You're probably in one of two positions right now. Either you've outgrown your current footprint and need a building, equipment, or both. Or you need flexible capital to buy a business, refinance debt, smooth cash flow, and keep growth moving without tying yourself in knots.

That's where the SBA decision gets interesting. On paper, SBA 7(a) vs 504 looks simple. One is flexible. One is asset-focused. In practice, the wrong choice can lock you into the wrong structure, the wrong timeline, and the wrong exit options.

A lot of owners default to the better-known program. That's lazy thinking. In 2024, the SBA approved over 70,000 7(a) loans and nearly 6,000 504 loans, so 7(a) was used by more than 11 to 1, largely because it's more versatile, according to Western Alliance's comparison of SBA 7(a) and 504 loans. Popular doesn't mean better for your deal. It usually just means easier to understand.

If you're still in startup mode, a founder-focused resource like this guide for indie hackers to get funded can help frame the broader capital stack. But if you're running a mature company and deciding how to fund your next move, you need sharper tools than generic startup advice. You need to match the loan to the objective.

For owners planning a larger facility move, expansion capital often sits alongside real estate or equipment financing, which is why it helps to understand the broader scope of business expansion loans before choosing the SBA path.

Table of Contents

- Choosing Your Growth Path With an SBA Loan

- SBA 7a vs 504 At a Glance

- Loan Purpose and Funding Structure

- Comparing Financial Terms and Hidden Costs

- Navigating Eligibility and Application Timelines

- Real World Scenarios Which Loan for Your Business

- Your Final Decision Checklist and Next Steps

Choosing Your Growth Path With an SBA Loan

A strong business can still get stuck at the exact moment it should be accelerating. Revenue is healthy. The team is proven. A new facility comes up for sale, or a competitor becomes available, or a production bottleneck starts costing you margin every month. The opportunity is real. The constraint is capital.

That's the moment when owners start comparing SBA 7(a) and 504. They sound similar because both sit under the SBA umbrella. They are not similar in how they behave.

One path is broad and flexible. The other is specialized and disciplined. I think of 7(a) as your general contractor. It can handle a lot of jobs under one agreement. I think of 504 as a purpose-built real estate and equipment structure. Less flexible, but often better engineered for long-term fixed assets.

The decision is really about precision

Owners get in trouble when they ask, “Which SBA loan is better?” That's the wrong question.

Ask these instead:

- What exactly are you financing? Real estate, equipment, working capital, acquisition goodwill, refinance, or a mix.

- How fast do you need to close? If timing is tight, complexity matters.

- What are you optimizing for? Flexibility, lower down payment on fixed assets, long-term payment stability, or exit freedom.

Practical rule: If your use of funds spills across several categories, 7(a) usually fits better. If the deal is mainly a building or heavy equipment, 504 deserves first look.

A discerning borrower doesn't choose based on brand familiarity. You choose based on where the friction shows up later. Sometimes that's monthly payment volatility. Sometimes it's application complexity. Sometimes it's a penalty when you refinance earlier than planned.

That's why surface-level comparisons aren't enough. The headline difference is easy. The strategic trade-offs are where the core decision resides.

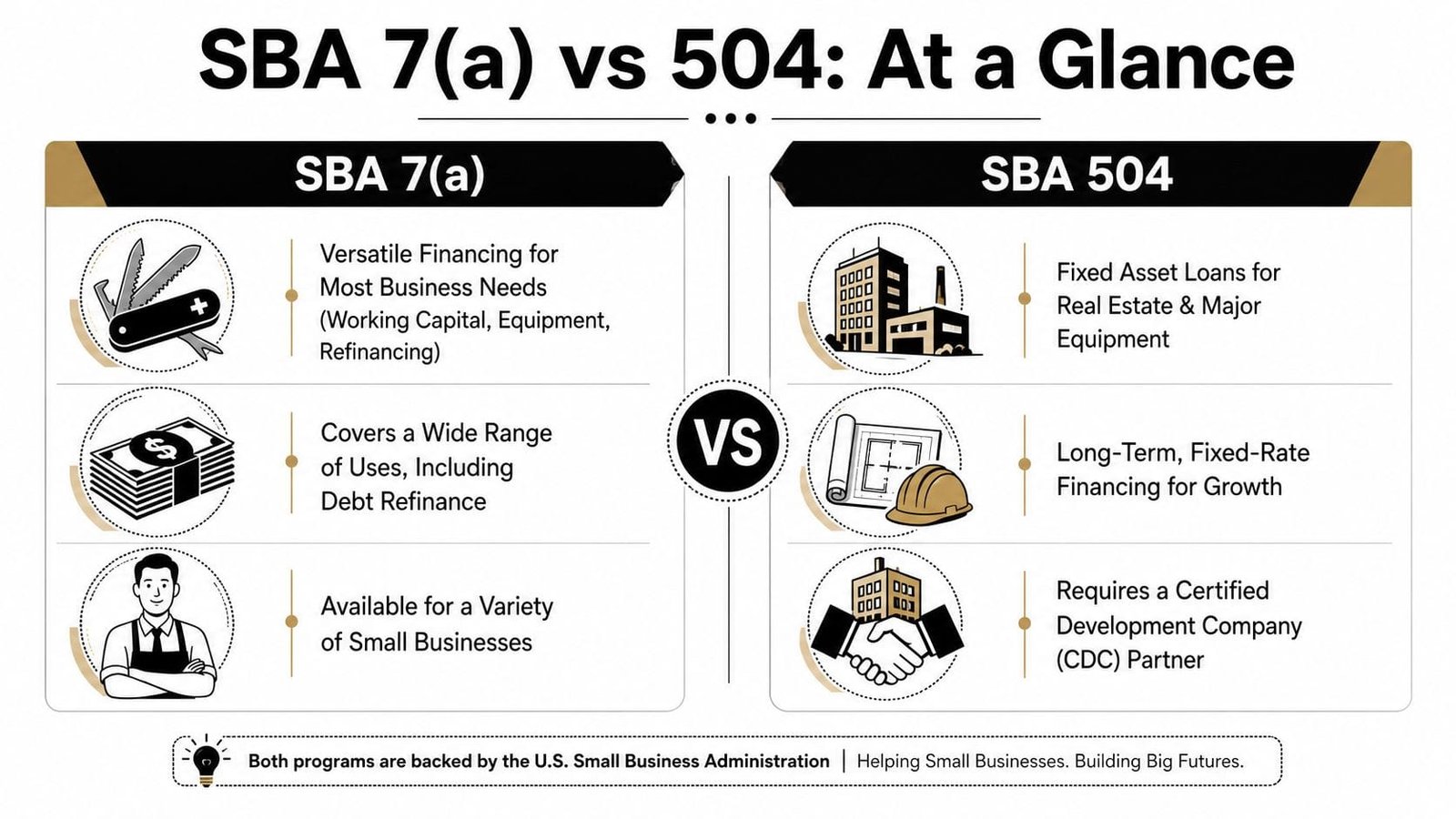

SBA 7a vs 504 At a Glance

If you only need the quick version, here it is. 7(a) is the versatile option. 504 is the specialist.

Quick comparison table

| Feature | SBA 7(a) | SBA 504 |

|---|---|---|

| Best use | Working capital, debt refinance, business acquisition, equipment, broader business needs | Commercial real estate and major equipment |

| Structure | Single loan through one lender with SBA backing | Three-party structure tied to a bank, CDC, and borrower |

| Maximum single loan amount | $5 million | Can support larger fixed-asset projects, with program structures discussed in specialist lending materials |

| Rate style | Often adjustable and tied to prime | Fixed rate on the CDC portion |

| Down payment | Flexible, depends on lender and use of funds | Typically built around a lower borrower contribution for eligible fixed assets |

| Collateral | Often required up to comparable commercial standards | Primarily secured by the financed asset |

| Speed | Usually faster | Usually slower because more parties are involved |

| Best fit | Owners who need flexibility | Owners buying long-term assets and want payment stability |

A lot of owners want one clean answer. There isn't one. There is only fit.

Later in this section, it helps to hear the basic framing in video form if you prefer that format.

What busy owners should take from this

First, don't use a 504 when you really need an operating loan. If part of the project includes inventory, payroll cushion, marketing, debt cleanup, or acquisition goodwill, 504 will feel like trying to carry groceries with a toolbox.

Second, don't use a 7(a) by default for a major property purchase if your real goal is low-down-payment, long-horizon asset financing. That's often where 504 is strongest.

Third, speed and simplicity favor 7(a). Structure and asset efficiency often favor 504.

A lot of borrowers compare these loans like they're two versions of the same car. They're not. One is a pickup truck. The other is a forklift.

Loan Purpose and Funding Structure

The biggest mistake I see is owners comparing SBA 7(a) and 504 on rates before they compare them on intended use. That's backwards. Purpose drives structure, and structure drives everything else.

The real dividing line

A 7(a) loan is designed for broad business use. It can cover operating needs, refinancing, acquisitions, equipment, and other growth uses. It's the loan you choose when your capital need doesn't fit neatly into one box.

A 504 loan is narrower by design. It is built for fixed assets, especially owner-used commercial real estate and major equipment. If your project is mostly a long-lived asset, 504 starts to look attractive very quickly.

The structure tells the story. The 504 program uses a three-party capital stack of 50% from a conventional bank, 40% from a Certified Development Company, and 10% from the borrower, while 7(a) is a single-loan product with up to an 85% SBA guarantee, according to Alabama 504's explanation of SBA 504 vs 7(a).

That's not a technical footnote. That's the entire personality of the loan.

Why structure changes strategy

A 7(a) is like hiring one general contractor to run the whole job. You have one primary financing relationship. The loan is easier to understand operationally, and that usually means a cleaner process.

A 504 is more like financing a building through a coordinated team. One lender handles the first mortgage position. The CDC handles the SBA-backed piece. You bring the equity contribution. That design is more rigid, but rigidity is not always bad. In fixed-asset finance, it can be exactly what you want.

Here's what that means in practice:

- Choose 7(a) when the deal has mixed uses. If you're buying a company and also need working capital, 7(a) handles that better.

- Choose 504 when the property or equipment is the point of the transaction. It's built for that lane.

- Don't underestimate administrative friction. More parties means more coordination, more document flow, and more chances for delay.

- Treat 504 as strategic infrastructure financing. It's not a catch-all growth loan. It's long-horizon capital for tangible assets.

My view: If the loan purpose needs explanation, start with 7(a). If the asset itself is the explanation, start with 504.

There's another layer strategic owners should care about. The 504 structure also ties financing to economic development logic, including job creation standards discussed in program guidance. That makes it more rule-bound than 7(a). For the right project, that discipline is fine. For a messy or evolving deal, it's a headache.

Comparing Financial Terms and Hidden Costs

Most owners fixate on the interest rate first. I get it. Rate is easy to compare. But in SBA 7(a) vs 504, the smarter comparison is cost plus flexibility over the life of the loan.

Rates matter less than most owners think

The usual shorthand is accurate but incomplete. 7(a) often carries adjustable pricing tied to prime. 504 gives you fixed-rate stability on the CDC portion and is often favored for long-term commercial real estate because of that stability.

That doesn't automatically make 504 cheaper in every situation. Fees, timing, intended hold period, and refinance plans all matter. A borrower who plans to hold a building for the long haul may value fixed-rate certainty. A borrower who expects to refinance or sell sooner may care more about penalty structure and process flexibility.

A lot of bad advice stems from people comparing note rate, ignoring the fee stack, ignoring prepayment, and acting surprised later.

If you want a practical framework for total borrowing cost, this walkthrough on how to calculate the real cost of a small business loan without the headache is worth reviewing before you sign anything.

The prepayment trap most articles ignore

This is the overlooked issue that deserves far more attention.

SBA 504 loans carry a 10-year prepayment penalty starting at 2.5% of the CDC balance, while 7(a) commercial real estate loans have a subsidy recoupment fee of 5% in Year 1, 3% in Year 2, and 1% in Year 3. A business refinancing in Year 2 faces a penalty 2.5 times higher with a 7(a) loan, based on WaFd Bank's SBA 504 vs 7(a) comparison.

That should change how you think about “flexibility.”

Here's the strategic takeaway:

| If you expect to… | Usually better fit |

|---|---|

| Hold the property for a long time and prioritize payment stability | 504 often makes more sense |

| Refinance, recapitalize, or sell within a shorter window | 7(a) can still work, but you need to model the recoupment fee carefully |

The irony is that many borrowers assume 7(a) is always the more flexible choice. Operationally, yes. On early payoff for commercial real estate, not necessarily in the way they expect.

Borrowers don't lose money on SBA loans because they chose the wrong headline rate. They lose money because they ignored what happens when the plan changes.

My advice is simple. Before choosing either product, decide whether this asset is something you'll likely keep, refinance, or sell on a shorter timeline. If you can't answer that, you're not ready to choose the loan.

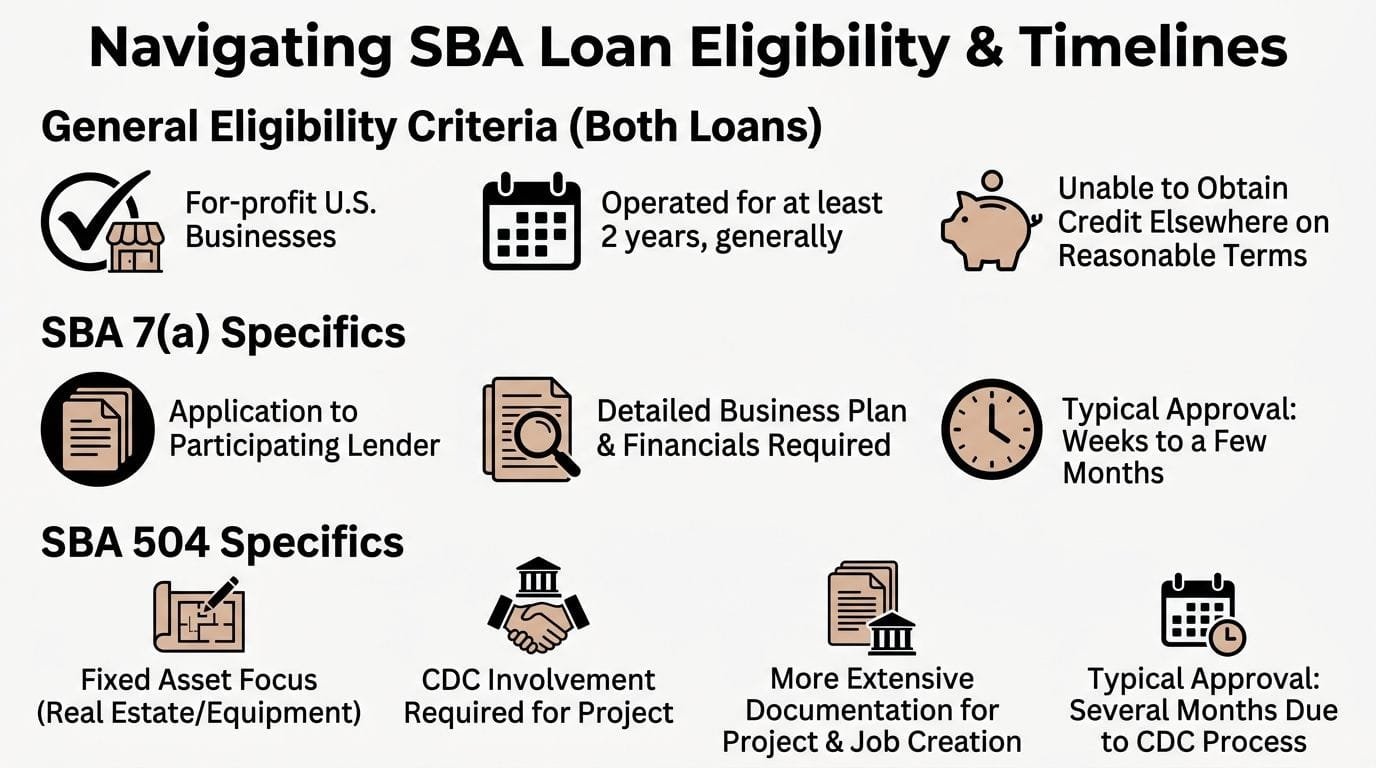

Navigating Eligibility and Application Timelines

Eligibility is where good deals either get structured correctly or get derailed by preventable mistakes. The broad rules matter less than the deal-specific ones.

Eligibility rules that actually affect the deal

For 504, the owner-occupancy issue is where many otherwise solid borrowers stumble. Too many comparison pieces treat occupancy as if it were a simple all-or-nothing rule. It isn't that simple in practice, especially for mixed-use properties.

For an owner buying a building with retail space, office space, storage, or a partial lease component, the details of how occupancy is measured can change whether the deal fits 504 at all. That's why mixed-use projects deserve careful structuring early, not after appraisal and legal work are already underway.

Job-creation expectations also matter more with 504 than with 7(a). That's another reason 504 works best when the project is stable, tangible, and aligned with long-term operating growth.

For 7(a), eligibility headaches usually center less on occupancy and more on underwriting quality, collateral, business performance, and whether the intended use of funds is well documented.

A simple rule helps here:

- Messy deal with several uses of proceeds: 7(a) is usually easier to shape.

- Clean real estate or equipment deal: 504 is often stronger if the property use fits program rules.

- Mixed-use property: don't assume ineligibility. Structure matters.

Speed, sequencing, and the 2026 change

If you care about speed, 7(a) usually has the edge because one lender can move the file through a simpler path. 504 adds coordination. More coordination usually means more time.

That timing issue matters even more now because of the recent rule change. Effective July 4, 2026, the SBA doubled the cumulative loan limit for combined 7(a) and 504 loans to $10 million. Eligible borrowers can now access up to $5 million through 7(a) and up to $5 million through 504 simultaneously, according to the SBA announcement on the new cumulative 7(a) and 504 limit.

That's a major development for capital-intensive businesses. It gives owners more room to pair operating flexibility with fixed-asset financing. But don't confuse that with a magic simplification. Combined structures still require sequencing and coordination.

If you're trying to time a transaction, this guide to realistic timelines for small business funding from application to cash in your account is useful because timing errors are expensive, especially when purchase contracts and real estate contingencies are involved.

If closing speed is non-negotiable, complexity is not your friend. That alone can tip the decision toward 7(a).

Real World Scenarios Which Loan for Your Business

Theory is helpful. Actual deal shapes are better. Here are three common situations where the answer becomes much clearer.

Scenario one the facility purchase

A profitable manufacturer wants to buy a larger facility and install heavy production equipment. This is classic 504 territory.

Why? Because the project centers on long-term fixed assets. The borrower is not mainly trying to fund payroll, inventory, or acquisition goodwill. The asset is the growth platform.

For commercial real estate, the SBA 504 loan's 90% loan-to-value ratio with only a 10% down payment is a significant benchmark advantage over 7(a), where lenders often demand 15% to 20% equity for high-value asset acquisitions, as noted earlier in the source used for loan structure guidance.

For this borrower, I'd lean 504 unless there's a compelling reason not to. The lower borrower cash requirement on the fixed asset side preserves liquidity for operations. That matters.

Scenario two the acquisition

A software company is buying a smaller competitor to gain customers, talent, and intellectual property. This is not a property-first deal. It is an operating business acquisition.

That makes 7(a) the practical choice. The value here includes items that don't sit neatly inside a building or machine. You need a loan product that tolerates broader uses and acquisition structure. 504 is too narrow for that job.

If the asset you're buying walks out the door every evening, 504 is usually the wrong tool.

The key point is not that 7(a) is “better.” It's that 504 was never designed for this transaction shape.

Scenario three the new location

A restaurant group wants to open a new location. The project includes build-out, kitchen equipment, launch expenses, and opening working capital. In this situation, owners often overcomplicate the decision.

If the deal includes a blend of asset and operating uses, 7(a) is usually the cleaner answer because one package can often cover the mixed needs. The flexibility is worth a lot when the business has to get open, staff up, market, and survive the ramp.

Could parts of the project align with 504 logic? Sure. But a loan structure that fits only part of the need can create more problems than it solves.

Here's the blunt version:

- Building-heavy deal: lean 504.

- Acquisition-heavy deal: lean 7(a).

- Mixed-use growth package with operating needs attached: usually 7(a).

That's the practical lens most owners should use.

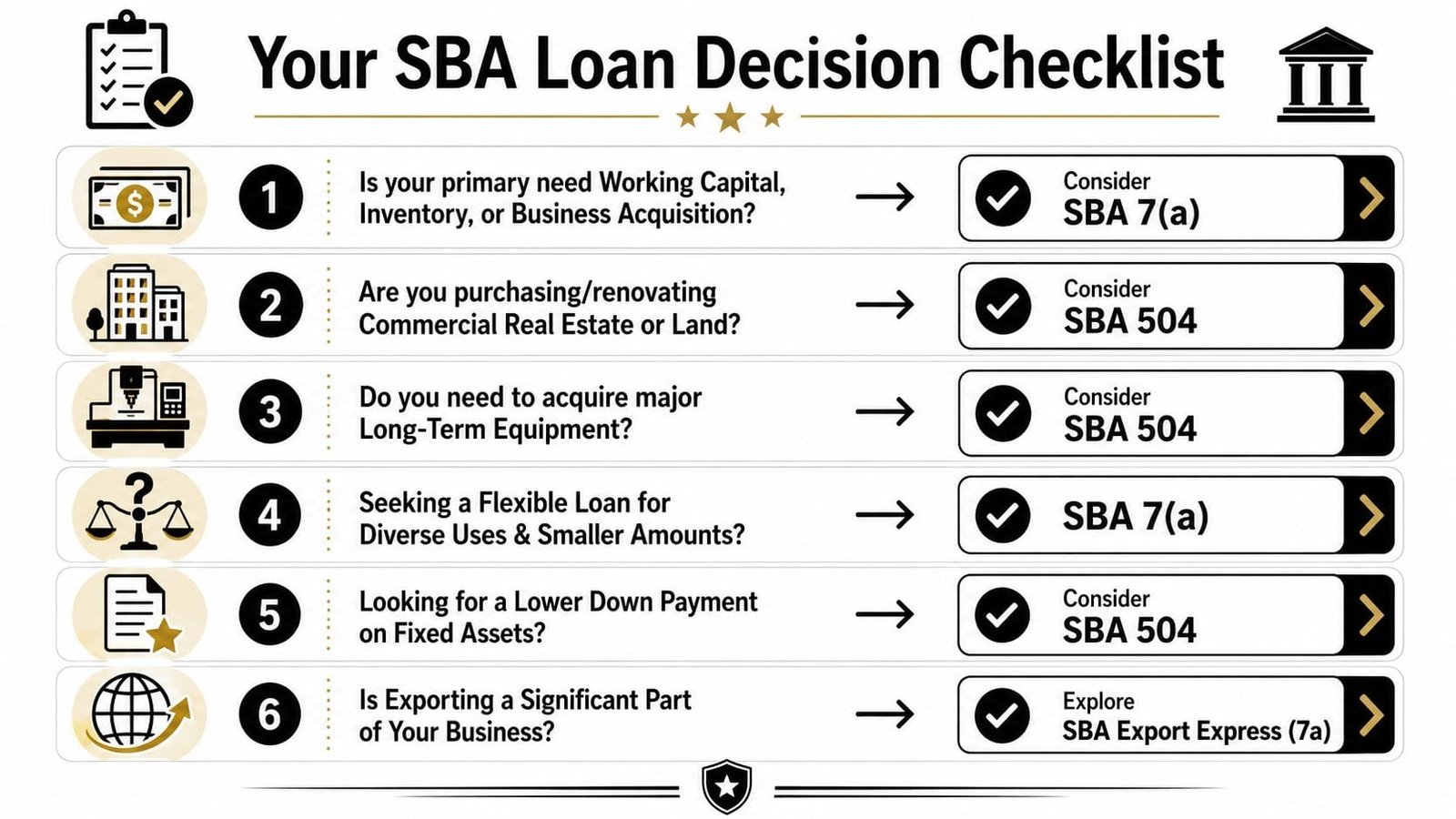

Your Final Decision Checklist and Next Steps

The right loan is usually obvious once you stop asking a generic question and start forcing a strategic one. What exactly are you financing, and what do you need the structure to do for you later?

A short decision filter

Carefully review this checklist:

- Need broad flexibility for working capital, debt refinance, or business acquisition? Choose 7(a) first.

- Buying owner-used commercial real estate or major equipment and want a structure built for long-term assets? Lean 504.

- Need to move fast with fewer parties and fewer moving parts? 7(a) usually wins.

- Want payment stability on a long-hold property? 504 deserves strong consideration.

- Expect you may refinance or sell earlier than planned? Model prepayment before you commit.

- Dealing with a mixed-use property? Don't guess. Structure the occupancy issue early.

What to prepare before you apply

Before you talk to lenders, get your deal story tight:

- Clarify the exact use of proceeds.

- Separate fixed-asset needs from operating needs.

- Decide whether speed or long-term structure matters more.

- Map your likely hold period.

- Flag any property occupancy complexity early.

Owners waste time when they shop loan products before they define the transaction. Define the transaction first. The right SBA lane usually follows.

If you want help pressure-testing the structure before you apply, Business Loan Warrior can help you compare options, check pre-approval without impacting credit, and move through SBA financing with both software efficiency and real underwriting guidance. For a business making a meaningful capital decision, that kind of clarity is worth having early, before the wrong loan choice becomes an expensive one.