Your business can be healthy on the surface and still get rejected for financing.

That happens every week. Revenue is coming in. Payroll is covered. Customers are buying. Maybe you’re running multiple locations or managing a company that does serious volume every month. Then a lender pulls personal credit, sees old damage, and treats the whole business like it’s unstable.

That disconnect is what makes the search for a business loan with bad credit so frustrating. You’re not asking for rescue money. You’re trying to fund inventory, equipment, expansion, bridge timing gaps, or smooth out operating pressure. The business works. The file doesn’t.

For established companies, especially those doing meaningful annual revenue, the pertinent question isn’t “Can I get funded?” It’s “Which lenders will look at the business instead of stopping at the score?”

Table of Contents

- The Good Business Bad Credit Dilemma

- What Lenders See Beyond Your Credit Score

- Comparing Your Viable Financing Options

- Funding Strategies for Established Mid-Sized Businesses

- Real-World Scenarios Two Paths to Funding

- Your Pre-Application Checklist to Get Approved

- How Business Loan Warrior Simplifies Your Funding Search

The Good Business Bad Credit Dilemma

A lot of owners assume a denial means they asked at the wrong time. Often, that isn’t true. It means they asked the wrong lender.

Banks have been getting tighter, not looser. Through 2025, thirteen consecutive quarters of data showed banks tightening credit standards for small business loans, and approval rates at large banks for any financing amount fell to as low as 13% in some Q2 2025 reports, down from 44% in 2024, according to Cardiff’s state of small business lending report.

That matters because many owners still approach financing like it’s a merit badge. Strong business, loyal customers, tax returns, bank statements. They expect those things to outweigh old credit issues. In a tight bank market, they often don’t.

Why this isn’t just your problem

The lending market now splits borrowers into very different lanes. Prime borrowers still get traditional offers. Everyone else gets pushed toward lenders that rely more on deposits, receivables, payment processing, collateral, and operating history.

Bad personal credit can be a financing problem without being a business failure.

If you’re running a company with real sales, the path forward usually isn’t to keep reapplying at banks that want a cleaner personal file. It’s to find underwriting that matches how your business performs.

What actually helps

Three things usually move the file forward:

- Clear business cash flow: Lenders want evidence that the business generates enough incoming revenue to support repayment.

- A specific use of funds: “Working capital” is acceptable. “Working capital to cover seasonal inventory build” is better.

- A lender-product match: Fast money, asset-backed money, and SBA-backed money are not interchangeable.

That’s the practical shift. Stop asking, “Will bad credit kill my chances?” Start asking, “Which underwriting model fits my business?”

What Lenders See Beyond Your Credit Score

A $30 million company can still get tripped up by a 580 personal credit score. I see it often. The owner assumes the file is dead on arrival, even though the business has real customers, steady receivables, and equipment on the floor that could support financing.

That is not how many nonbank lenders underwrite established companies. They still care about credit, but they also want to know a more practical thing. Does this business produce enough cash, or hold enough collateral, to support a new payment?

Your score is one signal. Cash flow and assets carry more weight.

For a mid-sized company, personal credit is rarely the full story. Underwriters often spend more time on bank statements, accounts receivable aging, equipment value, customer concentration, and existing debt service than owners expect. A weak score raises questions. Strong operating performance can answer them.

This matters more for established businesses than for startups. A startup with bad credit has very little else to show. A company doing $20 million to $50 million in annual sales has a track record. Lenders can review deposit volume, margins, seasonality, lien position, and collateral coverage. That creates options that do not exist for a younger company.

The comparison I use with clients is simple. Credit is the cover page. Cash flow is the operating manual. Assets are the backup plan if the deal goes sideways.

What underwriters usually focus on first

If you want to judge your odds before applying, review the same areas the lender will review:

- Deposit consistency: Regular deposits usually matter more than one strong month. Lenders want to see a business that collects predictably.

- Debt service capacity: They look at how much free cash flow remains after payroll, rent, taxes, and existing loan payments.

- Accounts receivable quality: B2B firms with credible customers and clean aging reports often have more financing paths than owners realize.

- Collateral position: Equipment, vehicles, inventory, and in some cases owner-occupied real estate can improve the file.

- Time in business and trend line: A ten-year company with a temporary credit issue reads very differently from a one-year company with uneven revenue.

- Use of funds: Buying inventory for a contracted order is easier to underwrite than a vague request for general growth capital.

One weak area does not always kill the deal. Two or three weak areas usually change the structure, the rate, or both.

What this means for a mid-sized borrower with poor personal credit

The biggest mistake is applying as if this were still a consumer-style credit decision. For an established company, the better approach is to present the business as an operating asset. Show cash coming in. Show what supports repayment. Show what the lender can rely on besides the owner's score.

That can mean different things depending on the company. A manufacturer may qualify because equipment and receivables support the request. A distributor may get farther by showing purchase orders, inventory turns, and strong customer payment history. A service company may win approval based on contract revenue and clean bank statement performance.

Practical rule: If personal credit is the weak point, the business file has to be organized enough to shift the conversation to revenue, debt capacity, and collateral.

Owners who prepare for that discussion tend to get better results and waste less time on the wrong lenders. If you want a clearer view of how to present a stronger file, this guide on business loan approval strategies when other lenders decline you is worth reading.

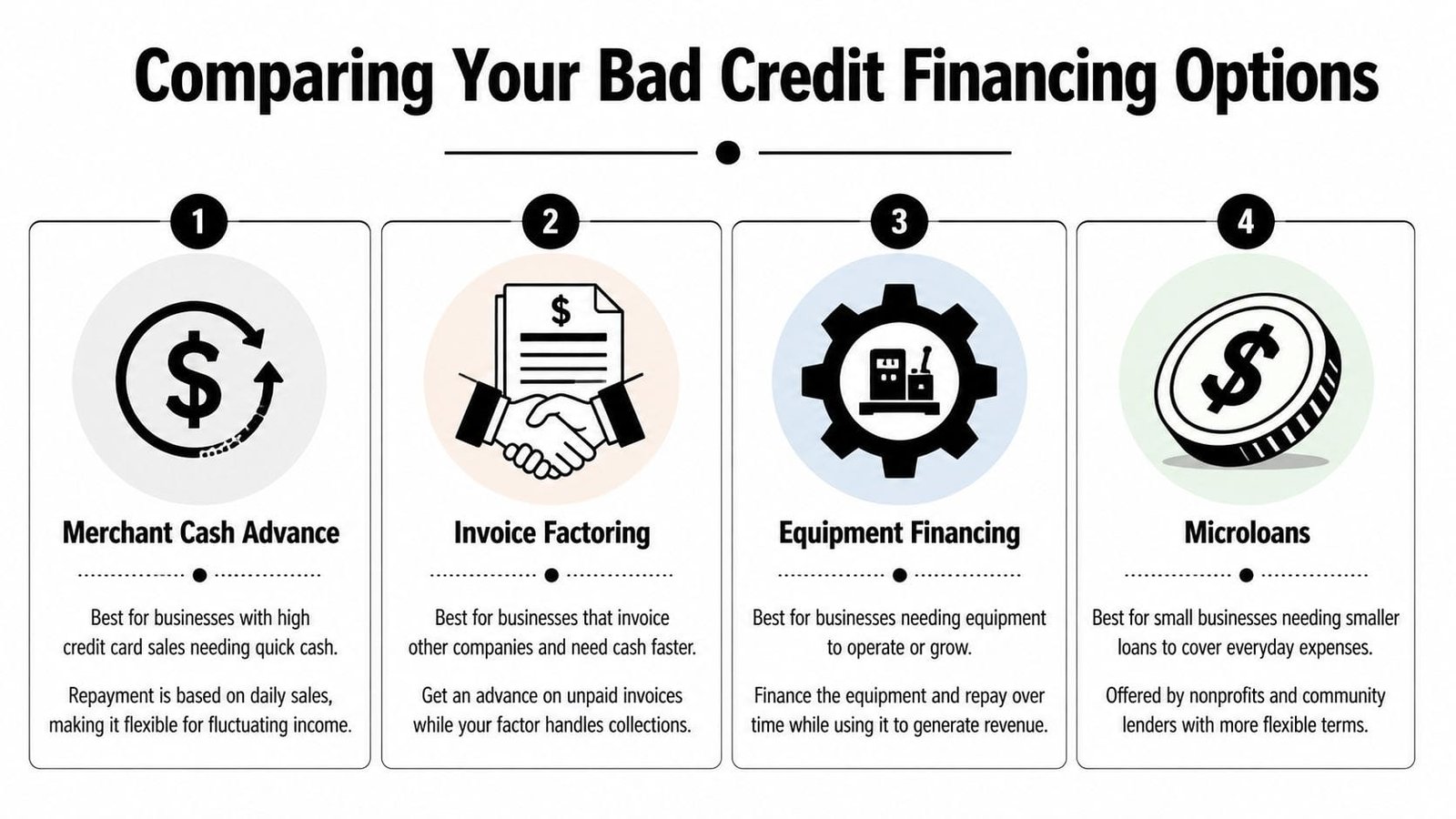

Comparing Your Viable Financing Options

A $30 million company can still make a bad financing choice when the owner is under pressure. I see it often. A lender says yes quickly, the money hits fast, and 45 days later the repayment schedule starts choking working capital.

That is why product fit matters more than approval alone.

The right structure depends on what the money has to do. Covering a short receivables gap, buying a piece of equipment, and funding a long expansion cycle are different jobs. Mid-sized companies with weak personal credit usually have more options than they think, but only if they choose based on cash flow, collateral, and timing instead of urgency.

Revenue-based funding for card-heavy businesses

Revenue-based funding can work for companies that process steady card volume and need speed. Lenders in this part of the market often focus more on deposit history and sales consistency than on the owner's score. That makes these products relevant for restaurant groups, retail operators, multi-location service businesses, and other companies with predictable card receipts.

The trade-off is cost and payment frequency. Daily or weekly remittances may feel manageable when sales are strong, but they can become restrictive if margins are thin or receipts swing by season. For a mid-sized business, that matters. A product that solves a two-week cash crunch can still create a three-month liquidity problem if the holdback is too aggressive.

Approval is only the first screen. Deal structure matters more. This overview of how alternative lenders are redefining business financing is useful if you want a clearer picture of how nonbank lenders price speed, risk, and flexibility.

A quick visual can help before you compare products in detail.

Asset-backed options when you have invoices or equipment

Asset-backed financing is often the cleaner path for established companies with real operating scale.

Invoice factoring fits B2B businesses that bill creditworthy customers on terms. The factor is primarily underwriting the invoice and the account debtor's payment strength. For a distributor or manufacturer doing $20 million to $50 million in annual sales, that can be far more practical than chasing unsecured capital tied closely to personal credit.

Equipment financing works well when the purchase is identifiable and the asset holds value. Trucks, production machinery, medical devices, and construction equipment all give the lender something tangible to secure. That usually improves pricing and term options compared with unsecured short-term money.

Secured lines of credit can be a strong fit for companies with stable receivables, inventory, or deposit balances. They take more documentation and more lender diligence, but the flexibility is often better. A revolving line gives finance teams room to manage timing gaps without refinancing every few months.

SBA paths when the business is stronger than the credit file

SBA financing still belongs on the list for some borrowers, even with poor personal credit.

It is slower. It is paperwork-heavy. It also can be one of the few ways an established company gets longer terms and lower monthly debt pressure when the business itself is performing well. Lenders that make SBA loans typically look closely at repayment ability, financial reporting, management experience, collateral support, and how the funds will strengthen the business. A weak credit file does not disappear, but it does not always end the conversation.

For mid-sized companies, this option tends to make the most sense when the request is strategic and documented clearly. Equipment expansion, partner buyouts, acquisition support, and refinancing expensive short-term debt are better candidates than vague working capital requests.

| Financing Type | Best For | Typical Cost (APR) | Funding Speed | Key Requirement |

|---|---|---|---|---|

| Merchant cash advance or revenue-based advance | Businesses with strong card sales and urgent needs | Cost varies by provider and structure | Usually faster than bank or SBA paths | Consistent payment processing volume |

| Invoice factoring | B2B companies waiting on receivables | Cost varies based on invoices and customer quality | Often relatively fast once invoices are verified | Eligible invoices from creditworthy customers |

| Equipment financing | Buying vehicles, machinery, or essential equipment | Cost varies by lender and asset strength | Often moderate | Equipment serves as collateral |

| SBA-backed loan | Established businesses seeking larger, more structured capital | Often lower than many non-SBA bad credit options, but deal-specific | Slower than online lenders | Strong business performance, documentation, and lender fit |

The best loan is the one your business can carry without losing flexibility.

Funding Strategies for Established Mid-Sized Businesses

A company doing $20M to $50M in annual sales sits in a different category from a startup or a microbusiness. The revenue profile is stronger. The operating history is longer. The financing need is usually tied to growth, working capital management, equipment, acquisitions, or expansion, not basic survival.

That changes the conversation. For mid-sized businesses in this range, lenders often prioritize monthly revenue of $100K+ and time in business of 1+ years over FICO scores, and options such as invoice factoring or secured lines of credit can have approval rates up to 70% for firms showing $300K+ annual revenue, according to Ameris Bank’s equipment finance overview of bad credit business loans.

Why mid-sized companies get treated differently

When a business has meaningful scale, lenders can evaluate more than a score. They can study receivables, customer concentration, contract flow, deposit history, inventory movement, equipment value, and operating margins.

That provides an advantage if you use it well.

A mid-sized operator with weak personal credit but strong monthly receipts should not approach the market like a newer company seeking unsecured startup money. That’s the wrong frame. The right frame is: this business has measurable cash flow, financeable assets, and a track record.

If your company has scale, lead with the business balance sheet and revenue profile, not with apologies about credit.

How to present a stronger borrowing case

For established firms, the strongest strategy is usually layered:

- Use receivables for working capital needs: If customers pay on terms, invoice financing can convert delayed revenue into present cash.

- Use equipment loans for asset purchases: Keep long-lived assets matched with financing built for those assets.

- Use secured lines for flexibility: A line tied to business strength can be more practical than stacking short-term advances.

- Separate urgent needs from strategic needs: Fast cash may handle a temporary squeeze, but expansion capital deserves a more structured product.

Mid-sized companies also benefit from acting like finance departments, not desperate borrowers. That means showing lender-ready reporting, explaining the use of funds clearly, and identifying which assets support the request. When owners in this bracket do that, weak personal credit becomes one factor in the file, not the whole file.

Real-World Scenarios Two Paths to Funding

A CFO at a $30 million company can face the same bad-credit problem as a much smaller business, but the financing answer should look very different. If the company has real revenue, customer concentration under control, and assets on the balance sheet, the question is not whether funding exists. The question is which structure fits the problem without putting unnecessary pressure on cash flow.

A retail operator choosing speed over price

Consider a multi-location retailer with bruised personal credit and strong daily card sales. Peak season is six weeks out. One store needs an urgent repair, and inventory has to be ordered now, not after a long underwriting cycle.

In that case, a revenue-based advance may be the practical choice. The lender is focused less on the owner’s credit profile and more on whether card receipts are steady enough to support frequent repayment. For a business with predictable daily sales, that can solve a timing problem fast.

Speed has a price.

The repayment usually hits harder and sooner than a conventional term loan or line of credit. For an established retailer, that only works if gross margins are healthy, sales are steady, and the use of funds produces a clear return. If inventory turns quickly and the repair protects revenue, paying more for speed can be rational. If the business is already tight each week, fast money can turn one short-term problem into a longer one.

A contractor using business strength to pursue SBA financing

Now take a construction company doing eight figures in annual revenue. The owner’s past credit issues still show up, but the business itself has improved. Jobs are under contract, equipment has value, and the company wants capital for expansion, not a temporary patch.

That borrower may fit better with an SBA 7(a) lender or another bank partner willing to underwrite the business on its current merits. The lender will spend more time on backlog, receivables quality, historical performance, collateral support, and whether projected cash flow matches how the company operates. A well-built cash flow forecast for a loan strategy carries real weight here because it helps explain repayment in plain numbers.

The questions in underwriting are practical:

- How stable is the project pipeline?

- What do margins look like after labor, materials, and overhead?

- Which assets or receivables support the request?

- Does management have a credible plan for using the capital?

A mid-sized business in this range often gets better results by acting like a serious credit applicant, not a borrower asking for an exception. That means clean reporting, a clear expansion case, and realistic projections tied to contracts or purchase orders.

Strong businesses with weak owner credit still get approved. They get approved when the file shows repayment capacity, collateral support, and a sensible use of funds.

The contractor accepts more paperwork and a slower closing because the structure fits the goal. That trade-off usually makes sense for expansion, equipment purchases, or larger working capital needs where repayment term and total cost matter more than same-week funding.

Your Pre-Application Checklist to Get Approved

A sloppy application gets judged harder when credit is weak. Lenders assume disorganization and repayment risk often travel together. You want to break that assumption before the file ever reaches underwriting.

Clean up the file before anyone reviews it

Start with the numbers.

- Gather core documents: Recent business bank statements, profit and loss statements, balance sheet, debt schedule, and any major contracts or receivables reports that support the request.

- Know the exact ask: Be ready to state how much you need, what it’s for, and what repayment source supports it.

- Review your bank activity: Lenders notice overdrafts, sharp revenue swings, and unusual withdrawals. If there’s a valid reason, prepare the explanation in plain language.

- Check for unresolved issues: Open liens, stale corporate records, and inconsistent entity information can slow down even a willing lender.

If your cash flow is uneven, don’t hide it. Explain it. Seasonal businesses, project-based firms, and expansion-stage companies often have lumpy periods. What hurts borrowers is silence, not imperfection.

Prepare the story behind the request

Underwriting is part math and part judgment. If the use of funds sounds vague, lenders assume the business is plugging holes.

Build a short explanation that answers four points:

- Why you need the money now

- What it will be used for

- How it helps the business produce or protect revenue

- Why the repayment is realistic

That story should sound operational, not emotional. “We need working capital” is weak. “We need capital to bridge receivables tied to signed customer work” is much stronger.

A useful exercise is building a borrowing forecast before you apply. This guide on building a cash flow forecast that empowers your loan strategy can help you pressure-test whether the requested financing fits the business.

Lenders don’t need a perfect company. They need a clear repayment path.

How Business Loan Warrior Simplifies Your Funding Search

Most owners with bad credit don’t just need capital. They need a cleaner process.

That usually means avoiding a pile of separate applications, limiting unnecessary damage to credit, and getting a way to compare offers without decoding lender jargon one by one. A platform built around pre-approval, bank-connect verification, offer tracking, and direct access to underwriters solves a practical problem. It reduces guesswork.

That’s especially useful for established companies that don’t fit neatly into one box. A mid-sized business may need equipment financing, a working capital line, SBA processing support, or invoice financing depending on the situation. Running that search manually takes time and often leads to mismatched products.

Business Loan Warrior simplifies the search by combining a single no-fee application with soft-pull pre-approval, secure account connections, a dashboard for tracking options, and human guidance when the file needs context instead of automation alone.

If you need a business loan with bad credit, Business Loan Warrior can help you check options without the usual chaos. You can start with one no-fee application, review potential matches, connect your accounts securely, and compare funding paths that fit your revenue, timeline, and credit profile.

Generated with Outrank