You're probably facing a familiar problem. Revenue is healthy, the business is moving, and growth isn't the issue. Timing is. A supplier wants payment before receivables clear. A new location needs build-out capital. Equipment has to be ordered now, not after next quarter closes.

That's where the business loan vs line of credit decision gets real.

Most articles make this sound simple. Loan for big purchases. Line of credit for flexibility. That's directionally true, but it's not enough for an established company doing serious volume. For a business in the $20M to $50M revenue range, the wrong structure can distort cash flow, weaken covenant headroom, and leave you paying for flexibility you barely use.

The better question is not which product is “best.” It's which product matches the way your business consumes capital, how lenders will underwrite your profile today, and what the total cost looks like under real usage patterns.

Table of Contents

- Choosing the Right Fuel for Your Business Growth

- The Core Difference A Lump Sum vs A Revolving Account

- A Detailed Comparison of Key Financial Terms

- Matching the Right Funding to Your Business Scenario

- How Lenders Assess Your Qualification for Each Product

- A Decision Framework for Choosing Your Best Option

- Applying for Funding in the Digital Age

Choosing the Right Fuel for Your Business Growth

Capital should solve a business problem. It shouldn't create a second one.

Owners often start the business loan vs line of credit conversation by asking about rate, speed, or limit. Those matter, but they come after the strategic question. What exactly are you trying to fund, and how predictable is that need? If you miss that step, you can end up with a structure that fights your operating model instead of supporting it.

Start with the use case

A clean funding decision usually starts with one of these realities:

- You know the full cost today. Equipment, expansion work, partner buyouts, or acquisition-related expenses usually fall here.

- You know the need will recur, but not the exact timing. Payroll gaps, uneven receivables, seasonal inventory swings, and surprise operating expenses fit this pattern.

- You want a cushion, not immediate funding. That's where many owners overpay, because backup liquidity can look cheap until fees and variable pricing show up.

If the need is fixed and defined, structure matters more than optionality. If the need is recurring and uneven, access matters more than elegance.

Practical rule: Match the debt product to the cash pattern, not the story you tell yourself about growth.

Ask the questions lenders will ask anyway

Before you apply anywhere, answer these four questions internally:

- Is this a one-time deployment of capital or an ongoing draw-and-repay cycle?

- Can the business support fixed payments every period, even in a softer month?

- Do you need capital for an asset, a project, or operating volatility?

- Would unused flexibility still be worth paying for if you only tap it occasionally?

That last question gets ignored far too often in the mid-market.

Why this decision is more important for established SMBs

A larger small business usually has more financing options, but also more complexity. You may have multiple entities, uneven margin by division, concentration in a few customers, or seasonal working capital bulges. A simplistic answer won't hold up.

The right product protects liquidity, keeps planning realistic, and gives operators room to execute. The wrong one can lock cash into amortization you didn't need, or leave you exposed to a facility that looks flexible but becomes expensive or hard to renew when conditions tighten.

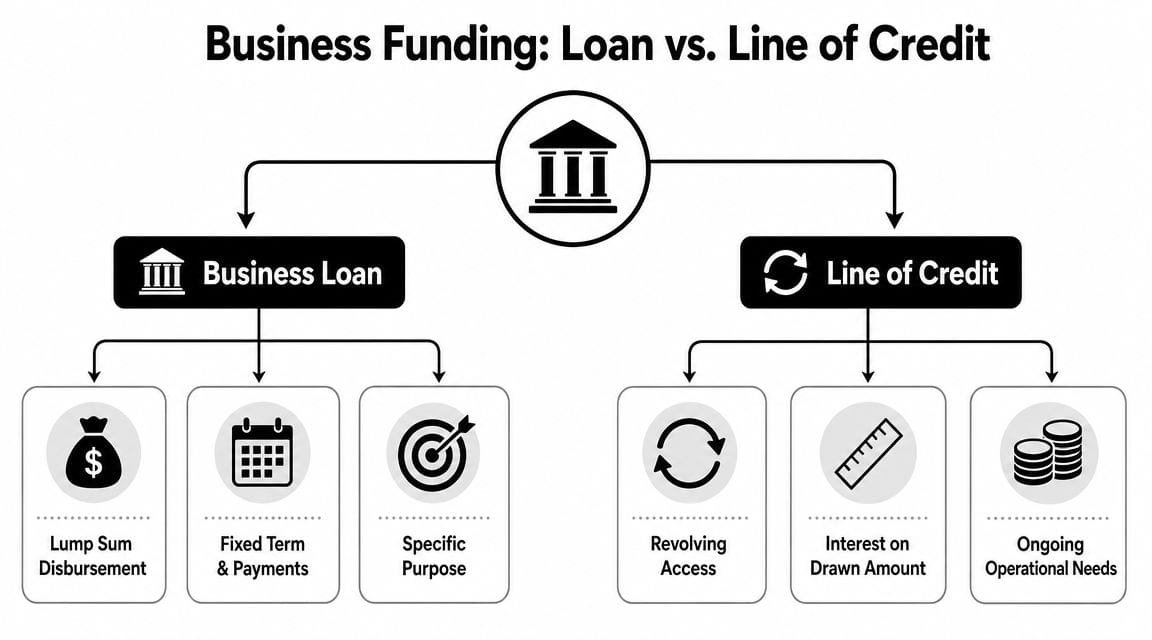

The Core Difference A Lump Sum vs A Revolving Account

The structural difference is straightforward. Its consequences are not.

A business loan gives you one disbursement up front. A business line of credit gives you access to a pool of capital that you can draw, repay, and draw again. That distinction drives funding size, repayment behavior, and how each product fits real operating needs.

Think in terms of delivery, not marketing labels

A loan behaves like a project-financing tool. You identify the need, borrow once, and repay on a defined schedule.

A line of credit behaves like a liquidity tool. You keep access available and use it when timing gaps appear.

According to NerdWallet's comparison of business loans and lines of credit, a business loan is structurally better suited for major capital needs because it delivers a one-time lump sum and usually supports larger funding sizes, while a line of credit is a revolving facility meant for repeated draws and is generally smaller. The same guide notes that loans are a stronger fit for equipment purchases, expansion projects, or acquisition-related outlays where the full capital requirement is known upfront, while lines of credit are better for working capital volatility, payroll gaps, or seasonal inventory swings.

A loan funds a plan. A line of credit supports motion.

That's the cleanest way to think about it.

What this looks like in practice

If you're buying production equipment, the vendor wants a defined payment. If you're opening a location, the contractor schedule is mapped out. In those cases, a lump sum aligns with the obligation.

If your receivables arrive unevenly, or you regularly build inventory ahead of demand, the need is less about one transaction and more about timing. A revolving facility works better because the draw pattern repeats.

Later in the section, this short video gives a quick visual explanation of the difference:

Why owners confuse the two

They often overlap in conversation because both provide capital. But they solve different operational problems.

- Loan mindset: “I need this amount for this purpose.”

- LOC mindset: “I need access because the timing keeps changing.”

- Common mistake: Using a line of credit as long-term project financing, then carrying revolving debt longer than intended.

For a business owner, the takeaway is simple. Don't compare them as interchangeable products. Compare them as different engines built for different loads.

A Detailed Comparison of Key Financial Terms

Once you understand the structure, the next step is comparing how each product behaves financially. During this comparison, a lot of expensive mistakes happen.

Business Loan vs. Line of Credit At a Glance

| Feature | Business Loan | Business Line of Credit |

|---|---|---|

| Funding structure | Lump sum disbursed up front | Revolving access to funds as needed |

| Interest accrual | Typically on the full principal from day one | Generally only on the outstanding drawn balance |

| Rate style | Usually fixed | Often variable |

| Repayment | Scheduled amortizing payments | Flexible payments, often tied to drawn balance |

| Best fit | Defined, one-time capital need | Ongoing working capital or uneven cash needs |

| Predictability | High | Lower |

| Flexibility | Lower after funding | Higher during the life of the facility |

| Fee exposure | Usually simpler to model | May include draw, maintenance, or inactivity fees |

| Typical positioning | Long-term investment or asset purchase | Cash flow management and short-term access |

Cost structure

The most important technical difference is how interest accrues.

As explained in Ramp's analysis of business loan vs line of credit costs, a business loan typically charges interest on the full principal from day one, usually at a fixed rate with scheduled amortizing payments. A business line of credit generally charges interest only on the outstanding drawn balance, often at a variable rate tied to prime. That means a line of credit can be cheaper for short, intermittent borrowing because unused capacity is not funded. The tradeoff is less payment predictability and possible extra charges such as draw fees, annual maintenance fees, or inactivity fees.

If you borrow all the money now and use all of it immediately, a loan often makes cleaner economic sense. If you borrow in bursts and repay quickly, a line can be more efficient.

Repayment behavior

A term loan is easier to budget because payment timing is known. Finance teams like that. Controllers like that. Owners sleeping at night tend to like that too.

A line of credit is more elastic. During draw periods, some structures allow minimum or interest-only payments. That can help when receivables stretch or revenue cadence is uneven, but it also means the facility can stay outstanding longer than planned if discipline slips.

What works: Fixed payments for fixed assets. Flexible draws for variable operating needs.

Funding amount and use of funds

Loans usually win when the requirement is larger and clearly defined. They're built for a full capital deployment at the start.

Lines of credit are generally better reserved for recurring operational needs where you don't want to borrow more than necessary at once. For many established businesses, that means inventory builds, receivable timing, payroll support during temporary gaps, or short-term vendor coverage.

Approval speed and practical friction

Speed often gets treated like a product feature. In reality, it's an underwriting outcome.

A cleaner deal with a clear use of funds, strong financials, and available collateral can move well in either structure. But revolving products can feel faster operationally after approval because you don't reapply every time you need a draw. That convenience has real value if your business routinely needs quick access.

The comparison that actually matters

Don't ask only, “Which rate is lower?”

Ask:

- How much will I draw, and when?

- How long will balances stay outstanding?

- What fees apply even if usage stays light?

- Can the business comfortably carry fixed amortization?

- Will this need repeat after the initial event?

That's the financial core of the business loan vs line of credit decision. One product optimizes certainty. The other optimizes optionality. Your cash pattern tells you which one deserves the job.

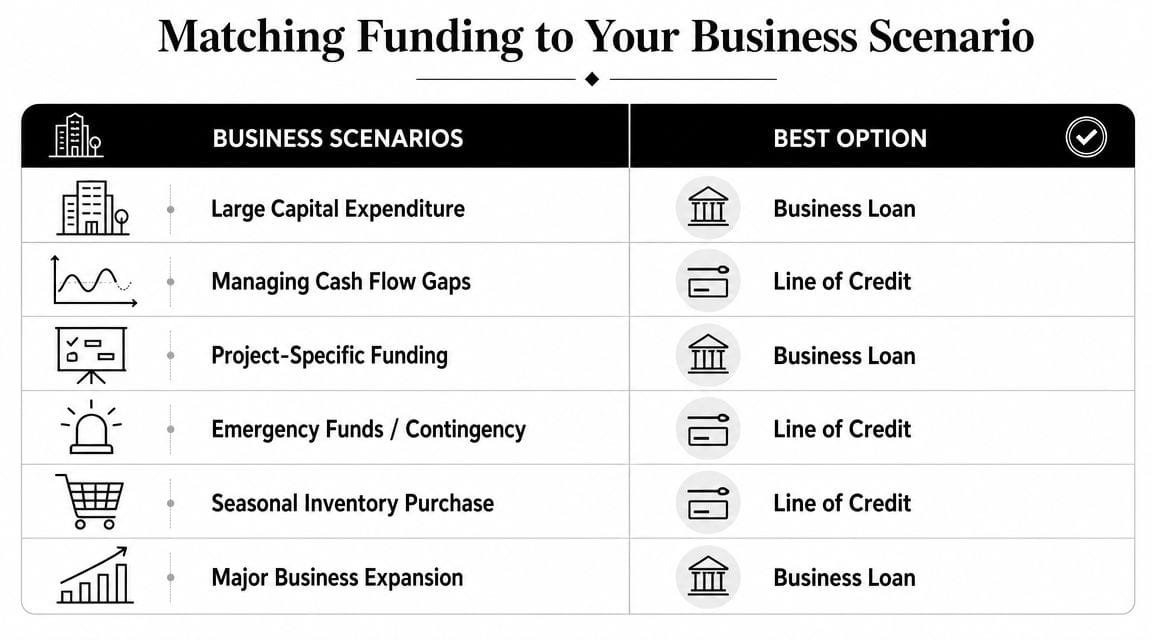

Matching the Right Funding to Your Business Scenario

The best funding choice becomes obvious when you stop talking in generalities and start looking at operating situations.

Equipment purchase with a defined return path

A manufacturer needs a new production machine. The vendor quote is firm, the installation schedule is known, and the asset will generate value over time.

This is usually a business loan situation.

Why it works:

- The capital need is specific.

- The full amount is required up front.

- Repayment can be aligned with the useful life of the asset and the revenue it supports.

- Budgeting is cleaner because debt service is scheduled rather than fluid.

Using a line of credit here often creates the wrong behavior. The business treats a long-term asset like a short-term liquidity need and risks carrying revolving debt longer than intended.

Seasonal inventory and uneven working capital

A restaurant group or retailer has predictable swings. Inventory needs rise ahead of peak periods, then cash converts after sales come in. The business doesn't need all the money all year. It needs access at the right moments.

A line of credit often proves particularly suitable.

The advantage isn't just convenience. It's matching borrowing to actual exposure. You draw when inventory or payroll pressure builds, then reduce the balance as cash receipts improve.

A term loan is clumsy for this because it forces you to fund the whole need in advance, even if the actual usage pattern is staggered.

If the need expands and contracts with the operating cycle, revolving capital usually fits better than fixed principal.

Expansion project with multiple moving parts

Opening a new location or expanding a service footprint is less simple. Some costs are known. Others move around. Leasehold improvements, deposits, equipment, hiring, and pre-opening working capital don't always land on the same timeline.

Many strong businesses should separate the needs instead of forcing a single answer.

A practical structure often looks like this:

- Use a loan for the defined, front-loaded capital requirement such as equipment, construction, or build-out.

- Use a line of credit only if you also need operating flexibility during ramp-up.

That separation keeps long-term investment on a predictable repayment track while preserving liquidity for launch volatility.

Marketing or project spending with uncertain timing

Some expenses don't produce a smooth return path. A marketing push, a temporary staffing surge, or a project with uncertain collections may not justify fixed amortization from day one.

In those cases, owners often prefer a line because it avoids overfunding. But the caution is important. If the spend drifts from short-term bridge to ongoing support, the facility can become a permanent crutch.

The right question isn't whether the expense is important. It's whether the repayment source is clear enough to support a structured obligation.

How Lenders Assess Your Qualification for Each Product

Strong businesses still get surprised in underwriting. Not because they're weak, but because lenders don't evaluate every product the same way.

Product type changes the underwriting lens

According to Academy Bank's guidance on when to use a business line of credit vs a traditional business loan, approval criteria can change materially by product type and lender structure. Secured lines of credit may require collateral, unsecured lines can be harder to qualify for, and some lenders require stronger credit history or financial statements. The same source notes that loans often have stricter repayment terms but can offer larger amounts and lower rates for established borrowers.

That's a useful starting point, but its practical implication matters more. The same company can look attractive for one product and borderline for another.

What lenders usually focus on for a loan

A lender reviewing a loan typically wants to understand whether the business can absorb fixed repayment over time. The emphasis often falls on durability.

Common pressure points include:

- Earnings consistency: Can the company support scheduled payments through strong and soft periods?

- Use of proceeds: Is the capital tied to a defined investment with a clear business rationale?

- Collateral support: If the loan is secured, what asset base stands behind it?

- Financial reporting quality: Established borrowers usually do better when statements are current, coherent, and lender-ready.

For companies in the $20M to $50M range, clean reporting often matters as much as the headline revenue number. Messy intercompany flows, weak documentation, or unexplained margin swings can slow a deal fast.

What lenders often scrutinize for a line of credit

A line of credit shifts the emphasis toward short-term liquidity behavior.

Underwriters often care about:

- Revenue volatility

- Receivables pattern

- Cash conversion rhythm

- How often the business may need to draw

- Whether the business is asking for a backup facility or a disguised long-term funding source

An unsecured line can be especially demanding if the company's cash flow is uneven. The lender knows repayment may depend on future operating performance without the comfort of pledged collateral.

Underwriting reality: Lenders don't just ask whether your business is strong. They ask whether your cash behavior matches the product you want.

A practical qualification framework

When owners assess business loan vs line of credit options, I'd look at four filters before submitting an application:

| Underwriting filter | Loan often fits better when | Line often fits better when |

|---|---|---|

| Business age | The company has an established operating history | The company is established but needs ongoing liquidity access |

| Bankability | Financial statements are solid and organized | Cash flow is solid enough to support revolving access |

| Collateral | Assets are available to support the request | Either collateral exists for a secured line or cash flow is strong enough for unsecured review |

| Revenue volatility | Revenue is stable enough for fixed repayment | Revenue is uneven enough that flexibility matters, but not so unstable that draws look permanent |

That framework won't replace lender underwriting, but it does help you choose the product you're more likely to qualify for now, not just the one you'd prefer in theory.

A Decision Framework for Choosing Your Best Option

The most useful way to decide is to model behavior, not compare marketing claims.

Step through the decision in order

Start with these questions:

Is the need fixed or fluid?

If the full requirement is known and tied to a specific investment, a loan usually deserves first consideration.Will you use most of the capital immediately?

If yes, paying for revolving flexibility may not buy you much.How predictable is repayment capacity?

Businesses with stable cash generation usually handle fixed amortization better. Businesses with uneven collections may value draw flexibility more.Is this short-term variability or a long-term investment?

Don't finance a long-life asset with a structure designed for working capital motion unless there's a very specific reason.

Model the real cost of flexibility

Many owners sharpen the decision in this situation.

As noted in PNC's discussion of business loan vs line of credit tradeoffs, a key consideration is the real cost of flexibility. A line of credit charges interest only on drawn funds, but it can include ongoing fees and variable rates. A business loan offers predictable payments and is often lower-cost for large, one-time needs. PNC also points to a useful framework: compare all-in cost under different draw patterns, such as 20% vs. 80% utilization, to see when flexibility becomes overpriced.

That's exactly the right lens.

If your company expects light, occasional use, the unused access may still be worth paying for if the facility protects payroll, vendors, or inventory continuity. But if you expect to keep a high balance outstanding for long stretches, the line may stop being an efficient working capital tool and start acting like an expensive substitute for a term loan.

Borrowers often focus on interest cost. Sophisticated borrowers model access cost, fee cost, and behavior cost.

A simple recommendation logic

Choose a business loan when these conditions are mostly true:

- The amount needed is clear

- The purpose is defined

- The business can support fixed scheduled payments

- You expect to deploy most of the capital soon

- Predictability matters more than optionality

Choose a line of credit when these conditions dominate:

- The timing of borrowing will vary

- Cash flow has normal operational swings

- You want access without funding the full amount at once

- The need is recurring rather than one-time

- You're prepared to monitor fees and variable pricing carefully

If your answer is “both,” that may be the honest result. Many established businesses use a loan for strategic investment and a line for operating stability. The mistake is not using both. The mistake is using one tool to do both jobs badly.

Applying for Funding in the Digital Age

The application process used to be a major barrier. For many owners, it still is if they're dealing only with traditional channels.

What a practical process should look like

A modern application flow should do three things well. It should reduce paperwork friction, give you visibility into options, and help you understand where underwriting stands.

In practice, an efficient process usually includes:

- One intake point: You submit business details once instead of repeating the same package across multiple lenders.

- Secure financial review: Bank account connections and digital document collection let underwriters review cash flow faster.

- Clear offer comparison: You can evaluate structure, repayment style, and use-case fit without bouncing between fragmented portals.

For an owner or CFO, that matters because financing decisions rarely happen in a vacuum. You're handling vendor negotiations, hiring, forecasting, and collections at the same time. The process has to fit the operating reality.

What still matters before you submit

Even with better technology, clean preparation still wins.

Bring these materials into shape first:

- Current financial statements: Lenders move faster when the numbers reconcile and tell a consistent story.

- Bank statements and revenue support: Especially important when cash movement matters more than tax-return history.

- A sharp use-of-funds explanation: “Growth” is not enough. State what the capital will do.

- Ownership and entity documents: Delays often come from simple documentation gaps, not underwriting resistance.

Speed is useful, but fit matters more

The easiest mistake in digital lending is treating fast access as proof of a good structure. It isn't. Quick approvals are valuable only if the product matches the need and the terms make sense operationally.

A good platform helps you compare options before you commit. A great one also makes repayment and ongoing visibility easier after funding closes.

If you're weighing a business loan vs line of credit and want a faster way to compare appropriate options, Business Loan Warrior offers a no-fee application, pre-approval without affecting credit, secure account connection, and a dashboard to track offers, repayments, and funding progress. For owners who want speed without losing clarity, it's a practical place to evaluate which structure fits the business.