You're probably in one of two spots right now. Either the plans are approved and your contractor wants to mobilize, or the bank has issued a term sheet and you've realized the critical risk isn't just rate or amortization. It's timing. More specifically, it's whether cash will arrive when payroll, subs, and suppliers need to be paid.

That's why the construction loan draw schedule matters so much on a commercial project. If you treat it like boilerplate, it can become the reason a good project stalls. If you manage it like a financial control document, it helps you protect liquidity, reduce conflict with your GC, and keep your lender confident all the way to completion.

Table of Contents

- Why Your Draw Schedule Is Your Project's Financial Blueprint

- The Anatomy of a Commercial Draw Schedule

- How to Build and Negotiate Your Draw Schedule

- Navigating the Draw Request and Inspection Process

- Common Draw Schedule Pitfalls in Commercial Projects

- Advanced Strategies for Financial Control and Reporting

Why Your Draw Schedule Is Your Project's Financial Blueprint

Most first-time commercial borrowers assume the loan closes, the funds hit an account, and construction spending starts. That isn't how it works. On a construction facility, the lender usually controls disbursements and releases money in stages after work is verified.

In residential projects, draw schedules are commonly structured around 4 to 7 draws tied to verifiable milestones such as foundation, framing, rough-ins, finishes, and final inspection, according to Get Built's explanation of multi-project construction draw schedules. Commercial deals often become more customized, but the core logic is the same. The lender funds progress, not promises.

That's why I tell business owners to think of the draw schedule as the project's financial blueprint. Your plans tell the contractor what to build. Your draw schedule tells the capital stack when money moves.

What the draw schedule actually controls

A good schedule does more than map payments. It governs daily operating pressure on the job.

- Cash flow timing: It determines whether your contractor gets paid in rhythm with actual work, or whether someone is floating labor and materials.

- Lender confidence: It gives the bank a framework for monitoring risk without interfering with the field.

- Project discipline: It forces the borrower, GC, and lender to agree on what “complete” means before money is released.

- Dispute prevention: It reduces the chances that one party says a phase is done while another says it isn't.

Practical rule: If a draw trigger isn't measurable before the job starts, it will become an argument later.

A poorly structured draw schedule creates a chain reaction. The contractor submits a request that doesn't match the lender's categories. The inspector can't confirm completion cleanly. The lender asks for revisions. Funding slips. Subs wait. The borrower starts using working capital to bridge the gap. That's when a manageable project starts feeling expensive.

A well-structured schedule gives you control over those pressure points. It also helps you ask better questions before you sign the loan documents. If you're still evaluating how the capital stack should fit the project, review a broader look at construction project financing options before you lock in the draw mechanics.

Why owners get surprised

The surprise usually isn't that draws exist. The surprise is how operational they are. Every request becomes a mini underwriting event. Documents must line up, site progress must be visible, and the lender has to believe the remaining budget still gets the project to the finish line.

That's why the draw schedule deserves executive attention. Not because it's complicated on paper, but because it decides whether your project stays liquid between groundbreaking and opening day.

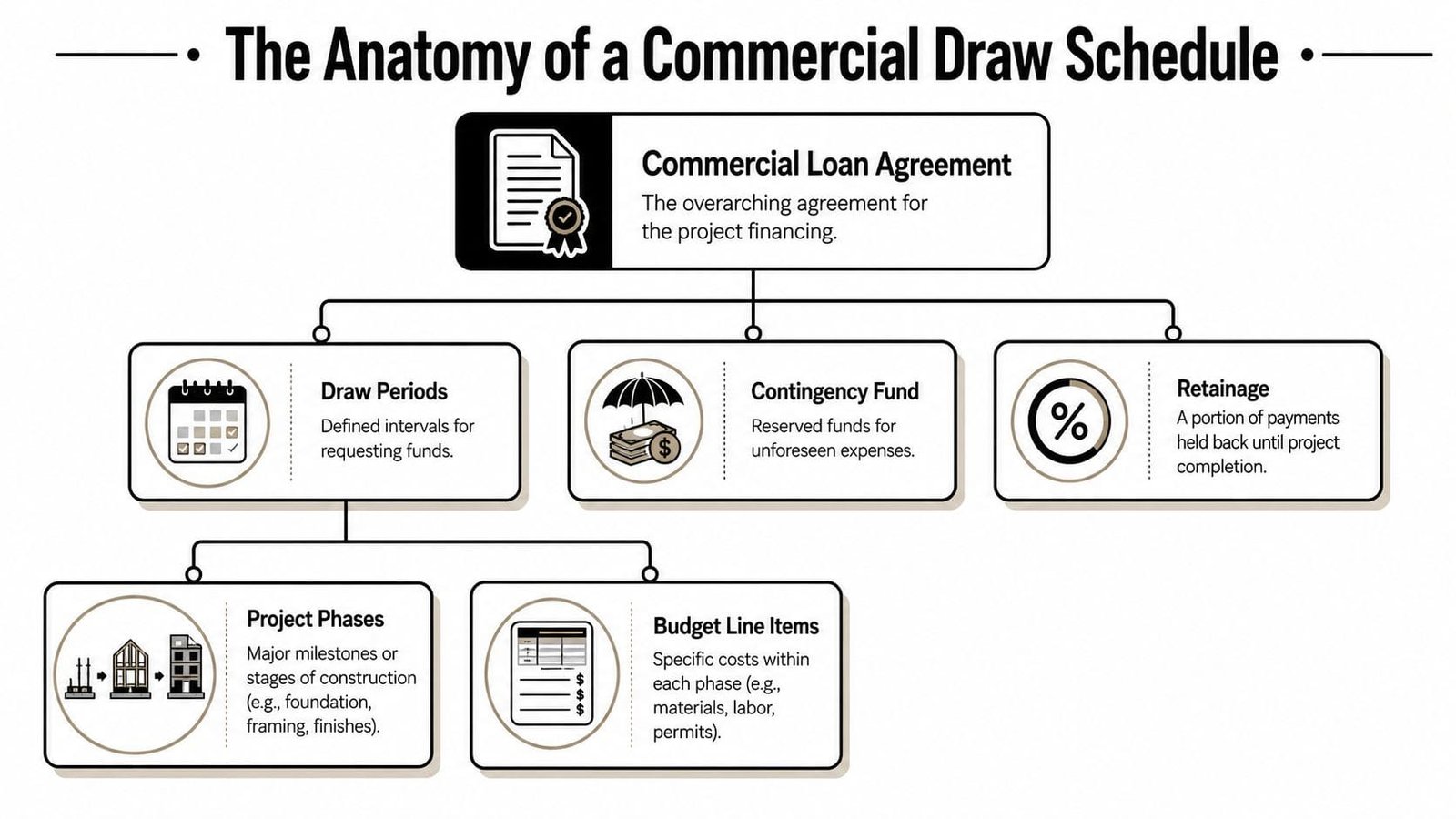

The Anatomy of a Commercial Draw Schedule

A commercial draw schedule usually looks orderly at closing. Then the project starts, long-lead materials shift, inspectors want backup, and the timing of cash out becomes just as important as the total budget. Owners who treat the schedule as a simple payment calendar usually feel that pressure by the second or third draw.

Start with the Schedule of Values

The Schedule of Values, or SOV, is the operating document behind the draw process. It breaks the contract amount into cost codes the lender can approve, the inspector can verify, and your team can reconcile against invoices and lien releases.

Get this wrong and the project starts carrying avoidable friction.

If the GC loads too much value into broad categories like “general conditions,” “MEP,” or “buildout,” the lender has trouble tying dollars to visible progress. If the SOV is too granular, every draw package turns into a bookkeeping exercise that burns time on both sides. The right version tracks how the job will buy materials, install work, and bill subcontractors.

For business owners, that matters because the SOV affects borrowing cost in practical terms, not just administrative terms. Delayed reimbursements increase the amount of cash you have floating in the job, and higher carry costs can make the all-in economics look different than the note rate suggested at closing. It helps to review how construction loan rates affect total project cost before you finalize the draw structure.

Two common draw structures

Commercial projects usually use one of two frameworks.

Milestone-based draws release funds after a defined phase is finished and documented. This approach is common on smaller projects, simpler site builds, and jobs where progress is easy to see. Typical milestones include sitework complete, foundation complete, dry-in, rough-ins, and substantial completion.

Percentage-of-completion draws release funds across SOV line items based on verified progress. This structure fits larger projects, tenant improvements with overlapping trades, and jobs where procurement and installation happen on different timelines.

Neither structure is automatically better. The right choice depends on how your project spends cash.

A milestone schedule is easier to administer, but it can create strain when expensive materials hit before the milestone is technically complete. A percentage-of-completion schedule tracks reality better on complex jobs, but it demands cleaner reporting and more discipline from the GC. Owners with long-lead equipment, custom fabrication, or imported materials often need some hybrid treatment so procurement does not sit outside the draw system.

What the line items usually include

Most commercial draw schedules are built around a predictable set of buckets, even if the wording changes by lender:

| Draw Phase | Description of Work Completed | Typical Funding Logic |

|---|---|---|

| Site work and foundation | Excavation, underground utilities, footings, slab, early civil work | Released against inspected progress and approved invoices |

| Structural shell | Steel, framing, roof, exterior sheathing, dry-in work | Released as structural completion can be verified |

| Rough-ins | Plumbing, electrical, HVAC rough-ins, fire protection, related inspections | Released by line-item completion or trade progress |

| Interior buildout | Drywall, finishes, doors, millwork, flooring, specialty systems | Released as installed work and stored materials are documented |

| Final completion | Fixtures, punch list, closeout items, certificates, occupancy-related work | Released after final inspection, lien control, and retainage conditions |

That table shows the anatomy, not a universal template. A medical office, restaurant, warehouse expansion, and owner-occupied retail build will all weight those categories differently. Restaurant projects, for example, often need more attention on kitchen equipment, ventilation, utility upgrades, and health-department signoff than a standard office build.

The part many owners miss

The visible phases are only half the structure. The other half sits in the loan documents and disbursement procedures.

Pay close attention to these items:

- Stored materials treatment. Some lenders fund materials delivered but not installed. Others discount them or require separate documentation, insurance proof, and site verification.

- Retainage. The lender may hold back a portion even if your construction contract uses different terms. If those two systems do not match, someone has to carry the gap.

- Contingency access. A contingency line in the budget does not mean the money is freely available. Many lenders require change-order approval before releasing any part of it.

- Interest reserve interaction. If draws slip, the project can pressure both operating cash and the interest reserve at the same time.

- Disbursement routing. Funds may go to the borrower, the GC, or joint payees. That affects how fast subcontractors get paid.

In commercial projects, these details decide whether the draw schedule supports operations or creates cash squeezes. Owners who understand them early usually keep better control of vendor relationships, avoid last-minute equity injections, and have a stronger footing when the lender asks hard questions mid-project.

How to Build and Negotiate Your Draw Schedule

You close on the loan, mobilization starts, and then the first cash squeeze shows up before the project feels fully underway. The GC wants deposits for equipment and early trade commitments. The lender wants completed work it can verify. If the draw schedule was built too loosely, your operating cash becomes the bridge.

That problem is avoidable.

Build the schedule from the cash curve, then tie it back to the job

Owners often start with the lender's template or the contractor's billing preferences. A better approach is to start with the project's spending pattern. Then line that up with the construction sequence and the lender's inspection rules.

On a commercial or small business project, the pressure points usually arrive early. Deposits for mechanical equipment, utility work, specialty fabrication, tenant improvements, and permit-related requirements can hit before visible progress catches up. If your draw schedule only funds installed work, someone has to carry that gap for weeks. Sometimes it is the GC. More often, it is the borrower.

Use a practical build sequence:

- Stabilize the scope. Plans, specs, allowances, and owner-supplied items need to be far enough along that the budget is usable.

- Break down the schedule of values. Review each trade and procurement category line by line so front-loaded costs are visible.

- Flag early cash-demand items. Long-lead equipment, utility deposits, fabricated components, and permit-driven work need special attention.

- Tie each line item to inspection evidence. The lender needs a clear way to confirm progress without arguing over interpretation.

- Model timing, not just totals. A balanced project budget can still fail if the first third of the job consumes cash faster than draws are released.

- Test the downside case. Ask what happens if a delivery slips, an inspection gets pushed, or a change order stalls for two weeks.

That last step matters more than many first-time borrowers expect. A draw schedule should work under normal conditions and under mild stress. If it only works when every subcontractor, supplier, and inspector stays on schedule, it is too fragile.

What to negotiate before closing

The best time to negotiate draw terms is before documents are final and before the project team is under payment pressure. After closing, lenders usually become less flexible because the file has moved from underwriting to administration.

Focus on terms that affect liquidity, not just the note rate.

Here are the pressure points worth negotiating:

- Advance treatment for long-lead materials: Get a clear answer on deposits, stored materials, off-site fabrication, and owner-purchased equipment.

- Draw frequency: Monthly is common, but some projects need a faster cycle during heavy procurement or early trade mobilization.

- Phase definitions: Terms like substantial completion, dry-in, or MEP rough-in should match how your contractor and the lender's inspector will measure progress.

- Minimum draw size and cutoff dates: Administrative rules can create avoidable delays if your team misses a submission window by a day.

- Retainage mechanics: Confirm whether retainage applies uniformly or differently by trade, and how it is released near completion.

- Contingency access: Spell out what documentation triggers approval and who can authorize use of those funds.

- Direct payment options: For large equipment packages or problem trades, ask whether the lender will fund by joint check or direct-to-vendor disbursement.

I usually tell borrowers to negotiate the draw structure with the same seriousness they bring to rate discussions. A lower coupon does not help much if the project repeatedly needs short-term cash support between draws. If you are comparing loan structures, review current construction loan rates and pricing trade-offs together with the disbursement language so you can see the full cost of each option.

One more point. Do not accept vague language where the project has known complexity. If the job depends on imported equipment, utility coordination, or health and safety signoffs, get that reality reflected in the draw terms while the lender is still listening.

Documents to organize early

Good negotiations are easier when your file is clean. Lenders give better answers when they can see the contract structure, the budget detail, and the payment logic without guessing.

Organize these items before closing:

- Executed construction contract: The final version, including exhibits and general conditions.

- Detailed project budget and schedule of values: These should reconcile cleanly and show where procurement pressure sits.

- Project schedule: Even a simple construction timeline helps the lender understand when spending will hit.

- Plans, specifications, and major equipment lists: These support inspection decisions and stored-material requests.

- Permit log and approval tracker: Delayed approvals often become delayed draws.

- Internal draw checklist: Assign responsibility for collecting invoices, lien waivers, photos, and updated budget reporting.

- Change order workflow: Set rules for pricing, approval, lender notice, and budget reallocation before the first dispute lands on your desk.

A borrower who can produce these documents quickly usually has more credibility when asking for exceptions or faster handling later.

What works and what fails

A good draw schedule reflects three things at once: how the job will spend money, how the lender will verify progress, and how much float your business can carry without strain.

What fails is a generic phase schedule copied from a residential template and dropped onto a commercial project with equipment deposits, specialized trades, or uneven procurement timing. That is where cash flow problems start. The project may still finish, but the owner absorbs more friction, more pay-application disputes, and more pressure on working capital than necessary.

If the first draft does not fit the job, push back before closing. Clear comments, marked-up draw language, and a revised schedule of values solve far more problems at this stage than urgent phone calls do later.

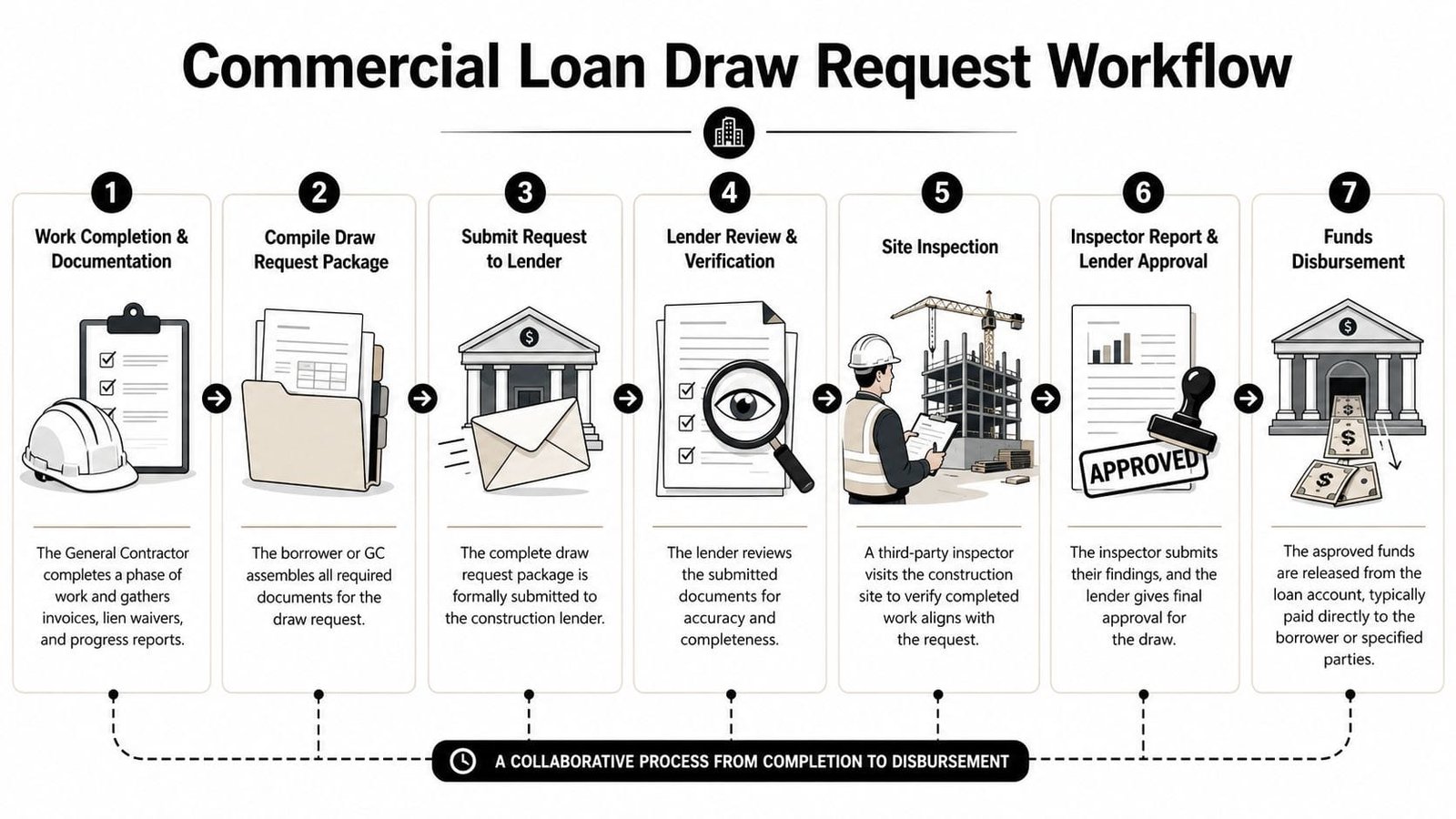

Navigating the Draw Request and Inspection Process

Friday afternoon, your contractor submits a pay application, subs want checks next week, and your bank says the draw package is missing backup. The job may be on schedule, but cash can still tighten fast if the request package, inspection timing, and lender review are not lined up. That pressure shows up more often on commercial and small business projects than owners expect, especially when payroll, rent, and regular operating expenses are competing with the build for liquidity.

What goes into a clean draw packet

A draw packet should answer three questions clearly. What work is complete, what amount is being requested, and how does that request tie back to the approved budget and current project status?

On a commercial file, I want the package to read like an audit trail, not a stack of attachments. If the lender has to guess how an invoice connects to a line item, or whether a change order is approved, the request usually stalls.

A clean packet usually includes:

- Current draw request form: Completed in the lender's exact format.

- Updated SOV or budget-to-actual report: Show prior disbursements, current request, retainage if applicable, and remaining balance.

- Invoices or contractor pay applications: Match them to the relevant budget lines.

- Progress photos: Organize them by area or trade, with dates that support the claimed progress.

- Lien waivers: Include conditional or unconditional forms based on the lender and title company requirements.

- Approved change orders: Show the cost impact and where the money is coming from.

- Stored materials support, if allowed: Include invoices, proof of payment, delivery status, storage location, and insurance if the lender funds materials before installation.

A lender can work with bad news. A lender hates unclear files.

That distinction matters. If steel is late, a tenant revision changed the electrical scope, or a municipal sign-off pushed work into next month, say so directly in the package. A lender can process a project with complications. It has a harder time processing one that looks disorganized or evasive.

How the inspection cycle works in practice

The formal sequence is simple. Submit the request, clear the lender's file review, get the inspection completed, resolve any exceptions, then wait for funding.

The lived experience is less tidy. Inspectors verify visible progress, but lenders are also checking budget discipline, prior overruns, permit status, title conditions, and whether the current request fits the approved loan structure. On a business-owner project, that review often matters as much as the site walk itself because the bank is watching both construction progress and the borrower's ability to carry the job without creating a working-capital problem.

For a first major build, assume every draw needs one correction. That assumption improves planning. It gives your team time to fix a missing waiver, reconcile a category mismatch, or answer an inspector question before vendors start calling about late payment.

A short explainer can help if you want to see how the process is commonly described from a lender workflow perspective.

What slows funding down

Draw delays usually come from routine friction. The package does not match the budget. The site is not ready to inspect. A deposit was paid for material the lender will not fund yet. A signed change order exists in the field, but not in the credit file.

| Common issue | What it does to your draw |

|---|---|

| Missing backup | The lender asks for clarification or a revised submission |

| Site not inspection-ready | The inspector cannot verify enough completed work to support the request |

| SOV mismatch | The request does not reconcile to approved budget categories |

| Unapproved change order | The lender treats it as a control problem and may hold part of the draw |

| Last-minute submission | You lose the buffer needed for review, inspection, title updates, and funding |

The cash-flow effect is what owners feel first. If your contractor expects reimbursement in a few days but the bank needs revisions, you either float the gap from operating cash, slow vendor payments, or create tension with the GC. None of those options is cheap.

The better approach is a fixed monthly draw cadence with internal cutoff dates. Have the contractor close billing early enough for your team to review the file before it reaches the bank. Confirm the site is clean, labeled, and accessible before the inspection is scheduled. Call out exceptions in advance instead of waiting for the lender to find them. Owners who do that usually get faster answers, and they have a much stronger case when they need an accommodation for stored materials, off-cycle disbursements, or a revised inspection sequence.

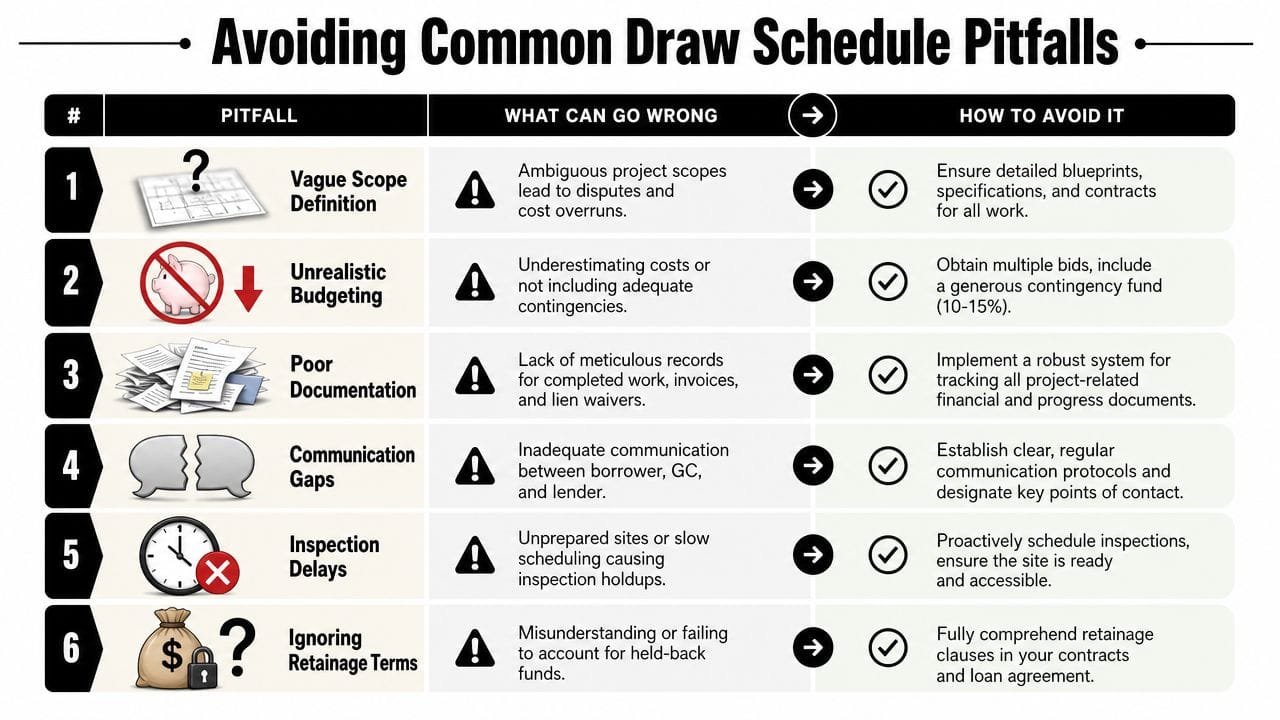

Common Draw Schedule Pitfalls in Commercial Projects

Commercial projects rarely fail because nobody knew what a draw was. They get into trouble because the sequence of spending, inspection, and reimbursement stops matching reality. When that happens, even profitable businesses can feel squeezed.

When long lead materials break the sequence

A common scenario is custom equipment or materials that must be ordered and paid for well before installation. Think rooftop units, specialty glazing, trusses, elevators, or kitchen equipment.

Ledger's discussion of construction loan draws highlights a major challenge here. Supply-chain delays and long-lead materials can push costs out of sequence, while lenders typically want draws tied to verified completion. That mismatch can create a cash-flow squeeze when money is needed well before the related milestone is inspectable, as explained in Ledger's article on construction loan draw issues.

The fix is not to hope the lender will make an exception later. The fix is to address stored materials, deposit documentation, and re-sequencing options before the project reaches procurement pressure.

What works in practice:

- Pre-negotiate treatment of off-site materials: Ask what evidence the lender needs.

- Use clear vendor documentation: Deposits, delivery schedules, and purchase confirmations need to be easy to review.

- Flag long-lead items early: Don't wait until the GC is asking for urgent funds.

When change orders distort the budget

Another frequent problem is that the field changes faster than the paperwork. A change order gets approved between the owner and GC, but the lender's version of the budget still reflects the old number and old category.

Then the next draw arrives. The contractor requests funds based on current reality. The lender reviews against outdated documents. That turns a normal funding cycle into a dispute over whether the request is even eligible.

The practical answer is simple, even if the discipline isn't. No change order should hit the job financially until it also has a path into the draw process. That means updating the SOV, budget, and internal draw tracker before the next submission.

If your construction team and finance team are looking at different versions of the budget, the draw request is already in trouble.

When retainage and payment timing squeeze cash

The third trap is a timing mismatch. Your lender may release funds only after inspection and approval. Your contractor may expect payment on a faster cycle. Add retainage, and the gap can widen.

That doesn't mean anybody is acting unreasonably. It means the cash conversion cycle of the project has not been fully planned.

Here's how that usually plays out:

- The contractor completes work and bills promptly.

- The borrower submits the draw after that point instead of ahead of it.

- The inspection takes time.

- Approval takes more time if documents need correction.

- Payment lands later than the contractor expected.

The solution is to align the contractor's billing expectations with the lender's actual draw process from day one. If those clocks run differently, someone has to bridge the gap. Decide who that is before the first invoice comes due.

Inspection failure is usually a documentation failure

Borrowers often say a draw “failed inspection” as if it were only a site problem. Sometimes it is. More often, the issue is that the package claimed more completion than the field or documentation could support.

You avoid that by being conservative on percentage claims, keeping photos organized, and making sure the GC's billing staff and field staff are speaking the same language. A clean, slightly understated draw tends to fund faster than an aggressive one that triggers questions.

Advanced Strategies for Financial Control and Reporting

Strategic borrowers stop treating draws as an administrative hurdle and start using them as a treasury tool. That shift changes the quality of decisions across the entire project.

Use draw cadence as a treasury tool

In larger commercial work, the draw structure can become much more frequent than the standard small-project pattern. River Editor notes that commercial projects often use 12 to 24+ monthly percentage-of-completion draws, while single-family projects more often use 4 to 6 milestone-based draws, in its explanation of how builder draw schedules differ across project types.

That difference matters because more frequent draws can tighten working-capital control. They can also increase administrative burden, dependence on inspection timing, and stress around lender approvals. In other words, a shorter draw cycle can help cash, but only if your team can support the reporting load.

Build reporting that satisfies both operations and credit

Your project team wants to know what's happening in the field. Your lender wants to know whether funded progress matches budgeted progress. Your finance team wants a clean view of commitments, invoices, approved change orders, and available liquidity.

Those aren't the same report.

Use a reporting stack that gives you at least these views:

- Budget versus actual by SOV line

- Funded to date versus remaining availability

- Pending change orders and approved change orders

- Expected next draw timing

- Known cash pinch points tied to procurement

If your team already uses systems like Sage Intacct or QuickBooks for accounting, tie project reporting discipline to those monthly close habits. The exact software matters less than consistency. One source of truth beats a spreadsheet on the project manager's laptop every time.

Track equity like it matters, because it does

Many lenders require borrower equity to be spent before or alongside loan proceeds. That's where first-time borrowers get caught flat-footed. They think they're preserving cash by delaying equity contributions, but the lender may see the file differently and hold back proceeds until the agreed capital is in.

That's why you need a separate equity tracker inside your draw process. Not as a side note. As a core control. If your team can't show what owner equity has funded, the lender may slow disbursements even when site progress is real.

A disciplined borrower treats the construction loan draw schedule as part of a broader control tower for project finance and reporting. If you want a sharper framework for building that kind of visibility, review this guide on how to architect a draw-to-revenue control tower and apply the same thinking to your construction pipeline.

The borrowers who manage this well tend to have fewer surprises, cleaner lender relationships, and better command of working capital throughout the life of the project.

If you're planning a build, expansion, or owner-occupied commercial project, Business Loan Warrior can help you evaluate financing options, compare structures, and prepare for the practical cash-flow demands behind the loan documents. The fastest way to protect your project isn't just getting approved. It's getting matched to funding that fits how your job will practically spend money.