You're probably looking at a piece of equipment your practice needs now, not someday. Maybe it's an ultrasound machine, a digital radiography unit, a new diagnostic analyzer, or a replacement for a device that's started to fail often enough to disrupt patient flow. The hard part isn't understanding why you need it. The hard part is deciding how to pay for it without draining cash reserves you still need for payroll, supplies, hiring, and the normal surprises that come with running a healthcare business.

That's where medical equipment financing becomes less about “borrowing money” and more about preserving options. The right structure can help a practice add revenue-producing equipment, keep treatment in-house, and avoid tying up capital in a single purchase. The wrong structure can leave you with a payment that looks manageable on paper but feels heavy once installation, training, maintenance, and reimbursement delays hit the books.

Table of Contents

- Why Smart Practices Finance Medical Equipment

- The Four Main Paths to Financing Medical Equipment

- Decoding the True Cost and Terms of Your Financing

- Tax Benefits and Depreciation Explained

- Your Step-by-Step Application Roadmap

- Real-World Scenarios When to Choose Each Option

- Frequently Asked Questions About Medical Equipment Financing

Why Smart Practices Finance Medical Equipment

A common turning point looks like this. A practice is busy, referrals are steady, and clinicians are sending too many patients elsewhere for imaging or diagnostics. The owner knows a new machine would improve patient experience and keep more revenue inside the practice, but the upfront price would punch a hole in working capital.

That's why experienced operators don't treat financing as a last resort. They use it as a cash-flow tool. If the equipment will support patient care and help the practice grow, paying over time can be the more disciplined move than writing one large check.

The broader market reflects that shift. The global medical equipment financing market was valued at approximately USD 192 billion in 2026 and is projected to reach USD 406.85 billion by 2034, growing at a 9.84% CAGR, according to Fortune Business Insights on the medical equipment financing market. That kind of scale tells you something important. Practices, hospitals, and healthcare operators already view financing as a normal part of acquiring essential technology.

Financing protects flexibility

The strongest reason to finance isn't that you can't afford the equipment. It's that you need your cash for more than one job.

A practice owner who spends heavily on equipment upfront may delay hiring, postpone marketing for the new service line, or lose their buffer when reimbursements come in slower than expected. A financed purchase spreads the burden so the equipment can start working while the business keeps breathing.

Practical rule: If buying the equipment outright would leave your practice financially stiff, financing is often the safer choice even when you have the cash.

Growth matters more than pride of ownership

Some owners still feel that financing means paying extra for something they should just buy. That thinking misses the business reality. Medical equipment often exists to generate or retain revenue, improve care, reduce referral leakage, or increase throughput. If the equipment helps the practice grow, the relevant question isn't “Can I avoid financing?” It's “Which structure fits how this asset earns money?”

For a broader look at how equipment funding supports business stability, see these equipment financing benefits for 2026.

The Four Main Paths to Financing Medical Equipment

Not all financing products solve the same problem. Some are built for ownership. Others are built for flexibility. Some work best when the equipment will stay useful for years. Others make more sense when technology changes quickly.

Market behavior backs that up. Leases account for roughly 52% of medical equipment deals by count, while loans represent about 58% by dollar value, according to GM Insights on the medical equipment financing market. In plain English, practices often lease smaller or faster-changing assets, while larger purchases more often use loan structures tied to ownership.

Equipment loans

An equipment loan is the closest thing to a mortgage for a machine. You borrow to buy the asset, make scheduled payments, and work toward ownership.

This is often the cleanest fit when the equipment has a long useful life and you expect to use it well past the financing term. It also tends to suit practices that want a clear end point. Once the note is paid, the asset is yours.

A loan usually works best when:

- The equipment will stay relevant for years: Think core diagnostic, treatment, or lab equipment you don't expect to replace quickly.

- You want ownership: That matters for balance sheet strategy, residual value, and tax conversations with your CPA.

- You prefer straightforward economics: Borrow, pay down principal, own the asset.

Capital leases

A capital lease, often called a buyout-style lease, behaves a lot like a loan in practice. You use the equipment during the term, and the structure is designed around eventual ownership or a nominal buyout.

This option often appeals to owners who want ownership-focused economics but also want a lease format. For practical decision-making, think of it as “ownership later, with lease paperwork now.”

Operating leases

An operating lease is closer to renting. You're paying for use, not necessarily for permanent ownership. That makes it attractive for equipment categories where obsolescence moves faster than your amortization schedule.

If you've ever seen a practice get stuck paying for equipment that no longer feels competitive, you've seen why operating leases exist. They can reduce the risk of being married to aging technology.

Vendor financing

Vendor or manufacturer financing is financing arranged through the seller. It can be convenient because the equipment quote and the financing conversation happen together.

Convenience, though, isn't the same as the best fit. Vendor programs can be efficient, especially when the manufacturer understands the equipment lifecycle and service requirements. But they can also narrow your shopping if you stop comparing structures.

The fastest paper process isn't always the best financial decision. A smooth vendor quote can hide end-of-term terms, service exclusions, or upgrade constraints.

Here's the side-by-side view:

| Feature | Equipment Loan | Capital Lease | Operating Lease | Vendor Financing |

|---|---|---|---|---|

| Ownership goal | Own at end of term | Usually designed toward ownership | Usually focused on use | Depends on program |

| Best fit | Long-life core equipment | Ownership-oriented lease structure | Fast-changing technology | Buyers who want one-stop convenience |

| Payment mindset | Paying down a purchase | Lease payments with buyout path | Paying for use and flexibility | Varies by manufacturer or dealer |

| End of term | Asset is paid off | Buyout or ownership transition | Return, renew, or possible purchase option | Depends on contract |

| Main risk | Overcommitting to aging tech | Confusing lease language with loan economics | Paying for convenience without understanding return terms | Accepting seller-friendly terms without comparison |

If you're comparing lender types and structures, this overview of equipment financing options for small businesses is a useful companion.

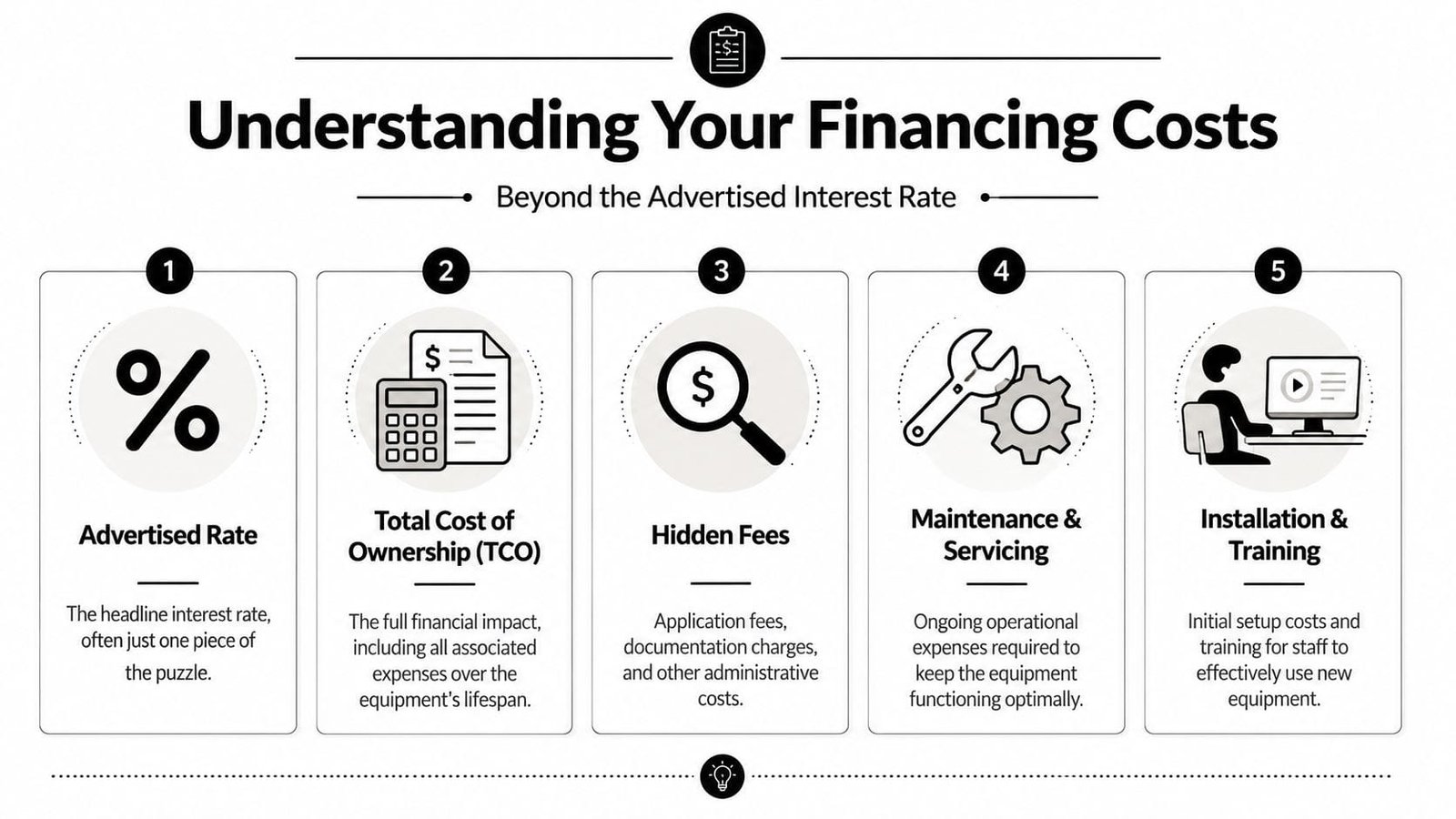

Decoding the True Cost and Terms of Your Financing

A lot of owners compare offers by monthly payment first. That's understandable, but it's also where expensive mistakes start. A lower payment can still produce a worse deal if it ignores setup costs, service costs, or a payment schedule that doesn't line up with how your practice gets paid.

Build the total cost before you compare payments

The key number to model is total cost of ownership, not just the financed amount. In medical settings, the machine itself is only one part of the spend.

Before signing anything, build a worksheet that includes:

- Delivery and installation: Site prep, freight, rigging, calibration, and setup can change the deal economics quickly.

- Training: Staff training has a direct cost and an indirect cost. Productivity usually dips while the team learns the new workflow.

- Maintenance and service contracts: These can be essential, especially for imaging and diagnostics.

- Downtime planning: If the machine needs service, what happens to scheduling and revenue during that period?

- Consumables and software: Some equipment is cheap to acquire and costly to operate.

Blue Bridge Financial's guide to the medical equipment financing application process notes that buyers should factor in delivery, installation, maintenance, and training, then align repayments with insurance reimbursement cycles. The same source also notes that approvals can happen in 24–48 hours, which is helpful operationally but can distract from a more important question: does the payment schedule match the practice's cash conversion cycle?

Terms should follow cash flow not sales pressure

The best financing term is the one your practice can carry comfortably while the equipment ramps up. If claims take time to pay, a rigid monthly obligation can feel heavier than the quote suggests.

That's why I advise owners to review financing in this order:

- How will the equipment produce value? Direct revenue, retained referrals, faster throughput, or better care delivery.

- What are the non-obvious costs? Installation, training, maintenance, software, supplies.

- When does cash arrive? Immediately at point of service, later through reimbursement, or unevenly over time.

- Does the payment schedule fit that timing? If not, the structure is wrong even if the rate looks attractive.

A good financing offer fits your billing cycle. A bad one assumes your cash hits the bank the moment the machine is delivered.

If you want a practical framework for evaluating all-in borrowing costs, this guide on how to calculate the real cost of a small business loan is worth reviewing.

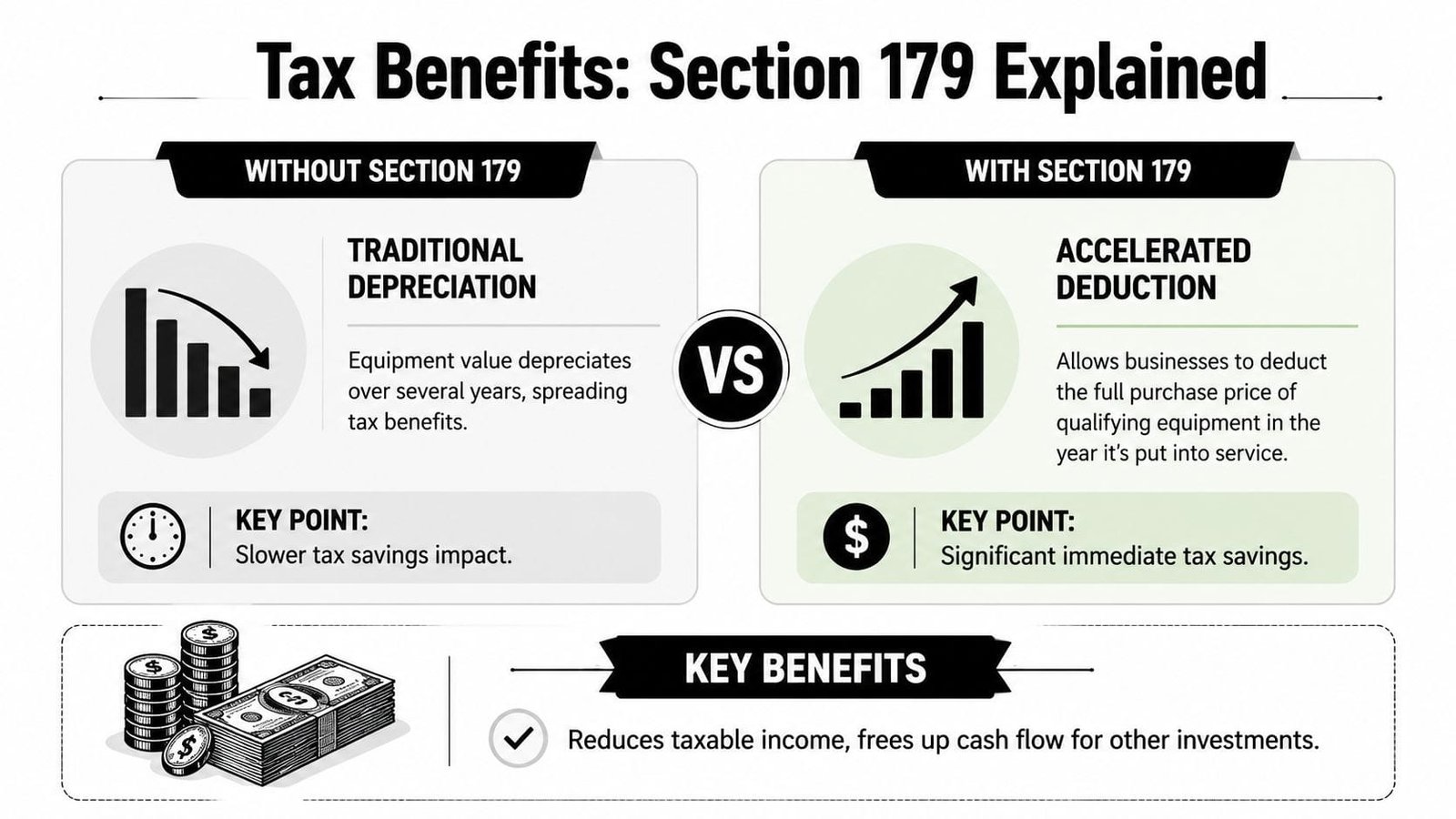

Tax Benefits and Depreciation Explained

Tax treatment can materially affect the value of a financing decision, but it only helps when the structure matches your accounting and cash-flow goals. Often, many practice owners hear broad statements about “write-offs” and assume every financing option works the same way. It doesn't.

A useful starting point is this: ownership-oriented structures and usage-oriented structures often create different tax conversations. If your financing is designed so the practice effectively buys and owns the equipment, your CPA may evaluate depreciation and potential Section 179 treatment. If your financing is structured more like rent, the payments may be treated more like operating expense.

Ownership structures and lease structures work differently

An equipment loan or buyout-style lease often appeals to owners who want the asset on a path toward ownership. In many cases, that opens the door to tax planning around depreciation and possible accelerated deduction treatment, subject to your CPA's guidance and current tax rules.

An operating lease is different. You're generally paying for use over a period, often with more flexibility around upgrades or end-of-term return. That can simplify the operational side of the decision, but it changes the tax discussion.

Medical equipment is financed constantly. The Equipment Finance Industry Horizon Report estimates that 84% of acquisition volume within the medical equipment vertical is secured by a lease, loan, or line of credit, making it the most likely equipment category to be financed across industry verticals, according to the Equipment Leasing & Finance Foundation Horizon Report. When so much equipment is financed, understanding structure-specific tax treatment isn't a niche issue. It's basic practice management.

What to ask your CPA before signing

Bring your CPA into the decision before you accept final terms, not after. Ask direct questions:

- Will this structure be treated as ownership or use?

- Does this equipment likely qualify for accelerated deduction treatment under current rules?

- Would spreading deductions over time be better for our tax position than front-loading them?

- How will this affect the balance sheet and future borrowing capacity?

The best tax result on paper can still be the wrong business decision if it creates a payment burden your practice doesn't want.

The right answer is rarely universal. It depends on profitability, timing, and whether the practice values ownership more than flexibility.

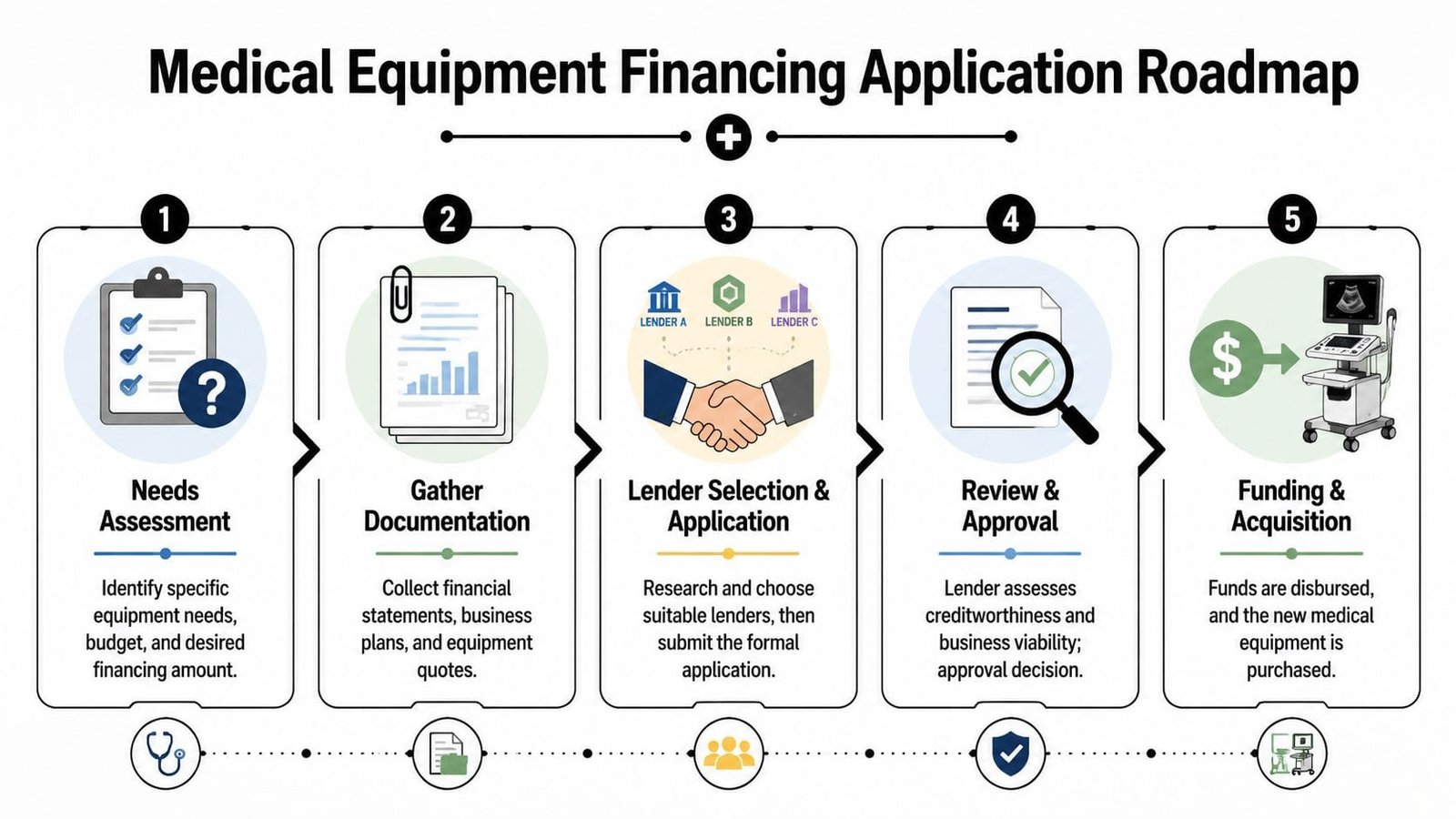

Your Step-by-Step Application Roadmap

The application process is usually less mysterious than owners expect. The smoother deals tend to have one thing in common: the borrower has already done the operational homework before filling out the form.

Start with the equipment plan not the application

Begin with the asset itself. Define what you're buying, why this model fits the practice, what it will cost beyond the sticker price, and how it will affect operations.

A clean pre-application checklist usually includes:

- A vendor quote: Make sure it reflects the exact equipment, accessories, and any service or software components.

- A rollout plan: When will it be installed, who will use it, and what training is required?

- A revenue or efficiency thesis: You don't need fantasy projections. You need a credible reason the purchase makes sense.

- A cash-flow view: Know how the payment fits alongside payroll, rent, supplies, and reimbursement timing.

Healthcare equipment commonly has a useful life of about 5 to 15 years, and loan terms are usually 10 years or less, while operating leases are often favored for fast-obsolescence assets such as imaging, IT, and diagnostic devices, according to SoFi's overview of medical equipment financing. That's a useful benchmark when deciding whether you're financing a durable workhorse or a piece of technology that may need replacement sooner.

What lenders usually want to see

Most lenders are trying to answer a short list of questions. Is the equipment appropriate for the business? Does the practice produce enough cash to handle the payment? Is management credible? If the equipment itself serves as collateral, how stable is its value?

Prepare documents that help answer those questions cleanly:

- Business financial statements

- Recent business tax returns

- Business bank statements

- Equipment quote or purchase order

- Ownership information and, when requested, personal financial details

Lenders also care about context. A replacement purchase for an established practice is different from a first major equipment purchase for a newer operation. Neither is impossible. The story just needs to make operational sense.

For a quick overview of the process in action, watch this short explainer:

Approval funding and rollout

Once approved, review the agreement like an operator, not just a borrower. Confirm the financed items, any soft costs included, payment start date, end-of-term terms, maintenance obligations, and whether funds go to you or directly to the vendor.

Then think about implementation:

- Installation timing: Don't start paying for idle equipment if the room or staffing won't be ready.

- Training completion: Productivity often improves only after the team gets comfortable with the machine.

- Billing readiness: Make sure coding, payer workflows, and documentation protocols are in place.

Approval is not the finish line. The equipment only becomes a good investment when your team can use it well and bill for it correctly.

Real-World Scenarios When to Choose Each Option

The easiest way to choose a structure is to tie it to the equipment's role inside the practice.

A startup dental clinic buying its first digital imaging system usually values flexibility more than pride of ownership. Cash is tight, patient volume is still building, and the owner may want the option to upgrade once the practice matures. In that situation, an operating lease can make sense because it prioritizes manageable use over long-term attachment to the first generation of equipment.

An established specialty practice replacing a core diagnostic machine often thinks differently. The equipment supports a stable service line, the clinical demand is proven, and the owner expects to keep using the asset for years. That's where an equipment loan or buyout-style lease often fits better. The practice is paying toward something it expects to keep.

A multi-location urgent care group faces a different problem altogether. It may need several units across sites and want standardization, easier procurement, and a simpler refresh cycle. Vendor financing can work well here if the manufacturer offers consistent servicing, coordinated deployment, and a contract the group has reviewed carefully. The key is not assuming convenience equals the best economics.

Here's the shortcut I use with clients:

- Choose a loan when the equipment is central to operations and likely to stay valuable for a long time.

- Choose a capital lease when you want something close to ownership but prefer that lease structure.

- Choose an operating lease when technology risk is high and flexibility matters more than owning the asset.

- Choose vendor financing when operational simplicity is valuable and the contract still holds up after comparison.

The wrong match usually comes from focusing on the payment alone. The right match comes from asking how long the equipment will stay useful, how quickly it will earn money, and whether the practice wants to own it at the end.

Frequently Asked Questions About Medical Equipment Financing

Can I finance used or refurbished medical equipment

Often, yes. Many lenders will consider used or refurbished equipment if the asset is from a credible source, has a supportable value, and still has enough useful life left to justify the term. The details depend on the lender and the equipment category.

What happens at the end of a lease term

It depends on the lease structure. With an operating lease, you may return the equipment, renew the lease, or have an option to purchase based on the contract. With a buyout-style lease, the agreement is usually designed around eventual ownership.

Does personal credit matter

Yes, especially for closely held practices. Even when the borrowing entity is the business, lenders often review the owners behind it. Strong business cash flow helps, but weak personal credit can still affect structure, pricing, or approval terms.

How quickly can funding happen

Some transactions move fast, especially when the equipment quote is clean and the borrower is organized. But speed shouldn't be the main goal. The better goal is getting a structure that fits the practice's real cash flow and total ownership cost.

Can installation and training be included in financing

Sometimes they can, depending on the lender, vendor, and how the quote is written. That's worth asking early. If those costs won't be financed, your practice needs to plan for them separately instead of getting surprised after approval.

Is leasing always cheaper than buying

No. Leasing may lower upfront burden or create better upgrade flexibility, but it isn't automatically the lower-cost path over the full life of the equipment. You need to compare the all-in economics, not just the starting payment.

If you're weighing medical equipment financing and want help comparing structures without wasting time on the wrong fit, Business Loan Warrior can help you explore suitable funding options through a single no-fee application. You can check pre-approval without affecting credit, review offers in one place, and find a structure that supports cash flow instead of straining it.