You need capital this quarter, not six months from now. A supplier offers a better buy if you move fast. Payroll is covered, but cash is tight because receivables are lagging. Or you want to launch a campaign before a seasonal window closes, and you don't want to put your building, trucks, or equipment on the line to do it.

That's where unsecured business loans enter the conversation. Not as a magical source of money, and not as the cheap option. They are a speed-and-flexibility tool. If you use them for the right job, they can protect your operating momentum. If you use them for the wrong job, they can squeeze cash flow hard.

The strategic question isn't just "Can I get approved?" It's "Is fast, collateral-free capital worth the cost and repayment pressure for this specific decision?"

Table of Contents

- What Are Unsecured Business Loans Really

- Unsecured vs Secured Loans A Strategic Trade-Off

- Qualifying for Funding Without Collateral

- The True Cost of Unsecured Financing

- Your Step-by-Step Application Guide

- Smart Ways to Use and When to Avoid Unsecured Loans

- Frequently Asked Questions About Unsecured Loans

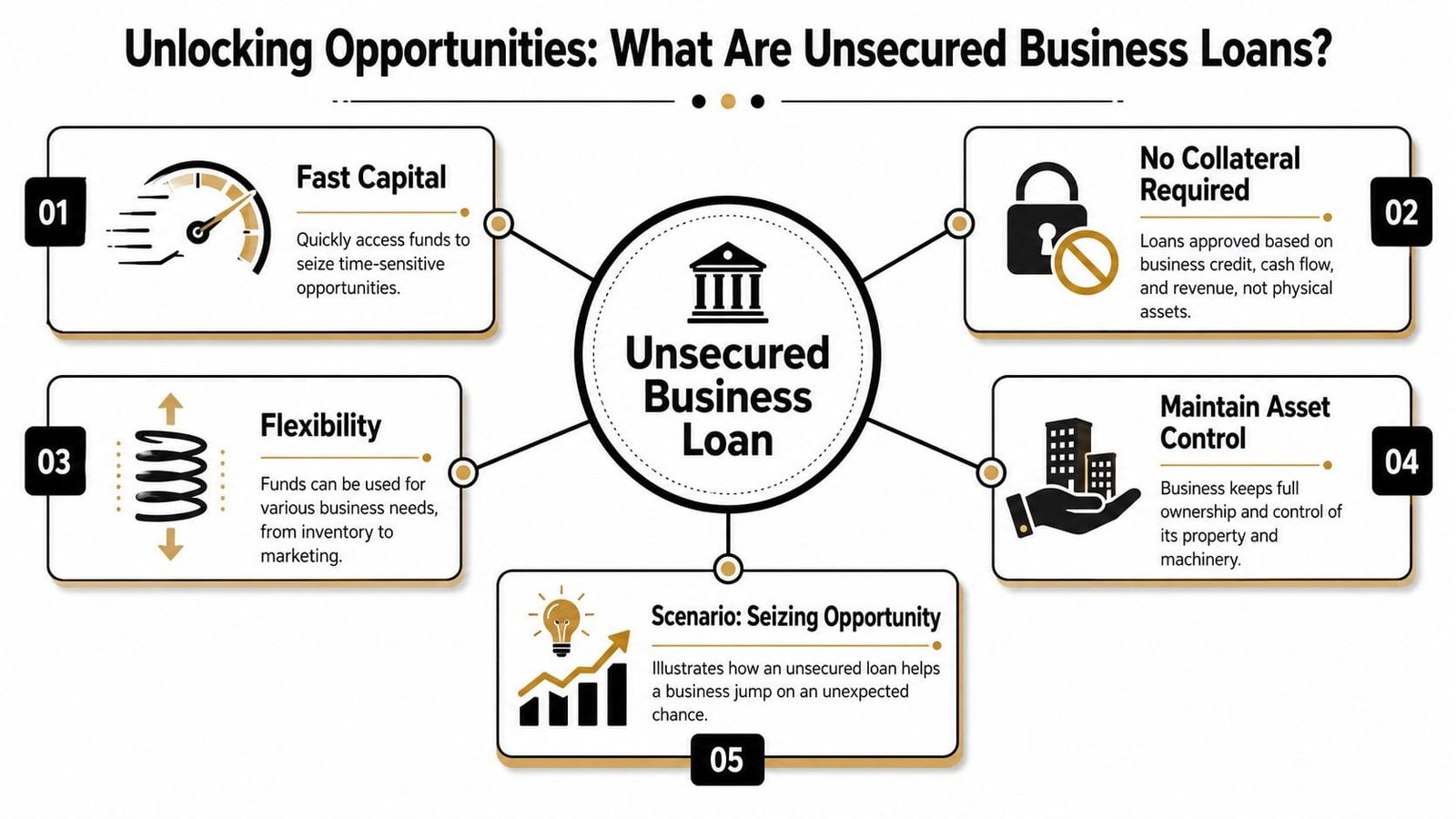

What Are Unsecured Business Loans Really

A customer pays late. Payroll is due Friday. Inventory has to be ordered now, not three weeks from now. That is the situation unsecured business loans are built for.

An unsecured business loan gives a company access to capital without tying the deal to a specific asset such as equipment, vehicles, or real estate. The lender is making a judgment about repayment from business performance and the owner's profile, rather than taking a direct claim on one named asset.

That distinction changes the decision from a simple funding question to a business strategy question. You are choosing speed and asset preservation, while accepting a higher price and tighter cash flow discipline. For many growing companies, that trade makes sense. For others, it creates pressure they do not need.

Why owners choose them

Owners usually pick unsecured financing for one reason. Time.

A fast approval can help cover a gap between paying suppliers and collecting receivables, fund inventory before a seasonal spike, or take on a contract that would otherwise be missed. In those cases, the question is not just "What rate can I get?" The better question is "What does delay cost me?"

That is why unsecured loans are often best used for short-cycle business needs where speed has economic value. The Bipartisan Policy Center's review of the small business financing market shows many small firms still struggle to get all the financing they need. In practice, that pushes owners toward products that can close faster, even when the cost is higher.

One warning from experience. Fast money fixes timing problems. It does not fix weak margins, inconsistent sales, or poor collections.

For a broader look at how this option stacks up against collateral-based borrowing, review this breakdown of secured vs unsecured business loans.

What the lender is really underwriting

With unsecured financing, the lender is not asking, "What can we seize if this goes bad?" The lender is asking, "How likely is this business to keep making its payments on time?"

That shifts the focus to cash flow quality. A company with steady deposits, decent margins, and clean account conduct often looks stronger than a company with higher revenue but erratic inflows. I tell owners to treat underwriting like a stress test on their operating rhythm. Lenders want proof that the business can absorb a monthly payment without throwing the rest of the company off balance.

They usually zero in on four areas:

- Owner credit history: personal credit still matters, especially for small firms with a personal guarantee

- Revenue consistency: stable monthly sales usually beat one or two standout months

- Time in business: longevity suggests the company has made it through ordinary shocks

- Cash flow coverage: lenders want room between incoming cash and fixed obligations

The U.S. Small Business Administration notes that some business financing may not require specific collateral, but owners may still be asked for a personal guarantee or a blanket lien on business assets. If you want to see how lenders document claims on collateral in secured deals, this guide on security agreements gives useful context.

That last point catches many borrowers off guard. "Unsecured" does not always mean the lender has zero recourse. It often means there is no appraisal and no loan built around one named asset. The risk still lands somewhere, and often part of it lands on the owner.

In practical terms, unsecured business loans buy speed and flexibility. You pay for that with higher cost, stricter underwriting, and less room for error in your monthly cash flow.

Unsecured vs Secured Loans A Strategic Trade-Off

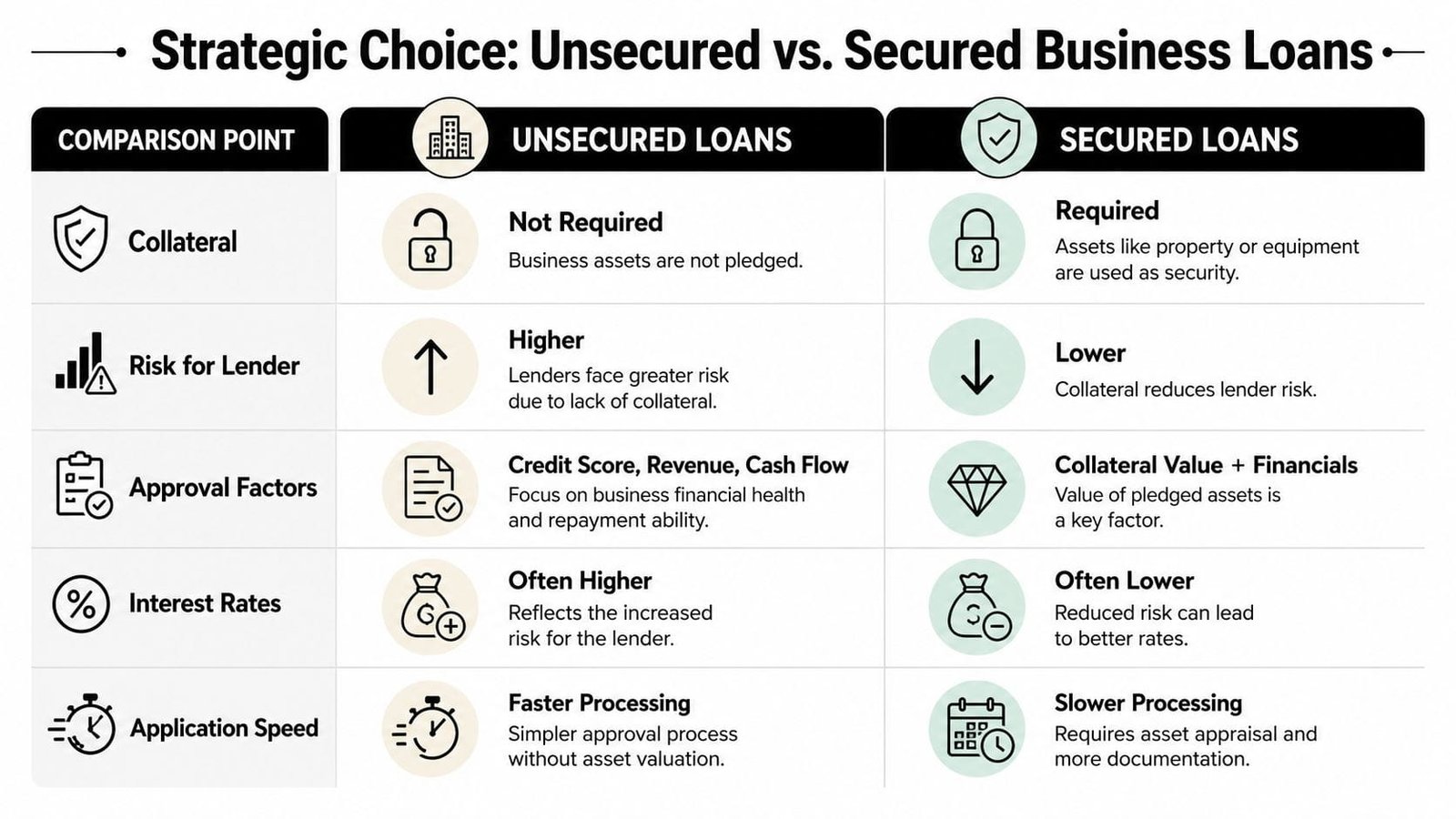

The difference between unsecured and secured borrowing isn't paperwork. It's how risk gets allocated. With a secured loan, the lender has a claim on a defined asset. With an unsecured loan, the lender has to trust the business's future cash flow and the borrower's profile.

That one shift affects pricing, approvals, and how fast money can move.

The core trade-off

If you care most about preserving assets and moving fast, unsecured financing usually fits better. If you care most about minimizing borrowing cost over a longer horizon, secured financing often wins.

PNC explains the pricing logic clearly. The risk shift from secured to unsecured loans creates a premium of 2 to 10 percentage points, and in 2026 APRs for unsecured term loans span 7% to 45% while comparable secured loans are lower, as outlined in PNC's overview of how unsecured small business loans work and what lenders require.

When lenders can't recover funds through asset liquidation, they charge for that uncertainty upfront.

If you're not fully clear on what it means to pledge business assets, a solid guide on security agreements is worth reading before you sign any secured deal. Too many owners focus on the rate and ignore the legal reach of the lender's claim.

Unsecured vs secured business loans

| Feature | Unsecured Loan | Secured Loan |

|---|---|---|

| Collateral requirement | No specific collateral pledged | Specific asset is pledged |

| Interest rates | Usually higher | Usually lower |

| Funding speed | Often faster | Often slower |

| Loan amounts | Often more limited by cash flow and profile | Often stronger for larger needs |

| Qualification difficulty | Heavy focus on credit, revenue, and consistency | May be easier if strong collateral offsets weaknesses |

The strategic mistake is comparing these products as if they're interchangeable. They aren't. A short-term inventory buy and a long-term equipment purchase should not be financed the same way.

A useful framework is simple:

- Choose unsecured when the value is in speed, flexibility, or avoiding asset risk.

- Choose secured when the asset itself supports the financing need and the lower cost matters more than speed.

- Pause and compare if you're financing a mixed purpose need, like expansion plus working capital. In that case, it helps to review a deeper breakdown of secured vs. unsecured business loans and which one fits your business best.

This isn't just a financing decision. It's a balance-sheet decision and a risk-management decision.

Qualifying for Funding Without Collateral

You need cash fast for inventory, hiring, or a short runway gap. The lender is looking at the same request from the other side of the table and asking one question: if there is no asset to seize, what makes repayment likely enough to approve this file?

That changes the entire approval process. With unsecured business loans, lenders focus less on what you own and more on how your business behaves. They want to see steady revenue, clean account activity, sensible margins, and an owner who manages obligations well. A strong file says, "this business generates enough cash to carry the payment without strain."

What creditworthiness means in practice

Underwriters often sort risk using the Five Cs of Credit. In unsecured lending, collateral matters less, so the other parts carry more weight.

- Character: Personal credit still matters. It shows whether you pay on time, how much debt you already carry, and whether there are recent problems that suggest stress.

- Capacity: This is the big one. Lenders want proof that the business can make the payment from normal operating cash flow, not from wishful forecasting.

- Capital: Cash reserves and retained earnings matter because they give the business a buffer when sales dip or customers pay late.

- Conditions: The use of funds has to make business sense. Covering a temporary inventory build before a busy season is easier to defend than plugging a long-running cash leak.

- Collateral: There may be no specific asset pledged, but that does not mean the lender ignores downside risk. It means the file has to stand up on cash flow and credit.

I see owners get tripped up here all the time. Revenue alone does not win approvals. A business can show healthy deposits and still get declined if overdrafts are frequent, debt payments already look heavy, or margins are too thin to absorb one more fixed obligation.

A realistic qualification checklist

Before applying, review your file like an underwriter would.

- Check your personal credit first: Fix reporting errors, pay down obvious revolving balances where possible, and be ready to explain any recent late payments or collections.

- Review business bank statements: Lenders look for consistency. Large swings, repeated negative days, and unexplained transfers can raise questions fast.

- Make sure the numbers agree: Your bank statements, P&L, balance sheet, and tax returns should tell the same story. If they do not, expect extra scrutiny or a lower offer.

- Define the use of funds clearly: "Working capital" is acceptable, but a specific plan is better. "Buy fast-turn inventory for signed purchase orders" gives the lender a clearer repayment path.

- Clean up admin loose ends: Missing filings, stale licenses, and unresolved documentation issues can slow or derail approval. A quick review of tax, GDPR, and IR35 compliance can help if your back office is messy.

Good applications reduce guesswork.

That is the strategic angle many owners miss. Qualifying for unsecured funding is not just about getting a yes. It is about getting a yes on terms your cash flow can support. The cleaner and more explainable your file is, the more likely you are to preserve options on rate, term length, and approval size.

Clarity matters too. If your numbers are decent but your explanation is vague, the lender usually assumes the risk sits somewhere they have not uncovered yet.

The True Cost of Unsecured Financing

A lot of owners shop loan offers the way people shop airline tickets. They look at the first number on the screen and assume that's the full story. It usually isn't.

With unsecured financing, the right question is not "What's the rate?" It's "What will this cost my business, month by month, and over the full life of the loan?"

Rate versus APR

An interest rate tells you the borrowing price in a narrow sense. APR gives a fuller picture because it can reflect fees and other financing charges along with the rate. When you're comparing offers from banks, online lenders, and other non-bank products, APR is usually the closest thing to an apples-to-apples measure.

That matters because unsecured products can carry more than just interest. Depending on the lender, you may also see origination fees, underwriting fees, documentation fees, or prepayment rules that change the economics if you repay early.

A short term can also distort your intuition. The payment may look manageable on a spreadsheet until you compare it against the rhythm of your receivables, payroll cycle, rent, and vendor obligations. Cash flow stress doesn't come from the annual cost alone. It comes from repayment timing.

How to pressure-test an offer

Use a simple screen before signing:

- Map the payment to cash flow: If your revenue is uneven, fixed repayment can still be painful even when the business is profitable.

- Ask whether the rate is fixed or variable: Variable pricing can add uncertainty at exactly the wrong time.

- Check prepayment language: Some lenders reward early payoff. Others don't.

- Look at total dollars repaid: That's the number your business bank account will feel.

- Tie the loan to a use case: If the capital funds a fast-return move, high cost can still be rational. If the return is slow or vague, it usually isn't.

Here's a practical way to think about it. If you borrow to cover a short-lived gap or seize a quick-turn opportunity, you're buying time. If you borrow for a long-horizon project with delayed payoff, you're layering an expensive payment on top of an uncertain return.

That mismatch is what hurts owners. Not the existence of debt, but the wrong debt for the wrong job.

Your Step-by-Step Application Guide

The fastest applications aren't always the strongest ones. The strongest ones are the files where the owner has already answered the underwriter's next three questions before they ask them.

Start there.

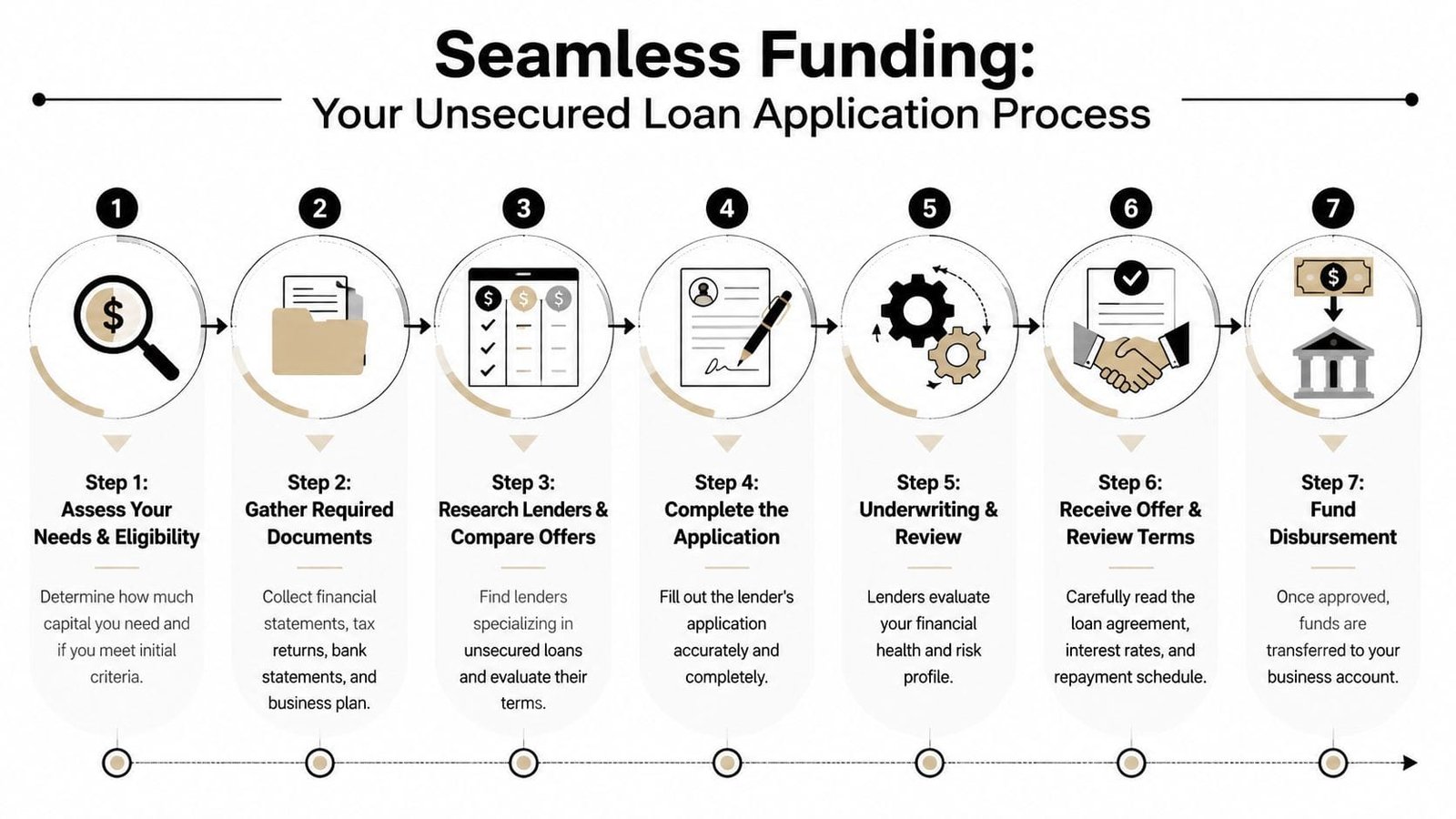

Before you apply

Gather your core file in one place. That usually includes bank statements, tax returns, business financial statements, formation documents, and a short explanation of how you'll use the funds. If ownership structure is complicated, clean that up now, not mid-underwriting.

The best applications also have a short operating narrative. Not a huge deck. Just a clear summary: what the business does, how it makes money, what created the financing need, and why repayment fits the current cash picture.

For a lean overview of what lenders often ask for when speed matters, review this breakdown of the minimal documentation required for a quick small business loan.

The application flow

Most unsecured loan applications move through a familiar sequence:

Initial fit check

You confirm rough eligibility before spending time on a full package.Document submission

Delays begin during document submission if records are incomplete, inconsistent, or spread across multiple systems.Underwriting review

The lender examines cash flow, credit profile, and business stability. Expect follow-up questions.

A short explainer can help if you want to see the process in motion:

Offer stage

You review pricing, repayment structure, fees, and any conditions tied to funding.Acceptance and funding

Once documents are signed and final conditions are met, funds are disbursed.

A few habits improve outcomes:

- Answer quickly: Underwriters like responsive borrowers because responsiveness often correlates with operational discipline.

- Don't overstate projections: Lenders trust realistic numbers more than optimistic ones.

- Be specific about use of funds: Precision reduces friction.

- Read the agreement: If the contract language feels rushed or vague, slow down.

The application is not a test of optimism. It's a test of whether your business records support your story.

Smart Ways to Use and When to Avoid Unsecured Loans

Unsecured business loans work best when they finance speed. They work badly when they finance patience.

Good uses

A strong use case usually has a near-term business purpose and a visible path back to cash.

- Inventory timing: You can buy stock ahead of demand or take advantage of a supplier opportunity without pledging equipment.

- Marketing with a clear runway: If you're funding a campaign tied to a launch, season, or proven offer, short-term capital can make sense.

- Payroll or receivables gap: When customers pay slowly but operations can't wait, unsecured funding can bridge the gap.

- Hiring for immediate revenue capacity: Bringing on key staff can justify financing if the role supports booked demand, not just hope.

Bad uses and better alternatives

Avoid unsecured debt for long-lived assets or projects with delayed payoff. Buying real estate, major equipment, or funding a broad strategic expansion with expensive short-term money can put unnecessary strain on the business.

In those cases, a secured loan, SBA structure, or equipment financing product often fits better. And if your need is recurring rather than one-time, a line of credit may be a better operational tool than a lump-sum loan.

If you're comparing multiple quick-capital options, this guide to short-term loans, merchant cash advances, and invoice factoring is useful because it matches products to problems instead of treating all fast funding the same.

The rule is simple. If the funds produce value quickly, unsecured borrowing can be smart. If the payoff takes a long time, the financing structure is probably wrong.

Frequently Asked Questions About Unsecured Loans

Can I get an unsecured business loan without perfect credit

You don't need perfection, but you do need a credible profile. Lenders want to see that the business and the owner can handle debt responsibly. If your file is uneven, strong cash flow and clean documentation help. If both credit and cash flow are weak, approval gets much harder.

Are unsecured business loans always faster

They are often faster because there is no collateral appraisal or asset lien process. But speed still depends on your readiness. A lender can't move quickly through a messy file.

Do these loans require a specific use of funds

Usually, the use is flexible. That's one of the attractions. But lenders still want to understand the purpose because it helps them judge repayment risk.

Is no collateral the same as no personal risk

No. Even when no business asset is pledged, owners may still face contractual obligations and credit consequences if the business can't repay. Read the agreement carefully and don't assume "unsecured" means consequence-free.

What's the biggest mistake borrowers make

Using short-term unsecured debt for a slow-return project. The structure has to match the business objective. Good financing solves a timing problem. Bad financing creates a new one.

If you're weighing funding options and want a faster way to compare what fits your business, Business Loan Warrior is a practical place to start. You can explore specific funding paths, review financing types for different business needs, and move toward pre-approval without turning the process into a second full-time job.