You're probably in one of these situations right now. You've got an acquisition under LOI, a facility expansion approved internally, or a major equipment program that rolls out in phases. You need committed capital, but you don't need all of it on day one.

That's where most owners make an expensive mistake. They take a standard term loan, receive a lump sum, and start paying interest on money that sits idle. Or they lean on a revolver that was built for working capital, not a long, staged growth plan. A delayed draw term loan solves a different problem. It gives you committed capital with a schedule that matches the project.

If your company is doing $20 million to $50 million in annual sales, this isn't a niche product. It's often the cleanest way to fund multi-step growth without dragging unnecessary interest expense through your P&L. The right move isn't just finding capital. It's structuring capital so timing works in your favor.

Table of Contents

- Your Next Big Move Needs Smarter Funding

- Deconstructing the Delayed Draw Term Loan

- DDTL vs Other Financing A Strategic Comparison

- Is a DDTL Right for Your Growth Plan

- Qualifying for a DDTL An Underwriters Checklist

- Decoding a Sample Term Sheet and Repayment Scenarios

- Securing Your DDTL with Business Loan Warrior

Your Next Big Move Needs Smarter Funding

A delayed draw term loan is best used when your growth plan has a known destination but an uneven timeline. That includes capex programs, phased equipment installs, branch rollouts, construction draws, and add-on acquisitions that won't all close at once. In those cases, taking a full disbursement upfront is sloppy finance.

The strategic issue is simple. Capital timing affects total borrowing cost. If funds arrive before you can deploy them, you're paying for optionality you're not using. If capital isn't committed when you need it, you risk missing a deal, delaying a project, or renegotiating from a weaker position.

A delayed draw term loan gives you a middle ground. You lock in a committed facility today, then pull funds later under agreed terms. That matters because uncertainty doesn't just come from revenue. It comes from project sequencing, vendor lead times, construction milestones, diligence windows, and integration risk.

The practical decision

Use this product when three things are true:

- You know the use of funds. The project is defined. You're not borrowing just to “have flexibility.”

- You won't need the full amount immediately. The spend happens in stages, not in a single wire.

- You want certainty. You need committed capital reserved for your business, not a bank's informal promise.

Practical rule: If your capital plan is phased but non-optional, a delayed draw term loan usually beats both a lump-sum term loan and a working-capital revolver.

That's also why the product keeps showing up in larger structured financings. It matches real business timing better than simpler loan formats. You get discipline, not just flexibility.

What matters to your bottom line

For an owner-operator, the value isn't academic. It shows up in four places:

- Lower carry cost early in the project. You don't accrue interest on undrawn principal.

- Cleaner cash flow forecasting. Draws can line up with milestones or purchase schedules.

- Better board-level capital planning. Finance, operations, and lenders all work from the same playbook.

- Less temptation to misuse proceeds. Because draws are staged, capital usually stays tied to the original plan.

The mistake I see most often is treating this as “just another loan option.” It's not. It's a financing structure for companies that already know where they're going and want to stop overpaying on the trip.

Deconstructing the Delayed Draw Term Loan

A delayed draw term loan gives you committed capital on a timetable

You are opening a second facility, rolling out equipment in phases, or funding a multi-quarter acquisition integration. You know the capital plan. You do not need every dollar on day one.

That is where a delayed draw term loan earns its place.

The lender approves a maximum facility upfront. You draw against that commitment later, in stages, under terms negotiated at closing. For a $20 million to $50 million business, that changes the financing conversation from “how much can we borrow today?” to “how precisely can we match debt to execution?”

A standard term loan is blunt. Full funding lands at close, and interest starts on the full balance. A DDTL is tighter. You bring in debt when the project needs it, not when the lender's documentation is finished.

That discipline protects margin. It also keeps your balance sheet cleaner while the project is still ramping.

The mechanics that affect cost, flexibility, and negotiating power

Three terms drive the outcome.

First, the commitment amount. This is the total capital the lender sets aside for your business. Even if you do not draw all of it, the lender is reserving lending capacity and pricing the facility accordingly.

Second, the draw period. This is the window in which you can access the approved capital. If your construction timeline, equipment deliveries, or integration milestones slip, a short draw period becomes expensive fast. You want the draw window built around your operating plan, not the lender's template.

Third, the cost structure. You pay interest only on drawn funds. That is the headline benefit. But you also need to price the reservation cost on undrawn capital, usually through ticking fees or commitment fees.

Here is the mistake owners make. They focus on the coupon and ignore the carry math.

If you negotiate a $5 million DDTL at 10% and draw only $2 million in the first six months, your annualized interest on the drawn amount is about $200,000 for that period. If the lender charges a 1% fee on the $3 million undrawn balance, that adds another $15,000 over six months. The structure still saves money versus taking the full $5 million upfront, but only if your draw timing is realistic and your fee schedule is reasonable.

That is why you should press on these points:

- Length of the draw window. Match it to your real project schedule, with cushion for delays.

- Conditions for each draw. Keep reporting and covenant tests tight enough for the lender, but not so restrictive that one soft quarter blocks funding.

- Ticking fee start date. Push for the fee to start later, or step up gradually instead of charging from day one.

- Minimum draw sizes. Small required draw increments can force bad timing and unnecessary interest expense.

If you are weighing staged capital against more flexible working capital, our guide on when to choose a secured line of credit over a term loan is worth reading before you sign anything.

What this loan does, and what it does not do

A DDTL is built for a defined use of proceeds. Expansion capex. Equipment rollouts. Acquisition-related integration. Large, phased investments with a known endpoint.

It is not a substitute for a revolver. Once you draw and repay, you usually cannot draw that money again. That single feature matters more than many term sheets make clear.

Use a DDTL when the spending plan is mapped, staged, and material. Do not use it to cover routine liquidity gaps, uneven receivables, or operating surprises. That is how businesses end up with the wrong product, the wrong covenants, and an avoidable cash squeeze halfway through a growth plan.

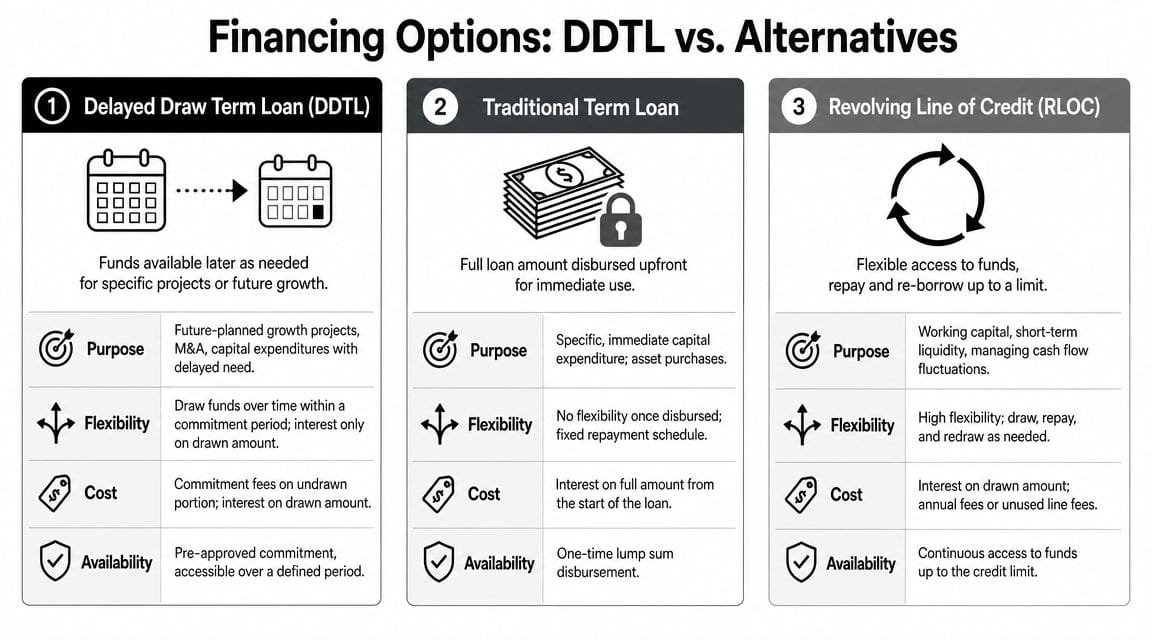

DDTL vs Other Financing A Strategic Comparison

The question isn't whether a delayed draw term loan is better than other financing. The question is whether it matches the job.

The market itself tells you this is a serious product category. The global DDTL market was valued at $14.8 billion in 2024, with banks holding over 70% of market share and secured DDTLs representing over 65% of revenue, according to Market Intelo's delayed draw term loan market report. That concentration makes sense. Asset-backed, project-based financing is exactly where this structure earns its keep.

Where each option wins

A traditional term loan works when the purchase is immediate and singular. Buy a machine, close on a building, refinance debt. You need all the money now. Simplicity matters more than timing precision.

A revolving line of credit works when borrowing needs fluctuate. Payroll gaps, inventory swings, seasonal working capital, uneven receivables. You draw, repay, and redraw. That's liquidity management.

A delayed draw term loan works when the spend is planned, material, and phased. You want committed capital, but you refuse to pay interest on idle cash. That's capital efficiency.

If you're still deciding between a line and a term structure, this guide on choosing a secured line of credit over a term loan is a useful parallel read because it clarifies when reusable liquidity beats fixed-purpose debt.

A side by side decision table

| Financing type | Best use case | Funding pattern | Reborrow after repayment | Main cost issue | Strategic downside |

|---|---|---|---|---|---|

| Delayed draw term loan | Multi-phase expansion, acquisition pipeline, construction, staged capex | Draw over time under a committed facility | No, generally not | Ticking fees on undrawn capital plus interest on drawn amounts | More documentation and tighter use-of-funds discipline |

| Traditional term loan | Immediate one-time purchase or refinance | Full amount funded at closing | No | Interest starts on the full principal | You can end up carrying idle cash |

| Revolving line of credit | Working capital and short-term liquidity swings | Draw, repay, redraw | Yes | Variable usage costs and line-related fees | Usually not ideal for long-horizon strategic projects |

Use a revolver for uncertainty in timing and amount. Use a delayed draw term loan when the amount is committed but deployment is staged.

That distinction matters because too many owners use the easiest product to close, not the right product to carry. The expensive part often comes later.

Is a DDTL Right for Your Growth Plan

Three situations where it fits

A manufacturer replacing and adding production capacity over several quarters is a strong candidate. The first draw might fund deposit payments and site prep. Later draws cover equipment delivery, installation, and ramp-up costs. That's cleaner than carrying a full lump sum while waiting on vendor timelines.

A private equity-backed company running a buy-and-build strategy is another obvious fit. The structure has already proven useful in M&A. One automotive platform secured an $825 million credit facility with $100 million allocated as a DDTL, and a healthcare company used a $1 million DDTL within a $9.25 million buyout structure, as outlined in SoFi's examples of delayed draw term loans in acquisition financing. The lesson for a middle-market owner is straightforward. When add-on deals won't all close at once, staged capital beats idle capital.

A real estate or construction-linked operating business also fits well. Draws can align with inspection points, contractor billing cycles, or completion milestones. That protects the lender, but it also protects you. It prevents overfunding early and forces better project controls.

The real tradeoffs

A delayed draw term loan is powerful, but not forgiving. It rewards preparation and punishes vague planning.

Here's where it shines:

- Capital efficiency: You borrow against a committed facility without taking the full hit on day one.

- Execution certainty: Your lender has already committed capital, which matters when a project can't pause.

- Governance: Draw schedules create discipline across finance, operations, and ownership.

And here's where owners get annoyed:

- Fees on unused money: The facility isn't free to reserve.

- More moving parts: Draw requests, milestones, conditions, and reporting all matter.

- Less flexible than a revolver: This is not a general-purpose liquidity tool.

If your spending plan is still fuzzy, don't use a delayed draw term loan. You'll pay for commitment without getting the benefit of precision.

The right borrower usually has a defined growth path, decent reporting, and enough internal discipline to manage milestone-based funding. If that's you, this product can tighten your capital structure. If it isn't, the structure will expose the weakness.

Qualifying for a DDTL An Underwriters Checklist

Underwriters don't approve a delayed draw term loan because the story sounds exciting. They approve it because the company can support the debt and the draw plan makes operational sense.

The first thing they want is a believable funding narrative. Not a vision deck. A practical schedule showing what gets funded, when it gets funded, and why each draw creates value. If your draw schedule changes every time someone asks a question, expect friction.

What lenders actually review

Think like an underwriter and prepare your file around these five buckets:

- Financial consistency: Clean statements, stable performance, and a business that doesn't look like it's guessing.

- Debt capacity: They'll pressure-test debt levels, fixed obligations, and post-draw repayment ability.

- Collateral support: Many of these facilities are secured, so asset quality matters.

- Management credibility: Lenders back operators who can execute a phased plan without surprises.

- Documentation discipline: They want reporting they can trust before each draw.

Conditions precedent are where many borrowers get tripped up. Before funding is released, lenders may require financial tests or milestone completion. Examples include maintaining Debt/EBITDA below 4x, hitting project milestones, and meeting minimum draw sizes that are often around $500K in private credit, according to Saratoga Investment Corp's guide to delayed draw facilities.

If your business relies on borrowing base assets or frequent collateral updates, tighten that process before you apply. This playbook on keeping SMB lines accurate between audits through borrowing base monitoring is useful because weak reporting can delay draws even after approval.

What kills approvals

Most failed deals don't die because the company is bad. They die because the borrower shows up underprepared.

Common problems include:

- A vague use of funds. “Growth” isn't a draw strategy.

- Weak milestone tracking. If no one internally owns the draw calendar, the facility becomes messy fast.

- Poor covenant awareness. Owners sign terms they haven't modeled.

- Collateral overstatement. Lenders will discount optimism quickly.

Your best move is simple. Build the credit memo before the lender asks for it. If you can explain the project clearly, support it with numbers from your own business, and show exactly when capital gets deployed, underwriting gets easier.

Decoding a Sample Term Sheet and Repayment Scenarios

You approve a $6 million equipment expansion, sign the term sheet, and expect capital to show up as the project moves. Then one delayed install, one vague milestone, and one overlooked fee line turn a good facility into an expensive distraction. That is why smart owners do not skim a delayed draw term sheet. They pressure test how the lender will behave after closing.

The spread matters. It is rarely the deciding factor.

For a $20 million to $50 million business, value is won or lost in four places: how long the capital stays available, what has to happen before each draw, what you pay on unused capacity, and how quickly principal starts coming back out of the business.

The clauses you should negotiate first

Use this as your first-pass review when a draft term sheet lands in your inbox:

| Clause | Why it matters | What to push on |

|---|---|---|

| Commitment amount | Sets the total reserved capital | Size it to the real project budget plus a reasonable cushion, not optimism |

| Availability period | Controls how long you can access future draws | Match it to the actual rollout schedule, with room for vendor or integration delays |

| Draw conditions | Determines whether funding is smooth or a recurring fight | Tie draws to objective milestones your team can document quickly |

| Ticking fee | Prices the undrawn commitment | Negotiate when it starts, whether it steps up, and whether unused commitments can be reduced |

| Repayment structure | Affects cash flow after each draw | Align amortization with the cash flow ramp, not the lender's template |

| Prepayment terms | Controls flexibility if plans change | Cut back penalties and carve out room for early paydown or refinancing |

Market terms have improved in some cases. United Capital Source's discussion of post-rate-cut delayed draw term loan trends notes longer draw periods and lower ticking fees than many borrowers saw in tighter credit conditions. Use that in negotiation. Do not accept stale lender paper when the market has moved.

A strong term sheet is one your finance team can execute without delays, surprises, or repeated lender approvals.

A simple cost model that owners should run before signing

Compare a DDTL to a standard term loan using total cash cost, not stated rate.

Start with three inputs:

- Interest on drawn funds only

- Ticking fee on undrawn funds

- Timing of draws relative to the project's earnings ramp

Here is the simplest way to frame it. If you leave $2 million undrawn for a year and pay a 1% ticking fee, that idle capacity costs $20,000. That number is not alarming by itself. The key question is whether that $20,000 is cheaper than paying a full year of interest on money you did not need yet.

Now get more practical. Assume your company closes a $5 million DDTL for a plant expansion, but only draws $2 million in the first six months because equipment deliveries slip. Under a standard term loan, you would likely be paying interest on the full $5 million from day one. Under a delayed draw structure, you preserve cash while the project catches up. That helps EBITDA conversion, keeps working capital cleaner, and reduces the odds that growth spending starts choking operations.

Execution matters in this context. Build a draw-readiness control room that gets lender funding requests approved faster so treasury, operations, and accounting are all working from the same milestone and document set.

Model three scenarios before you sign:

- Base case: Draws happen on schedule and the earnings ramp follows plan.

- Slow case: Vendors slip, integration takes longer, or a site launch moves out by a quarter.

- Fast case: Inventory, hiring, or equipment deposits hit sooner than expected.

If the structure only works in the base case, reject it or renegotiate it. A delayed draw term loan should give you timing flexibility and cost control. If it cannot handle normal execution drift, it is the wrong facility.

Securing Your DDTL with Business Loan Warrior

Negotiating a delayed draw term loan well starts before you ever pick a lender. You need to know which terms are cosmetic and which ones hit cash flow, operations, and future flexibility.

First, push hard on the availability period. If the draw window is too short, the product loses its value. A lender's aggressive timeline can force premature draws or leave you paying reservation costs on capital you can't use properly.

Second, negotiate objective draw conditions. You want measurable milestones, not vague lender discretion. “Completion of phase one equipment install” is better than language that lets credit committees reinterpret the deal midstream.

Third, treat the ticking fee as a live issue, not boilerplate. Ask when it begins, whether it increases over time, and whether the facility can be right-sized if your capital need changes.

Fourth, model the repayment profile against the actual earnings ramp from the project. If a draw funds expansion before the cash flow arrives, aggressive amortization can squeeze the business at the worst moment.

A platform approach helps because delayed draw structures involve more comparison points than plain vanilla loans. You're not just comparing rates. You're comparing draw flexibility, covenants, collateral terms, reporting burdens, and the ease of getting money released when you need it.

Business Loan Warrior simplifies that process with one application, access to multiple lenders, and a secure dashboard that helps borrowers track approvals, repayments, and credit insights. If speed on draw execution matters to your business, their guide on building a draw-readiness control room for faster funding is worth reviewing.

The best use of a fintech-enabled advisor isn't just finding approval. It's improving the structure before you sign and reducing operational friction after closing. That's where borrowers usually win or lose real money.

If you're weighing a delayed draw term loan for an acquisition, expansion, equipment program, or construction-linked project, Business Loan Warrior can help you check options through one no-fee application without affecting credit, compare lender structures clearly, and move faster from term sheet to funded draw.