Cash gets tight fast when you're running a business. A freezer fails on a Friday, a supplier offers a one-time inventory deal that expires tomorrow, or payroll lands before a large batch of customer payments clears. In that moment, you're not looking for a finance lecture. You're looking for money that shows up quickly enough to solve the problem.

That urgency is exactly why so many owners search for the merchant cash advance meaning. They want to know whether an MCA is a loan, whether it's safe, and why the offer sounds so simple. The short answer is this: an MCA can deliver fast capital, but the legal structure and repayment mechanics make it very different from a normal business loan, and often much riskier than people realize.

Table of Contents

- The Need for Speed When Cash is Tight

- What Exactly Is a Merchant Cash Advance

- How Repayment and Costs Actually Work

- Calculating the True Cost of an MCA

- The Hidden Dangers and Critical Red Flags

- When an MCA Makes Sense and Smarter Alternatives

The Need for Speed When Cash is Tight

A restaurant owner loses the main oven during lunch service. A retailer gets offered a deep discount on inventory, but only if payment goes out by tomorrow. A service company has jobs lined up, but needs working cash to buy materials before customer payments arrive.

Those aren't rare situations. They're ordinary operating problems, and they create the exact opening where a merchant cash advance becomes attractive. When the bank says, “We need more paperwork,” and the clock keeps ticking, speed starts to matter more than price.

According to Allied Market Research's merchant cash advance market outlook, the global MCA market was valued at $17.9 billion in 2023 and is projected to reach $32.7 billion by 2032, with typical approval rates ranging between 70% and 80% compared with around 14% at large banks. The same source notes that funds are often disbursed within 24 to 72 hours.

Why owners say yes so quickly

The pitch is powerful because it lines up with what a stressed owner needs in the moment:

- Fast decisions: You may get an answer while a bank is still requesting documents.

- Less friction: MCA underwriting often focuses more on sales flow than on the standards a traditional lender may require.

- Urgent-use fit: Equipment repairs, inventory buys, and short-term cash gaps feel like problems that can't wait.

If you're weighing urgent options, it helps to compare MCAs against other forms of short-term business financing before signing anything.

Practical rule: Fast money solves timing problems. It doesn't automatically solve expensive-money problems.

Why speed can hide the real issue

The danger starts when owners treat “approved quickly” as proof that the product is safe. It isn't. It only means the provider is willing to advance cash based on future sales.

That distinction matters because the easier the cash is to get, the more disciplined you need to be. Owners usually don't get in trouble with MCAs because they fail to understand urgency. They get in trouble because they underestimate what the daily repayment pull will do to cash flow after the emergency passes.

What Exactly Is a Merchant Cash Advance

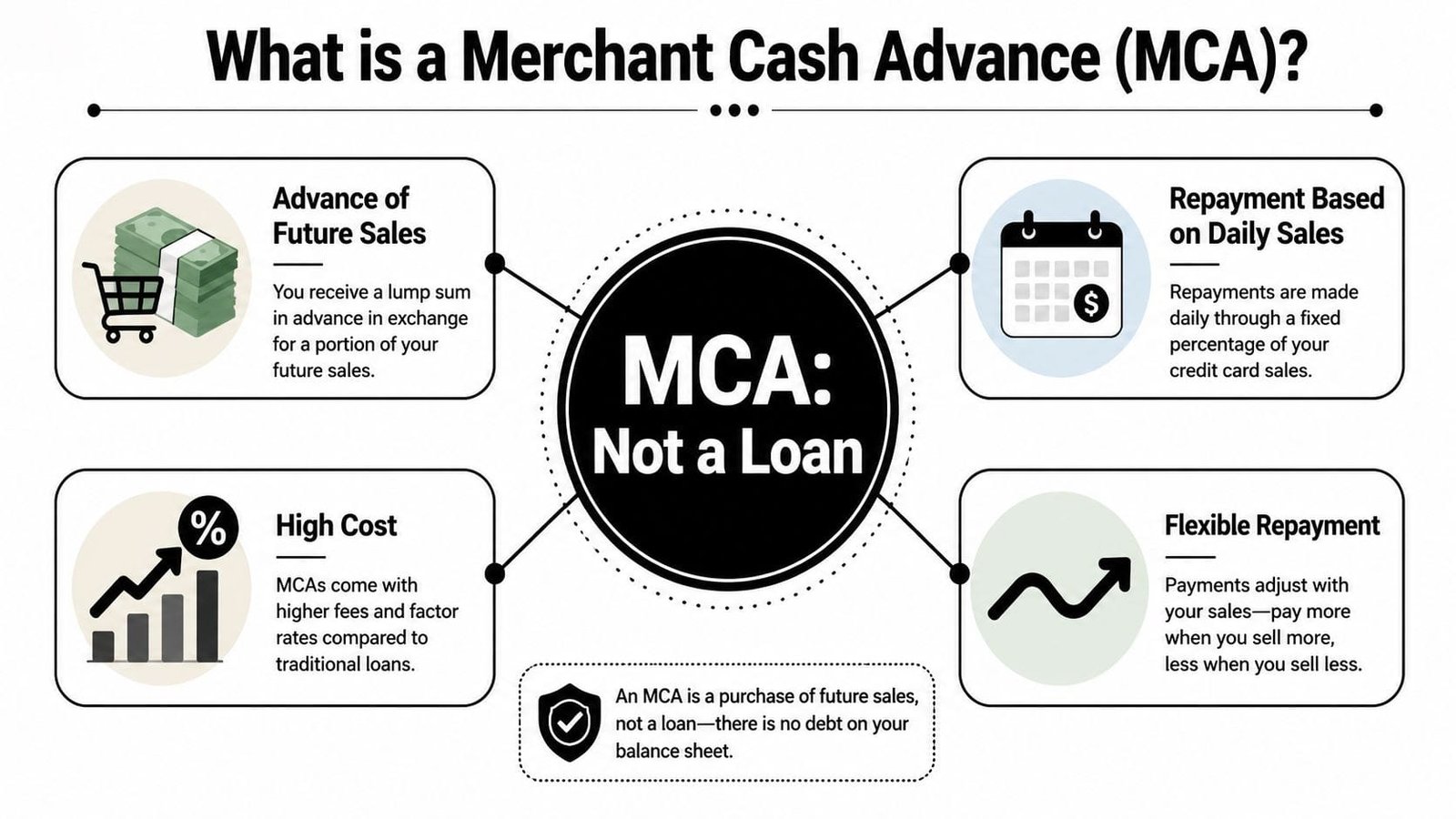

The cleanest way to understand the merchant cash advance meaning is to stop calling it a loan.

An MCA is structured as a purchase of future revenue receivables rather than a traditional loan, according to Wikipedia's summary of merchant cash advances. That same source explains that MCA pricing uses a factor rate, typically 1.20 to 1.50, instead of an interest rate. A factor rate of 1.40 means you repay 140% of the amount advanced.

A visual helps here.

Think of it as selling tomorrow's sales today

Say your business expects future card sales over the coming months. An MCA company offers you cash now in exchange for the right to collect an agreed portion of those future sales until it receives the full purchased amount back.

That's why many MCA contracts talk about receivables, remittance, and purchased amount instead of loan terms like principal and interest. The wording isn't cosmetic. It reflects the structure.

A simple analogy works better than finance jargon. If a farmer sells part of a future harvest before it's picked, that's not the same as borrowing from a bank. The farmer gets cash now by giving up part of what future production is expected to generate. An MCA works in a similar way, except the “harvest” is your future business revenue.

Later in the section, this video adds another layer of context:

Why the legal label matters

Many guides stop too early. They define the product, but they don't explain why the legal label changes the risk.

Because the MCA company says it is buying future receivables, not making a loan, the agreement may sit outside parts of the lending framework business owners assume will apply. That means you shouldn't read an MCA offer with a loan mindset. If you do, you can misunderstand both the cost and the protections you may not have.

If you're signing an MCA agreement, don't ask only, “How much am I getting?” Ask, “What rights am I giving up because this isn't legally framed as a loan?”

That single question gets closer to the actual merchant cash advance meaning than the marketing language does.

How Repayment and Costs Actually Work

The mechanics matter more than the sales pitch. Once you understand how repayment works, you can see why some businesses tolerate an MCA for a short period, while others get squeezed almost immediately.

Two moving parts control everything

The first moving part is the factor rate. It sets the total amount you must repay. Unlike interest on a standard amortizing loan, the factor rate isn't reduced because you pay early or because the balance declines over time. It's a fixed multiplier applied upfront.

The second moving part is the holdback rate. According to PayPal's explanation of cash advance versus business loan, MCA repayment typically relies on a holdback rate of 10% to 20% of daily sales, automatically deducted from daily credit and debit card transactions until the total advance plus fees is satisfied.

Here's the plain-English version:

- You receive a lump sum.

- The provider sets the total payback using the factor rate.

- A portion of your daily sales is pulled automatically.

- Those deductions continue until the full purchased amount is collected.

What daily repayment feels like in real life

On paper, a holdback can sound flexible because the payment moves with sales. In practice, it changes how every sales day feels.

Good sales days don't just bring relief. They can also accelerate how much cash leaves your business. Slow days reduce the amount pulled, but they don't remove the pressure because the business still has rent, labor, inventory, utilities, and taxes to cover.

A normal term loan hits once a month. An MCA can affect your operating cash every business day. That difference is operational, not just mathematical.

A repayment method tied to daily sales can look flexible from the lender's side and restrictive from the owner's side. Both can be true at once.

What to look for in the agreement

Before signing, owners should isolate the repayment language and read it without distraction. Focus on these points:

- Collection method: Is repayment taken from card sales, bank account debits, or both?

- Frequency: Daily and weekly pulls create different cash flow pressure.

- Reconciliation language: If sales drop, does the contract clearly explain whether collections can be adjusted?

- Total purchased amount: This matters more than the advertised speed of funding.

If you can't explain those points back to someone else in one minute, you don't yet understand the deal.

Calculating the True Cost of an MCA

Most confusion around MCAs starts with one innocent-looking number. The factor rate.

A factor rate doesn't behave like the interest rate on a conventional loan, so owners often underestimate the cost. A rate of 1.3 or 1.4 can sound manageable because it doesn't look like a high annual percentage. But that's because it isn't presented as one.

Why factor rates confuse owners

According to Crestmont Capital's merchant cash advance statistics overview, MCAs typically charge factor rates from 1.1 to 1.5, which can translate to effective APRs from 40% to over 350%. The same source explains that because MCAs are legally classified as purchases of future receivables rather than loans, they can bypass state usury laws that cap interest rates.

That's the key translation issue. The factor rate tells you the total payback multiple. It does not tell you the annualized cost in the intuitive way most owners compare financing products.

For example, if a provider advances $50,000 and uses a factor rate of 1.40, the total payback is $70,000. That means $20,000 is the financing cost before you even get into how quickly it is collected. If repayment happens fast, the effective annualized cost rises sharply. That's why the same-looking factor rate can feel very different depending on remittance speed.

If you want a more grounded way to compare offers, this guide on how to calculate the real cost of a small business loan without the headache is useful because it trains you to focus on total payback and cash flow impact, not just the headline number.

A simple comparison of cost structure

The table below isn't a pricing quote. It's a framework for reading the differences between product types.

| Metric | Traditional Term Loan | Merchant Cash Advance |

|---|---|---|

| Pricing language | Interest rate | Factor rate |

| Cost presentation | Usually easier to annualize and compare | Often looks simpler than it really is |

| Repayment rhythm | Typically fixed scheduled payments | Usually daily or weekly remittance tied to sales |

| Legal treatment | Loan | Purchase of future receivables |

| Exposure to usury caps | Generally within lending rules | May fall outside those caps |

| Cash flow effect | More predictable budgeting | Ongoing drain on daily operating cash |

The problem isn't just that an MCA can be expensive. It's that the structure can make the expense less obvious at first glance.

Loan vs. MCA Cost Comparison ($50,000 Advance)

A disciplined owner should ask these questions before accepting a quote:

- What is the total payback? This is the first number that matters.

- How fast is remittance expected to occur? Faster repayment can make the annualized cost far worse.

- What happens in a weak sales month? A provider's answer tells you whether “flexibility” is real or mostly marketing.

If the representative keeps steering you back to speed, simplicity, or approval odds, push harder on total cost. That's where the truth sits.

The Hidden Dangers and Critical Red Flags

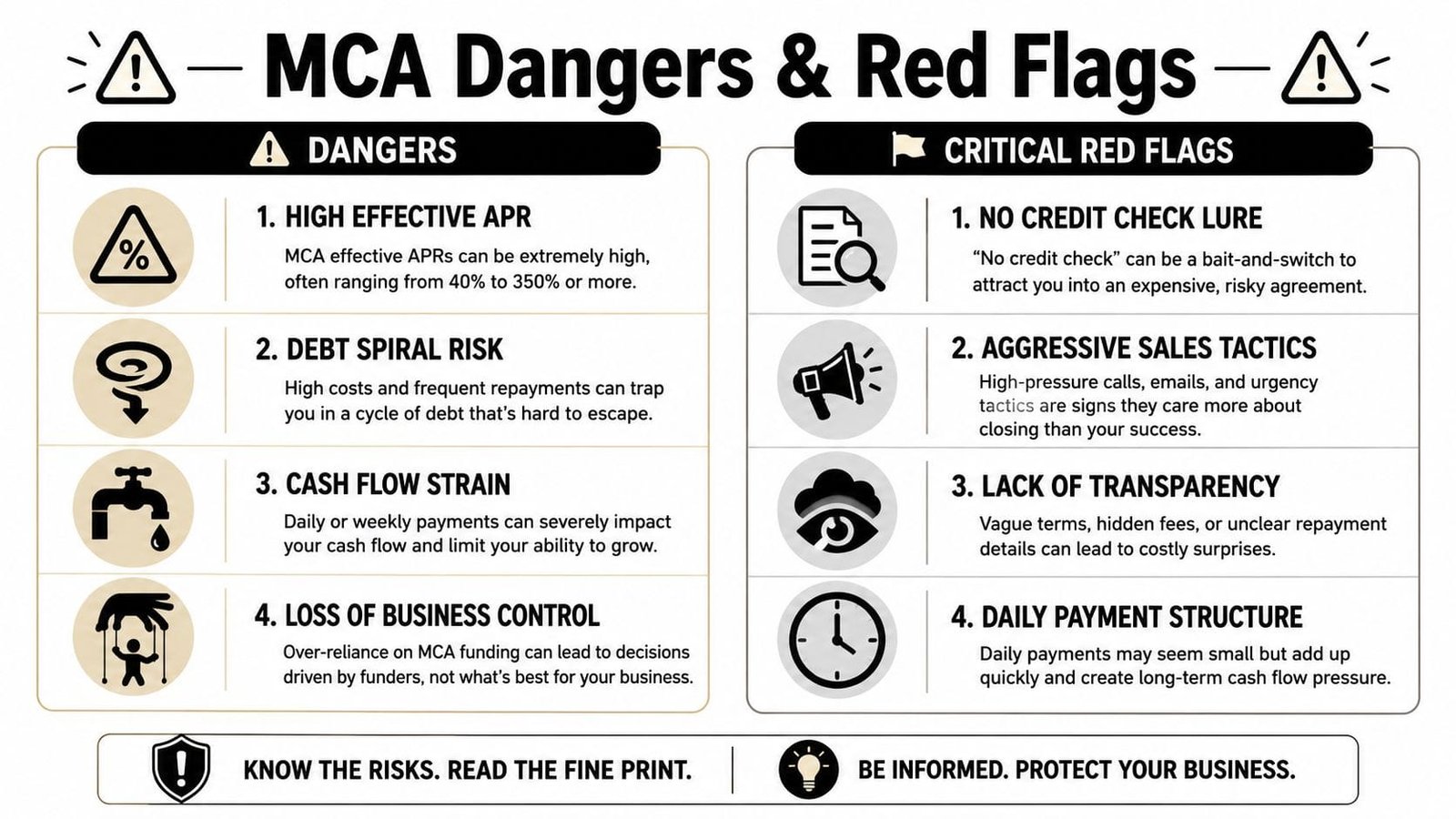

The biggest MCA risk isn't just price. It's the combination of high cost, daily cash extraction, and a legal structure many owners don't fully understand.

The non-loan problem most owners miss

According to Stripe's guide to merchant cash advances, the legal non-loan classification of MCAs can strip business owners of federal protections like the Truth in Lending Act. The same source warns that a high holdback rate, such as 20%, can create a revenue death spiral during seasonal dips because the provider continues pulling a large share from shrinking sales.

This is the part that deserves more attention than it gets.

Many owners think, “It's expensive, but it's still financing.” Legally, that assumption can be dangerous. If the product isn't treated like a loan, some of the borrower protections you expect may not apply in the same way. That changes how disputes, disclosures, and enforcement can play out.

If you want a broader framework for evaluating exposures before taking on any fast capital product, this primer on what is risk management is worth reading. It helps you separate a temporary cash need from a financing choice that can create a larger operating problem.

How a revenue death spiral starts

This spiral usually begins with a business problem that feels temporary. Sales soften. A location has a weak month. A major account pays late. Then the holdback keeps pulling from each day's receipts.

The business now has less cash for payroll, inventory, vendor terms, and routine operating slack. To cover that gap, the owner may cut necessary spending, delay payments, or take more expensive capital. That second move is where many companies lose control.

When revenue falls, your business needs breathing room. A high holdback removes it.

The MCA provider may call this sales-based flexibility. The owner experiences it as a shrinking pool of usable cash right when resilience matters most.

Red flags before you sign

Not every MCA agreement is equally dangerous, but several warning signs should make you slow down:

- Aggressive sales pressure: If someone pushes you to sign before your accountant or attorney reviews the contract, that's a bad signal.

- Murky reconciliation terms: If the provider says payments adjust with sales but the contract is vague, treat that as unresolved risk.

- Personal guarantees or severe enforcement clauses: These can expand the fallout far beyond business cash flow.

- Lack of transparency on total payback: If you can't identify the full purchased amount immediately, stop.

A stressed owner often focuses on approval and funding time. A careful owner focuses on what happens after the money lands.

When an MCA Makes Sense and Smarter Alternatives

There are situations where an MCA can be rational. They're narrower than the marketing suggests, but they do exist.

Situations where an MCA can be rational

An MCA can make sense when the need is short-term, the return is clear, and the cash event it finances has a high probability of paying back more than the advance costs. Think emergency equipment replacement that restores revenue immediately, or a time-sensitive inventory purchase with unusually strong margin and fast sell-through.

It makes far less sense when you're using it to patch recurring operating weakness. Payroll, chronic rent pressure, or a business model with ongoing cash burn are poor matches. In those cases, the MCA often speeds up the problem instead of solving it.

For owners comparing funding categories more broadly, The Owner's Shortlist financing resources can help frame the alternatives without reducing everything to “fastest money wins.”

Better options for common funding needs

A smarter approach is to match the product to the problem:

- Ongoing working capital needs: A business line of credit is often better suited than daily MCA remittance.

- B2B companies waiting on invoices: Invoice financing may fit the cash cycle more naturally.

- Revenue-driven businesses with variable sales: Revenue-based financing may be worth comparing if you want a structure tied to revenue without assuming every MCA term is interchangeable.

- Longer-term investments: A term loan or equipment financing usually aligns better with assets that produce value over time.

The practical test is simple. If the capital need is temporary and highly profitable, an MCA may be a tool. If the capital need is structural, an MCA can become a trap.

If you're comparing funding options and want a clearer path through term loans, lines of credit, equipment financing, invoice financing, or merchant cash advances, Business Loan Warrior can help you review choices without the usual confusion. Their platform lets business owners check options through one application, compare funding paths, and move faster with more clarity on cost and fit.