many of these programs are highly structured. They just use a different evidence set.

What works well:

- One primary operating narrative. Even if you have many accounts, the lender should be able to trace how money enters and moves.

- Consistent system exports. If your accounting software and processor data disagree, approval slows down.

- A clear purpose for funds. Working capital, equipment, and receivables support each fit different structures.

What doesn’t work:

- Sending screenshots from multiple platforms with no reconciliation

- Calling a loan “no doc” and assuming the lender won’t verify repayment ability

- Applying for a long-term need with a short-term product because it funds faster

A short-term advance can solve a timing gap. It can also create a new one if the repayment cadence is too aggressive for your operating cycle.

Understanding the True Costs and Modern Risks

Fast capital is useful. It is not cheap by accident. If a lender can move quickly with less manual review and more flexible underwriting, that convenience usually shows up in pricing, repayment structure, or both.

A lot of borrowers make the same mistake here. They compare only the advance amount and the payment amount. That’s not enough. You need to know the full payback, the payment frequency, and whether the term matches the reason you’re borrowing.

What factor pricing means in practice

Many no-bank-statement products use a factor rate rather than a traditional interest structure. That means the lender applies a multiplier to the amount advanced, and you repay the fixed total.

The important point is simple: a factor rate tells you the total repayment multiple, not the full economic cost in the same way an APR does. If the term is short and payments are frequent, the effective cost can feel much heavier than the pricing looks at first glance.

Use this checklist when you review an offer:

- Total payback: What is the exact amount leaving the business over the full term?

- Payment cadence: Daily and weekly payments hit cash flow differently from monthly payments.

- Term fit: A short-term product should fund a short-term need.

- Fees: Origination and other charges change the actual cost.

A working capital bridge can be sensible. Funding a long-arc expansion project with a very short repayment schedule usually isn’t.

The inverse documentation problem

This is the underwriting shift many experienced operators still miss. Years ago, “no bank statements” sounded like convenience. Today, for some lenders, refusing to share verifiable data can look like a warning sign.

According to SoFi’s overview of no-doc business loans, lenders now distinguish between borrowers who cannot provide bank statements and those who will not provide them. The latter can trigger enhanced scrutiny and may lead to higher rates or denial, even when deposits are strong.

That distinction matters for established companies. A large operating business that refuses account linking or declines to provide equivalent data may cause the lender to assume there’s an issue the borrower doesn’t want surfaced.

A mature company that says, “Trust us, revenue is strong,” but won't let the lender verify it is creating its own risk.

Here’s a useful way to think about it. “No bank statements” should mean different evidence, not no transparency.

For a quick visual walkthrough of the cost and underwriting trade-offs, this video gives helpful context before you accept a fast-capital offer.

How to Prepare Your Application for Fast Approval

Strong applications rarely happen because the borrower got lucky. They happen because the financial story is easy to verify.

For larger businesses, the challenge usually isn’t proving that revenue exists. The challenge is making that revenue legible to an underwriter who doesn’t know your internal setup. That gets harder when deposits flow through multiple accounts, payment processors, business units, or cross-border channels.

According to AMP Advance’s discussion of no-doc lending and fragmented business records, high-revenue businesses in the $20M-$50M+ range often struggle because they need to present a consolidated financial picture across multiple bank accounts or payment processors, and lenders increasingly rely on technology to verify acceptable bank statement equivalents.

Build a clean data package

Think like an underwriter for a minute. They’re asking one question: can they verify stable repayment capacity without chasing your controller for three rounds of clarification?

Start with these items:

- Primary revenue map: Show where money enters the business. Bank accounts, processor accounts, receivables systems, and major operating entities should connect logically.

- Accounting export: Pull clean reports from QuickBooks or your ERP that match the period under review.

- Processor support: If sales land through Stripe, Square, or merchant services, include those reports as part of the income trail.

- Credit profile check: Review business credit and owner credit in advance so there are no surprises.

- Use-of-funds summary: Keep it short. The lender should immediately understand why the capital is needed and how it will be repaid.

Remove avoidable friction before underwriting starts

A few practical fixes can speed things up a lot:

- Consolidate explanations, not necessarily accounts. You don’t need to rebuild your treasury structure. You do need a simple summary that explains it.

- Match names across systems. If your legal entity, DBA, and processor profile don't line up, approval slows.

- Address unusual deposits early. Large one-off transfers, affiliate movements, and owner injections should be labeled before the lender asks.

- Be ready to link data securely. If the lender uses connected account verification, hesitation can be interpreted as risk.

Underwriter view: Clean data shortens the distance between “interesting file” and “fundable file.”

Many owners lose time because they send too much noise and not enough structure. Ten disconnected reports are less useful than three reconciled ones.

If you’re getting ready to submit, this guide to business loan applications is worth reviewing for the mechanics that often slow approvals.

What tends to help most for established companies:

- A single point of contact who can answer underwriting questions quickly

- A reconciliation sheet tying processors, accounting records, and operating accounts together

- A realistic request amount that fits the documented cash profile

- A willingness to explain complexity plainly without overlawyering the file

What tends to hurt:

- Saying “our business is too advanced for standard underwriting methods”

- Uploading partial data and expecting the lender to assemble the story

- Treating account linking as optional when the product depends on digital verification

Choose the Right Offer with Business Loan Warrior

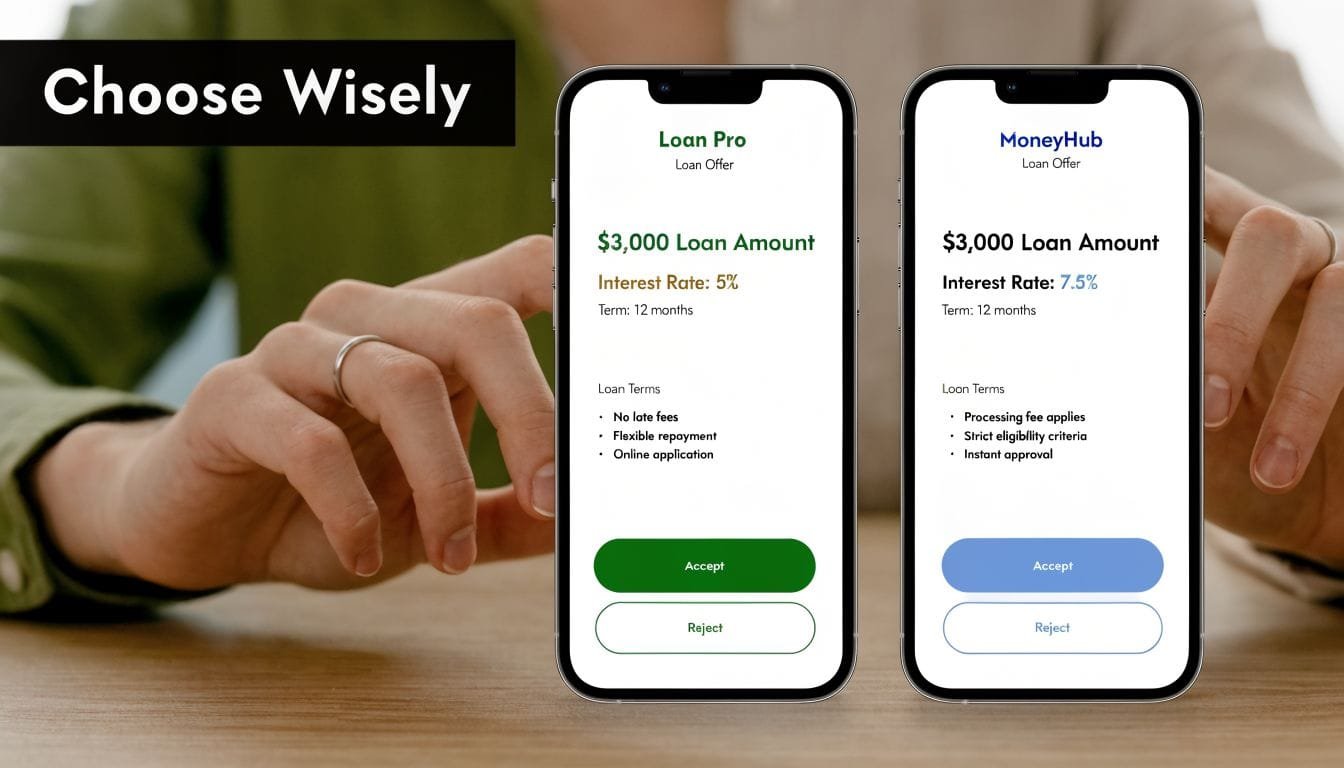

When offers arrive, most borrowers focus on approval first and details second. That’s backwards. Approval is only the start. The real question is whether the structure helps the business or pressures it.

What to compare before you accept

Two offers can look similar on the surface and behave very differently in your cash flow. Put them side by side and review:

- Funding amount versus what you need

- Total payback rather than just the quoted rate

- Repayment frequency and how it lines up with your receivables cycle

- Term length relative to the use of funds

- Any fees or holdbacks that change net proceeds

A good offer does more than fund fast. It fits the life of the problem you’re solving.

For example, a short-term bridge may work well for inventory that turns quickly. It may be a poor choice for expansion spending that pays back over a longer arc. The wrong structure can make a healthy business feel tight for months.

Why a centralized process matters

This is where platform design matters as much as lender choice. If you’re comparing multiple offers manually, email chains and scattered term sheets create mistakes fast. A centralized process gives you a better shot at comparing real terms cleanly and responding to underwriters without duplication.

Business Loan Warrior is built for that workflow. Through a single, no-fee application, owners can check pre-approval without affecting credit, connect accounts securely, review offers in one dashboard, and communicate with underwriters without repeating the same intake over and over.

The best borrowing decision usually comes from better comparison, not harder negotiation.

For businesses that need speed but still want control, that combination matters. You reduce administrative drag, keep documentation organized, and compare transparent options with less guesswork.

If you want to review real funding options without filling out multiple applications, Business Loan Warrior gives you one secure place to check pre-approval, compare offers, and move from application to funding with less friction.