If you're thinking about funding right now, you're probably doing what most owners do. You're looking at revenue, checking the bank balance, and wondering why a lender still asks for more documents. From your side, the business may feel stable. From the lender's side, stability has to be proven.

That's what a financial health assessment does. It translates your business into the language underwriters, banks, and nonbank lenders use every day. Done right, it doesn't just tell you whether the company is healthy. It tells you whether a lender will see it as ready, risky, or worth a second look with conditions.

Table of Contents

- Gathering Your Financial Documents

- Understanding the Core Pillars of Financial Health

- Calculating and Benchmarking Your Key Ratios

- Reading the Red Flags What Lenders See

- Building Your Action Plan for Lender Readiness

- Tracking and Maintaining Your Financial Health

Gathering Your Financial Documents

A lender doesn't start with your story. They start with your records.

If those records are incomplete, out of date, or inconsistent across statements, the application slows down immediately. In some cases, it dies there. The cleanest loan files usually come from owners who assemble the whole picture before anyone asks.

The core file every lender wants

Start with the last 12 to 24 months of financial statements and operational records. That time range isn't arbitrary. It's the standard described in an expert SMB financial check methodology, which also stresses comparing performance over time rather than relying on a single snapshot in this guide to SMB financial health checks.

Pull these first:

- Profit and Loss statement. This shows whether the business model produces profit, but by itself it can hide collection problems, inventory buildup, and debt pressure.

- Balance sheet. Lenders test strength with this document. They look at cash, receivables, inventory, payables, debt, and equity.

- Cash flow statement. This is the statement owners skip most often, and it's often the one that explains why a profitable company still struggles.

- Business bank statements. These help lenders verify deposit activity, payment behavior, and real cash movement. If you want a practical breakdown of what underwriters look for, review these business bank statement requirements and warning signs.

- Business tax returns. Tax filings anchor the application to filed records rather than internal reporting.

- Accounts receivable aging and accounts payable aging. These show whether customers are paying slowly and whether you're leaning too hard on vendors.

- Debt schedule. List every loan, line, payment amount, maturity, and collateral position.

Practical rule: If the P&L says you're doing well but the bank account tells a different story, the lender will trust the bank data first.

Where to get the documents and what to clean up

In QuickBooks Online, Xero, and similar systems, you can usually export the P&L, balance sheet, and cash flow statement by date range in a few clicks. That part is easy. The harder part is making sure the data is coded correctly.

Misclassified owner draws, stale receivables, duplicate expenses, and uncategorized transfers can make a decent business look chaotic. If your books have drifted, getting them current before applying is worth it. For owners dealing with incomplete records, catchup bookkeeping services can help rebuild a usable file before a lender starts asking questions.

There's a bigger reason this documentation matters. Objective, supply-side records from banks, payment providers, and tax data create a more reliable picture of real balances, transaction activity, and repayment conditions than subjective surveys do, as discussed in CGAP's analysis of financial health measurement.

What owners usually miss

Two omissions come up constantly:

- They bring only the P&L.

- They bring reports that don't match tax returns or bank activity.

A lender reads inconsistency as risk. Not always fraud. Often just poor controls. But poor controls still affect approval.

Your file should let an outsider answer simple questions fast. What comes in each month? What goes out? What debts already exist? How much pressure is building in receivables, payables, and working capital? If your documents answer those clearly, you're already ahead of many applicants.

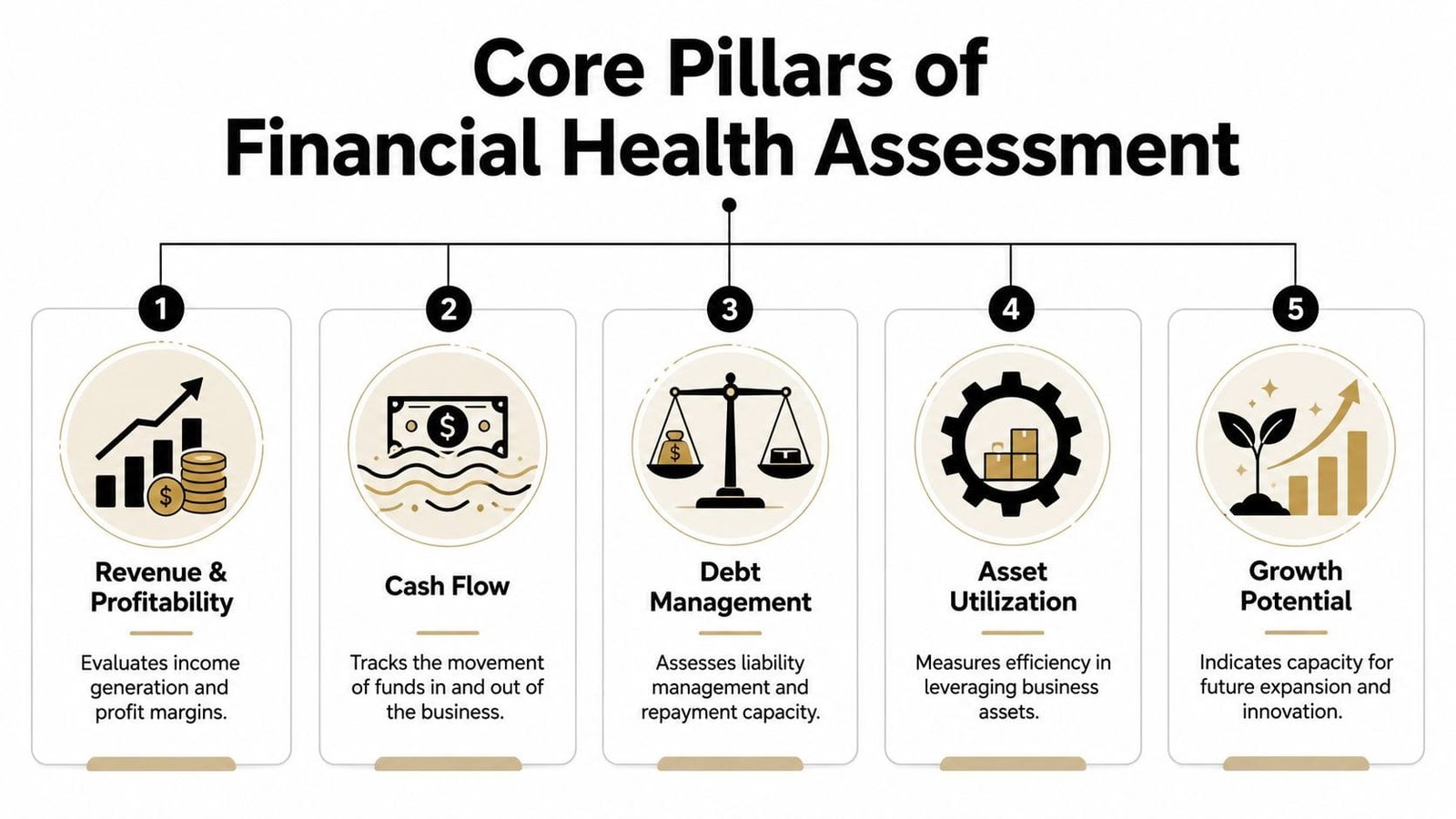

Understanding the Core Pillars of Financial Health

A business can show a profit on paper and still get declined for financing.

That happens when the owner is reading the company from the inside, while the lender is reading it from the outside. Lenders want to know whether the business can take on another fixed obligation without creating strain in payroll, vendor payments, inventory purchases, or existing debt service. A useful financial health assessment starts there.

For owners, I keep the review grounded in five pillars that line up with how underwriters evaluate risk:

- Profitability

- Liquidity

- Solvency

- Efficiency

- Cash flow

This lender-ready view also fits the broader financial health approach developed by the Financial Health Network, which organizes financial health around spending, saving, borrowing, and planning. Their framework is useful because it pushes the conversation beyond income alone and toward financial stability and capacity, which is the same shift lenders make during credit review, as explained in the Financial Health Network's FinHealth Score methodology.

Why these pillars matter in credit review

Profitability answers a basic question. Does the company produce enough margin to support itself? But underwriters know net income can look acceptable while the business still struggles to meet obligations on time. Depreciation policy, owner compensation decisions, and one-time expenses can all change the picture.

Liquidity gets closer to daily operating reality. It measures whether short-term assets can cover short-term obligations without last-minute borrowing or delayed payments. That is why businesses with decent sales and thin cash reserves often run into trouble during underwriting. If you are trying to close timing gaps between receivables and payables, a clear grasp of working capital for businesses helps because that is exactly where lenders start pressing for detail.

Solvency looks at the long game. A lender reviews how much debt the business already carries, how much owner equity is at risk, and how much room is left if revenue softens. A company with moderate profit and low debt can still look financeable. A company with the same profit and heavy debt often does not.

Efficiency tells lenders how well management turns resources into revenue and cash. Slow collections, aging inventory, or underused equipment do not always show up as a crisis in the profit and loss statement. They do show up in repayment risk.

Cash flow ties the whole file together. It answers the question lenders care about most. Can this business make loan payments from normal operations while still running the company properly?

How lenders read the pillars together

No lender approves a loan because one metric looks good. They weigh the combination.

A business with strong margins and a temporary liquidity squeeze may still be a workable borrower if receivables are clean and debt is controlled. A business with thin margins, weak liquidity, and rising debt gives the lender three separate reasons to hesitate. This reveals the value of a financial health assessment. It shows whether one weak area is manageable or whether several weak areas are starting to stack up.

Interest burden is a good example. Owners often focus on the payment amount and miss the coverage question underneath it. Lenders do not. They want to see how comfortably operating earnings support interest expense, which is why understanding interest cover for due diligence matters when you are judging whether current debt already limits your borrowing capacity.

Later in the review, this short visual helps frame the discussion with owners and finance teams.

The goal is not perfection across every pillar. Few businesses have that. The goal is a balanced file that shows the company can absorb debt, handle routine volatility, and keep operating cleanly. Once owners start viewing financial health through a lender's eyes, loan decisions stop feeling mysterious and start looking much more predictable.

Calculating and Benchmarking Your Key Ratios

A lender reviewing your file is doing simple math before they buy into the story. If the ratios are weak, every explanation has to work harder. If the ratios are sound, underwriting starts from a better place.

Start with the ratios lenders use

Pull the numbers from your own balance sheet and income statement. Then calculate the ratios that map to the credit questions underwriters care about: liquidity, indebtedness, operating efficiency, and whether the business is improving or slipping.

| Ratio Category | Ratio Name | Formula | What It Measures |

|---|---|---|---|

| Liquidity | Current Ratio | Current Assets / Current Liabilities | Near-term ability to cover short-term obligations |

| Solvency | Debt-to-Equity Ratio | Total Liabilities / Total Equity | How much debt supports the business relative to owner equity |

| Efficiency | Asset Turnover Ratio | Revenue / Average Total Assets | How effectively assets generate revenue |

| Growth | Revenue Growth Rate | (Current Period Revenue – Previous Period Revenue) / Previous Period Revenue | Direction of top-line performance |

| Growth | Operating Income Growth Rate | (Current Period Operating Income – Previous Period Operating Income) / Previous Period Operating Income | Whether operations are strengthening or weakening |

These are standard credit review measures. The formulas are consistent with ratio definitions used in lender training materials, commercial banking analysis, and financial statement guidance from institutions such as the Corporate Finance Institute's ratio analysis reference and the U.S. Small Business Administration's guidance on preparing financial statements for financing.

The calculation matters less than the read-through. Here is what lenders are looking for behind the number:

Current Ratio

If current assets are 200 and current liabilities are 100, the current ratio is 2.0. On paper, that looks comfortable. In practice, a lender will check whether those current assets are usable. Cash counts. Receivables usually count if collections are clean. Old inventory gets discounted fast.Debt-to-Equity Ratio

If liabilities are 300 and equity is 150, the debt-to-equity ratio is 2.0. That tells the lender creditors are carrying a large share of the capital structure. Some industries can support that. Others cannot. The key question is whether earnings and cash flow are strong enough to justify the debt already on the books.Asset Turnover Ratio

If revenue is 500 and average total assets are 250, the ratio is 2.0. That suggests the business is generating two dollars of revenue for each dollar invested in assets. A wholesaler and a manufacturer will not benchmark the same here, so this ratio only means something when you compare it to the right peer set.

Lender lens: A good ratio in the wrong business model is still a weak credit argument.

Benchmarking is where owners often go off course. They compare this year to last year, see improvement, and assume the file is strong. A lender compares your trend to your industry, your debt load, and your repayment capacity at the same time.

Benchmark against the right peer group

Use industry data that matches your business type as closely as possible. The Federal Reserve Banks note in their Small Business Credit Survey reporting that lender decisions depend heavily on cash flow strength, debt burden, and how the business compares within its operating context. Risk teams do not benchmark a plumbing contractor the same way they benchmark a SaaS firm or a seasonal retailer.

A practical benchmarking process looks like this:

- Use the right industry classification. A category that is too broad can make weak numbers look normal.

- Review several reporting periods. Seasonal businesses can look unhealthy or unusually strong in a single quarter.

- Compare to a range, not just an average. Median and upper-quartile performance often tell you more than one blended number.

- Track direction. Lenders will often finance improvement with a credible explanation faster than decline with no explanation.

Liquidity deserves extra scrutiny because it shapes daily repayment confidence. If you want a practical benchmark for that area, review what a healthy working capital ratio means for loan approval. It helps separate a balance sheet that looks fine from one that can absorb payroll, vendor terms, and loan payments without constant strain.

Debt service capacity also belongs in this ratio review. A file can survive average margins and modest debt levels if interest coverage is clean. It gets much harder to defend when current debt is already eating into operating flexibility, which is why understanding interest cover for due diligence belongs alongside your other credit ratios.

The goal is not to produce perfect numbers. The goal is to know, before the lender tells you, which ratios support the loan request, which ones need explanation, and which ones need fixing first.

Reading the Red Flags What Lenders See

A business owner walks into a loan meeting convinced the story is strong. Sales are up from last year, the team is busy, and there is real demand in the pipeline. Then the lender starts asking why payables keep stretching, why draws increased while cash fell, and why the last loan did not produce stronger operating cash flow. That gap matters. Lender readiness means seeing the file the way an underwriter sees repayment risk, not the way an owner experiences effort and momentum.

Underwriters read for pressure points first. They want to know what could interrupt repayment over the next 12 to 24 months, and whether management sees those risks early or only after cash gets tight.

Trends that trigger lender concern

One weak month rarely kills a deal. A pattern without a credible explanation often does.

Red flags usually show up in combinations:

- Sales are holding, but gross profit keeps slipping

- Accounts receivable are growing faster than revenue

- Past-due receivables are turning into the main source of working capital pressure

- Inventory is rising, but turnover is slowing

- Short-term liabilities are covering problems that should have been fixed operationally

- Owner distributions continue while the business is asking for outside capital

- Bank activity shows frequent overdrafts, last-minute transfers, or uneven cash management

A lender also tests whether reported strength is usable strength. Cash on a balance sheet means less if it is spoken for by tax obligations, delayed payroll, or supplier pressure. A healthy current ratio means less if too much of it sits in old inventory or slow receivables. Strong revenue growth means less if collections, margins, and cash conversion do not improve with it.

That is why mature businesses get harder questions than early-stage firms. A newer company may get room for uneven earnings if the model is proving out. An established company is expected to show operating control.

Good debt versus distress debt

Debt itself is not the problem. Purpose, structure, and timing are the problem.

I have seen lenders support businesses with meaningful debt loads because the borrowing financed equipment that improved throughput, inventory tied to confirmed orders, or a location expansion backed by clear demand. I have also seen lenders decline smaller requests because the new loan was really covering payroll, old vendor balances, and prior borrowing that never fixed the underlying issue.

That is the line between growth debt and distress debt. The Federal Reserve Bank of St. Louis discusses the financing patterns of growth-oriented firms and why debt can support expansion when the business can carry it, which is a useful counterweight to the idea that all borrowing signals weakness: Growth opportunities and debt financing.

An underwriter will usually pressure-test new borrowing with questions like these:

Does this loan fund an asset or activity that improves revenue, margin, or capacity?

Is there a clear repayment source beyond hope, seasonality, or another refinance?

Did management identify the problem early, and can they explain the numbers without guessing?

Are they borrowing to expand a stable engine, or to keep an unstable one running?

Good debt leaves evidence. You can see what it bought, how it helps operations, and how repayment fits into normal cash generation. Distress debt leaves a different trail. Rising balances, repeated renewals, stretched vendors, and no measurable improvement after prior borrowing.

That distinction shapes lender confidence more than many owners realize. If your financial health assessment shows that new debt has a defined job and a realistic payoff, the request reads as planned growth. If the file suggests the loan mainly buys time, the lender prices for risk, asks for more collateral, shortens terms, or declines the deal outright. For owners who want a clearer view of documentation and lender expectations, these legal insights on commercial loans help connect the financial story to the approval process.

The practical question is simple. If a lender froze your credit line tomorrow, would the business still function long enough to repay what it already owes? If the answer is no, the red flag is already visible in the file.

Building Your Action Plan for Lender Readiness

A lender asks for updated financials on Tuesday. By Thursday, you need more than decent numbers. You need a clear explanation of what is weak, what is improving, and what management is doing about it. That is what an action plan does. It turns a financial health assessment into a credit case.

Fix the urgent issues first

Start with the items that can block repayment capacity over the next 30 to 90 days. Lenders look for short-term stability before they give much credit for long-term plans.

If cash flow is under pressure, focus on speed and timing.

- Shorten collection time. Push overdue invoices harder, bill faster, and ask for deposits or progress payments when the market supports it.

- Match payables to receivables. Better supplier terms can relieve strain if they line up with how cash comes in.

- Stop avoidable cash loss. Freeze spending that does not protect revenue, delivery, or collections.

If debt is the weak point, clean up purpose and structure.

- Stop adding debt without a defined return. Each loan should fund capacity, margin, or a specific contract, not cover a recurring shortfall with no fix behind it.

- Review refinance offers with caution. Lower monthly pressure can help, but a longer term or extra fees may leave the business weaker six months from now.

- Limit owner draws during the repair period. A lender will notice if cash leaves the business while the business is asking for support.

If margins are soft, fix economics before chasing volume.

- Reprice work that does not earn enough. Owners usually know which customers, jobs, or product lines are busy but not worth the effort.

- Cut low-value cost before cutting productive capacity. The goal is better earnings, not a weaker operation.

- Review sales mix. More revenue does not help if the added volume carries thin margin or high service cost.

I have seen plenty of turnarounds built on ordinary moves. Cleaner invoicing. Tighter expense control. Better job costing. Fewer exceptions. None of that sounds dramatic, but lenders trust boring improvements because they are easier to verify.

Set goals that are specific, measurable, and time-bound. For example, reduce days sales outstanding over the next quarter, bring inventory back to a target range by a set date, or raise gross margin on a weak service line before the next renewal request. The Small Business Administration recommends setting clear, realistic business goals and reviewing progress regularly, which is the discipline lenders want to see in an improvement plan.

Turn weak spots into a lender narrative

A strong loan file does not pretend nothing is wrong. It shows that management understands the problem, can document the cause, and has taken steps that fit the numbers.

Say receivables jumped because one large customer paid late. Show the aging, note how concentrated that customer is, and explain what changed, such as revised terms, a deposit requirement, or a backup customer pipeline. If inventory rose ahead of a signed contract, tie the increase to purchase orders and delivery dates. If debt went up to buy equipment, connect that purchase to throughput, labor savings, or the capacity to take on more profitable work.

At this juncture, owners either build confidence or lose it. A vague explanation sounds defensive. A documented explanation sounds managed.

Keep the narrative practical. What happened. Why it happened. What changed. What the numbers should look like next if the plan works. That is how you help an underwriter see the business through a credit lens instead of a crisis lens.

That same discipline matters when questions come up about collateral, guarantees, covenants, and loan structure. Owners who want a plain-English primer on those issues can review these legal insights on commercial loans before signing anything.

Lender readiness comes down to evidence. Show that the business knows its weak spots, is fixing the right ones first, and can explain the path from today's numbers to a safer loan tomorrow.

Tracking and Maintaining Your Financial Health

Strong borrowers don't wait for a funding need to review the numbers. They build a rhythm and stick to it.

Build a review rhythm

Review key ratios monthly if cash is tight or the business is growing quickly. Review them quarterly if operations are stable and your reporting is clean. In either case, use the same definitions each time so you can spot real change instead of reporting noise.

Track a short list consistently:

- Liquidity measures so short-term strain doesn't surprise you

- Debt measures so debt doesn't creep past comfort

- Efficiency measures so cash isn't trapped in operations

- Revenue and operating trends so deterioration shows up early

Keep the process simple enough that it happens. A spreadsheet can work. A dashboard is better if it pulls in accounting and banking data reliably. The point isn't flashy reporting. The point is staying ready before the next opportunity or problem arrives.

A good financial health assessment becomes part of operating discipline. That changes the lending conversation. Instead of scrambling to explain last-minute numbers, you're showing a business that knows itself and manages risk on purpose.

If you're preparing for funding and want a faster way to organize your next move, Business Loan Warrior gives you a practical starting point. You can explore funding options, review loan pathways, and move toward lender readiness with a process built for real business operators, not just perfect paper files.