You’re probably looking at a familiar problem. Payroll is due, inventory needs to be restocked, a large customer is paying slowly, or a growth opportunity just opened up and won’t wait for a traditional loan process.

At that moment, most owners want the same thing: access to capital without turning financing into a week-long distraction or risking unnecessary damage to their credit profile. That’s where line of credit pre approval becomes useful. It’s not final funding, and it’s not a blank check. It’s a practical first read on whether a lender is likely to work with you, on what scale, and under what general terms.

For a busy business owner, that matters because financing decisions are rarely made in a calm, perfect quarter. They’re made while you’re still running operations. A good pre-approval process helps you size your options before you commit time to full underwriting.

Table of Contents

- Securing Capital Without the Risk

- Pre-Approval vs Pre-Qualification Explained

- How Lenders Evaluate Your Pre-Approval Request

- The Impact on Your Credit Score

- Your Pre-Approval Preparation Checklist

- From Pre-Approval to Funding What To Expect Next

- Streamline Your Search with Business Loan Warrior

- Frequently Asked Questions

Securing Capital Without the Risk

A supplier needs a deposit by Friday. Payroll hits next week. Two customers are paying late. That is the wrong moment to start hunting for a line of credit.

The safer move is to get clarity before the pressure shows up. A line of credit pre-approval lets you test whether financing is likely to be available while you still have time to compare offers, fix weak spots, and avoid desperate choices. Financing decisions are rarely made in a calm quarter. They happen while you are still running the business.

That early signal has real value. You can check fit, review likely terms, and understand your borrowing range before committing to a full application. For owners comparing lenders, that reduces guesswork and helps protect credit while you shop.

What this looks like in real business use

A pre-approval is useful when:

- You want backup liquidity in place: Many owners apply before they need funds so they are not forced to borrow on a bad week.

- You are comparing line structures: Some businesses benefit from collateral-backed pricing, while others need speed and flexibility. If collateral is part of the decision, review secured vs. unsecured business lines of credit.

- You want a reality check on borrowing power: A pre-approval can show whether your current profile supports the limit you want, before you build plans around money that may not be there.

Here is the part owners often miss. Pre-approval is not the same as final approval. It is an early read based on limited information, and that is where the pre-approval gap starts.

I see this gap most often when the business looks fine at first glance, but the full file tells a different story. Revenue may be acceptable, yet cash flow is inconsistent. The business may show profit, but existing debt payments leave too little room for another monthly obligation. Bank balances may be too thin to handle normal volatility. Those are underwriting issues, not marketing issues, and they are common reasons a pre-approved borrower gets declined later.

Use pre-approval as a readiness tool. If the lender comes back with interest but asks for more documentation, treat that as useful feedback. It tells you what needs attention before final underwriting, especially cash movement, debt service coverage, and liquidity. That is the difference between getting a positive signal and closing the line.

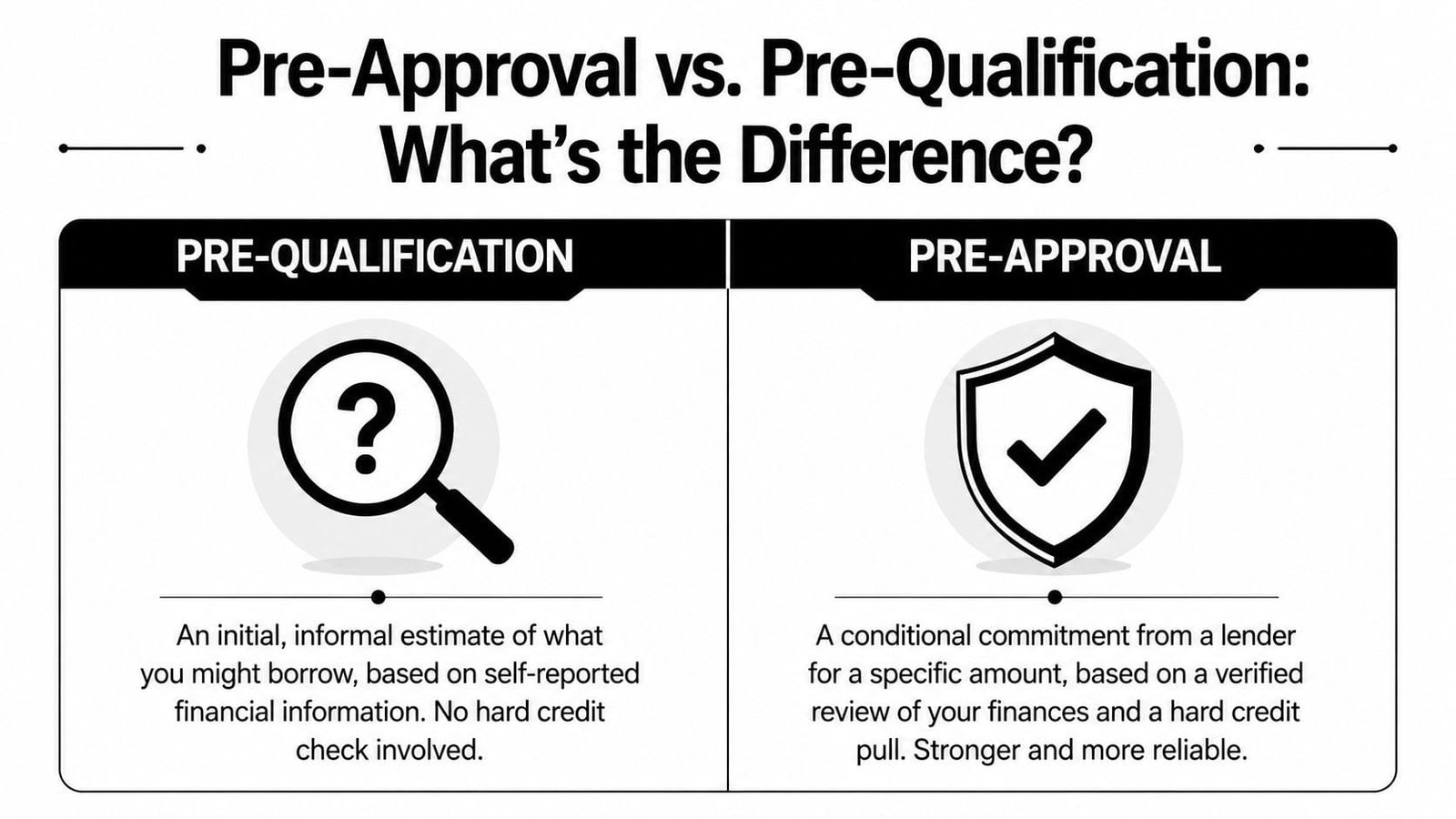

Pre-Approval vs Pre-Qualification Explained

These two terms get mixed together constantly, and that causes expensive misunderstandings.

Pre-qualification is usually a broad estimate. It often relies on information you provide about the business, such as revenue, time in business, and the amount you want. It’s useful for an early conversation, but it’s still a rough sketch.

Pre-approval is stronger. It involves a more serious review of your profile and gives you a clearer idea of whether a lender is likely to approve you, subject to final underwriting. In practice, pre-approval should carry more weight than pre-qualification because the lender has done more work.

Why the distinction matters

The easiest analogy is this:

- Pre-qualification is like getting a rough estimate over the phone.

- Pre-approval is like having a contractor visit the site and inspect the property before quoting the job.

Both are useful. Only one should shape your planning.

Owners get into trouble when they take a pre-qualification email and start making decisions as if the money is already lined up. That can lead to overcommitting on inventory, hiring, or equipment before the lender has verified what really drives approval.

A lender can like your profile at first glance and still decline the deal once the file reaches underwriting.

Pre-Qualification vs. Pre-Approval At a Glance

| Factor | Pre-Qualification | Pre-Approval |

|---|---|---|

| Basis | Usually based on self-reported information | Based on a more lender-reviewed initial assessment |

| Reliability | Ballpark estimate | Stronger indication of likely borrowing capacity |

| Credit review | Often lighter-touch | Typically includes a soft-pull review at this stage |

| Use case | Early exploration | Serious planning and lender comparison |

| Business owner risk | Low time commitment | More useful, but still not final approval |

| Common mistake | Treating it as a promise | Assuming it guarantees funding |

A good rule is to ask one direct question: “What has been reviewed so far?” If the answer is mostly self-reported information, you’re closer to pre-qualification. If the lender has pulled credit softly and reviewed initial financial inputs, you’re closer to true pre-approval.

Another practical difference is how you should use each one. Pre-qualification helps narrow the field. Pre-approval helps you prepare for the underwriting conversation.

How Lenders Evaluate Your Pre-Approval Request

Lenders don’t just look at a score and pick a number. They’re trying to answer a more practical question: if this business draws on a line, what evidence suggests it can manage repayment without creating stress for the company or the lender?

Credit, capacity, and business context

Most line of credit pre approval reviews boil down to three areas.

Credit is part of the picture, but it’s rarely the whole story in business lending. Lenders may look at business credit, personal credit tied to the owner, and any signs of repayment trouble.

Capacity is where many real decisions get made. The Consumer Financial Protection Bureau found that financial institutions use statistical models to estimate a borrower’s ability to pay, and about 3% of credit line increase applications were denied solely for failing those ability-to-pay assessments, as summarized in this CFPB-based analysis. The takeaway for business owners is straightforward. Cash flow quality often matters more than a static score.

Character and business context also matter. Lenders look at time in business, industry risk, ownership stability, and how well the company explains its use of funds. A messy story raises more concern than a complicated one that’s documented clearly.

If you want a broader breakdown of qualifying factors, this overview of line of credit eligibility for new or asset-light small businesses is useful background.

What stronger files usually have in common

A strong file often shows:

- Stable operating liquidity: For institutional credit facilities, lenders may look for meaningful liquidity. According to institutional lending criteria summarized here, commercial lines of credit can require a minimum loan size of $5 Million, minimum operating capital liquidity of $1 Million, and baseline institutional facility eligibility at $20M in revenue, assets, or capital investment.

- Recent financials that match the story: If your application says one thing and your bank activity says another, the file weakens quickly.

- A clear borrowing purpose: Working capital, contract fulfillment, inventory timing, and seasonal smoothing all make sense when the numbers support them.

Underwriters trust consistency. They get cautious when the tax return, P&L, and bank statements describe three different businesses.

What doesn’t work is relying on revenue alone. A company can post large top-line numbers and still struggle with timing, margins, or heavy obligations. Pre-approval gets stronger when the business shows not just earnings, but controllable cash movement.

The Impact on Your Credit Score

You see a lender advertise line of credit pre approval, want to check your options, then stop because you assume the inquiry will hurt your score. That hesitation is common. It also causes owners to wait until cash is tight, which is the worst time to test the market.

What happens at the pre-approval stage

Early pre-approval reviews often rely on a soft credit pull, not a hard inquiry. In practical terms, that usually lets you check likely fit and terms without the same credit-score impact tied to a full application.

For a business owner, that creates room to compare lenders intelligently. You can screen for realistic options before you commit time, documents, and attention to a full underwriting process.

That matters even more because the actual risk is not usually the pre-approval check itself. The larger problem is the pre-approval gap. An owner gets encouraging early feedback, assumes the line is effectively approved, then final underwriting finds weak cash flow coverage, strained liquidity, declining deposit activity, or debt payments that already absorb too much of monthly cash. Credit score concerns get most of the attention, but business performance metrics often decide the outcome.

When the hard pull happens

A hard inquiry usually happens when you move from early review to a formal request for the facility. At that stage, the lender is no longer asking, "Could this fit?" They are asking, "Does this business still meet policy once we verify everything?"

That is where busy owners get caught off guard. A small score impact from a hard pull is manageable. A final denial after you have counted on the line is the bigger operational problem.

Used well, a line of credit can still support your profile over time. Consistent payments, controlled balances, and disciplined use tend to help more than a brief inquiry-related dip hurts. The practical rule is simple. Shop pre-approvals broadly, but submit full applications selectively.

This short explainer is useful if you want a visual overview before applying.

Shop pre-approvals broadly. Submit full applications selectively.

That approach protects your time and keeps your file cleaner. More important, it gives you a chance to check whether the business can hold up under final underwriting, not just pass an early screen.

Your Pre-Approval Preparation Checklist

A pre-approval can look solid on Monday and fall apart in final underwriting by Friday. In my experience, that usually happens because the owner prepared for an initial screen, but not for the closer review that tests cash flow strength, debt capacity, and liquidity.

The goal is simple. Build a file that answers the underwriter’s next question before they have to ask it.

Documents that speed up the process

Have these ready before you request line of credit pre approval:

- Recent business bank statements: These show real cash movement, average balances, large withdrawals, and whether deposits are stable enough to support a revolving facility.

- Profit and loss statements: Lenders use these to review revenue trends, margins, and whether earnings cover repayment.

- Balance sheets: These show working capital, liquidity, retained earnings, and how much debt the business already carries.

- Business tax returns: These help confirm that reported income matches filed results.

- Owner tax returns when requested: Some lenders still review personal income or contingent support, especially for newer businesses or closely held companies.

- Debt schedule: A current list of lenders, balances, monthly payments, and maturities helps underwriters measure total debt burden.

- Accounts receivable and payable aging reports: These show whether customers pay on time and whether vendor obligations are building pressure.

- Use-of-funds explanation: A short note that ties the line to a clear business purpose helps the lender size the request correctly.

What to review before you submit

Collecting documents is not enough. Review them the way an underwriter will.

Start with cash flow. A business can show profit on a P&L and still raise concerns if deposits are uneven, overdrafts appear, or large withdrawals drain liquidity right before the application. That is one of the most common causes of the pre-approval gap. The early screen liked the profile, but final underwriting saw weaker operating cash than expected.

Then check debt service. Add up existing monthly loan payments, equipment notes, merchant advances, and any draws on current credit lines. If those payments already take too much out of monthly cash, the lender may reduce the offer or stop the file. Owners often miss this because revenue looks healthy. Underwriters care more about what is left after obligations are paid.

Liquidity deserves its own review. Cash on hand acts like a shock absorber. It gives the lender confidence that a slow-paying customer, seasonal dip, or one rough month will not turn the line into a problem account.

A simple preparation routine works well:

- Reconcile every major number: Bank statements, internal financials, and tax returns should tell the same story.

- Identify recent changes: New debt, expansion costs, uneven sales, owner draws, or large one-time expenses should be explained clearly.

- Review receivables quality: Strong sales matter less if collections are stretching out and cash is arriving late.

- Test the payment load: Estimate whether current cash flow can support existing debt plus the new line if it is used.

- Write a specific use case: “Working capital” is broad. “Covering payroll and inventory for 60-day receivable cycles on larger contracts” gives the lender context.

If you want a practical timeline for what happens after you submit, review our guide on how long it takes to get a business line of credit approved.

A clean file does more than speed up review. It reduces the odds that final underwriting finds a gap between the pre-approval and the business your documents actually show.

From Pre-Approval to Funding What To Expect Next

Many owners become frustrated. They receive a promising pre-approval, assume the hard part is done, and then hit a wall in underwriting.

That gap is real. A pre-approved business can still be declined because final underwriting reviews far more than the initial screen.

Why pre-approved deals still get declined

The biggest reason is verification. During underwriting, lenders test the business you described against the business your documents show.

According to NetCredit’s explanation of why pre-approved borrowers can still be denied, a critical gap exists because underwriting involves a deeper review of business financials, including cash flow verification and debt service coverage analysis, which can reveal risks that weren’t obvious during the initial soft-check stage. That’s the heart of the pre-approval gap.

In business lending, the common trouble spots are usually practical, not mysterious:

- Cash flow doesn’t support the requested limit: Revenue may be healthy, but timing is inconsistent.

- Debt service looks tight: Existing obligations leave less room than the initial screen suggested.

- Receivables are aging too slowly: Sales on paper don’t help much if collection is drifting.

- Recent changes altered the risk picture: New hires, expansion costs, or recently added debt can weaken the file.

- Documentation doesn’t line up: Numbers conflict across statements, returns, and application answers.

If you want a better sense of timing during this stretch, this breakdown of how long business line of credit approval can take helps set expectations.

How to reduce the pre-approval gap

The best way to avoid surprises is to prepare for underwriting before you ever submit the pre-approval request.

That means reviewing the business the way an underwriter will. Look at cash concentration, debt load, unusual withdrawals, seasonal swings, and whether your explanation of the line matches the evidence in your accounts. Owners who do this early don’t eliminate every issue, but they do reduce the odds of a sudden denial after a promising start.

A good mental model is this: pre-approval tells you the lender is interested. Underwriting decides whether the story survives inspection.

Streamline Your Search with Business Loan Warrior

A better borrowing process doesn’t just save time. It improves decision quality.

Business Loan Warrior is built around that idea. Instead of filling out separate applications across multiple providers, owners can use a single no-fee application to check pre-approval, connect bank accounts securely, and monitor progress through one dashboard. That matters because the businesses that get the best outcomes usually aren’t the ones applying everywhere. They’re the ones comparing intelligently, then moving decisively.

Why a better pre-approval process matters

The platform’s structure addresses the three biggest friction points in line of credit pre approval.

First, it reduces guesswork. A soft-pull pre-approval process lets owners evaluate options without worrying about immediate credit impact.

Second, it improves visibility. When bank data is connected securely, the borrower can see the same operational signals lenders care about, which helps close the gap between early optimism and final underwriting.

Third, it supports smarter matching. Advanced scoring models can improve screening accuracy. For example, VantageScore reports that VantageScore 4.0 identified 11.1% more high-risk loans that later defaulted compared with older approaches in the mortgage pre-screening context. The business takeaway is straightforward. Better pre-screening tools help qualified borrowers move faster while helping lenders filter out weaker files earlier.

That’s what owners want from a financing platform. Not more noise. A clearer path from inquiry to confident action.

Frequently Asked Questions

How long does a business line of credit pre-approval last

It depends on the lender and how stable your business profile remains. A pre-approval isn’t meant to sit untouched forever. If your revenue, debt, or cash position changes materially, the lender may need to revisit the file before moving forward.

Can you get pre-approved with imperfect credit

Yes, sometimes. Pre-approval decisions in business lending often consider more than a personal credit profile. If the company shows stable cash flow, healthy liquidity, and a credible repayment story, that can help. Weak documentation, on the other hand, can sink even a borrower with decent credit.

Is a line of credit the same as a business credit card

No. Both are revolving forms of access to capital, but they behave differently. A business line of credit is generally better suited for planned working capital needs, cash flow timing, and larger operational uses. A business credit card is usually more transactional and often better for smaller recurring purchases.

Does pre-approval guarantee funding

No. Pre-approval is a positive signal, not a final commitment. Final approval depends on underwriting, verification, and whether the deeper review confirms the business can support the facility requested.

If you want the strongest possible outcome, treat pre-approval as the beginning of lender scrutiny, not the end of it. Organize your documents early, know your cash flow story, and assume the underwriter will test every major claim in the application.

If you want to check your options without adding unnecessary friction, Business Loan Warrior offers a practical starting point. You can submit one no-fee application, explore pre-approval through a soft-pull process, connect bank accounts securely, and track progress through a dashboard built for busy owners who need clarity before they commit.