You've probably been here before. The business is healthy, the opportunity is real, and the capital ask is finally large enough that the old approach starts to feel reckless. Maybe you're buying out a competitor, opening a second facility, adding production capacity, or taking on a contract that will strain working capital before it pays out. The lender says yes, but there's a catch. They want you on the hook personally.

At an earlier stage, that made sense. You used your own credit and your own name to get the company moving. Most owners do. But at some point, signing another unlimited personal guarantee stops feeling like confidence and starts feeling like a mismatch. The company is operating. It has customers, revenue, systems, and assets. You want the business to stand on its own.

That's where a business loan without personal guarantee enters the conversation. Not as a trick. Not as a workaround. As a financing structure lenders reserve for businesses that can prove repayment at the company level.

Table of Contents

- Unlocking Growth Without Personal Risk

- How Lenders Think About No-Guarantee Loans

- Common Types of No-Personal-Guarantee Business Loans

- Qualifying for a Loan Without a Guarantee

- Practical Alternatives and Negotiation Tactics

- Navigating the Application Process and Risks

- Frequently Asked Questions

Unlocking Growth Without Personal Risk

You have a profitable company, a cleaner balance sheet than you had two years ago, and a real need for growth capital. Then the term sheet arrives and puts your home, savings, or both back into the credit decision. That is usually the moment owners start asking for a business loan without personal guarantee.

The request is reasonable. If the business has steady deposits, reliable customers, and books that hold up under review, the credit should stand on the company's merits. From an underwriting perspective, that is the threshold. The lender has to believe the business is a borrower in its own right, not just an extension of the owner.

Practical rule: If you want a lender to underwrite the business instead of the owner, the business has to look and behave like a separate creditworthy borrower in every visible way.

Personal guarantees are still standard across much of small-business lending. The SBA also requires a personal guarantee from every owner with 20% or more ownership in many SBA loan structures, as noted in the SBA's general SBA loan requirements guidance at https://www.sba.gov/funding-programs/loans. That matters because it frames the market correctly. A true no-guarantee deal is usually a narrower credit box, not a default option.

What this means for a growth-stage company

Owners often start by asking which lenders offer no-PG loans. A stronger question is what would make a lender comfortable waiving the guarantee in the first place. That shift improves the conversation because the decision usually comes down to risk substitution. If the lender gives up your personal backstop, something else in the file has to carry more weight.

At the front end, lenders usually want clear proof that the company operates like a real borrowing entity with stable cash movement and clean documentation. In practical terms, that often means:

- Recent bank activity: enough statements to show consistent deposits and expense patterns

- Core entity documents: formation records, ownership details, and business licenses where applicable

- Revenue support: current sales evidence that matches bank activity

- Account verification: in some cases, direct connection to the business bank account during review

I see the strongest no-guarantee files come from owners who have already separated themselves from the business operationally and financially. Business expenses run through business accounts. Financial statements reconcile to deposits. Tax returns, bookkeeping, and ownership records tell the same story.

That is what reduces friction in underwriting.

A no-personal-guarantee loan does not remove risk. It reallocates risk to the business, its cash flow, its assets, and its records. For the right company, that is exactly the point. It protects personal assets and signals that the business has reached a higher standard of creditworthiness.

How Lenders Think About No-Guarantee Loans

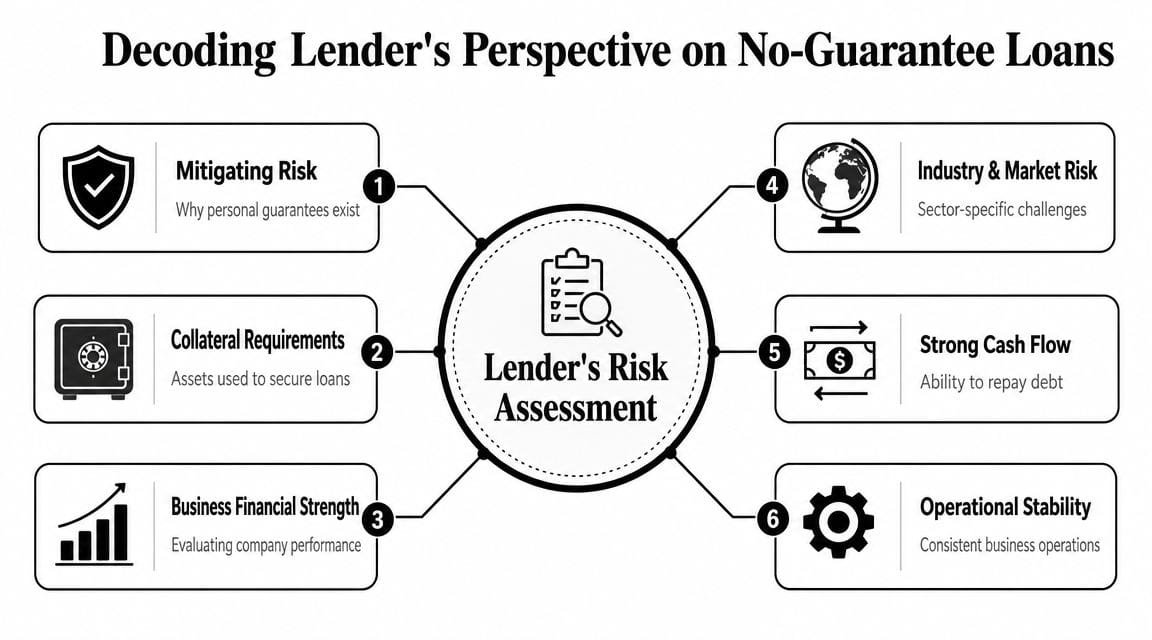

A lender asks for a personal guarantee because it lowers loss severity if the business fails. Remove that guarantee, and the lender has to replace it with something else. That's the whole game.

The cleanest analogy is a landlord. If a tenant doesn't have a strong file, the landlord may ask for a cosigner. If the tenant has a stronger file, the landlord may rely on a larger deposit, a stronger income record, or a better lease structure instead. Commercial underwriting works the same way. The lender isn't being generous when it waives a guarantee. It's finding enough security somewhere else.

The lender is replacing one form of security with another

When no personal guarantee is available, the file usually wins on one or more of these grounds:

- Cash flow strength: the business shows enough recurring income to support repayment

- Business credit quality: the company has built a reliable payment record in its own name

- Operating history: the business has been around long enough to prove stability

- Entity separation: books, accounts, and obligations are clearly business-level, not mixed with the owner's personal finances

- Asset support: equipment, receivables, or other business assets can give the lender a fallback

Industry guidance notes that in no-personal-guarantee lending, underwriting shifts toward business-level repayment capacity, especially cash flow, business credit, operating history, and entity separation. It also notes lenders commonly require at least 2 years of operating history, a strong business credit profile, and consistent revenue before waiving a PG, according to Nav's guide to business loans without a personal guarantee.

What underwriters actually want to verify

An underwriter reviews a no-PG request with a simple internal question: if this company hits a rough quarter, what still gets me paid?

That answer can come from different places. For one borrower, it's contractual receivables from good commercial customers. For another, it's equipment with resale value. For another, it's deposit history that shows the business produces cash reliably enough to service debt without owner support.

The strongest no-PG files don't ask a lender to trust the story. They let the lender verify the repayment source from records the business already keeps.

This is why owners get frustrated when they apply based on revenue alone. Revenue matters, but lenders care about quality and predictability. Volatile deposits, messy books, customer concentration, and commingled accounts can ruin a file that looks strong on the surface.

If you understand this risk substitution model, the market makes a lot more sense. A business loan without personal guarantee is not “easier if you ask the right lender.” It's available when the lender can clearly identify what replaces your signature.

Common Types of No-Personal-Guarantee Business Loans

Different no-PG products exist because different businesses generate security in different ways. Some have hard assets. Some have receivables. Some have card sales or recurring deposits. The loan structure follows the repayment source.

That's why broad advice on this topic is often unhelpful. A manufacturer, staffing firm, medical practice, and restaurant may all want a business loan without personal guarantee, but the right structure won't be the same.

What each structure is really secured by

Asset-based lending works when the company has financeable business assets. That might be inventory, equipment, or receivables, depending on the lender and the borrowing base they're willing to recognize. The lender is relying less on the owner and more on what the business owns or can convert to cash.

Invoice financing is one of the cleaner no-PG paths for B2B companies. The receivable itself drives repayment. Industry guidance notes that invoice financing commonly advances 70% to 90% of invoice value, because the lender is underwriting the receivable and the payer, not the owner's personal balance sheet, according to Noble Business Loans' overview of no-PG business loans.

Equipment financing often allows more flexibility on guarantees because the equipment secures the transaction. If the asset has durable value and the business has an operating track record, a lender may be more willing to reduce or waive personal support.

Merchant cash advances or revenue-based structures look at future sales rather than traditional collateral. This can work for businesses with strong card volume or dependable deposits. The trade-off is usually cost and repayment frequency. A product can be easier to access than a bank loan and still be a poor fit if the cash sweep pressures your working capital.

For owners comparing structures, it helps to understand the difference between secured and unsecured debt at a basic level. This guide on secured vs. unsecured business loans gives a useful frame for that decision.

Comparison of No-Personal-Guarantee Financing Options

| Financing Type | Security Basis (What Replaces the PG) | Typical Use Case | Ideal Borrower Profile |

|---|---|---|---|

| Asset-based lending | Business assets such as inventory, receivables, or equipment | Working capital, seasonal needs, acquisition support | Established business with financeable assets and organized reporting |

| Invoice financing | Outstanding receivables | Bridging payroll, vendor payments, and growth tied to invoicing cycles | B2B company with reliable commercial customers and clean AR aging |

| Equipment financing | The equipment being purchased | Machinery, vehicles, production tools, technology | Company buying useful equipment with resale value and clear business need |

| Merchant cash advance or revenue-based financing | Future card sales or business deposits | Urgent working capital, inventory buys, short-cycle opportunities | Business with strong sales flow that can tolerate frequent repayments |

A few realities matter here.

Traditional lines of credit and term loans are generally the hardest products to get without a personal guarantee. The more realistic no-PG paths tend to be tied to collateralized or specialized underwriting structures. Also, no collateral and no personal guarantee are not the same thing. A lender may waive one and still require the other through business assets, account control, or lien rights.

If your business doesn't have stable receivables, usable equipment, or reliable deposit flow, the no-PG conversation usually gets much harder.

Owners often chase the label instead of the fit. That's a mistake. The best product is the one whose repayment logic matches the way your company produces cash.

Qualifying for a Loan Without a Guarantee

A business owner walks in with solid sales, a decent margin, and a clean personal credit profile, then asks for a no-PG loan. The first question in credit is not whether the owner is trustworthy. It is whether the company can carry the debt on its own if the owner steps back tomorrow. That is the standard.

That is why this part of the process feels stricter than many owners expect. Without a personal guarantee, the lender loses a fallback source of repayment and loses pressure on the owner to keep the loan current at all costs. To approve anyway, the file has to show a business that is separate, stable, and easy to verify.

The file has to work without your personal backstop

Underwriters usually look for a company that already behaves like a stand-alone borrower.

That means:

- Meaningful operating history: enough time in business to show repeatable performance, not a short good stretch

- Reliable cash flow: revenue that supports debt service across ordinary ups and downs

- Business credit in the entity name: vendor history, trade lines, and payment habits that do not depend entirely on the owner

- Financial statements that reconcile: profit and loss, balance sheet, bank statements, and tax returns that line up

- Clear entity separation: no routine mixing of personal spending with company operations

The separation issue matters more than many applicants realize. If the owner regularly plugs cash shortfalls with informal transfers, pays personal expenses from the operating account, or moves money between related entities without documentation, the lender sees hidden dependence on the owner. In plain terms, the business is not yet standing on its own.

For companies considering funding without pledged assets, this guide to unsecured business loans and how lenders evaluate repayment risk gives useful context on what a lender needs to see when collateral is limited.

A short explainer can help frame what lenders are screening for in practice.

What to tighten before you apply

The strongest no-PG files are usually the least dramatic. Clean records, predictable account behavior, and a clear repayment story do more for approval odds than a polished pitch deck.

Focus on the points that reduce uncertainty for credit:

- Reconcile the books. If tax returns, internal financials, and bank activity point in different directions, the lender will question the whole file.

- Clean up owner-account activity. Move personal expenses, irregular draws, and undocumented transfers out of the operating pattern where possible.

- Document the legal structure clearly. Ownership, affiliates, and related entities should be easy to follow without extra explanation.

- Make the repayment source obvious. Show whether the loan will be supported by receivables, recurring contracts, equipment productivity, or steady deposits.

- Match the request to the business model. A company with predictable invoicing may fit one structure. A company with volatile deposits may fit another. Asking for the wrong product can create a decline even when the business itself is financeable.

I have seen good businesses get turned down for no-PG requests because the company was weak, and I have seen equally good businesses get turned down because the file was messy. Underwriting cannot give credit for strength it cannot verify.

You do not need a perfect company. You need a company that shows the lender one clear answer to the core question: if there is no personal guarantee, what makes this business dependable enough on its own?

Practical Alternatives and Negotiation Tactics

You ask for a no-personal-guarantee facility, and the lender comes back with a term sheet that includes one anyway. That response usually means the lender likes the business but still sees one gap in the risk structure. The question is not whether the deal is possible. The question is what protection the lender still needs before it will rely on business cash flow alone.

That distinction matters. A guarantee is only one tool in the credit file. If you want it reduced or removed, the practical move is to replace that support with something the lender can underwrite with confidence.

If the answer is not yet, structure the next best deal

Owners often treat the guarantee as a yes-or-no issue. Underwriting rarely sees it that way. Risk can be resized, time-limited, or shifted to a different part of the deal.

Useful alternatives include:

- A limited personal guarantee: your liability is capped at a stated amount or percentage

- A burn-off provision: the guarantee expires after a defined period of clean payment history and covenant compliance

- Specific collateral instead of a blanket lien: the lender takes a position in receivables, equipment, or another identified asset pool rather than all business assets

- A smaller first facility: the lender starts at a lower exposure and reviews for an increase after performance is established

- A stronger liquidity requirement: cash-on-hand or minimum balance covenants can sometimes reduce the need for full personal support

Each option changes the lender's recovery path. Each also changes your downside if the business hits a rough patch. A capped guarantee may be acceptable where an unlimited one is not. A narrower lien may preserve flexibility with future lenders, but it can also limit who will approve the deal now.

Ask underwriting questions, not emotional ones

The strongest negotiation usually starts with one direct question: what specific weakness is the guarantee covering?

If the answer is customer concentration, address concentration. If the answer is thin liquidity, show how cash will be maintained. If the answer is short operating history, ask what performance period would support reconsideration. That is how real progress gets made.

Useful questions include:

- What condition would allow the guarantee to step down from unlimited to limited?

- After how many on-time payments will the file be reviewed for release?

- Would a lower loan amount remove the need for full recourse?

- Would a borrowing base, reserve, or deposit relationship change the structure?

- Is the concern collateral coverage, cash flow volatility, or something else?

Those questions force clarity. They also tell you whether the lender is open to structure or reading from policy.

Match your concession to the lender's actual risk

A good negotiation is an exchange, not a speech. If you ask the lender to give up a guarantee, expect to offer something in return.

That might mean tighter reporting, monthly borrowing base certificates, a lower advance rate, more cash retained in the business, or a shorter amortization period. None of those terms are free. They can improve approval odds while adding operational pressure after closing. Owners should weigh the legal risk of a guarantee against the cash management burden of stricter loan terms.

I have seen borrowers win meaningful changes by offering the right substitute. I have also seen borrowers push so hard on the guarantee that they missed a workable deal with limited recourse and reasonable release terms.

Compare structures before you decide

If a bank will not move, the next step is not to accept bad terms out of frustration. It is to compare how other lenders price the same risk. Different capital providers make different bets. Some care more about deposits. Others care more about receivables, equipment, or recent revenue performance. A practical review of alternative unsecured business finance options for small businesses can help you see which structures rely less on owner support and more on business performance.

The goal is not to win an argument over principle. The goal is to keep personal exposure proportionate to the actual risk in the deal. Strong borrowers do that by giving lenders another credible way to get comfortable.

Navigating the Application Process and Risks

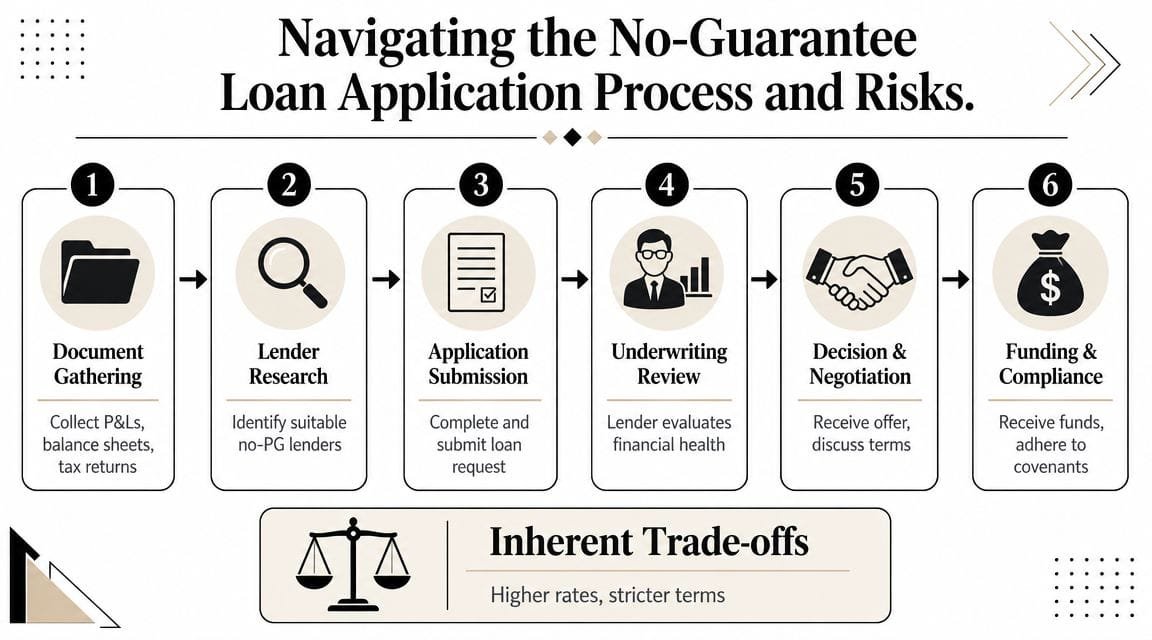

Most no-PG applications fail before the credit decision because the file arrives incomplete, inconsistent, or pointed at the wrong lender. The process is not complicated, but it is unforgiving.

A practical way to approach it is to assemble the same package an underwriter would ask for anyway, then choose lenders based on the actual source of repayment in your file.

How to move through underwriting cleanly

The workflow usually looks like this:

- Gather current financial records. That typically includes profit and loss statements, balance sheets, tax returns, bank statements, and formation documents.

- Match the lender to the structure. Receivable-heavy companies should talk to lenders comfortable with invoice-based facilities. Equipment-heavy companies should look at equipment lenders.

- Submit a coherent request. State the amount, use of proceeds, and primary repayment source plainly.

- Prepare for follow-up. Underwriters will ask where cash comes from, what could interrupt it, and what business assets support the deal.

- Review liens and covenants before signing. Many owners move too fast at this stage.

The risk is shifted, not erased

A critical distinction in this market is the difference between no personal guarantee and no collateral. Lenders may replace a personal guarantee with other security, such as a UCC lien against business assets, which means a no-PG loan is often not entirely unsecured and can still put business assets at risk in default, according to Fora Financial's discussion of personal guarantees.

That has real consequences:

- A UCC filing can affect future financing: another lender may require subordination or payoff before extending new credit

- Pricing may be higher: if the lender can't rely on your personal assets, it may charge for that extra risk

- Terms can be tighter: more reporting, more controls, or more restrictive default language

Read the remedies section as carefully as the rate. In stressed situations, remedies determine how much control the lender has over your business assets.

“No PG” sounds simple. It isn't. It means your personal balance sheet may be shielded, but the business itself is often more directly pledged.

Frequently Asked Questions

Can a startup get a business loan without personal guarantee

Usually not in any practical sense. No-PG lending is generally reserved for companies with operating history, business credit, and verifiable repayment strength. Startups rarely have enough of those on a standalone basis. They usually need owner support, collateral, or both.

Does a UCC lien matter if there is no personal guarantee

Yes. A UCC lien can still give the lender rights against business assets even when your personal assets are outside the deal. That can limit flexibility on future borrowing until the lien is released, subordinated, or refinanced.

Are no-PG loans always unsecured

No. That's one of the biggest misunderstandings in the market. A lender may waive the personal guarantee but still secure the deal with receivables, equipment, deposit controls, or a lien on business assets.

When does a merchant cash advance make sense

Only when the business has strong short-cycle sales, very clear margin on the use of funds, and a realistic path to absorbing frequent repayments. It can work for a fast inventory turn or a near-term revenue opportunity. It's a bad choice when the advance is just covering chronic cash flow weakness.

What's the fastest way to improve eligibility

Separate personal and business finances completely, tighten reporting, and apply for a product that matches the asset or revenue stream your company already has. Underwriters approve clarity faster than they approve ambition.

If you're weighing a business loan without personal guarantee, Business Loan Warrior lets you review funding options through one no-fee application, check pre-approval without affecting credit, connect business bank accounts, and track offers through a secure dashboard. For owners comparing unsecured loans, equipment financing, invoice financing, lines of credit, or short-term working capital, that kind of side-by-side view can make it easier to see which structure fits the risk profile of the business.