You're probably in one of two spots right now. Either your lender asked for financials and you realized you're not fully sure which number counts as your real profit, or you've got money moving through the business but your bottom line still feels blurry.

That's common. Owners often know sales, payroll, and the bank balance. Then the loan application asks for net income, and suddenly the question changes from “How much cash do I have?” to “How profitable is this business after everything?” Those are not the same question, and lenders know it.

For a loan file, net income is more than an accounting line. It's one of the clearest signals of whether the business can carry debt without strain. If you know how to find net income, explain it, and present the right adjustments, you make the underwriter's job easier. When you make an underwriter's job easier, approvals tend to move faster and with fewer follow-up questions.

Table of Contents

- Why Your Bottom Line Is Your First Impression with Lenders

- A Step-by-Step Guide to Calculating Net Income

- Common Adjustments Lenders Look For

- Accrual vs Cash Accounting What Lenders Prefer

- How to Present Your Net Income for Loan Approval

- Your Net Income Questions Answered

Why Your Bottom Line Is Your First Impression with Lenders

You send in a loan package on Monday. By Tuesday, an underwriter has already formed an opinion.

That first read usually starts with the income statement, and the line that gets the most attention is net income. It shows whether the business still produces profit after direct costs, overhead, interest, and taxes. For lending, that matters more than a healthy bank balance on a single day.

I see the same mistake all the time in loan files. The owner points to cash in the account. The lender looks past it and asks a harder question. Is the business consistently profitable once the full cost of running it is on the books?

Those are not the same thing.

Cash can rise because a large receivable cleared, inventory purchases got pushed into next month, or owner draws were paused for a short stretch. None of that proves the company can comfortably support new debt. Net income gives the lender a cleaner starting point because it shows whether the operation itself is earning enough after expenses.

It also shapes how the rest of your package is read. Strong revenue with weak net income raises pricing and cost-control questions. Positive net income with messy expense classifications raises credibility questions. Thin profit with large add-backs can still work, but only if the adjustments are documented and reasonable.

What lenders hear from your net income

A lender reads net income as a signal, not just a number. It helps answer questions like:

- Are margins holding up? Sales growth means less if cost of goods or operating expenses are rising just as fast.

- Are expenses controlled? Payroll, rent, software, and discretionary spending all affect how much room is left for debt service.

- Is existing debt already pressuring the business? Interest expense can turn an otherwise solid operation into a tighter credit risk.

- Can these financials be trusted? If the bottom line changes sharply because personal expenses, one-time costs, or owner perks are mixed into operations, the lender will examine the file more closely.

That last point gets missed in generic net income guides. For a loan application, the calculation matters, but presentation matters too. Underwriters want to see the reported figure, then understand any adjustments that make it more representative of ongoing performance.

If you want a broader view of how lenders judge profitability, this guide on what profit margin lenders want to see in small businesses adds useful context.

A lender does not need flawless numbers. A lender needs numbers that tie out, make sense, and hold up under questions.

Businesses get funded faster when owners can show three things clearly: what net income is, what changed it, and which expenses were unusual versus ongoing. That is the difference between handing over statements and presenting a credit case.

A Step-by-Step Guide to Calculating Net Income

Loan files often slow down at the same point. The owner sends over a P&L, the lender spots unclear expense groupings or numbers that do not line up with the reporting period, and the underwriter comes back with questions. Calculating net income correctly helps, but for funding, the bigger win is showing the number in a way that holds up on first review.

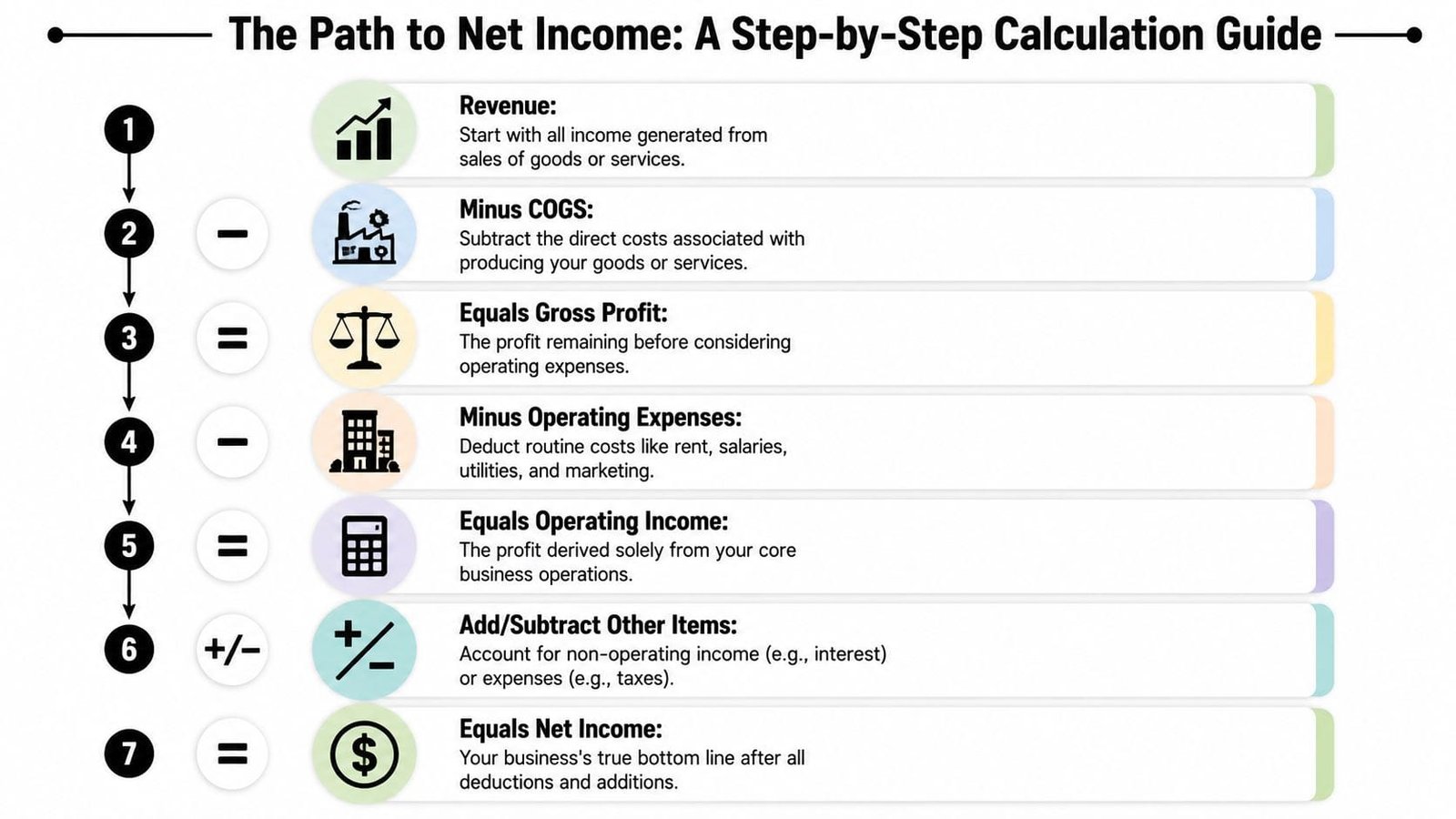

AOFund lays out the cleanest sequence: revenue → gross profit → operating income → pre-tax income → net income, by subtracting COGS, then operating expenses, then non-operating items, then income taxes (AOFund on reconstructing net income from the income statement). That order matters because lenders read the statement in layers. If one layer looks off, they usually do not trust the bottom line that follows.

Start with the income statement, not the bank balance

For a loan application, use the profit and loss statement for the exact period the lender requested. Monthly, year-to-date, and full-year figures each answer a different underwriting question, so mismatched date ranges create avoidable follow-up.

The calculation itself is straightforward:

-

Revenue

Start with income earned during the period shown on the statement. -

Minus cost of goods sold

Subtract direct costs tied to producing goods or delivering services. The result is gross profit. -

Minus operating expenses

Subtract overhead such as rent, administrative payroll, utilities, software, insurance, and marketing. The result is operating income.

Before the final steps, watch this quick walkthrough if you want a visual explanation of how the bottom line flows through the statement.

Work through the layers in order

Then finish the calculation:

-

Add or subtract other income and expenses

This usually includes interest expense, interest income, and other items outside normal operations. The result is pre-tax income. -

Subtract income taxes

What remains is net income.

That is the accounting answer. For lending, presentation matters just as much. Keep the line items separated clearly enough that an underwriter can tell what came from operations, what came from financing, and what may need a second look. If your books lump loan interest, owner benefits, repairs, and office expenses into one broad category, the lender has to recast the statement before they can judge repayment strength.

Here is the fast read underwriters use:

| Layer | What to check | Why it matters for a loan |

|---|---|---|

| Revenue | Consistent sales recognition and period matching | Shows whether reported income is reliable |

| Gross profit | Margin movement from direct costs | Highlights pricing, fulfillment, or production pressure |

| Operating income | Fixed-cost control | Shows whether the business can carry overhead and debt |

| Pre-tax income | Interest burden and unusual items | Separates operating strength from financing drag |

| Net income | Final reported profit | Sets the baseline for repayment analysis |

What helps your number hold up

Clean categories make underwriting easier. Reconciled statements make it faster. A short note for unusual line items can save days of back-and-forth.

I tell borrowers to review the P&L the way a lender will. Check whether the date range matches the request, whether payroll is split correctly between direct labor and overhead, whether interest sits below operating income, and whether owner-related expenses are clearly labeled. If deposits on the bank statements do not roughly support reported sales timing, build a simple bank statement variance tracker for faster SMB approvals before you submit the file.

One more practical step helps. Calculate net income from the P&L, then sanity-check it against what happened in the business during that same period. If sales rose sharply but margins collapsed, or if profit improved only because expenses were deferred, expect questions. It is better to fix classification problems before submission than explain them under deadline.

Practical rule: If a lender cannot understand a line item quickly, they may exclude it, question it, or ask for revised statements.

Common Adjustments Lenders Look For

Generic accounting guides usually stop too early. They show you how to calculate accounting net income, but lenders often look at a more practical version of earnings when deciding how much debt the business can support.

That doesn't mean they ignore your books. It means they ask whether certain expenses reflect ongoing operating reality or just accounting treatment, owner preference, or a one-time event.

Why lenders adjust accounting profit

Rippling's explanation gets to the heart of it: net income can mislead people about cash flow because it's an accrual-based profitability metric, not a cash measure, and it includes non-cash charges like depreciation while excluding cash timing effects. That distinction matters because loan decisions often depend on cash generation, not just reported profit (Rippling on why net income can be misleading for cash flow).

That's why underwriters look for add-backs or adjustments. They want to know what the business earned under normal operating conditions and what cash may be available for debt service.

Your accounting net income isn't always your lending net income.

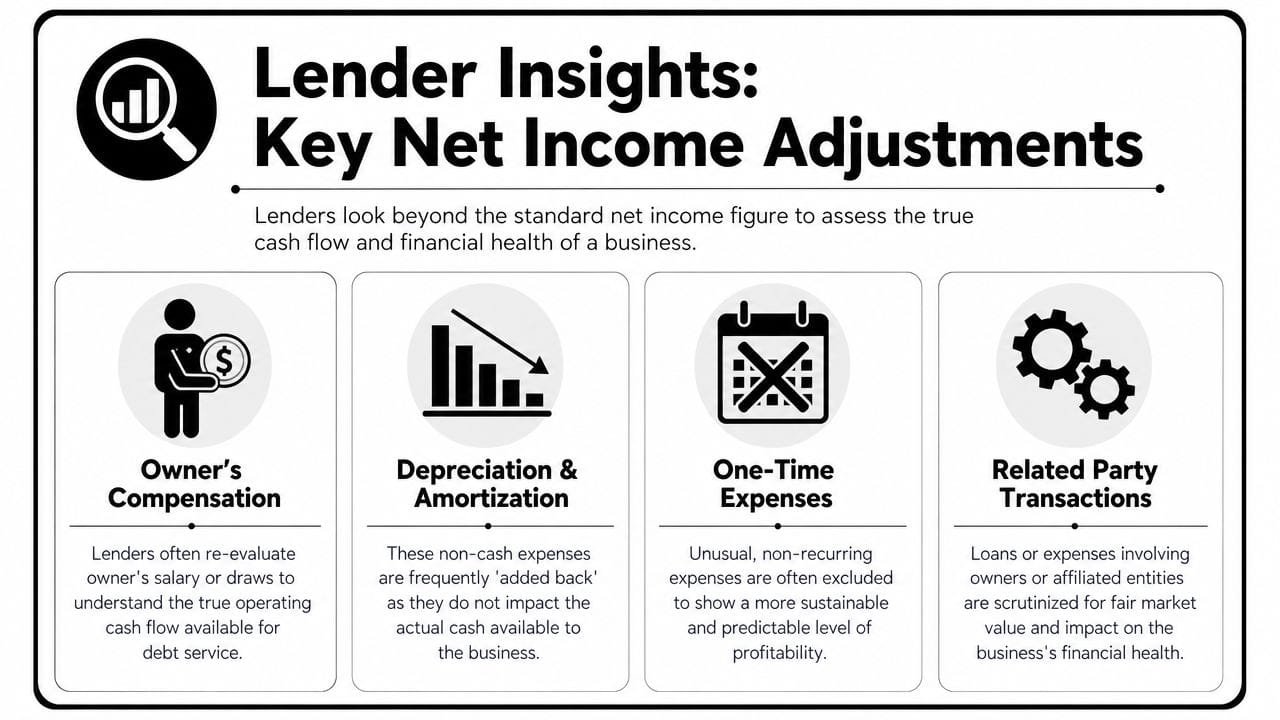

Adjustments that get attention fast

Some adjustments are common and legitimate. Some are overstated by borrowers and quickly challenged. The difference is documentation.

-

Depreciation and amortization

These are non-cash charges. Lenders often isolate them because they reduce accounting profit without representing a current-period cash outflow. That said, don't assume every lender treats them the same way for every product. -

Owner's compensation

If an owner pays themselves above what a replacement manager would reasonably cost, a lender may normalize that line. If the owner underpays themselves, the lender may go the other way and add a management expense back in. Either way, they're trying to see the business as an ongoing operation, not as a tax strategy. -

One-time expenses

Large legal bills, unusual repairs, relocation costs, cleanup costs after an isolated event, or a one-off consulting project can be candidates for adjustment if they are demonstrably non-recurring. “We don't expect this again” is not enough. You need support. -

Related-party transactions

Rent paid to an entity owned by the same principals, management fees, family payroll, or intercompany charges get scrutiny fast. Underwriters want to know whether those amounts reflect market reality or discretionary owner behavior.

A clean support package often includes:

- A simple adjustment schedule that starts with book net income and shows each proposed add-back on its own line.

- Backup documents such as invoices, lease agreements, payroll reports, or general ledger detail.

- A bank-activity check to make sure the adjusted story still aligns with actual inflows and outflows. A disciplined bank statement variance tracker for faster SMB approvals can help surface questions before the lender raises them.

The weak approach is trying to “add back” normal ongoing expenses just because they hurt profit. If the business regularly incurs the cost, lenders usually won't pretend it doesn't exist.

Accrual vs Cash Accounting What Lenders Prefer

A lender can decline a file even when the business is profitable on paper, because the timing in the financials makes the earnings hard to trust.

Take a contractor that finishes work in December, invoices at year-end, and gets paid in January. On a cash-basis P&L, that revenue shows up in January. On an accrual-basis P&L, it belongs in December, when the work was performed. The difference matters because underwriters are trying to judge operating performance for a specific period, not the luck of when checks cleared.

Why lenders usually prefer accrual

Accrual accounting gives lenders a cleaner read on whether the business earned money during the period under review. It matches revenue to the work completed and expenses to the period that generated that revenue. That makes trend analysis easier, especially for businesses with receivables, payables, deposits, progress billing, or uneven vendor payment timing.

Cash-basis reporting is not wrong. It is often practical for running the business day to day. The problem shows up in underwriting. A cash-basis statement can make one month look unusually strong because several customers paid at once, then make the next month look weak even though operations were steady.

Here is how the two methods usually read in a loan file:

| Accounting method | What it shows well | What lenders question |

|---|---|---|

| Cash basis | Actual cash in and out | Whether profit is overstated or understated by collection and payment timing |

| Accrual basis | Period performance | Whether the balance sheet support is accurate and current |

For loan review, accrual usually wins because it connects the income statement to the balance sheet. If accounts receivable are rising, the lender can see why revenue is up but cash has not arrived yet. If accounts payable jumped, the lender can see whether profit was preserved by delaying payments rather than improving operations.

What to do if your books are cash basis

Many small businesses keep internal books on cash basis. That alone does not kill a loan request. What hurts is submitting cash-basis reports without explaining the timing gaps.

The fix is to give the lender a short bridge from cash to accrual. Keep it simple and tied to the reporting period:

- List accounts receivable outstanding at period end so earned revenue is visible.

- List accounts payable so unpaid operating costs are not hidden.

- Separate customer deposits and deferred revenue from earned sales.

- Flag prepaids and large timing items such as annual insurance, bulk inventory buys, or year-end vendor catch-up payments.

- Match the P&L and balance sheet dates so the numbers reconcile.

This presentation does two things. It shows the lender you understand your own financials, and it reduces avoidable follow-up questions from underwriting.

If the gap between profit and cash is wide, include a short explanation and support it with a cash flow forecast that helps your loan strategy. That gives the underwriter a practical answer to the question behind every file: can this business make the payment on time, even when cash timing is uneven?

The strongest approach is consistency. If your tax return is cash basis, your management P&L is accrual basis, and your application form mixes both, expect friction. Pick the reporting logic you are using for the loan file, label it clearly, and show the bridge if needed. That is how a messy set of books becomes a financeable story.

How to Present Your Net Income for Loan Approval

You can have a profitable business and still lose a lender if the file is sloppy. I see this often. The numbers may be fine, but the package leaves the underwriter doing cleanup work, and that usually slows approval or weakens the terms.

Presentation matters because lenders are not judging net income in isolation. They are judging whether the profit is credible, repeatable, and strong enough to support the new payment.

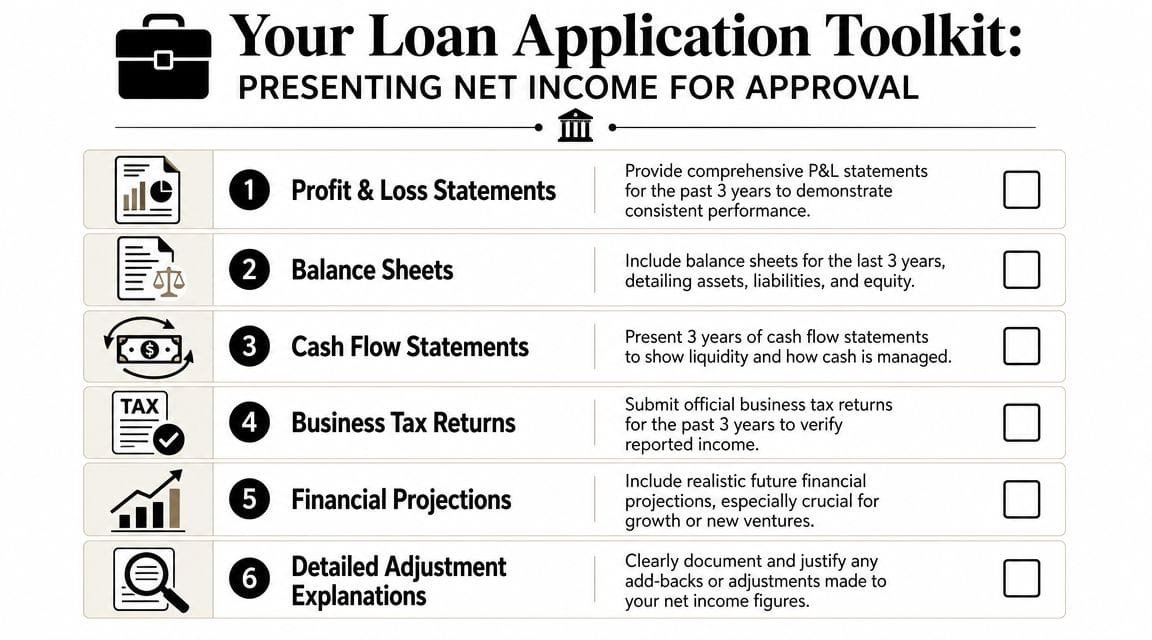

Build a clean lender package

A lender-ready package should let someone unfamiliar with your business understand the story quickly. Start with the core reports, then add only the support that answers likely questions.

Include:

- Profit and loss statements for the last full periods and the current interim period

- Balance sheets dated to match the P&L periods

- Business tax returns if the lender wants third-party verified history

- An adjustment schedule for any add-backs you want considered

- Cash flow support when profit looks acceptable but cash is tight or uneven

The goal is not volume. The goal is alignment.

Names, dates, entity structure, and accounting basis should match across the package. If the tax return shows one entity name, the P&L shows another, and the application uses a trade name with no explanation, underwriting will stop and ask questions. The same goes for reporting periods that do not tie out.

Show adjusted net income the right way

Many generic guides stop too early here. For a loan request, reported net income is only the starting point. Underwriters often review adjusted net income or cash flow to see what the business can support.

That does not mean adding back every expense you dislike. It means separating normal operating costs from items that are clearly one-time, discretionary, or non-cash, then documenting each one.

Common examples lenders examine closely include:

- Owner compensation above market if the business could operate with a lower replacement salary

- One-time legal, repair, relocation, or settlement costs

- Depreciation and amortization

- Personal expenses run through the business

- Non-recurring startup or expansion costs

- Interest expense when the lender is analyzing earnings before debt service

Be careful here. If you add back vehicle expense, meals, and travel every year, an underwriter may treat those as normal operating costs, not exceptions. Add-backs only help when they are reasonable, documented, and tied to the lender's repayment analysis.

Write the short narrative underwriters want

A good credit memo from your side is brief. Three to six sentences is usually enough.

Cover the points that an underwriter will ask anyway:

- What changed in net income

- Why it changed

- Whether the issue is temporary or ongoing

- What management has already done

- What current performance looks like compared with the period on the statements

For example, if profit fell because you replaced equipment, hired ahead of growth, or absorbed a one-time vendor issue, say that plainly and attach support. If margins improved in the most recent quarter, point to the reason. Price increase, lower freight cost, cleaner labor scheduling, better mix. Specific beats vague every time.

A strong loan package explains weak spots before underwriting has to chase them.

One more point. Pair historical net income with a forward-looking cash view so the request looks grounded in repayment capacity, not optimism. A practical cash flow forecast that helps your loan strategy gives the lender a clearer answer to the question behind the file: can this business make the payment on time?

Your Net Income Questions Answered

Can I find net income without a profit and loss statement

Yes, but treat it as a backup method, not your first choice.

Sage notes that if the income statement is unavailable, net income can be inferred from retained earnings using Ending Retained Earnings – Beginning Retained Earnings + Dividends Paid = Net Income. That can be useful for a closed period, but it's sensitive to equity adjustments that are not profits, so it isn't a perfect substitute for the P&L (Sage on inferring net income from retained earnings).

If you use this approach, check for restatements, owner equity entries, and manual journal adjustments before relying on the result.

Is higher net income always better

Not automatically.

A lender likes profit, but they also look at how that profit was produced. Strong net income driven by delayed maintenance, underpaying taxes, or pushing vendors too far isn't reassuring. Lower profit tied to a sensible expansion plan can be easier to explain than unstable profit with no operational discipline behind it.

The cleanest story is durable profitability, supported by orderly books and a credible operating plan.

Do loan payments reduce net income

Partly.

The interest portion of a loan payment typically affects the income statement. The principal portion generally reduces the loan balance on the balance sheet rather than showing up as an expense on the income statement. That's one reason owners can feel squeezed on cash even when net income looks acceptable on paper.

If you're preparing a loan file, separate those two pieces clearly. Lenders notice when borrowers mix them together.

If you want a faster path from messy financials to a lender-ready package, Business Loan Warrior helps business owners move from application to funding with a single no-fee application, customized financing options, and hands-on support that can surface underwriting issues before they slow down approval.