You're probably staring at a loan checklist right now with a mix of urgency and dread. The business opportunity is real. Maybe it's a second location, a piece of equipment, a refinance, or a working capital cushion before a busy season. Then Form 413 shows up, and suddenly the question isn't just whether your business qualifies. It's whether you can present your personal finances clearly enough that the lender doesn't hit pause.

That's where many borrowers lose time.

The SBA personal financial statement isn't hard because the form is mysterious. It's hard because it forces clean lines between what you own personally, what your business owns, what you owe, and what you earn. If those lines are blurry, underwriters notice fast. If they're clean, the review moves much more smoothly.

Table of Contents

- Why the SBA Personal Financial Statement Matters More Than You Think

- Understanding the Anatomy of SBA Form 413

- A Step-by-Step Guide to Listing Your Assets

- Detailing Liabilities and Clarifying Business vs Personal Funds

- Your Essential Documentation Checklist for Form 413

- Common Errors to Avoid and Tips to Strengthen Your Application

Why the SBA Personal Financial Statement Matters More Than You Think

A borrower sits down to complete Form 413 and sees a business checking account with a healthy balance, a company truck, and equipment the business owns. The instinct is to list everything that shows financial strength. That instinct causes a lot of avoidable delays.

Form 413 is about you personally, not a general summary of everything tied to your business. Lenders use it to evaluate the financial strength, obligations, and credibility of the individual owners standing behind the loan request. If personal assets, business assets, and household assets are mixed together without clear support, underwriting stops to sort it out.

That line between personal and business property gets misunderstood all the time. A business bank account is not personal cash just because you own the company. Company equipment is not your personal asset unless you own it outside the business. Your ownership interest in the business may belong on the form, but the business's assets usually do not appear item by item under your personal holdings. That distinction matters because lenders compare Form 413 to business tax returns, personal tax returns, account statements, and entity records. When those records point in different directions, the file gets slower and harder to approve.

A good Form 413 does not require perfect finances. It requires numbers you can support, ownership you can explain, and balances that match the rest of the application.

What the form really does

The SBA personal financial statement provides the personal side of your loan file. Your business financials show how the company performs. Form 413 shows who is backing the debt, what they own, what they owe, and whether their financial picture is presented clearly.

That is why this form carries more weight than many applicants expect. It often reveals whether an owner keeps clean boundaries between personal and business money. In practice, that tells a lender a lot. Clean separation suggests reliable records and fewer surprises. Blurred lines suggest follow-up questions, document requests, and possible concerns about how cash moves.

If you want a broader view of what lenders review alongside Form 413, this guide on top SBA loan qualification requirements is a useful companion.

The SBA's own Form 413 instructions also make the purpose clear by asking for a signed statement of personal assets and liabilities, plus supporting details on real estate, notes payable, and other obligations.

Practical rule: If a lender has to guess whether an asset is yours personally or belongs to the business, expect a request for clarification before the file can move ahead.

What works and what doesn't

What works:

- Using current statements that support the values listed

- Showing business ownership as equity interest instead of dropping business cash and equipment into personal asset lines

- Listing liabilities in full even if the payment is current and the balance is unpleasant

- Keeping personal and business accounts separate before the application is ever submitted

What doesn't:

- Estimating values from memory when statements are available

- Treating business balances like personal liquidity

- Listing the same value twice, such as counting business equity and then separately counting business cash as a personal asset

- Leaving blanks for items you plan to explain later

Borrowers sometimes assume the form is mainly a test for errors. In actual underwriting, it is more of a consistency check. A clear, supportable Form 413 gives the lender fewer reasons to pause, and that can make the difference between a smooth review and a long chain of follow-up emails.

Understanding the Anatomy of SBA Form 413

A borrower hands over a Form 413 that looks complete, but the file still stops. The reason is often simple. Personal assets are mixed with business assets, and the numbers no longer tell a clean story.

Form 413 works as a dated snapshot of your personal finances. Lenders read it to answer a practical question: what do you personally own, what do you personally owe, and how clearly can that be verified on the date listed on the form. If the form shows business cash, business equipment, or company real estate as if those items were personally owned, underwriting usually pauses until the ownership issue is sorted out.

Who has to complete it

For SBA lending, Form 413 is generally required from each proprietor, general partner, managing member, or owner with a significant ownership stake, based on current SBA use of the form and lender practice. The current official SBA Form 413 also shows that the statement is signed personally and includes identifying information used to match the form to the rest of the loan file.

The spouse signature question catches borrowers off guard. The practical rule is easier than the wording makes it sound. If the application relies on jointly held assets, or if state law and ownership structure make the spouse financially relevant to the disclosure, expect the spouse section to matter and expect the lender to ask for clarity.

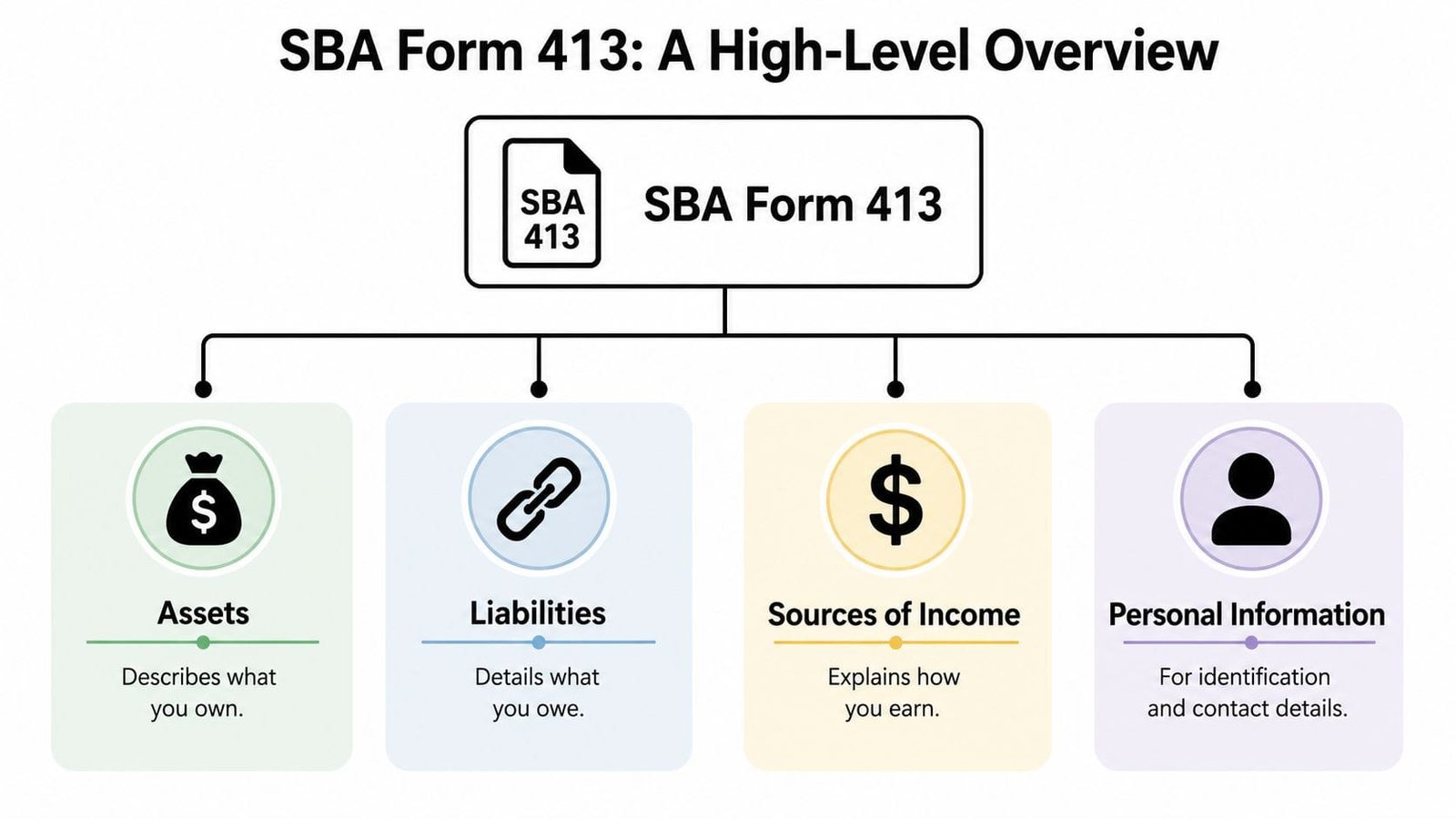

The four parts lenders focus on

The form can be broken down into these key areas:

| Section | What it tells the lender | What borrowers often miss |

|---|---|---|

| Assets | What you personally own as of the statement date | Title and ownership control whether an item belongs here |

| Liabilities | What you personally owe | Debts still belong on the form even if payments are current |

| Sources of income | How income reaches your household | The amounts should make sense alongside tax returns and statements |

| Personal information and signatures | Who is making the disclosure and certifying it | Missing or inconsistent signatures can stop processing quickly |

Borrowers often focus on the numbers and miss the ownership question. Lenders do the opposite. A personal checking account belongs on the form. A business operating account usually does not, even if you are the sole owner. Your company interest may belong as an equity asset, but the company's underlying cash and equipment generally should not be listed again as personal assets. That is one of the most common Form 413 mistakes I see, and it creates avoidable delays because the balance sheet looks stronger on paper than the documents support.

The sections with extra detail

Form 413 also asks for supporting detail beyond the summary balance sheet. The SBA SOP 50 10 lender guidance explains the broader credit review framework lenders use, and that is why real estate owned, notes payable, other liabilities, and related disclosures matter so much. These sections give the underwriter context for the totals shown on page one.

Short answers can cause long follow-up requests.

If a borrower lists personal property, unpaid taxes, or life insurance with cash surrender value, the form usually needs enough detail for the lender to tell what the item is, who owns it, and whether the value is realistic. This is also where borrowers with complex estates or trusts should be careful. If an asset has legal protections, restrictions, or shared ownership, clean disclosure matters more than a high estimated value. For readers dealing with that kind of planning, this overview of asset protection for high net worth individuals gives useful legal context, though your loan file still has to show what is personally available and documentable.

If you want to place Form 413 in the full underwriting sequence, this walkthrough of the SBA loan application process for small business owners shows where this statement fits in the larger file.

A Step-by-Step Guide to Listing Your Assets

A borrower shows $180,000 in “cash and savings” on Form 413. The bank statements arrive, and half of that money sits in the business operating account. The loan does not die there, but it usually stops cold until the numbers are reworked. That is one of the most common delays I see, and it starts with a simple misunderstanding. Form 413 is about what you own personally, not everything you control.

Use a practical rule. If the asset is titled in your personal name, or jointly in a way that gives you a personal ownership interest, it usually belongs on your personal financial statement. If it is titled to the company, it belongs on the business balance sheet, even if you are the sole owner. Owners blur that line all the time with bank accounts, vehicles, real estate, and investment accounts.

Start with assets you can verify quickly

Begin with the items that tie cleanly to a statement. That gives you a reliable base before you move into assets that require judgment.

Cash on hand and personal bank balances

Use recent statements for personal checking, savings, money market, and CDs held in your name. Do not pull in the company's operating account, payroll account, or merchant reserve just because you can access them. Access is not ownership.Stocks, bonds, and brokerage accounts

Use the current statement value, not your original cost. Underwriters look at present value because that is what the asset contributes to your balance sheet today.Retirement accounts

Personal IRAs and 401(k)s usually belong here. Label them clearly. A retirement account is still an asset, but it is not the same as unrestricted cash, and lenders read it differently.

A simple worksheet helps. List the asset, whose name is on it, how it is titled, the current value, and the document that supports it. That five-column check catches many of the errors that create follow-up requests.

Treat real estate like a file within the file

Real estate entries deserve more care than a quick estimate from memory. For each property, the lender is trying to understand value, debt, ownership, and whether your number is supportable.

Have these details ready:

- Property address

- Current estimated market value

- Mortgage balance

- How title is held

- Your ownership percentage, if shared

Use one reasonable valuation method and stay consistent. A recent mortgage statement, tax assessment, broker opinion, or appraisal can all be useful, depending on the situation. Inflated values create problems because they invite a challenge. A conservative number with support moves faster than an aggressive number that nobody can verify.

List business ownership correctly

If you own part or all of a company, that ownership interest may belong on Form 413. The business checking account does not. The company truck does not. The company-owned building does not, unless title is in your personal name.

That distinction matters well beyond lending. Owners with larger estates often review topics like asset protection for high net worth individuals because title, control, and liability do not always sit in the same place. Form 413 works the same way. Control over a business asset does not make it a personal asset.

A useful analogy is a rental house owned by an LLC. You may control the LLC, approve repairs, and collect the economic benefit. But if the property is titled to the LLC, it is not listed on your personal statement as personally owned real estate. Your asset is the value of your ownership interest in the LLC.

Handle life insurance and personal property with restraint

These categories are often overstated or skipped entirely. Neither approach helps.

Life insurance

Report the cash surrender value if the policy has one. Do not list the death benefit as an asset. If you do not know the surrender value, ask the carrier for it.Personal property

Use care with jewelry, collectibles, vehicles, art, and similar items. List material items when the form calls for them, but use reasonable values you can explain. Sentimental value has no place on Form 413.Use one valuation date

Keep your numbers anchored to the same general point in time. A brokerage balance from this week, a real estate guess from last year, and a loan payoff from three months ago create a balance sheet that does not hold together.

A strong asset section reads like an inventory prepared for scrutiny. Each item belongs to the right owner, carries a supportable value, and matches the documents behind it. That is how you keep Form 413 from turning into a long chain of avoidable lender questions.

Detailing Liabilities and Clarifying Business vs Personal Funds

A borrower sits across from me and says, “I own 100 percent of the company, so I listed the business cash with my personal funds.” That single choice can stall an otherwise workable SBA file for days because it blurs the line underwriters need to see clearly.

Liabilities do more than show what you owe. They show how much of your personal cash flow is already committed each month, and they give the lender a way to test whether the rest of the form is internally consistent. Leave off a credit card, an auto loan, a personal note, or a mortgage, and the gap usually shows up when the credit report, tax return, or account statements are reviewed.

The line that causes trouble

The most common delay I see is not a math error. It is ownership confusion.

Form 413 is a personal financial statement. That sounds obvious, but borrowers regularly mix in business checking balances, company vehicles, or debts owed by the business because they control the company and use those resources every day. Control is not the test. Legal ownership and personal liability are the tests.

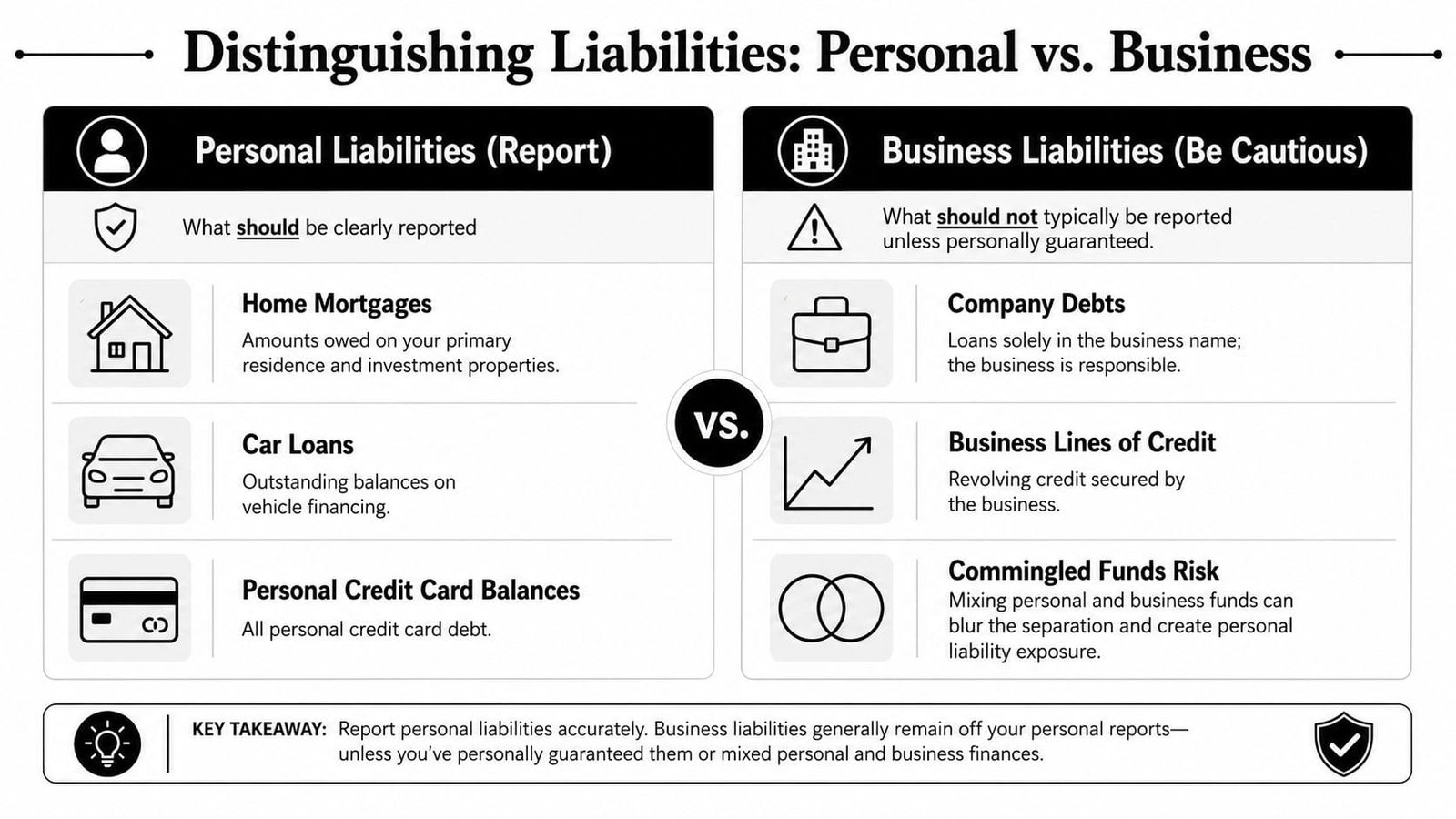

Use this quick rule:

- Personal credit cards belong on Form 413

- Personal auto loans belong on Form 413

- Mortgages in your own name belong on Form 413

- Business loans signed only by the company usually belong on the business financials

- Business debts you personally guaranteed often need to be disclosed because you carry personal responsibility if the business cannot pay

- Business bank accounts belong on the business financials, even if you are the sole owner

A good way to sort gray areas is to ask two separate questions. Who owns it? And who is legally obligated to repay it? Those answers matter more than who uses the asset or who benefits from the business.

Sole proprietors and single-member LLC owners struggle with this point more than anyone else. Day to day, the money can feel interchangeable. Underwriting does not treat it that way. Two drawers may sit in the same desk, but the lender still needs each document in the right drawer.

How to handle business debt on a personal statement

Business obligations are not automatically personal liabilities. The key issue is whether your name is attached.

If the company borrowed money and only the company signed, that debt is generally a business obligation. If you signed a personal guaranty, co-borrowed, or pledged personal collateral, the debt has a personal dimension the lender will want explained. The SBA's borrower information materials and Form 413 instructions make the same basic point. List what you personally owe, and be prepared to clarify contingent or guaranteed obligations when the loan package calls for it, using SBA resources such as the Form 413 instructions and guidance.

That distinction matters in practice. A company line of credit can sit on the business balance sheet, but if you personally guaranteed it, an underwriter may still ask how that exposure affects your personal repayment capacity.

Income needs clean labeling too

The income section creates trouble for the same reason. Borrowers mix salary, owner draws, distributions, and gross business revenue as if they are interchangeable. They are not.

Use figures you can trace to payroll records, tax returns, K-1s, benefit statements, or other support. If you receive wages from your company, report wages. If you take irregular draws, label them accurately and be ready to explain the pattern. If rental property produces income, use a number that reflects expenses, not just the top-line rent.

For borrowers who keep uneven records, a simple source-document habit helps. The same discipline behind essential source documents for HMRC applies here. Start with the record that proves the number, then carry that number onto the form.

| Income type | Good reporting habit | Common problem |

|---|---|---|

| Salary or wages | Match payroll or W-2 records | Treating owner draws as wages |

| Investment income | Use statements and tax reporting | Estimating from memory |

| Real estate income | Show income after relevant expenses | Reporting gross rent only |

| Other income | Name the source clearly | Using vague labels with no support |

Clean separation speeds review. When personal assets, personal liabilities, business assets, and business obligations are each presented in their proper place, the form reads like a reliable financial snapshot instead of a set of estimates that need to be untangled.

Your Essential Documentation Checklist for Form 413

The easiest way to make Form 413 harder is to fill it out first and hunt for support later. Do the opposite. Gather the paper trail first, then complete the form.

That approach prevents two problems at once. First, it reduces guesswork. Second, it keeps your numbers consistent across statements, tax returns, and loan exhibits.

What to gather before you start

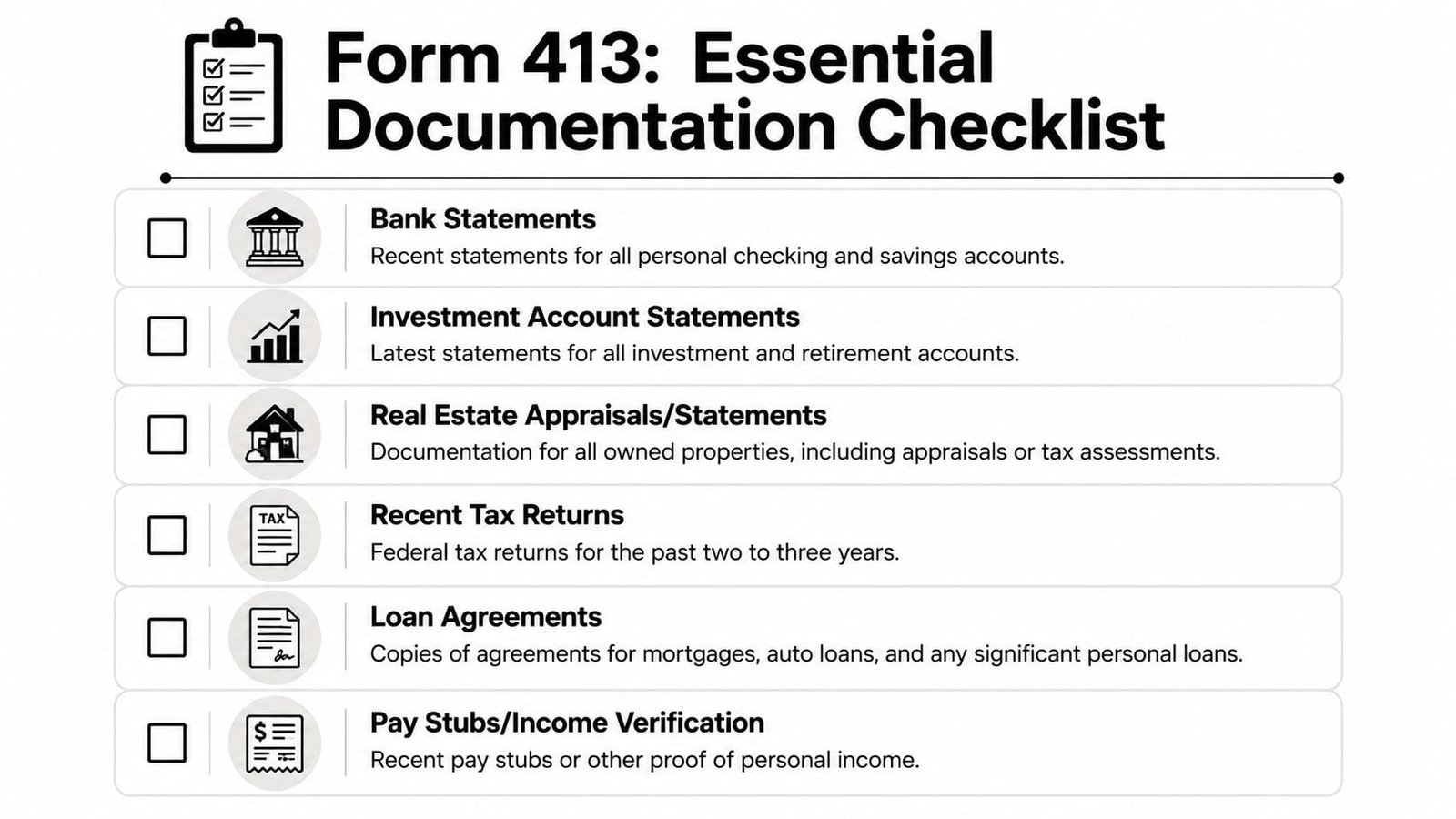

Use this checklist as your working file:

- Personal bank statements for checking, savings, and money market accounts

- Investment account statements for brokerage and retirement accounts

- Mortgage statements for each property you own personally

- Property value support such as tax assessments, appraisals, or broker opinions

- Auto loan statements showing payoff balances and monthly payments

- Credit card statements for personal cards

- Student loan and personal loan statements

- Life insurance policy information showing cash surrender value, if applicable

- Income support such as pay stubs, payroll reports, benefit statements, or other clear proof

- A list of business interests with documentation supporting ownership and estimated value if required

If you already keep records organized for tax or audit purposes, that habit pays off here. If you don't, this is a good time to fix the system. Even resources outside lending, like this overview of essential source documents for HMRC, are useful because the core principle is the same: original records make reporting cleaner and defensible.

This walkthrough can also help if you want a visual explanation before assembling your package.

How to organize the file

Don't send a lender a pile of unnamed PDFs.

Use a simple folder structure:

- Assets

- Liabilities

- Income

- Real estate

- Insurance

- Signed form

Inside each folder, name files in plain English. For example: “Personal Checking June Statement” or “Primary Residence Mortgage Statement.” Good naming saves time when underwriting asks a follow-up question.

The borrower who can retrieve a document in thirty seconds usually has a smoother process than the borrower who says, “I know I have that somewhere.”

Common Errors to Avoid and Tips to Strengthen Your Application

A borrower sends in Form 413 showing a healthy net worth. Two days later, underwriting asks a simple question: why is the business operating account listed as a personal asset? That single mistake can stall a file fast, because it raises a bigger concern. If ownership lines are blurry on the form, the lender starts wondering where else they are blurry.

That is one of the most common avoidable problems I see.

Form 413 does more than list what you own and owe. It shows whether you understand the boundary between you and your business. For SBA lending, that boundary matters. A sole owner may feel like the business account is "my money," but if the legal owner is the company, it usually does not belong on your personal financial statement as a personal cash asset.

Errors that trigger avoidable delays

Some issues are clerical. Others make the lender question the whole file.

Using the wrong date or mixed reporting periods

If the bank statement is current but the mortgage balance is from months ago, the form stops reading like a snapshot. It reads like a collage.Listing business assets as personal assets

This is the big one. Business checking, company equipment, and assets owned by an LLC or corporation should not be dropped into the personal asset section just because you control the business. If you own an interest in the company, that ownership interest may belong on the form. The company's individual assets usually do not.Forgetting contingent or partial obligations

Personal guarantees, co-signed debts, and installment obligations still matter even if you are not the only party responsible.Net worth math that does not reconcile

Underwriters do not ignore arithmetic problems. If the totals are off, they will verify more aggressively.Unsigned or incomplete forms

An unsigned Form 413 is unfinished. Missing schedules or omitted details create the same problem.

What actually makes the application stronger

Clean reporting builds trust faster than optimistic reporting.

A modest personal balance sheet, supported by statements and prepared carefully, is stronger than a larger one built on rough estimates. Underwriters review Form 413 alongside tax returns, credit reports, bank statements, and business financials. If those documents line up, the file feels reliable. If they conflict, the review slows down.

Clarity also helps more than volume. Ten extra PDFs do not fix a confusing form. A clear explanation does. If you pull figures from statements before entering them into Form 413, tools like a comprehensive guide for PDF data extraction can help with the mechanics, but the borrower still needs to verify every number and make sure each asset belongs on the personal side of the line.

The business versus personal line borrowers miss

Good applications are often won or lost at this stage.

Use a simple test. Ask, "Who legally owns this asset or owes this debt?" Not "Who uses it?" Not "Who benefits from it?" Legal ownership is the starting point.

For example:

| Common mistake | Better treatment |

|---|---|

| Listing the company operating account as personal cash | List your ownership interest in the business, if applicable, not the company cash itself |

| Listing business equipment under personal property | Keep equipment with the business unless you own it personally and lease it to the company |

| Omitting a personal guarantee on business debt | Disclose the guarantee or contingent liability if the form or lender requires it |

| Estimating values from memory | Use recent statements, payoff letters, or other current support |

That distinction sounds technical, but it affects credit judgment. A lender trying to assess personal liquidity needs to know what cash you can access personally, without stepping through the company entity. Mixing those categories can overstate strength on paper and create credibility problems once underwriting traces the source.

A lender-side checklist before you submit

Review the form the way an underwriter will.

Can a lender tell what you own personally, separate from what the business owns?

Can a lender see every meaningful debt that touches your household or your guarantees?

Do the values tie back to documents you can produce quickly?

If a number looks high or unusual, is there a plain-English explanation ready?

Those are practical questions. They drive file speed.

If you want a broader view of approval problems beyond Form 413, read this breakdown of top reasons SBA loans get denied and how to avoid them.

A strong personal financial statement is organized, supportable, and honest about the line between personal wealth and business value. Borrowers who get that line right usually move through underwriting with fewer surprises.