You’re probably looking at a deal package right now that looks good on the surface. The seller has fuel volume numbers, the store looks busy, and the asking price feels just within reach if financing comes together. Then the questions start. How much cash do you need down? Which loan program fits a gas station? What will the lender care about most? And the one first-time buyers often underestimate: what happens if the tanks or site history trigger environmental concerns?

Gas station loans aren’t simple retail loans. A lender isn’t just financing a store. They’re evaluating a business, a real estate asset, specialized equipment, fuel operations, compliance history, and environmental liability all at once. That’s why a clean-looking transaction can still stall late in underwriting, and why a well-prepared borrower can often move faster than a borrower with a stronger balance sheet but weaker documentation.

The gas station and convenience store sector still matters at scale. The industry supports over 152,000 locations and total industry revenue is projected to reach $121.0 billion in 2025, despite a slight decline from the prior year, according to Clarify Capital’s gas station business loan overview. That scale is exactly why lenders stay active in this space. They know demand is durable. They also know bad deals usually fail for very specific reasons.

Table of Contents

- Fueling Your Ambition An Introduction to Gas Station Loans

- Decoding Your Funding Options Gas Station Loan Types

- Passing the Lender's Test Key Qualification Metrics

- The Hidden Deal-Breaker Environmental Due Diligence

- SBA vs Conventional Loans Choosing Your Path

- Your Application Roadmap From Checklist to Closing

- Common Pitfalls and Alternative Funding Sources

- Frequently Asked Questions About Gas Station Financing

Fueling Your Ambition An Introduction to Gas Station Loans

Owning a gas station can be a strong business if you buy the right site, finance it correctly, and respect the operational details. It’s not just fuel. It’s inside sales, labor, payment systems, vendor terms, compliance, and often a real estate decision wrapped into the same transaction. That combination creates upside, but it also creates financing friction.

Buyers usually focus first on price and down payment. Lenders often focus first on cash flow quality, site risk, and whether the file can survive environmental review. That difference in focus is where many deals go sideways. A borrower thinks the deal is about valuation. The lender thinks the deal is about repayment and risk containment.

Practical rule: A gas station deal rarely gets approved because the story sounds good. It gets approved because the numbers, documents, and site history line up cleanly.

The financing path is usually clearer once you answer three questions early:

- Are you buying, refinancing, or upgrading? The use of funds drives the loan structure.

- Is the property included? A business-only purchase underwrites differently than a business-plus-property deal.

- Has environmental work already been done? If not, assume that issue can shape both approval and pricing.

Owners who prepare for those questions early tend to negotiate from a stronger position with both lenders and sellers.

Decoding Your Funding Options Gas Station Loan Types

Loan structure matters more in gas station financing than many buyers expect. A good site can still become a bad loan request if the debt product does not match the actual use of funds, collateral, and site history. I see that mistake most often when a buyer tries to force acquisition costs, equipment upgrades, and short-term operating needs into one facility without considering how the lender will treat environmental risk on each piece of the request.

The first decision is simple. Are you financing a business purchase, real estate, equipment, working capital, or a mix of all four? Your answer will narrow the field fast.

The main loan categories

SBA 7(a) is usually the most flexible option for a gas station purchase. It can work for an acquisition, partner buyout, refinance, equipment, and some working capital in the same transaction. That flexibility helps when a station changes hands with fuel inventory, inside-store inventory, franchise fees, and deferred maintenance all showing up at once.

SBA 504 is a better fit when property and fixed improvements carry the deal. If the plan involves land, the building, canopy work, tank-related site improvements, or a major renovation, 504 often gives a stronger long-term structure. It is less flexible for mixed business-purpose costs, but it can be attractive when property is the main collateral and the borrower wants predictable occupancy cost.

Equipment financing works best for identifiable hard assets with a useful life the lender can underwrite clearly. Pumps, point-of-sale systems, refrigeration, kitchen equipment, signage, and some car-wash components often fit here. Separating equipment from the main acquisition loan can preserve liquidity, but it also creates another monthly payment, so the cash flow needs to support both notes.

Conventional commercial term loans can work well for stronger borrowers, especially in refinance transactions or acquisitions with larger down payments. Banks like them when the station has clean financials, stable deposits, and a property file that will not create problems in closing. If environmental reports show unresolved issues, conventional lenders often tighten terms faster than borrowers expect.

Lines of credit serve a different purpose. They are operating tools, not purchase money loans. Fuel purchases, payroll timing, seasonal inventory swings, and short-term cash gaps are common uses. Using a revolving line for a major capital project usually creates repayment pressure too early.

Merchant cash advances are emergency money. They are expensive, they pull hard on daily cash flow, and they can weaken a future bank or SBA request. I only view them as a last option when the owner has a clear exit plan and no realistic lower-cost alternative.

Comparison of Common Gas Station Loan Types

| Loan Type | Typical Use Case | Typical Term | Equity Requirement | Main Caution |

|---|---|---|---|---|

| SBA 7(a) | Acquisition, refinance, mixed-use funding | Medium to long term | Usually a borrower injection is required | Environmental issues can delay approval and reduce flexibility |

| SBA 504 | Real estate, construction, major fixed assets | Long term | Usually lower cash outlay than many conventional structures, depending on the deal | Less useful for inventory, goodwill, or broad working capital |

| Equipment Financing | Pumps, POS systems, refrigeration, signage | Matches asset life more closely | Often lower upfront cash than a full term loan | Creates separate debt service and may exclude site-related work |

| Conventional Term Loan | Purchase or refinance for stronger borrowers | Varies by bank and collateral | Often higher equity required than SBA | Banks may be stricter on environmental history and debt coverage |

| Line of Credit | Fuel purchases and short-term operating swings | Revolving | No traditional down payment structure | Poor fit for long-term improvements |

| Merchant Cash Advance | Urgent repair or immediate cash need | Very short term | No traditional equity injection | High cost and heavy pressure on daily cash flow |

How owners should choose

Start with the asset that drives lender risk.

If real estate is included and underground storage tanks are part of the collateral, the loan choice is never just about rate and term. It is also about which lenders will stay in the deal after they review the Phase I report, prior releases, monitoring history, and state cleanup file. First-time buyers often miss this point and waste time comparing products that are not equally realistic for the site.

A practical framework helps. Match the loan to the business objective, then test whether the station’s financial profile supports that structure. This guide on aligning loan types with financial KPIs is useful for that second step.

Here is the short version:

- Buying a station with business value, inventory, and goodwill: start with SBA 7(a).

- Buying or improving owner-occupied real estate: evaluate SBA 504 and conventional bank debt.

- Replacing specific hard assets: price equipment financing separately before adding everything to the main loan.

- Managing fuel and inventory swings: use a line of credit if the cash cycle supports it.

- Covering a true emergency: use fast money only if you can show exactly how it will be repaid.

One more trade-off matters. A single loan is simpler to close, but it is not always the cheapest or safest structure. Splitting the request between a real estate loan, an equipment note, and a working capital line can improve flexibility. It can also complicate underwriting and intercreditor issues. The right answer depends on cash flow, collateral, and how clean the environmental file is.

That last point changes more deals than buyers expect. A station with strong sales but a messy environmental history may still get financed, but often on narrower terms, with more cash required, more reserves, or fewer lender options. The loan type does not override site risk. It has to fit around it.

Passing the Lender's Test Key Qualification Metrics

Gas station underwriting is a business health check. Lenders review the borrower, the site, the cash flow, and the downside case. A borrower may think the station is profitable. An underwriter wants proof that it can stay profitable under pressure.

What underwriters are really measuring

For stations in the $20 million to $50 million revenue range, underwriters often use adjusted EBITDA multiples of 4.5x to 6.5x and look for DSCR above 1.5x, especially when the location has more than 30 percent non-fuel revenue, according to AMAA’s deal analysis on underwriting gas-station-type assets. That tells you two things immediately.

First, lenders don’t want to rely only on fuel. Fuel volume matters, but inside sales, foodservice, and other non-fuel revenue streams can make the file stronger. Second, they care about how much room the business has after debt payments, not just whether last year looked good.

How to think about DSCR in plain English

Debt Service Coverage Ratio answers one question: after normal business expenses, is there enough cash flow left to pay the proposed debt with margin for error?

If a lender wants DSCR over 1.5x, they’re saying the business should produce meaningfully more cash than the annual debt obligation. A borrower doesn’t need to obsess over the formula as much as the implication. Thin coverage means one bad quarter can turn into a payment problem.

Lenders don’t underwrite to your best month. They underwrite to whether the station still pays its debt when fuel margins tighten, traffic softens, or repair costs show up.

Adjusted EBITDA matters for a related reason. It’s the lender’s attempt to normalize earnings. They’ll review reported profit, then adjust for owner-specific items, one-time expenses, or unsupported add-backs. Borrowers often overestimate how much “adjustment” a lender will accept. If it can’t be documented cleanly, it usually won’t help.

For a broader framework on matching financing structure to the numbers lenders care about, this guide on aligning loan types with financial KPIs is useful context.

What strengthens a file before submission

The strongest applications usually have the same traits:

- Clean financial statements: tax returns, P&Ls, and balance sheets should reconcile without obvious gaps.

- A credible operating story: if revenue depends heavily on inside sales, document that clearly.

- A realistic down payment source: lenders want to know where the cash comes from and whether it stays available.

- Experience or support: if you haven’t operated a station before, bring in an experienced manager, consultant, or operating partner.

What weakens a file is just as predictable. Inconsistent books, inflated projections, undocumented seller claims, and vague explanations around site performance all slow approvals.

The Hidden Deal-Breaker Environmental Due Diligence

Most first-time buyers spend too little time on environmental review until the lender forces the issue. That’s backwards. On a gas station, environmental due diligence should start early, because once underground storage tanks enter the picture, the lender’s risk analysis changes.

Why gas stations get screened differently

A 2025 EPA report noted that about 40 percent of U.S. underground storage tanks show leaks, which can add $20,000 to $100,000 in due diligence and cleanup costs per site and lead traditional banks to reject many gas station loans, according to CRELender’s gas station financing summary. That’s not a side issue. It can determine whether the lender proceeds at all.

Borrowers often assume a busy operating station must be financeable. That’s false. A site can produce cash and still fail credit because contamination risk changes the collateral picture, the closing timeline, and the lender’s exit options if the loan goes bad.

Phase I and Phase II are not the same thing

A Phase I Environmental Site Assessment is the initial screen. It reviews records, site history, and visible conditions. A Phase II goes further and tests soil or groundwater when the first review raises enough concern to justify deeper investigation.

That distinction matters in practice.

- Phase I can uncover risk indicators: prior releases, neighboring contamination, old tank issues, or inconsistent records.

- Phase II can confirm or clear the concern: the file either strengthens or becomes far more complicated.

- A clean report has financing value: it can support lender comfort and reduce friction in underwriting.

- A problematic report changes everything: pricing, reserves, cleanup responsibility, and sometimes the viability of the transaction itself.

Underwriting reality: Environmental reports are not paperwork. They are credit documents.

A short explainer on site investigation can help if this is your first transaction:

How environmental findings change loan terms

If the file comes back clean, the lender can focus on normal credit issues. If contamination appears, several things can happen. The lender may require remediation plans, added documentation, reserves, different collateral assumptions, or decline the deal. Even when financing remains possible, environmental uncertainty usually weakens your negotiating position.

Some SBA-backed structures can cover eligible environmental assessment and cleanup costs in certain situations. That can keep a transaction alive when a conventional lender won’t touch it. But borrowers should not mistake that flexibility for leniency. The reports still have to support a financeable outcome.

The practical move is simple. Order the environmental work early, review it with counsel and your lender, and never commit hard money to a station before you know what the ground and tank history may cost you.

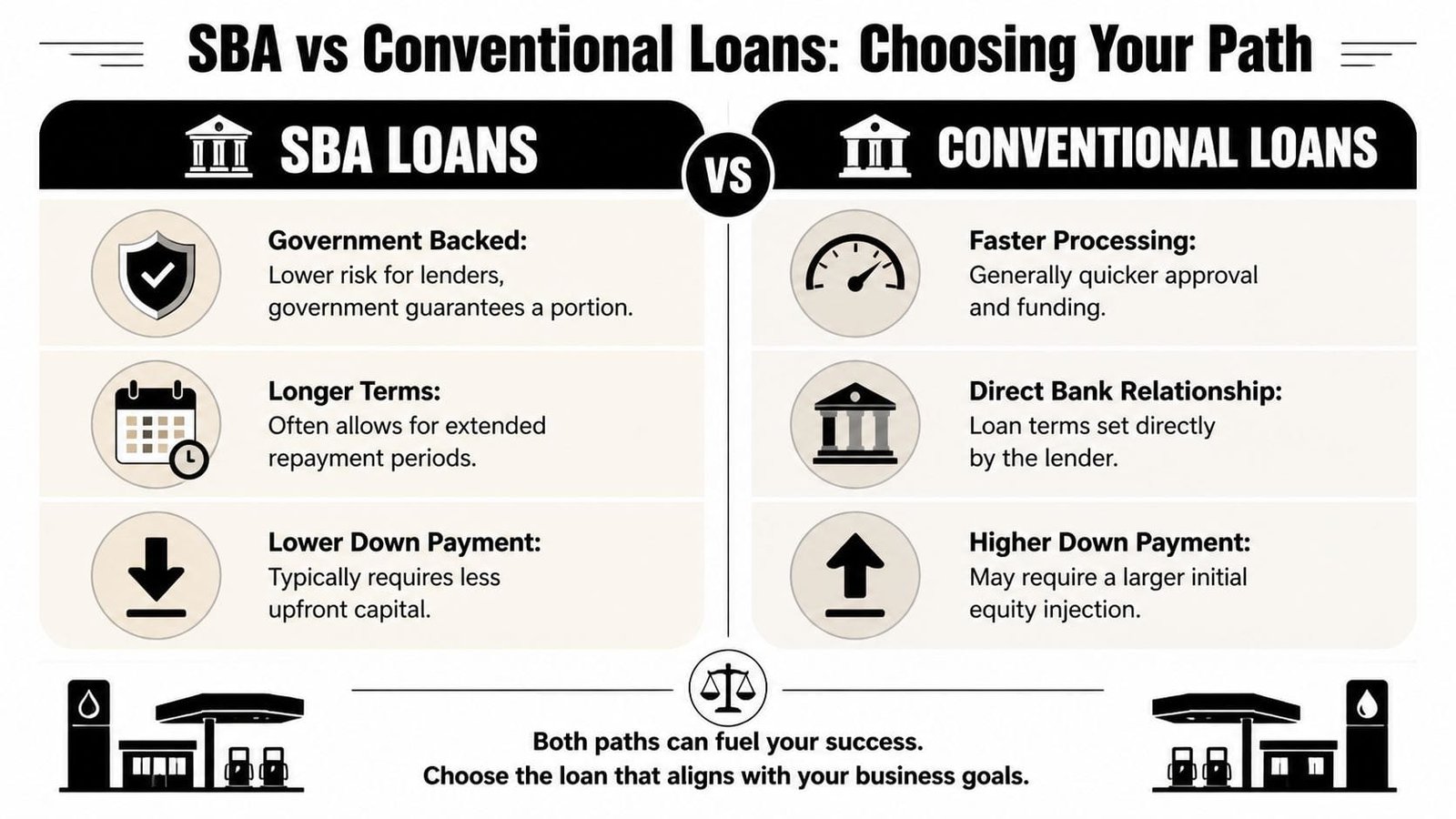

SBA vs Conventional Loans Choosing Your Path

A buyer can qualify on paper, agree on price, and still choose the wrong loan structure for the deal. I see that happen most often when the borrower focuses only on rate and down payment, while the pressure points are closing speed, cash reserves after closing, and how the lender reacts if the environmental file raises follow-up questions.

When SBA is the smarter play

SBA financing usually fits buyers who need to conserve cash, stretch repayment over a longer period, or combine several business purposes into one loan. That can include real estate, business acquisition, equipment, and working capital. For first-time or early-stage operators, that flexibility often matters more than getting the absolute simplest structure.

SBA is often the better fit when:

- You want to keep more cash available after closing

- The deal includes multiple uses of proceeds

- You are buying your first station or expanding from one to two sites

- The transaction is sound, but a bank’s conventional credit box feels too tight

SBA can also be the better path when environmental diligence is clean enough to support financing, but the file still carries some complexity. A conventional bank may hesitate if the reports require extra review, tank documentation is incomplete, or prior site history needs legal clarification. An SBA lender may have more room to structure around that complexity, provided the risk is understandable and the borrower has a credible plan.

Borrowers who need context on program fit can review this comparison of SBA 7(a), 504, and microloan options for small businesses.

When conventional financing makes more sense

Conventional financing tends to reward strong sponsors and cleaner deals. If you have meaningful liquidity, solid station-level cash flow, experience in fuel retail, and a property with straightforward environmental history, a conventional loan can be faster and less layered.

That speed matters. Sellers get impatient. Franchise approvals have deadlines. Fuel supply changes can affect margins if closing drags out.

Conventional also works well when the transaction is simple. One borrower. One site. Clear financials. Clean reports. Adequate cash injection. In that case, the bank may move more directly than an SBA process with extra forms, eligibility review, and government-driven documentation.

The trade-off many buyers miss

The wrong comparison is “SBA is easier, conventional is harder.” A more apt comparison is flexibility versus strictness.

SBA financing usually gives more room on equity and structure. Conventional financing usually gives more room on speed if the file is clean. Environmental diligence can tip that decision quickly. A bank that likes the deal today may tighten terms tomorrow if a Phase I recommends more work or if an old tank closure raises unanswered questions. In those cases, the borrower who chose conventional because it looked faster can end up losing more time than expected.

I tell clients to decide based on the deal’s bottleneck. If cash to close is tight, SBA often solves the immediate problem. If time is tight and the file is clean, conventional may be the better answer. If the environmental history is anything less than straightforward, assume that loan structure and lender appetite will matter as much as rate.

A practical way to decide

Use this filter before you start sending the file around:

- Choose SBA if preserving liquidity matters more than getting to the finish line as fast as possible.

- Choose SBA if the loan needs to cover real estate, business value, equipment, and operating cushion in one package.

- Choose conventional if you can handle a larger equity requirement without draining reserves.

- Choose conventional if the station, borrower, and environmental file are all clean enough to support a direct bank credit decision.

- Reconsider both options early if environmental review is still incomplete, because terms and lender interest can change once the reports are in.

Good borrowers do not shop loan types in the abstract. They match the structure to the station, the site history, and the amount of risk the lender will accept.

Your Application Roadmap From Checklist to Closing

Good gas station loan files don’t happen by accident. They’re assembled. The smoother applications usually come from borrowers who treat underwriting like an audit before the lender does.

What to gather before you apply

Start with the documents that prove both repayment ability and site legitimacy.

Business and personal tax returns

Lenders use these to anchor the story in filed numbers, not seller optimism.Current financial statements

P&L, balance sheet, and debt schedule should tie together. If they don’t, fix that first.Purchase contract or letter of intent

The lender needs the terms, timing, and assets included in the transaction.Fuel supply or franchise agreements

These can affect assignability, margins, and operational continuity.Environmental reports and compliance documents

If they already exist, produce them early. If they don’t, prepare for that work immediately.Business plan and projections

Keep these grounded. Lenders respect disciplined assumptions more than aggressive upside.

For a broader borrower-facing checklist, this guide to business loan applications is a practical reference.

What the timeline usually feels like

The timeline depends on loan type and deal complexity. SBA files can take longer because they require more documentation and more review steps. Environmental review and appraisal often determine the pace more than the borrower expects.

That said, some project-specific financing can move faster. For major projects such as EV charger installations, combining financing with incentives like the 30C tax credit and pairing it with an SBA 7(a) loan can cut time-to-fund to under 30 days and reduce project payback to less than 3 years, according to the Douglas County economic development lending document.

How to keep the deal moving

A few habits make a real difference:

- Answer lender questions once, with backup: incomplete replies create repeat requests.

- Coordinate your professionals early: accountant, attorney, broker, and consultant should all work from the same file.

- Flag weak spots yourself: if there’s a dip in performance or a site issue, explain it before underwriting has to ask.

- Separate must-haves from nice-to-haves: don’t overload the initial package with distractions.

If you need a platform that combines application intake, SBA processing support, dashboard tracking, and access to products such as lines of credit, equipment financing, merchant cash advances, and acquisition loans, Business Loan Warrior is one option in the market.

The biggest application mistake is passivity. Borrowers who wait for the lender to discover every issue usually lose time and bargaining power.

Common Pitfalls and Alternative Funding Sources

Most bad gas station loan outcomes start before the closing. The borrower either overestimates the station’s resilience or underestimates the capital the business will keep demanding after acquisition.

Mistakes that cost borrowers approvals

A few patterns show up repeatedly.

- Overreliance on fuel margin: if the business has weak inside sales, lenders get less comfortable with volatility.

- Underbudgeting the first year: repairs, inventory, and compliance items don’t wait until cash flow feels convenient.

- Weak market analysis: traffic patterns, nearby competition, and local demand still matter, even when the seller says the station has always performed.

- Ignoring site condition: buyers may notice aesthetics but miss equipment age, deferred maintenance, or environmental records.

Borrowers also make the mistake of trying to force one long-term loan to carry every need. Acquisition debt should not become a catch-all substitute for working capital planning.

When alternative funding actually helps

Alternative products are useful when they solve a narrow problem cleanly.

- Line of credit: good for short-term cash flow gaps, fuel purchases, and operating swings.

- Inventory financing: useful if you’re building out the c-store and don’t want to drain operating liquidity.

- Equipment financing: cleaner for replacing pumps, POS systems, or similar assets.

- Merchant cash advance: sometimes appropriate for an urgent repair when speed matters more than cost.

The key is discipline. Alternative funding works when it fills a temporary operational need. It becomes dangerous when it props up a station that never had enough cash flow to support the acquisition in the first place.

Frequently Asked Questions About Gas Station Financing

Can you get gas station loans without prior station ownership experience

Yes, but the burden of proof gets higher. Lenders usually want confidence that operations won’t fall apart after closing. If you don’t have direct experience, bring in experienced management, a credible operating plan, and clean financial support for the deal.

What down payment should you expect in practice

That depends on the loan type and the transaction. SBA-backed structures are often attractive because they can require less cash down than conventional loans. The exact requirement still depends on the file, collateral, and lender judgment.

Can you finance a station without a convenience store

You can, but the file may be less attractive if revenue depends too heavily on fuel alone. Lenders usually prefer diversified income streams because they strengthen repayment durability.

How is the EV transition affecting approvals

The shift is already influencing lender behavior. Stations that diversify and add EV charging are seeing stronger financing treatment. For example, SBA 504 approvals for hybrid sites were up 22 percent in Q1 2026, according to Greenbox Capital’s write-up on gas station funding and EV diversification. Lenders increasingly view mixed-revenue sites as more resilient than pure fuel plays.

Can environmental problems be financed around

Sometimes, but not casually. Certain SBA-backed structures may help with eligible assessment or remediation-related costs in the right circumstances. That doesn’t remove the need for a financeable environmental outcome. If the reports are ugly enough, the deal can still die.

What should a buyer do first

Get the documents before you get emotionally committed. That means financials, fuel agreements, and environmental history early. The fastest way to waste time on a gas station acquisition is to negotiate price before you understand site risk.

If you're weighing acquisition financing, a refinance, equipment funding, or a working-capital backstop for a gas station business, Business Loan Warrior lets you start with one application, review appropriate options, and see whether an SBA-backed or alternative structure fits the deal without adding unnecessary friction to the process.