You win the contract, then the main problem shows up. The job needs an excavator, loader, crane, or specialized trailer capacity your current fleet can't cover, and paying cash would gut working capital right when payroll, fuel, materials, and mobilization costs are ramping.

That's where heavy equipment loans stop being “just debt” and start acting like a production tool. In construction and logistics, the machine is often the revenue engine. If the financing is built around how that machine earns, how fast it depreciates, and when your projects convert into cash, the loan can support growth. If it's built only around headline rate, it can pin your balance sheet under an asset that no longer matches your operation.

A lot of owners make the same mistake. They compare offers like they're buying a commodity. Lowest rate wins. But heavy equipment loans work best when term, down payment, collateral value, and operating cycle line up. The right structure keeps your cash available for crews and contingencies. The wrong one leaves you making payments on a machine that's underused, underwater, or expensive to keep compliant.

Table of Contents

- Introduction The Growth Dilemma

- How Heavy Equipment Loans Power Your Business

- Choosing Your Financing Vehicle Loan and Lease Options

- Unlocking the Best Rates and Terms

- The Strategic Decision Loan vs Lease In-Depth

- Your Heavy Equipment Loan Application Checklist

- Making the Final Decision with a Trusted Partner

Introduction The Growth Dilemma

The strongest companies usually feel this squeeze at the same moment. Revenue opportunity is there, backlog looks healthy, but the next phase of growth requires iron in the field now, not after cash accumulates.

Heavy equipment loans solve that timing problem by letting the asset help pay for itself over time. In plain terms, the lender advances funds to buy the machine, and the equipment serves as collateral. That structure matters because it ties the credit decision to a tangible asset with resale value, not just to a general promise to repay.

For a contractor or logistics operator, that provides an advantage in the good sense of the word. You preserve liquidity for hiring, fuel, insurance, bonding support, and change-order delays while still putting productive equipment to work.

Practical rule: Treat a heavy equipment loan like a project scheduling decision. The machine, the contract timeline, and the repayment schedule all have to fit together or the whole job gets harder.

The trap is financing a productive asset with a structure that ignores how your business collects cash. A machine used on long-cycle civil work needs a different repayment rhythm than one used on shorter-turn site packages or recurring haul contracts. The best loan is the one that matches useful life, utilization pattern, and the periods when receivables clear.

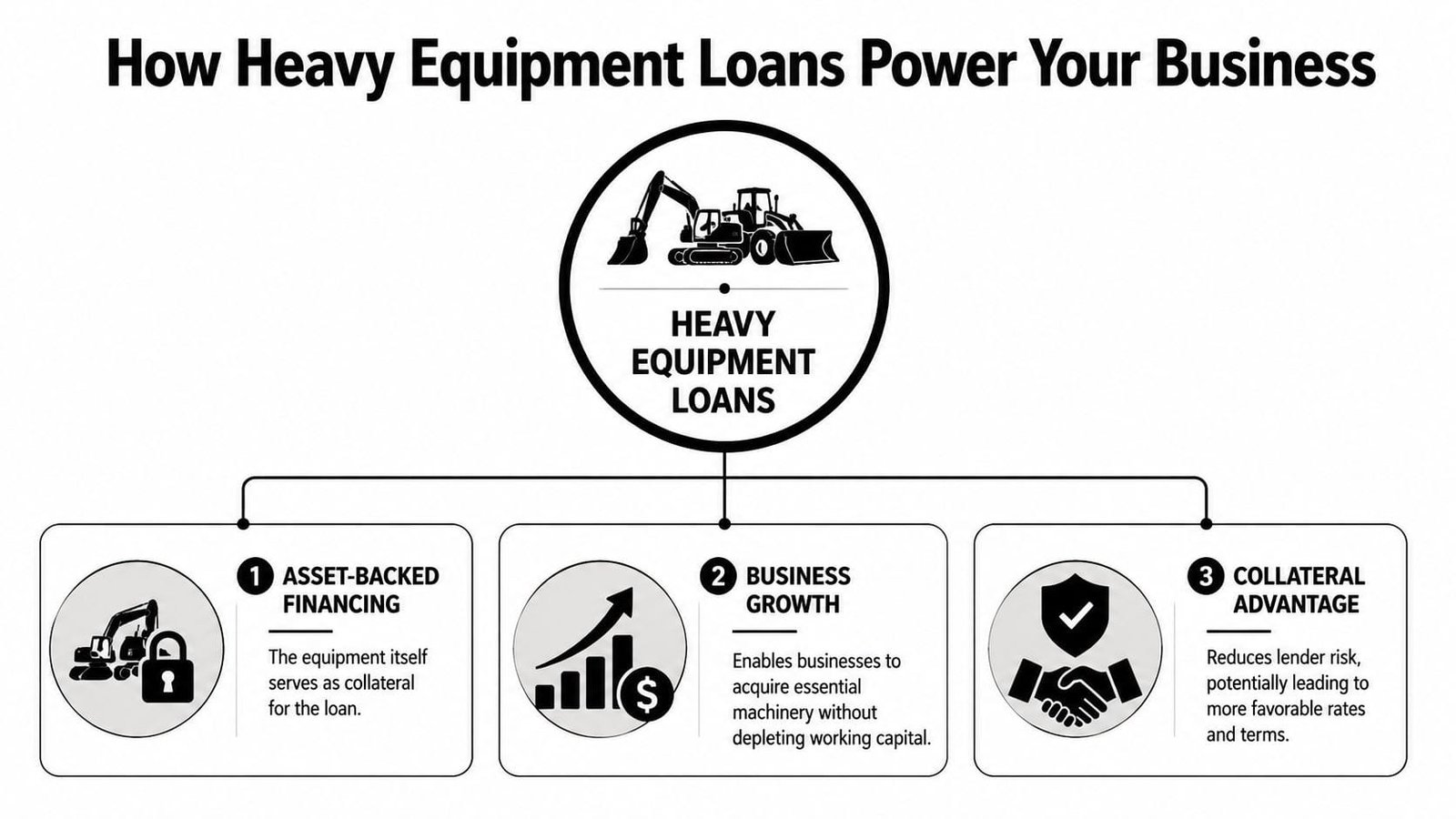

How Heavy Equipment Loans Power Your Business

Heavy equipment financing isn't niche anymore. The construction equipment finance market was estimated at USD 94.27 billion in 2024 and is projected to reach USD 157.26 billion by 2033, with loans and term loans holding a 34.7% revenue share. That tells you how central this product has become for companies that need productive assets without draining operating cash.

Early in the process, it helps to visualize what the lender is really underwriting.

Why this financing category matters

A heavy equipment loan works a lot like a mortgage on a business asset. The lender has collateral. You get control of the equipment. The machine goes to work immediately, and repayment happens over time from the revenue capacity it creates.

That's why owners in capital-heavy industries rely on it. Paying cash for every excavator, paver, dozer, crane attachment, or fleet trailer may feel conservative, but it can create a different problem. You become asset-rich and cash-poor right when jobs demand flexibility.

Three practical benefits stand out:

- Preserved working capital: You keep cash available for labor, mobilization, repairs, and surprises that always show up mid-project.

- Better alignment with earning power: The machine starts generating billable output before you've fully paid for it.

- Collateral-based underwriting: Because the lender can secure the loan with the equipment, approval and structure often make more sense than a general unsecured request.

A lot of business owners make financing decisions as if the equipment purchase is separate from operations. It isn't. If the machine expands capacity, protects a margin-rich contract, or eliminates chronic rental costs, financing isn't just a way to “afford” it. It's part of your operating model.

Here's a quick explainer if you want a visual walk-through of the category and how lenders think about these loans.

What makes equipment debt different

The biggest difference between heavy equipment loans and plain working capital debt is the relationship between asset life and loan life. Good equipment financing is built around that relationship. Bad financing ignores it.

In practice, strong structures usually do four things well:

- Match amortization to useful life so you're not still carrying large balances after the asset's productivity has faded.

- Respect your cash conversion cycle so payments don't fight your billing pattern.

- Leave room for maintenance and compliance costs because ownership never stops at principal and interest.

- Protect optionality in case you need to trade, refinance, or rotate the asset earlier than expected.

The monthly payment matters. The timing of that payment against utilization and receivables matters more.

Choosing Your Financing Vehicle Loan and Lease Options

Not every equipment need should be financed the same way. The right product depends on whether you want ownership, flexibility, tax treatment, balance sheet control, or the lowest operational friction. Start with the equipment's role in the business. Is it core fleet, seasonal capacity, or a short-window contract requirement? That answer usually narrows the field fast.

Traditional equipment term loans

This is the standard buying structure. You borrow against a specific machine, take title, and repay over an agreed term while the asset serves as collateral.

This option tends to fit businesses that know the equipment will stay busy and remain central to operations. If the machine is a core production asset, owning it often gives you more control over scheduling, modifications, maintenance standards, and eventual resale.

What works:

- Long-use assets: Machines you expect to keep working for years.

- Fleet standardization: Equipment that fits your existing operator training and service model.

- Equity building: You want residual value instead of handing the asset back at term-end.

What doesn't:

- Rapidly changing specs: If technology or contract requirements shift fast, ownership can trap you in yesterday's machine.

- Uncertain utilization: If the work pipeline is uneven, fixed debt can outlast demand.

SBA-backed structures

SBA-backed financing can be useful when a conventional equipment request doesn't fit cleanly or when the transaction includes more than just the machine. These structures are often considered when a borrower wants longer support around a broader growth plan, not only a narrow piece-of-equipment advance.

For established companies, the appeal is usually flexibility. If the purchase is part of expansion, a facility upgrade, or a wider capital stack, SBA-backed options may provide a better fit than a single-asset note.

The trade-off is process. More flexibility usually means more documentation, more underwriting layers, and less speed than a straightforward equipment lender can offer.

Equipment leases

Leasing is best understood as paying for use rather than building ownership. That can be a very smart move when the asset's productive window is shorter than its useful life, or when the equipment category changes quickly enough that resale risk belongs with someone else.

A lease may fit if:

- You need lower upfront pressure and want cash preserved for deployment.

- The equipment is tied to a defined contract term and may not stay busy afterward.

- You want upgrade flexibility rather than a long ownership tail.

If you're evaluating low-cash-entry structures, this guide on zero-down equipment financing helps frame when preserving cash is smart and when it merely postpones cost.

Sale-leaseback and working capital release

A sale-leaseback lets you access capital from equipment you already own. You sell the asset to a financing company, then lease it back so operations continue uninterrupted.

This can help when the fleet is solid but cash is tied up in iron instead of available for growth. It's often a useful move for companies carrying valuable equipment but facing expansion costs, seasonal working capital gaps, or a need to clean up more expensive debt elsewhere.

The caution is simple. Don't use sale-leaseback to patch a recurring operating loss. It's a balance sheet tool, not a cure for weak margins.

How lenders actually sort the file

Owners often think product choice is separate from underwriting. It isn't. Lenders sort files by a few practical questions:

| Underwriting factor | Why the lender cares | What it changes |

|---|---|---|

| Equipment type | Some machines hold value better and sell faster | Advance rate and term comfort |

| New or used | Used equipment carries more valuation risk | Down payment and appraisal scrutiny |

| Revenue quality | Contracted, diversified cash flow is easier to trust | Structure and speed |

| Time in business | Operating history reduces execution risk | Approval path |

| Existing debt load | Lenders test whether payments can be absorbed | Monthly payment tolerance |

A lender isn't only asking, “Can this borrower pay?” They're also asking, “If the plan changes, can this asset protect the loan?”

That's why two offers with similar rates can behave very differently in practice. One may give you room to operate. The other may be cheaper on paper but tighter where it counts.

Unlocking the Best Rates and Terms

Strong pricing usually goes to borrowers who make the lender's risk easy to understand. Not by talking more, but by showing clean cash flow, realistic utilization, and a loan structure that respects the machine's life.

Typical heavy equipment loan terms run 3 to 7 years, lenders often look for a DSCR above 1.25x, and down payments around 20% for new equipment are common. Those numbers matter, but they don't tell the whole story. The deeper issue is fit. A cheap payment on the wrong term can be more dangerous than a slightly higher payment on a cleaner structure.

What lenders want to see

Lenders look for evidence that the machine will produce enough value to support repayment without squeezing the rest of the company. They also want confidence that the collateral will still protect them if they need a second exit.

Bring them a clean package built around these points:

- Cash flow strength: Show that the business can absorb the payment even if one project slips.

- Asset fit: Explain where the machine works, how often, and whether it replaces rental spend or expands capacity.

- Down payment discipline: Equity in the deal tells the lender you're not asking them to carry all the risk.

- Collateral quality: Newer, well-documented equipment is easier to finance than vague descriptions of a used unit from a private seller.

If you're comparing lender types, this practical guide to commercial equipment lenders and rate structures helps clarify how lender appetite affects terms, not just pricing.

When a loan beats a lease

A loan is usually strategically better when the equipment is central to the company's long-term production model. If you know the machine will stay utilized, ownership gives you control and future value.

Choose a loan when:

- You want the asset on your side of the ledger because it's part of core capacity.

- You expect a long service life and can align repayment to that life.

- You care about resale or trade flexibility later and don't want contractual return conditions.

A loan also makes more sense when maintenance practices are already disciplined in-house. If your shop keeps machines in strong condition, you're more likely to protect residual value.

When a lease is the smarter move

Lease logic wins when uncertainty is high. If the machine is tied to one contract, one customer, or one temporary service line, renting the use of the asset may be better than owning the risk.

Consider a lease when:

- Your backlog is strong but concentrated and you don't want long-tail ownership if the work mix changes.

- The asset category evolves quickly and upgrading matters more than equity.

- You want to limit balance sheet drag from equipment that may become non-core.

Buy the machine when ownership strengthens the business. Lease it when flexibility strengthens the business.

The rate conversation only gets useful after you answer that question.

The Strategic Decision Loan vs Lease In-Depth

The loan-versus-lease decision gets expensive when owners reduce it to monthly payment. That's the wrong lens. The key question is which structure best matches the asset's value curve, your contract timeline, and the company's appetite for ownership risk.

A key danger is term mismatch. Heavy equipment loans often run 24 to 72 months, while used construction machinery can lose 15% to 25% annually, which can leave a borrower underwater if the balance declines more slowly than the asset value. That one issue changes refinancing options, sale options, and negotiating power if your operating plan shifts.

Heavy Equipment Loan vs. Lease Comparison

| Factor | Equipment Loan (Buying) | Equipment Lease (Renting) |

|---|---|---|

| Ownership | You own the equipment | Lessor owns the equipment |

| Upfront cash | Often higher because equity is expected | Often lighter at the start |

| Long-term value | You keep residual value if maintained well | Residual value usually stays with lessor |

| Flexibility at end of term | Sell, trade, or keep using | Return, renew, or transition depending on contract |

| Depreciation risk | Yours to manage | Shifted partly or largely away from you |

| Maintenance discipline | Directly affects your asset value | Still important, but end-of-term conditions drive cost |

| Best use case | Core fleet with predictable utilization | Contract-tied or fast-changing equipment needs |

The biggest strategic divide is residual risk. If you buy used equipment with a steep depreciation curve and stretch payments too long, your balance sheet can get pinned under an asset worth less than the debt against it. Leasing can help avoid that. On the other hand, if the machine is stable, proven, and heavily used, a lease can become an expensive way to avoid ownership.

A practical pre-flight check

Before choosing either route, gather these items and review them like a flight checklist:

Vendor quote or purchase order

Lenders and lessors need to know exactly what asset they're underwriting, including model, age, condition, and configuration.Utilization plan

Write down where the machine will work, how often, and whether it replaces rentals, adds capacity, or protects a contract award.Maintenance plan

A lender gains confidence when you can show who services the equipment, where records live, and how downtime risk is handled.Exit plan

Many borrowers get sloppy in this area. If the work changes in year two or three, can you redeploy, refinance, sell, or trade the equipment without taking a hit that damages the rest of the company?

Don't choose a structure because it closes fastest. Choose it because it still works if the original operating plan changes.

Tax treatment matters too, but it should follow strategy, not replace it. Ownership may support depreciation-based planning, while lease payments may fit cleaner as operating expense. Your CPA should model that after you've identified which structure suits the asset and the cash cycle.

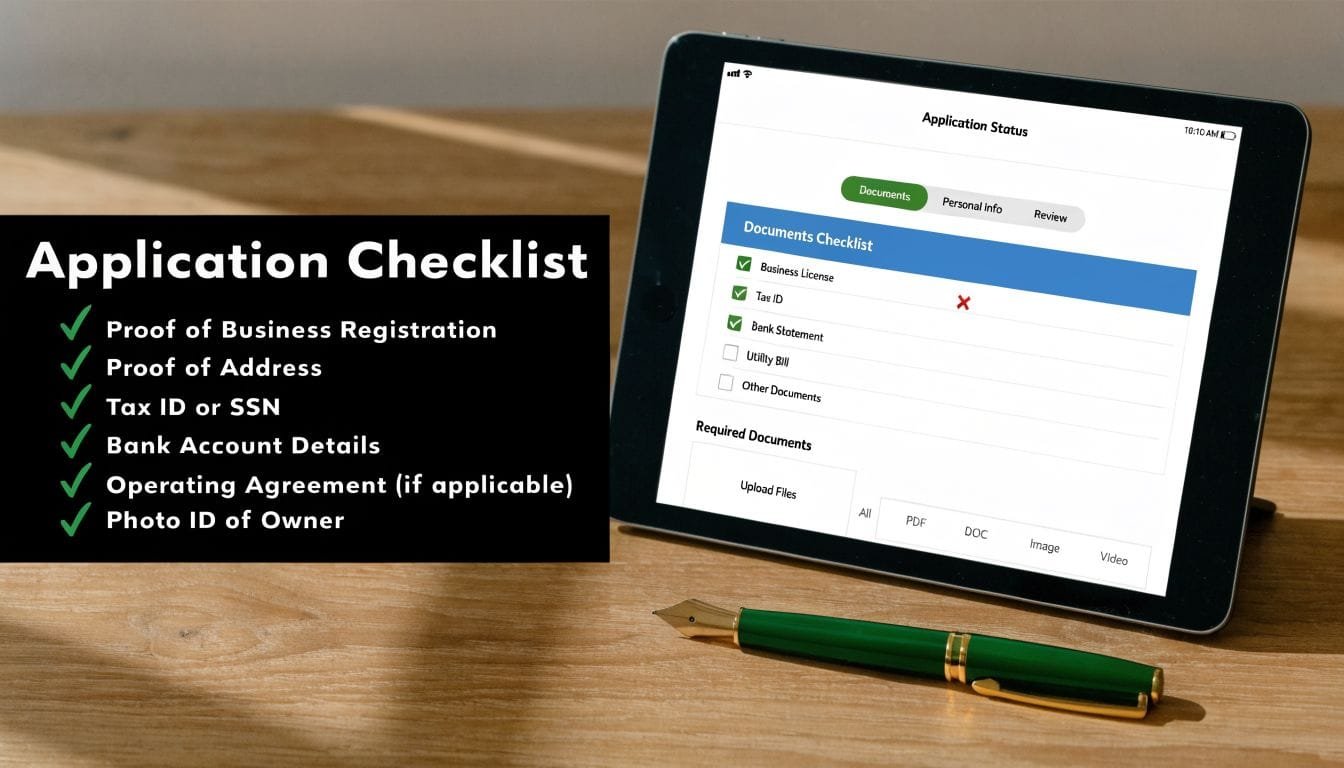

Your Heavy Equipment Loan Application Checklist

A heavy equipment loan application moves faster when the file tells a coherent story. Lenders don't just want paperwork. They want confidence that the borrower understands the asset, the operating plan, and the total cost of carrying it.

For new equipment, lenders often finance 80% to 100% of cost, while used equipment often finances at 50% to 70% of value. A certified appraisal that verifies condition and usage hours, with under 5,000 hours viewed favorably, can help improve loan-to-value and reduce down payment needs from 30% to 50% toward 10% to 20% in some cases. That makes document quality more than an admin issue. It can change structure.

The documents that move approval faster

Use this list before you submit anything:

- Equipment quote or invoice: This anchors the request to a specific asset. Generic requests slow everything down because the lender can't assess collateral properly.

- Certified appraisal for used equipment: Especially important for older or specialized machines. This helps establish value, condition, and financeability.

- Recent financial statements: A current profit and loss statement and balance sheet show whether the business can carry the payment without stressing operations.

- Business tax returns: These validate revenue history and smooth out any seasonality or one-off swings in internal statements.

- Bank statements: Lenders use them to confirm liquidity patterns and operating discipline.

- Debt schedule: Existing obligations matter because equipment debt has to fit into the whole capital stack.

- Ownership and entity documents: This prevents avoidable closing delays.

- Project or contract context: If the machine supports a specific backlog need, say so clearly. Underwriters understand machines better when they can tie them to actual work.

If you're preparing a full package, this step-by-step guide to business loan applications is a useful reference for tightening your file before underwriting sees it.

Why total cost matters before you sign

A clean approval can still turn into a bad deal if you underwrite only the note and ignore the asset's operating burden. The smartest borrowers build a total-cost view before they commit.

That means asking:

- What does insurance require?

- What maintenance cadence does the lender expect?

- Are there usage restrictions, tracking requirements, or reporting obligations?

- How will transport, storage, licensing, and downtime affect actual carrying cost?

A machine that looks affordable on paper can become expensive if compliance and upkeep aren't budgeted from day one.

Approval is not the finish line. It's the start of a multi-year operating commitment tied to a piece of equipment that needs cash, attention, and discipline.

Making the Final Decision with a Trusted Partner

The final decision shouldn't come down to rate alone. It should come down to whether the structure helps the company grow without boxing it into the wrong asset, the wrong payment pattern, or the wrong ownership burden.

That's why total cost of ownership has to sit next to interest rate in every serious review. Standard equipment financing discussions often leave out downstream insurance, maintenance, and compliance obligations, even though those costs can add 8% to 15% to the true cost of capital. If those obligations aren't visible up front, the cheapest quote may not be the cheapest decision.

A good financing partner does more than send term sheets. They help pressure-test the file, the asset, and the operating assumptions behind the request. They ask the questions an experienced owner should want asked anyway:

- Does the term match the machine's real working life in your fleet?

- Will the payment schedule fit your billing and collection cycle?

- Are you buying capacity or just buying pressure relief?

- If the contract mix changes, what's your exit path?

The best heavy equipment loans act like a growth tool. They put productive assets to work without stripping liquidity from the rest of the business. The wrong ones create a second job for ownership. Managing debt that never should've been structured that way in the first place.

Choose the structure that still makes sense after the excitement of the equipment purchase wears off. That's usually the one built around utilization, residual value, and total ownership cost, not the one with the flashiest quote.

If you're ready to compare heavy equipment loans with a clearer view of term fit, cash flow timing, and total cost, Business Loan Warrior gives you a practical place to start. You can review suitable options through one application, check pre-approval without affecting credit, and evaluate offers with more context than a simple rate comparison.