You’re probably looking at a project that feels strategically obvious and financially awkward at the same time.

Maybe you need a second location, a larger service facility, a warehouse build-out, or a ground-up property that finally matches the scale of a business doing real volume. The operating case makes sense. The harder question is financing the messy middle, when you’re paying to create an asset that doesn’t exist yet.

That’s where construction loan rates matter. Not because rate shopping alone wins the deal, but because the rate tells you how a lender is pricing your project’s risk, your liquidity, your timeline, and your ability to execute. For a business in the $20 million to $50 million revenue range, that rate should be treated as an ROI input, not just a borrowing cost.

Table of Contents

- Understanding Current Construction Loan Rates in 2026

- The Key Factors Driving Your Interest Rate

- Choosing Your Loan Structure Fixed vs Variable

- Comparing Lenders for Your Construction Project

- How to Secure the Best Possible Construction Loan Rate

Understanding Current Construction Loan Rates in 2026

A construction loan is best understood as build-phase financing. It funds creation, not a finished asset. A traditional mortgage finances something complete and already valued by the market. A construction loan finances the uncertainty between blueprint and certificate of occupancy.

The simplest analogy is this. Financing a completed building is like buying a finished DVD. Financing construction is like funding the movie production itself. More moving parts. More dependencies. More chances for delay, cost drift, or execution problems. Lenders price that uncertainty into the rate.

By early 2026, fixed-rate construction loans were stabilizing in the 7.0% to 8.5% range, while adjustable-rate loans were running 6.0% to 8.0%, according to Trident Home Loans’ construction loan rate overview. That same source notes this remained a premium over the average 30-year fixed mortgage rate of 6.24%, which reflects the extra risk attached to short-term, interest-only financing during the build phase.

Why the rate sits above a standard mortgage

During construction, the lender isn’t financing a fully operating, fully stabilized property. They’re advancing money in stages while a project is still exposed to contractor performance, inspection timing, material availability, and final valuation. That’s why even strong borrowers often react to a construction quote by saying, “Why is this above conventional real estate debt?”

Because this isn’t conventional real estate debt.

Practical rule: Compare a construction loan quote to other construction loan quotes first. Comparing it to a stabilized mortgage can mislead you.

The structure also matters. Most construction loans involve interest-only payments during the build, which helps preserve cash while the property isn’t yet producing its full economic value. That eases near-term pressure, but it doesn’t remove the lender’s risk. It just changes the repayment profile.

What a competitive quote looks like

For a business owner, “good” doesn’t mean “lowest number on the page.” It means the quote matches the quality of the project and doesn’t hide risk in the fine print. A slightly higher rate with cleaner draw mechanics, realistic contingency handling, and fewer rollover headaches can outperform a lower headline rate.

I’d look at these elements together:

- Rate structure: Is it fixed for the relevant period, or can it reprice at the worst moment?

- Draw process: How easy is it to access funds as work is completed?

- Conversion plan: What happens when construction ends?

- Covenants and fees: Are there restrictions that could create friction if the timeline moves?

If you want context on how repayment structures and borrowing costs have shifted more broadly for small businesses, this review of lending trends in repayment terms and interest rates is a useful companion read.

A quote only becomes meaningful when you place it inside the full capital stack and your expected return on the project. That’s how owners avoid chasing the wrong loan.

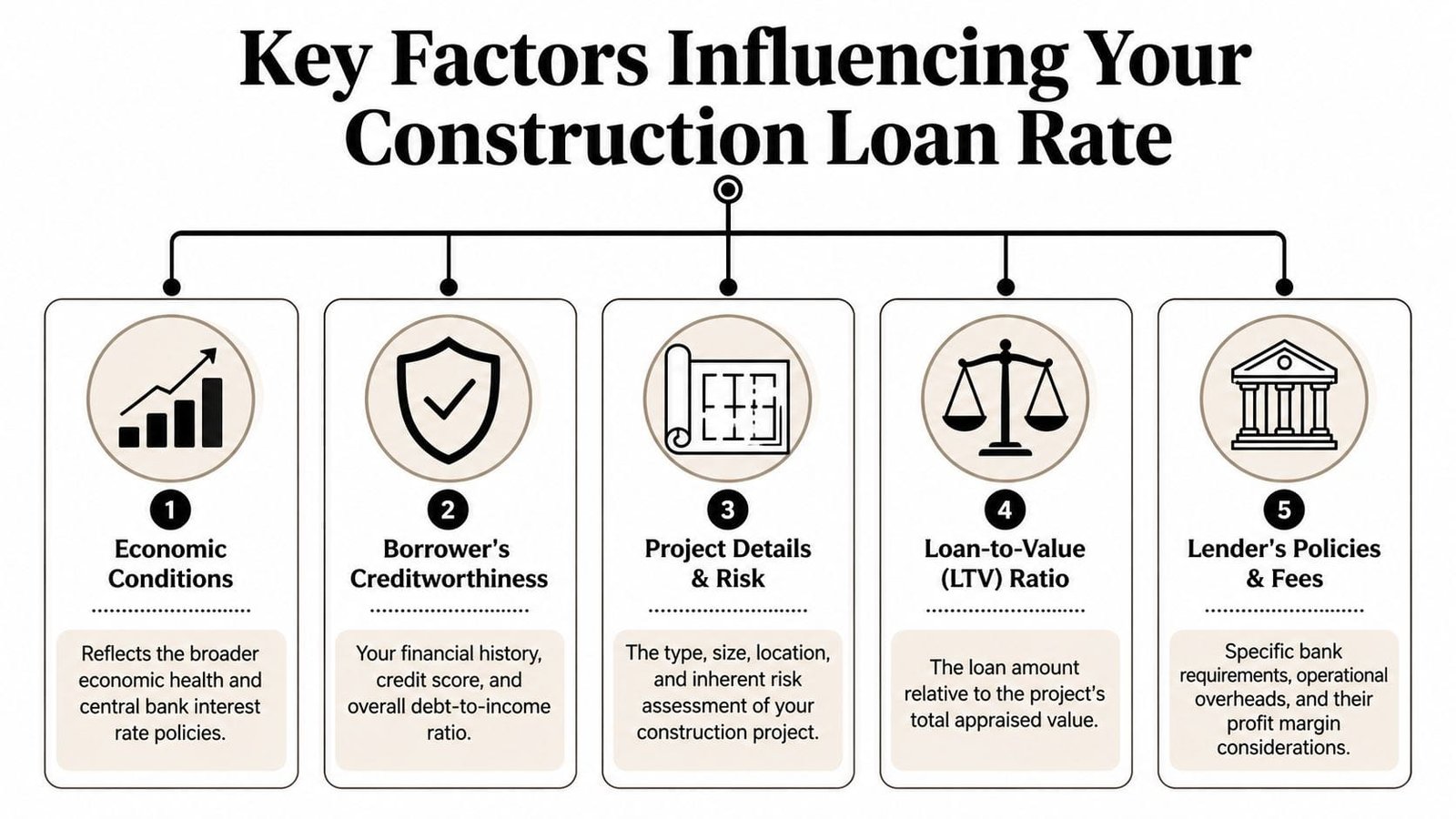

The Key Factors Driving Your Interest Rate

Most borrowers see a construction loan rate as a verdict. It’s better to treat it like a diagnostic report. The lender is telling you how they see the risk profile of the deal.

Here’s the visual version of that risk stack.

Creditworthiness sets the tone

Credit doesn’t just affect approval. It shapes pricing, flexibility, and how much benefit of the doubt a lender extends when a file gets complicated.

In construction lending, lenders look beyond the score itself. They care about repayment history, debt load, liquidity discipline, and whether your business financials tell a coherent story. A borrower with clean statements and stable cash management often gets a different conversation than one with the same project but weaker documentation.

Loan-to-value changes the lender’s exposure

Loan-to-value, or LTV, measures how much the lender is advancing relative to the project’s value. The more borrower equity in the deal, the more protection the lender has if something goes wrong.

That’s why owners sometimes focus too narrowly on rate and ignore valuation strategy. If the appraised as-complete value comes in lower than expected, the lender may tighten structure, require more equity, or price the loan more conservatively.

A weak appraisal can quietly turn a decent project into an expensive one.

This is one place where better plans, stronger contractor bids, and clearer finish specifications can help. They don’t just improve presentation. They can support the economics behind the file.

Project quality affects pricing more than many owners expect

A lender reads your project package the way a pilot reads weather. They want to know where the turbulence is likely to hit.

These project details usually move the needle:

- Scope clarity: A clean budget and detailed timeline reduce underwriting friction.

- Builder strength: An experienced general contractor lowers execution risk.

- Property type: Some projects are easier for lenders to understand and monitor than others.

- Exit logic: The lender wants a believable path from construction phase to permanent financing or stabilized operations.

A vague project memo almost always gets priced defensively. Lenders assume uncertainty where the borrower leaves blanks.

Loan term and type change the risk profile

Short-term construction debt and construction-to-permanent financing don’t behave the same way. Neither do fixed and adjustable structures. The lender is pricing not only your project but the path the loan will take from first draw to final repayment.

That’s why two quotes that look similar at first glance can produce very different outcomes for cash flow and refinancing risk.

The lender’s own model matters

Not every rate difference is about you. Some of it comes from the lender’s own cost of funds, appetite for a certain property type, internal concentration limits, and tolerance for custom underwriting.

One bank may love owner-occupied projects and price them tightly. Another may be overexposed to the category and back away by quoting less attractive terms. Specialty lenders may move faster, but they may also structure around flexibility differently than a traditional bank.

| Driver | What it affects most | What you can influence |

|---|---|---|

| Credit profile | Rate, approval confidence, flexibility | Financial cleanup and documentation |

| LTV | Pricing and required equity | Equity contribution and appraisal support |

| Project package | Underwriting comfort | Budget quality, plans, contractor selection |

| Loan structure | Payment profile and rollover risk | Fixed vs variable, one-time vs two-step |

| Lender model | Final quote style | Who you approach and how broadly you shop |

Think of the rate quote like a car engine with five major components. If one part runs poorly, the whole machine gets less efficient. Borrowers who understand that usually negotiate better because they know which lever to pull.

Choosing Your Loan Structure Fixed vs Variable

The wrong structure can cost more than a slightly higher rate.

A lot of owners spend weeks negotiating pricing and only a few minutes on the structure itself. That’s backward. The structure determines how rate risk, refinancing risk, and payment timing hit your business while the project is still vulnerable.

Fixed rate loans offer predictability

A fixed structure works best when your priority is budget certainty. If your project has tight operating assumptions, multiple dependencies, or a board-level need for clean forecasting, predictability usually matters more than squeezing out a small initial pricing advantage.

You know what debt costs are likely to be. That helps with planning occupancy, ramp-up, and post-construction cash use.

The trade-off is simple. You may not always get the lowest initial quote. You’re paying for certainty.

Variable rate loans can work when flexibility matters

Adjustable structures can make sense if you expect a short build window, have strong cash reserves, and can tolerate some rate movement without stressing the rest of the company. They can also suit borrowers who believe they’ll refinance or exit the construction phase quickly.

But variable doesn’t mean “cheaper” in a practical sense. It means the future cost is less certain. If a project slips, that uncertainty can become expensive at exactly the wrong time.

If your timeline is fragile, don’t pair it with a loan structure that adds another moving target.

Why many borrowers prefer construction-to-permanent financing

For many growing businesses, the most useful middle ground is a construction-to-permanent loan, also called a one-time close loan. It combines the build-phase financing and the long-term mortgage into one structure, rather than forcing you to refinance after construction.

That matters because refinancing risk is often underestimated. Owners plan for the build. They don’t always plan for what happens if rates are worse, underwriting gets tighter, or project timing shifts right when they need permanent debt.

According to Llama Loan’s late-2025 review of construction-to-permanent rates, these loans could lock in a 30-year fixed rate as low as 7.5% with APR 7.553%, though pricing depends heavily on credit. The same source notes that borrowers with excellent credit of 740+ can secure a rate below 6.0%, while borrowers in the 660 to 699 range may face rates closer to 6.8%.

How to choose the right structure

Use the business, not the spreadsheet alone, to make the call.

- Choose fixed if margin visibility matters, your opening date is important, or your liquidity cushion isn’t huge.

- Choose variable if you have timing flexibility, stronger reserves, and a clear path to refinance or payoff.

- Choose construction-to-permanent if you want to reduce the risk of having to re-underwrite the whole deal after the build ends.

The best structure is the one that still works when the project is a little late, a little over budget, or a little slower to stabilize than you hoped.

Comparing Lenders for Your Construction Project

Capital is available. The issue isn’t whether money exists. The issue is whether your project fits the lender’s risk box.

That distinction matters in construction lending because the wrong lender can waste months. They may like your business, but not your property type. They may like the property type, but not your timeline. They may like both, but their internal process can’t keep up with a project that needs coordinated draws and practical judgment.

A helpful sign for borrowers came in late 2025, when single-family construction loan volume posted its first annual gain in more than two years, reaching $91.2 billion, according to Scotsman Guide’s report on construction lending volume. That doesn’t mean every commercial borrower gets easy terms. It does mean lenders still have appetite for projects that are clearly structured and well documented.

Three lender types and what they usually mean

| Lender Type | Best For | Typical Rate Environment | Key Consideration |

|---|---|---|---|

| Large banks | Established borrowers with strong financials and time for process | Often disciplined and policy-driven | Approval can be slower and less flexible |

| Local credit unions | Relationship-focused borrowers with community ties | Can be competitive for the right member profile | Capacity and project size fit matter |

| Specialty lenders and fintech platforms | Borrowers who value speed, optionality, and a wider lender network | Varies by structure and risk profile | You need to understand the full economics, not just the headline quote |

What works and what doesn’t

Large banks work well when your file is clean, your reporting is strong, and your project fits a category they already know. They don’t work well when the deal needs unusual timing, nuanced judgment, or exceptions.

Credit unions can be excellent when local knowledge matters. They often understand regional contractors, submarkets, and owner-occupied demand better than distant institutions. They can be less ideal when your project needs broader structuring options or larger-scale lending capacity.

Specialty lenders and fintech-enabled platforms are often strongest when speed, comparison, and packaging matter. They can help borrowers surface options that a single bank relationship won’t reveal. If you want a practical overview of how these models differ in speed and process, this comparison of fintech lenders and banks is worth reading.

The best lender isn’t the one with the best brand. It’s the one whose underwriting model matches your project.

The smartest borrowers I’ve seen don’t ask, “Who has the cheapest rate?” They ask, “Who can execute this structure without slowing the project down?”

How to Secure the Best Possible Construction Loan Rate

Lowering your construction loan rate starts before you ask for one.

Lenders don’t reward optimism. They reward files that remove doubt. If you want stronger pricing, your job is to make the project easier to understand, easier to monitor, and easier to repay.

Build a lender-ready package

A good project package doesn’t read like a pitch deck. It reads like an execution plan.

Include the plans, permits status, contractor information, itemized budget, timeline, source and use of funds, and a clear explanation of what the completed project does for the business. If the property supports expansion, show how. If it improves operating efficiency, explain where. If it consolidates multiple facilities, make that operational logic easy to follow.

The stronger the package, the less the lender has to guess.

Strengthen the parts of the file you control

You can’t control the market. You can control how risky you look inside it.

Focus on these areas:

- Credit presentation: Clean up avoidable issues before applying. Lenders price uncertainty harshly.

- Liquidity proof: Show that the business can absorb delays, cost surprises, and working capital needs during the build.

- Contractor quality: A vetted general contractor gives lenders confidence that the timeline and budget are grounded in reality.

- Valuation support: Detailed specs, finishes, and project rationale help the appraiser and underwriter understand the completed value.

A quote usually improves when the lender sees fewer loose ends.

Field note: Owners often negotiate rate first. Strong borrowers negotiate doubt out of the file first, then discuss rate.

Negotiate beyond the interest rate

The note rate gets attention because it’s easy to compare. It isn’t the only term that matters.

Ask about draw timing, inspection requirements, extension flexibility, conversion mechanics, reserves, and any fees tied to changes during construction. A loan with a slightly better headline price can still become the more expensive option if draws are slow or extension terms are punitive.

This is especially important for operating businesses. A delayed draw can affect contractor relationships, opening schedules, inventory planning, and hiring timelines. That operational spillover is real.

Consider government-backed paths if credit isn’t pristine

Plenty of borrowers assume construction financing is closed off unless they bring near-perfect credit and a very large equity check. That’s not always true.

For borrowers with credit scores below 680, alternatives to conventional structures exist. According to Trident Home Loans’ comparison of 2025 construction loan rates, VA construction loan rates were in the 6% to 7.25% range, and FHA programs can also provide a path that many standard rate roundups overlook.

That doesn’t mean every business project fits those programs directly. It means owners shouldn’t accept generic advice that treats one borrower profile as the only financeable profile.

Use competition carefully

Shopping lenders is smart. Spraying the market is not.

A controlled process works better. Present the same clean package to a selected group of lenders that finance your project type. That gives you real comparables without creating conflicting narratives or unnecessary underwriting noise.

If you’re evaluating build-phase financing more broadly, this guide to navigating commercial construction loans before breaking ground is a practical next read.

Think in ROI, not just borrowing cost

A lower rate is good. A faster, cleaner project is often better.

If one lender offers a modestly tighter quote but creates approval drag, rigid draws, or uncertain conversion terms, the business may lose more in delays and distraction than it saves in financing cost. Construction debt should support the expansion plan, not compete with it for management attention.

The best construction loan rate is the one attached to a structure your business can execute well.

Business owners who need to compare options without turning the process into a full-time job can start with Business Loan Warrior. The platform lets you check pre-approval through a single no-fee application without affecting credit, compare suitable funding paths, and move faster on construction and expansion financing when timing matters.

Refined using Outrank tool